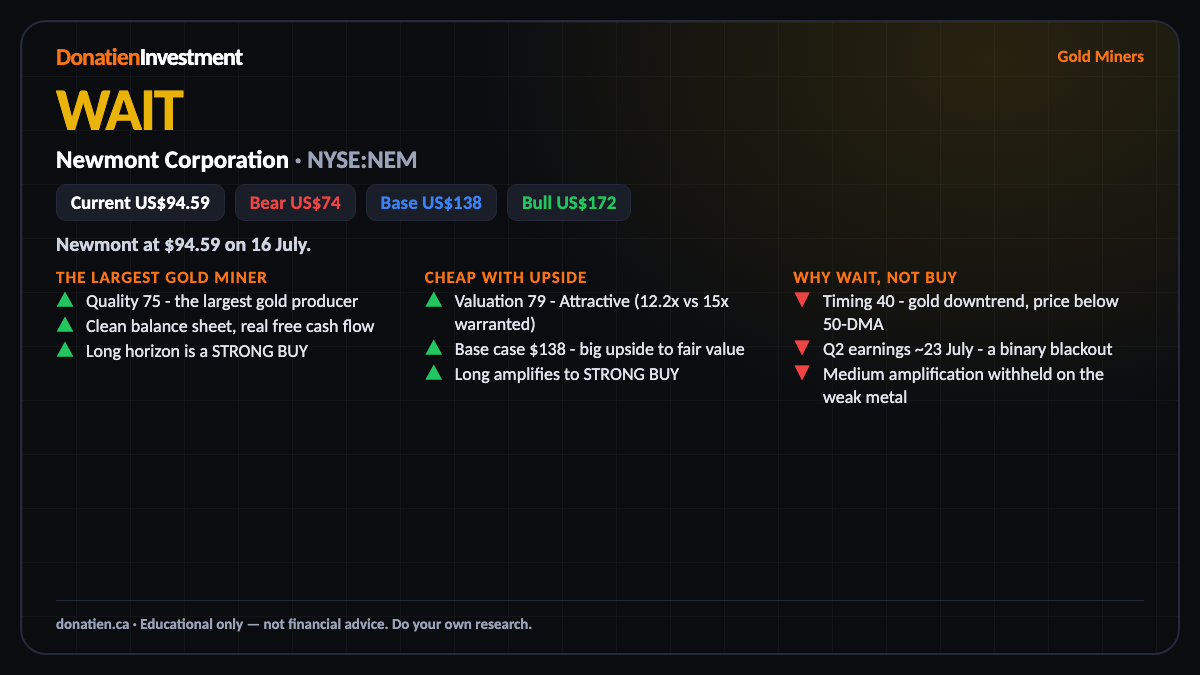

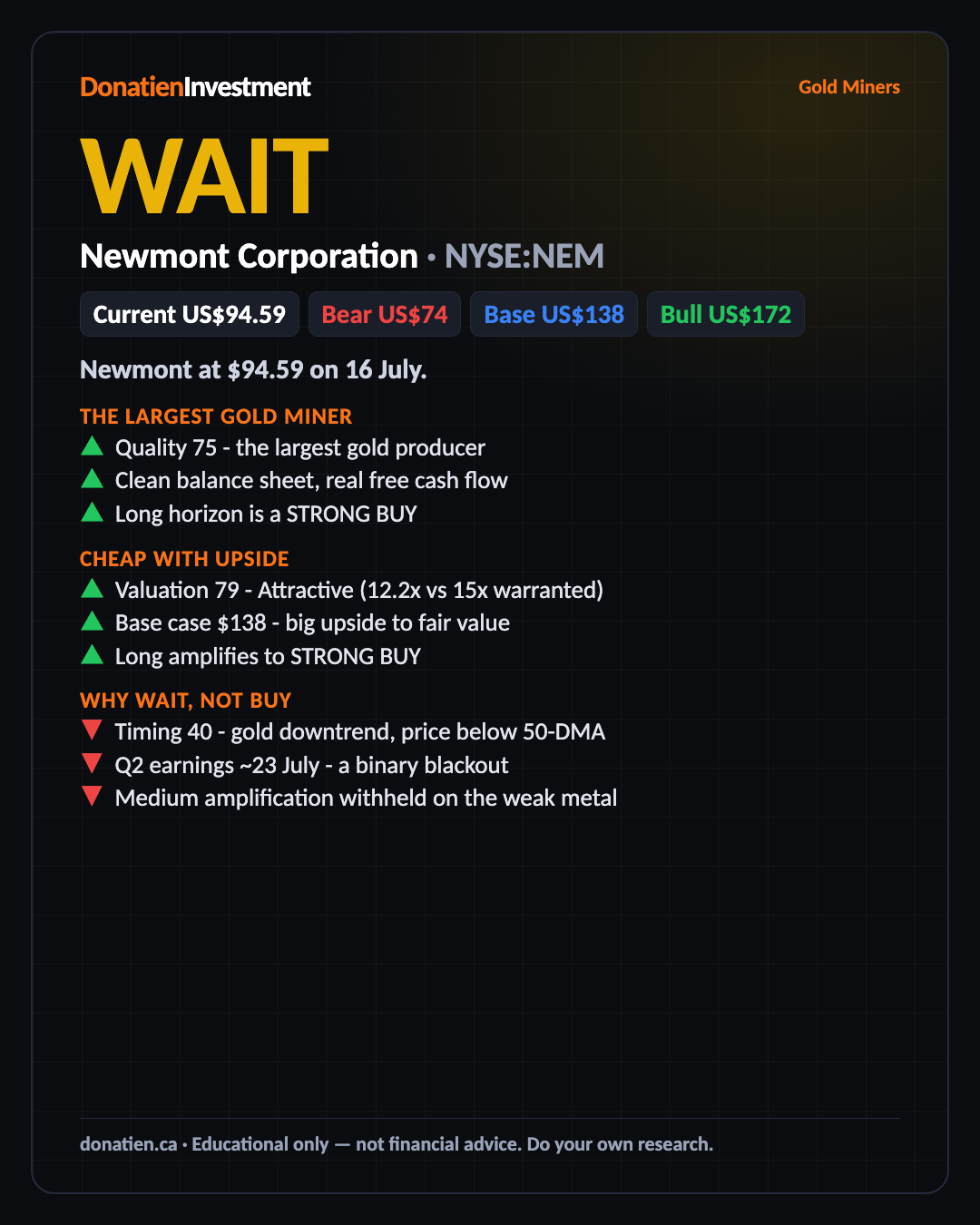

Newmont Corporation (NYSE:NEM) WAIT

An elite, cheap gold miner with real upside - but gold is falling and earnings loom, so wait for the entry rather than chase it now.

Newmont at $94.59 on 16 July. Short-term Wait: the valuation is attractive and the long-term call is Strong Buy, but a falling gold price and imminent earnings mean there is no entry edge yet.

The largest gold miner

Newmont scores 75 on quality, the world largest gold producer, with clean earnings and a solid balance sheet. It throws off real free cash flow across a big, diversified asset base. On the structural gold thesis the long-term call is a Strong Buy. As with the others, the debate here is the metal and the timing, not the company.

Cheap with upside

The valuation is genuinely attractive at 79. On clean earnings it trades near 12.2 times against a warranted 15, and the base case at 138 implies real upside from 94.59. That discount plus the structural driver is what carries the medium Buy and amplifies the long-term call to Strong Buy. The value is here; what is missing is a reason to act this week.

Why Wait, not Buy

So why Wait, not Buy? Gold is in a downtrend, and Newmont trades below its 50-day average. On top of that, Q2 earnings land around 23 July, a binary event you do not want to buy into blind. Because the metal is weak, we also hold the medium call at Buy rather than amplifying it. No entry edge yet - wait.

What could go wrong

The risk is the metal and the print. Gold below a falling average is a live downtrend; bear case near 74. Q2 earnings on 23 July add a binary event. Wait is the honest read - do not chase it into a falling metal and an earnings blackout; base 138, bull 172.

Risk vs Reward

Against the current US$94.59, the report frames a bull case at US$172 (+82%), a base case at US$138 (+46%) and a bear case at US$74 (-22%). See the full report for the probability weight behind each path.

The verdict

An elite, cheap gold miner with real upside - but gold is falling and earnings loom, so wait for the entry rather than chase it now.

Read the full report on donatien.ca →{kind=link}

{kind=link}