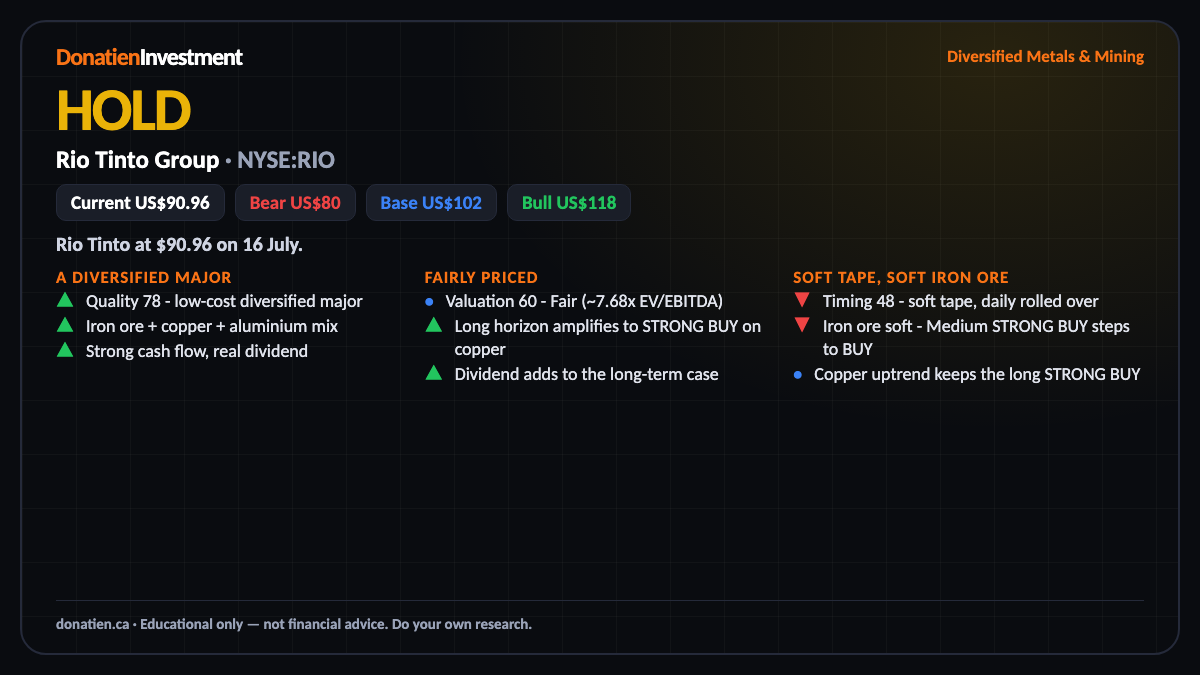

Rio Tinto Group (NYSE:RIO) HOLD

A cheap, diversified miner, but a soft tape and rolling iron ore mean wait - a hold now, with copper's structural case carrying the long term.

