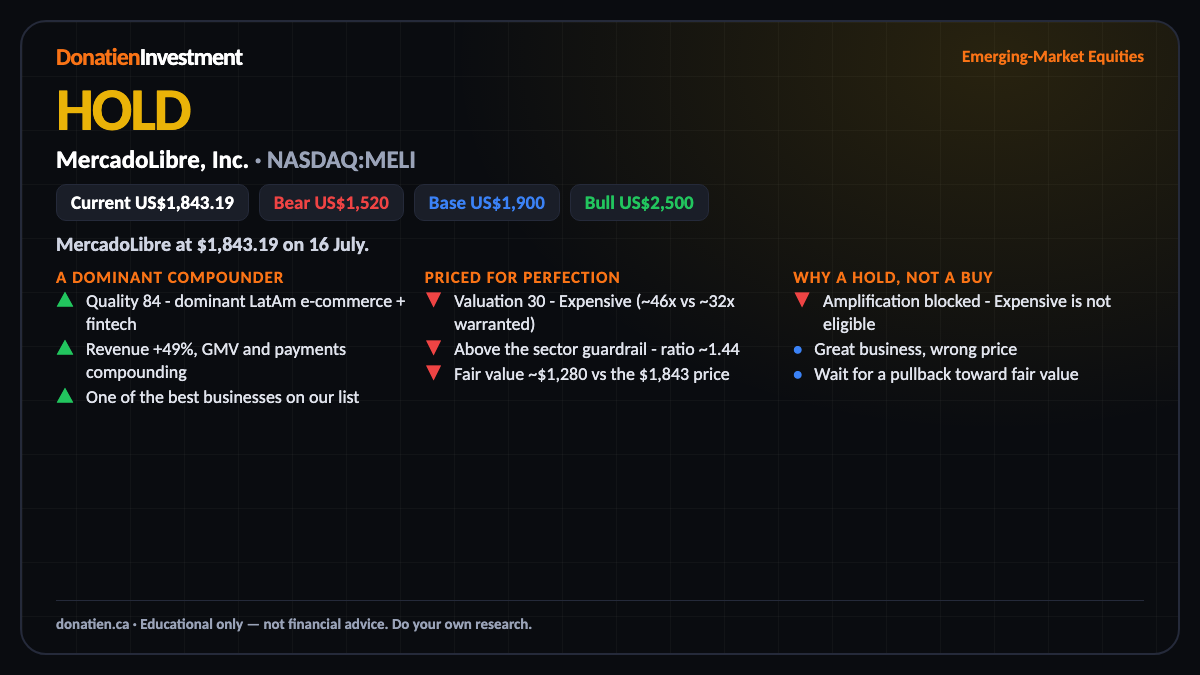

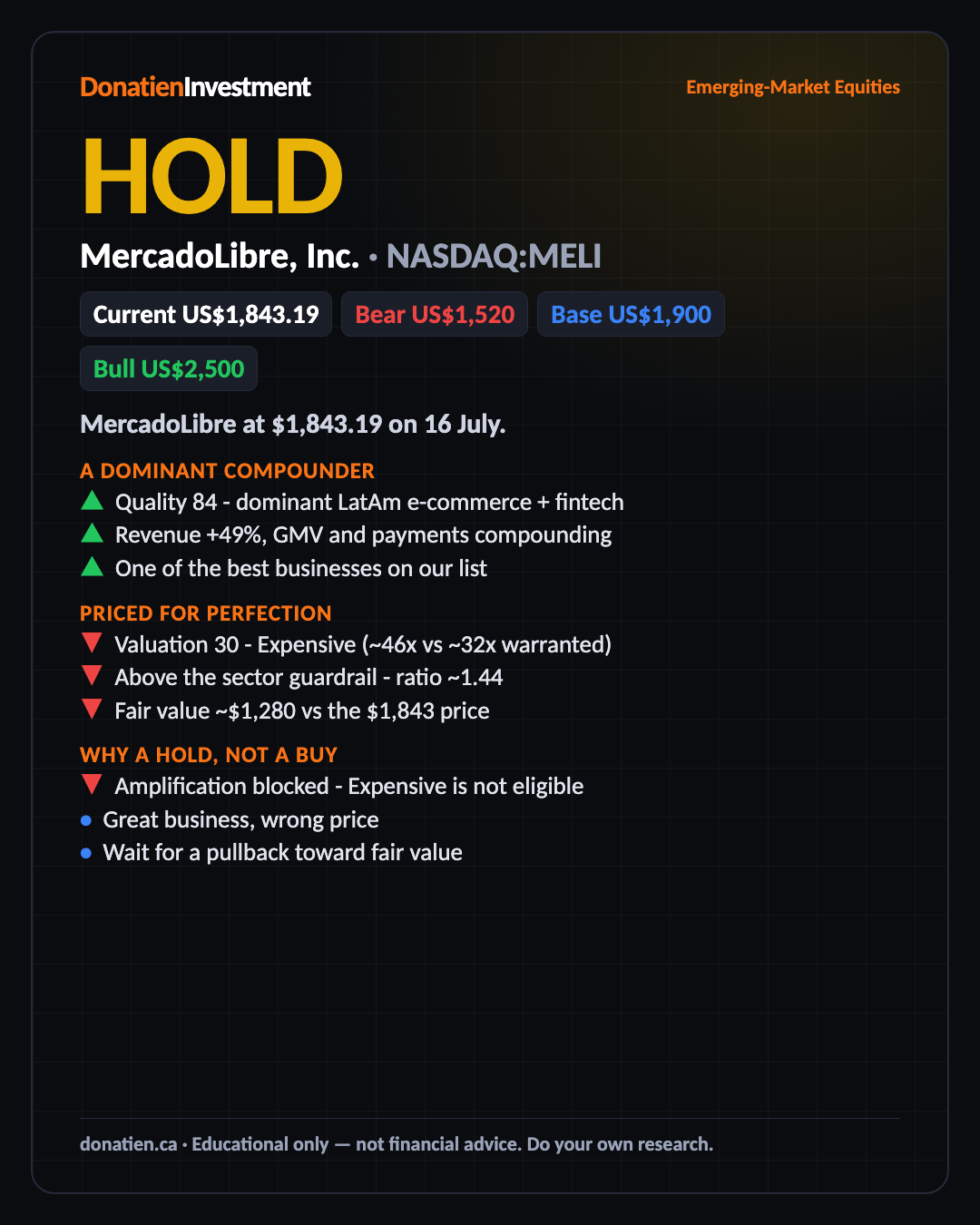

MercadoLibre, Inc. (NASDAQ:MELI) HOLD

A superb LatAm compounder priced for perfection - expensive on every measure, so a hold until the price comes to you.

MercadoLibre at $1,843.19 on 16 July. A Hold on all horizons: the business is elite, but near 46 times clean earnings it is expensive, and the framework will not chase it.

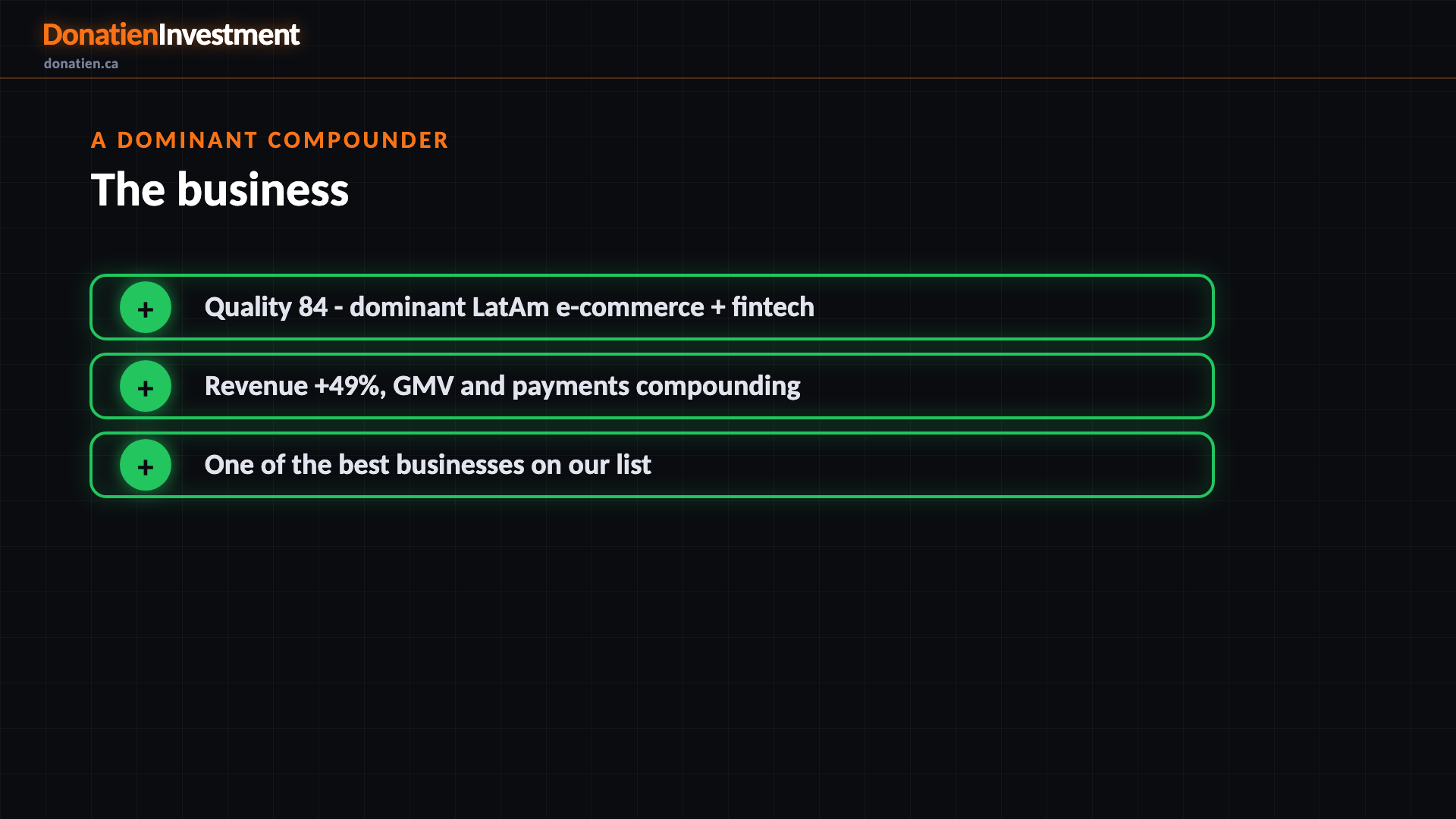

A dominant compounder

MercadoLibre scores 84 on quality, a dominant LatAm e-commerce and fintech flywheel. Revenue grew 49 percent last quarter. Its marketplace, payments and credit arms reinforce each other, and it keeps taking share. This is one of the best businesses we cover - which is the trap, because a great company is not a great investment at any price.