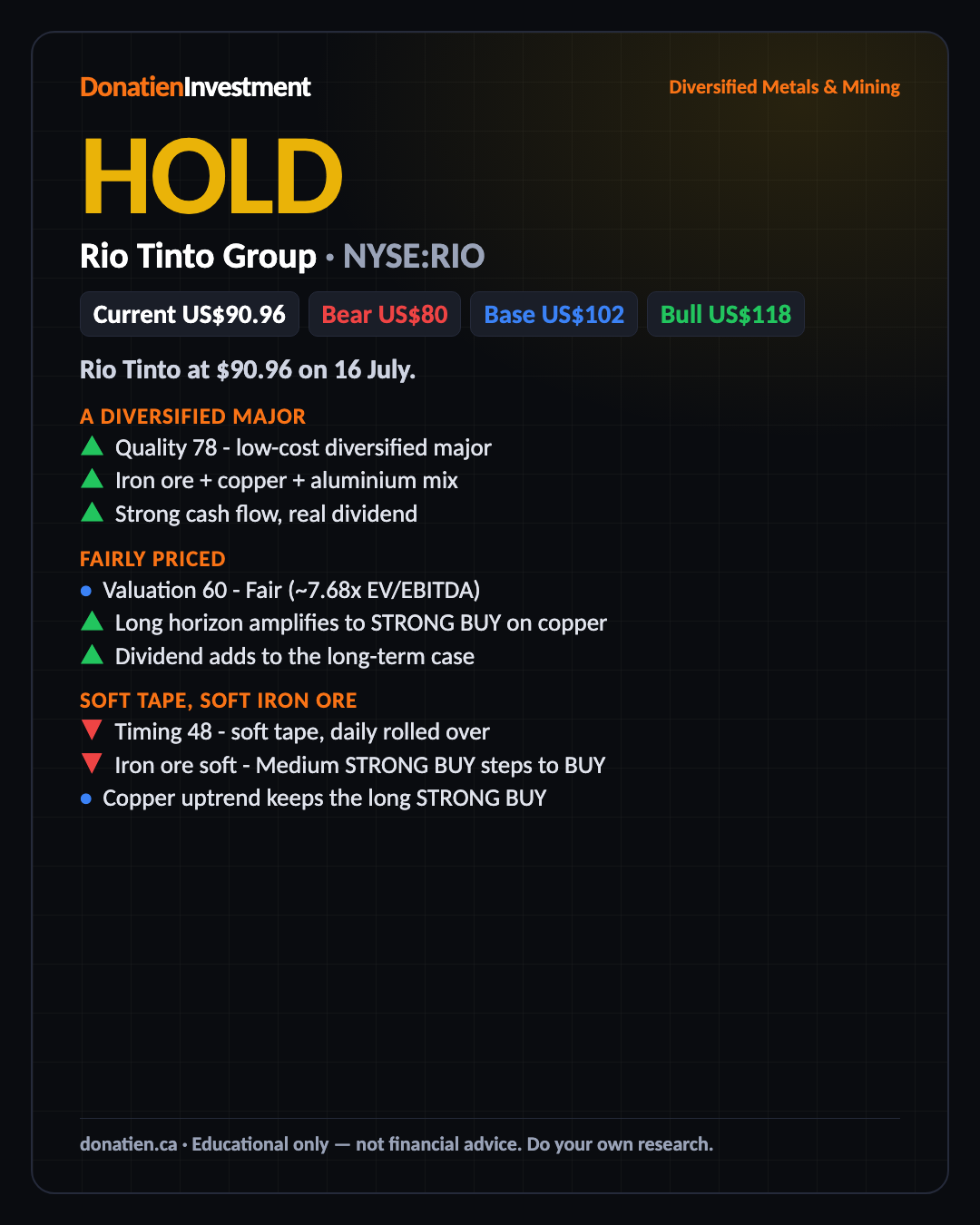

Rio Tinto at $90.96 on 16 July. Short-term Hold: the tape is weak and iron ore is soft, so the timing is not there - though the long-term copper case stays Strong Buy.

A diversified major

Rio Tinto scores 78 on quality, a low-cost, diversified major in iron ore, copper and aluminium. That spread of commodities smooths the cycle and funds a real dividend. It is a solid, cash-generative business. As with the miners, the question is the commodities and the tape, not the company.