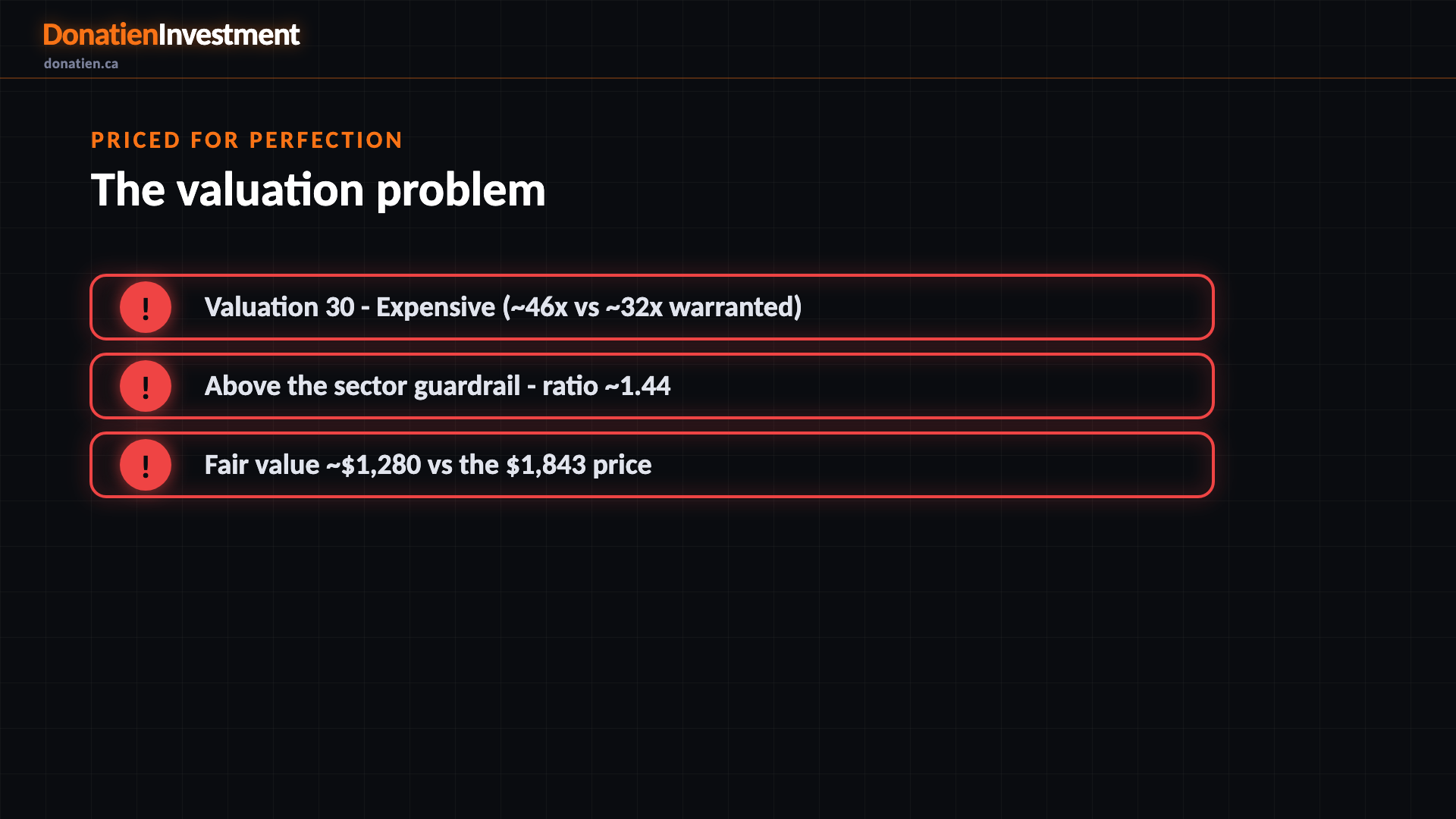

Priced for perfection

The price is the problem: valuation scores just 30. On clean earnings it trades near 46 times against a warranted 32 - a ratio around 1.44, into the expensive band and above the sector guardrail. Our fair value sits near 1,280, well below the 1,843 quote. You are paying today for years of flawless execution.

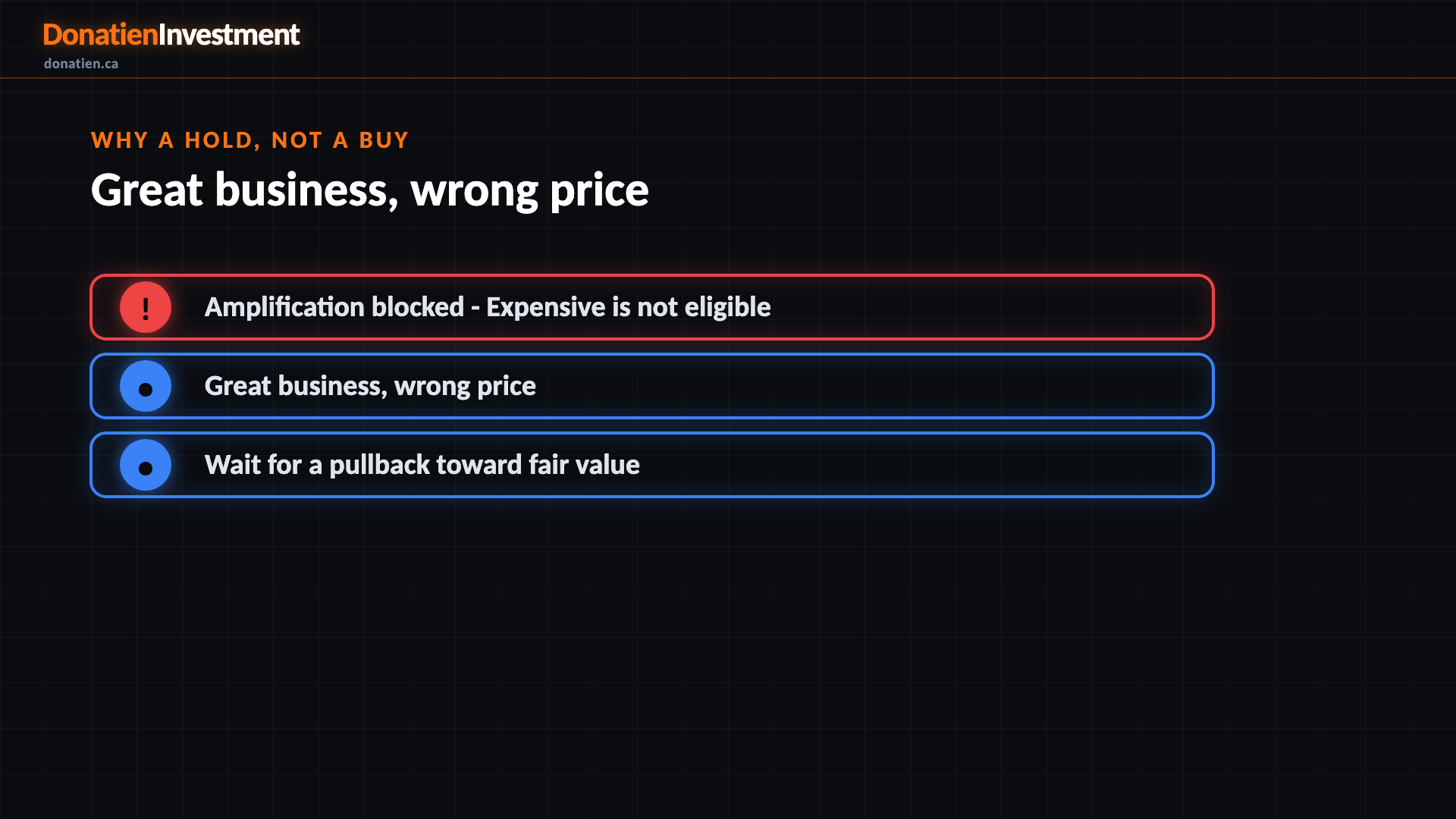

Why a Hold, not a Buy

So even a business this good is a Hold here. The valuation is Expensive, so the driver cannot amplify it. This is the discipline the framework exists for - refusing to chase a wonderful company at a full price. Wait for a pullback toward fair value, and it becomes interesting again.