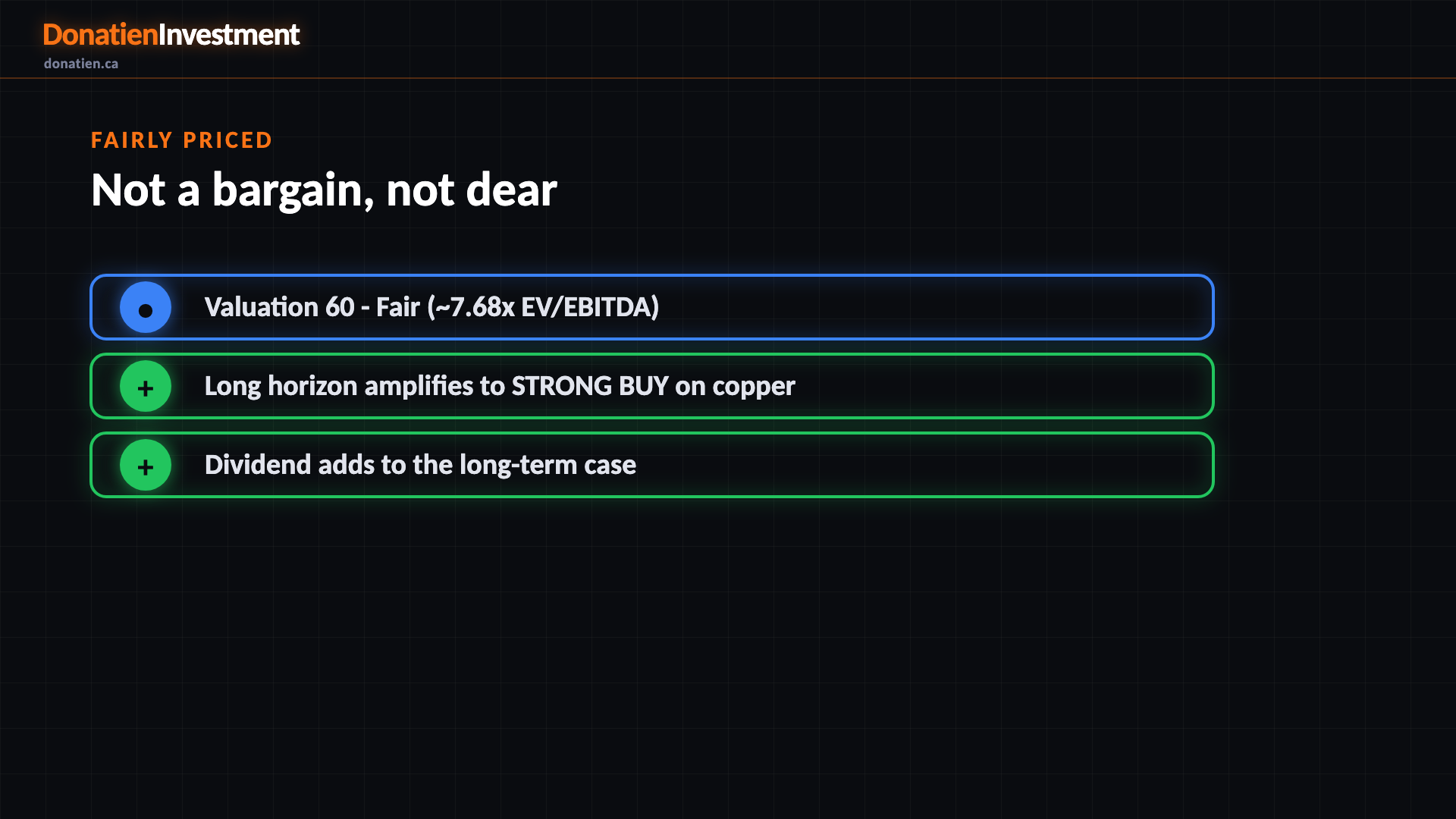

Fairly priced

Valuation is fair at 60, near 7.68 times EV/EBITDA. Reasonable for a cyclical major, not a bargain. On the structural copper-deficit thesis the long-term call still amplifies to Strong Buy, and the dividend adds to that long-term case. Fair value plus a structural driver makes this one to accumulate patiently, not chase.

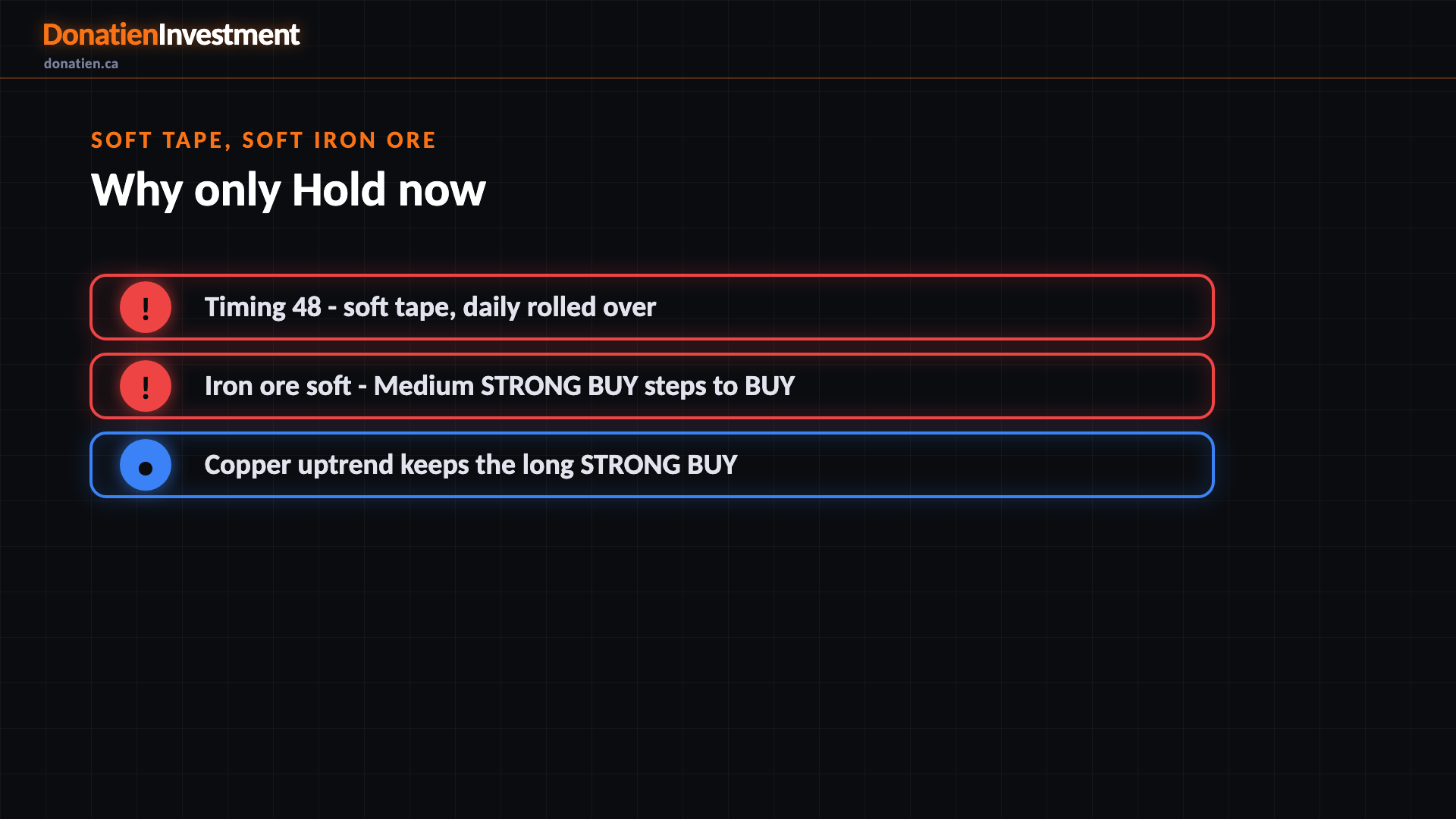

Soft tape, soft iron ore

The catch is the tape and iron ore, both soft. The daily trend has rolled over below its averages. Iron ore, still Rio biggest earner, is soft rather than in a clean uptrend, so the medium-term call steps back from Strong Buy to Buy. Copper, in a genuine uptrend, is what keeps the long horizon at Strong Buy. Short-term, wait for confirmation.