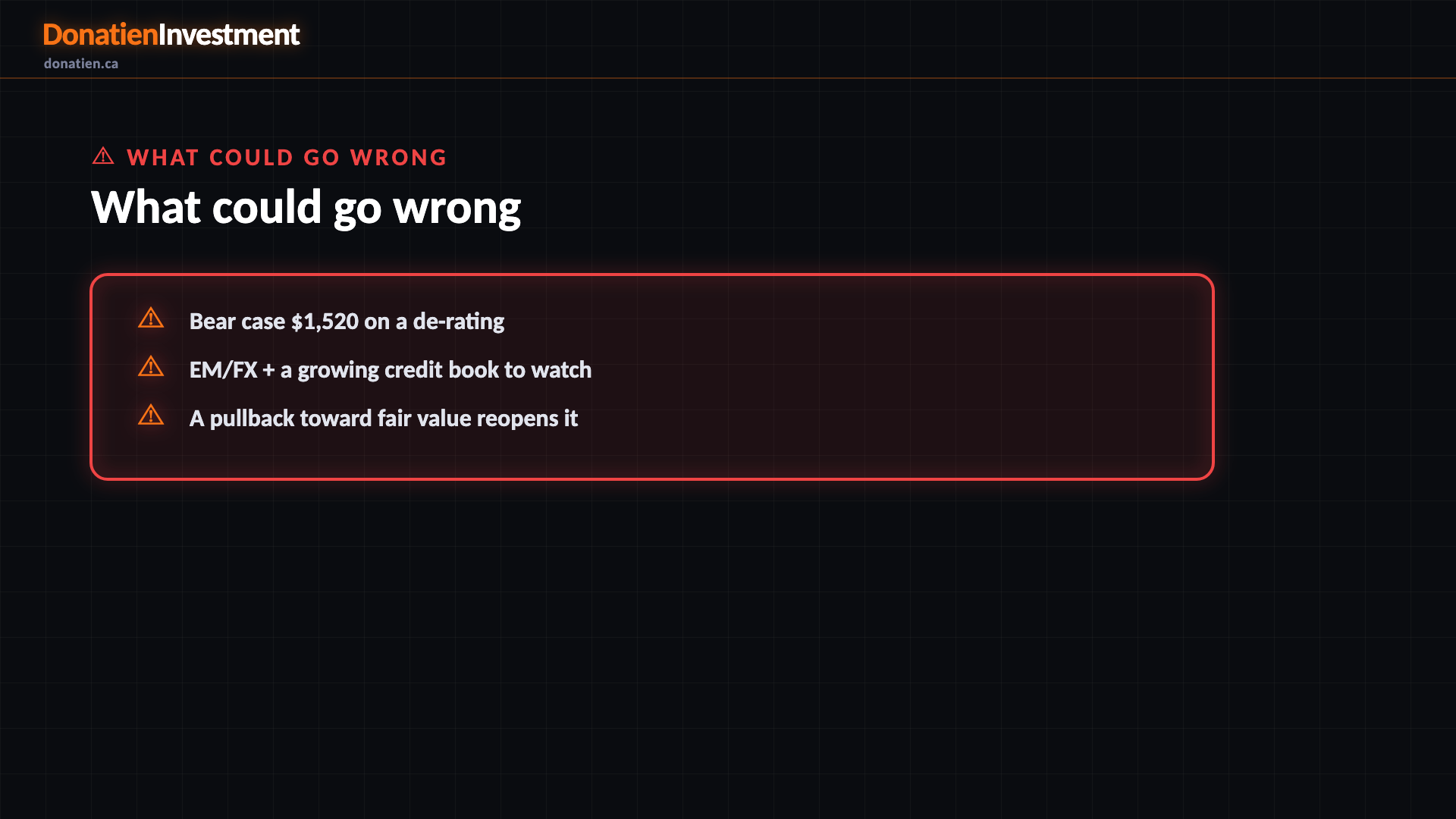

What could go wrong

The risk is two-sided. Pay up here and a de-rating bites; the bear case sits near 1,520. But a strong print could keep it expensive and leave a patient buyer behind, with a base of 1,900 and a bull of 2,500. There is also EM currency risk and a growing credit book. Hold is the honest read: wait for the price to come to you.

Risk vs Reward

Against the current US$1,843.19, the report frames a bull case at US$2,500 (+36%), a base case at US$1,900 (+3%) and a bear case at US$1,520 (-18%). See the full report for the probability weight behind each path.

The verdict

A superb LatAm compounder priced for perfection - expensive on every measure, so a hold until the price comes to you.

Read the full report on donatien.ca →{kind=link}

{kind=link}