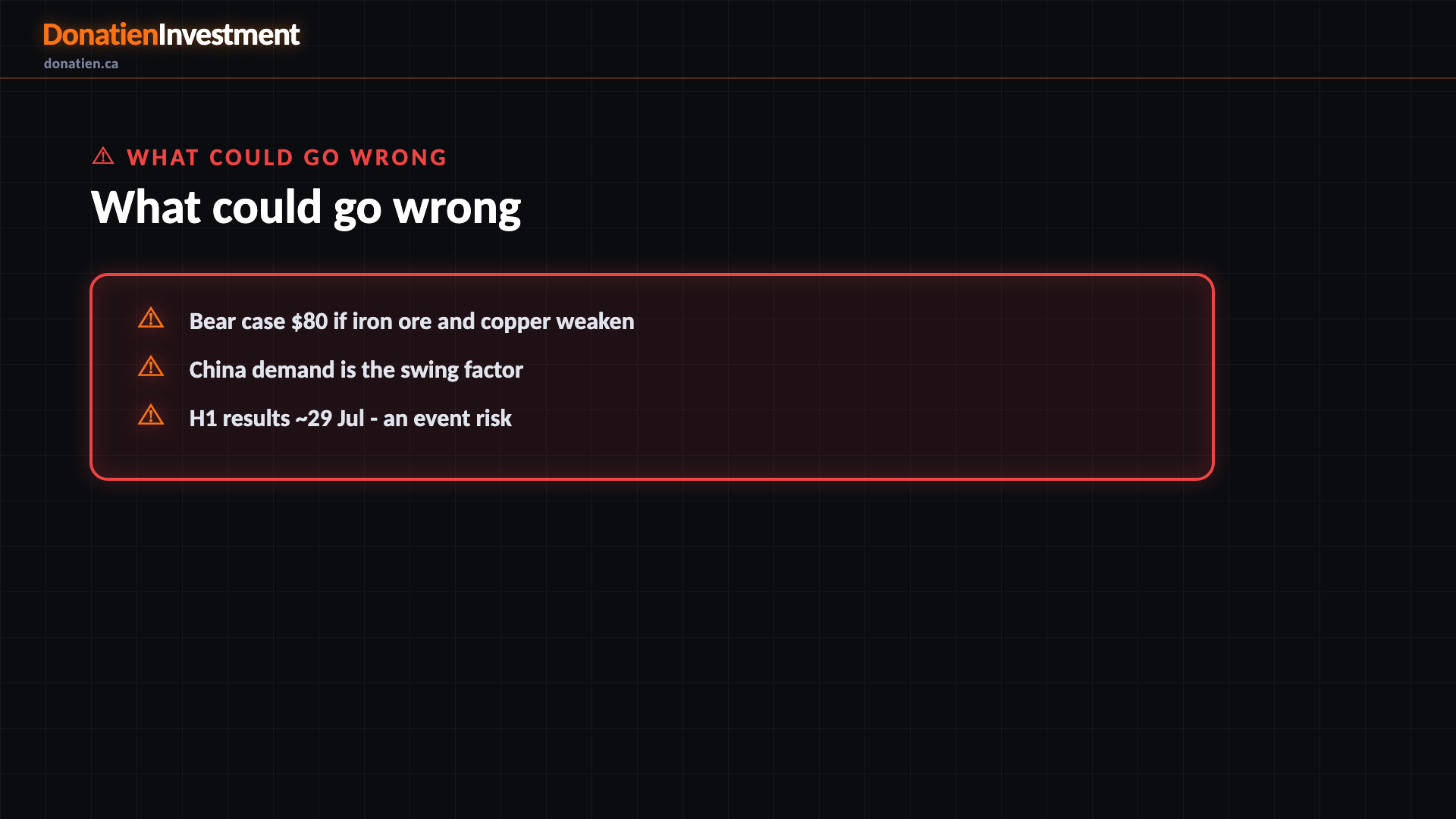

What could go wrong

The risk is cyclical and macro. Iron ore and copper swing with China and global growth, and the bear case sits near 80, below today price. H1 results land around 29 July, a near-term event. Hold is the honest read - own the quality and the copper optionality for the long term, but wait for the tape and iron ore to firm; base 102, bull 118.

Risk vs Reward

Against the current US$90.96, the report frames a bull case at US$118 (+30%), a base case at US$102 (+12%) and a bear case at US$80 (-12%). See the full report for the probability weight behind each path.

The verdict

A cheap, diversified miner, but a soft tape and rolling iron ore mean wait - a hold now, with copper's structural case carrying the long term.

Read the full report on donatien.ca →{kind=link}

{kind=link}