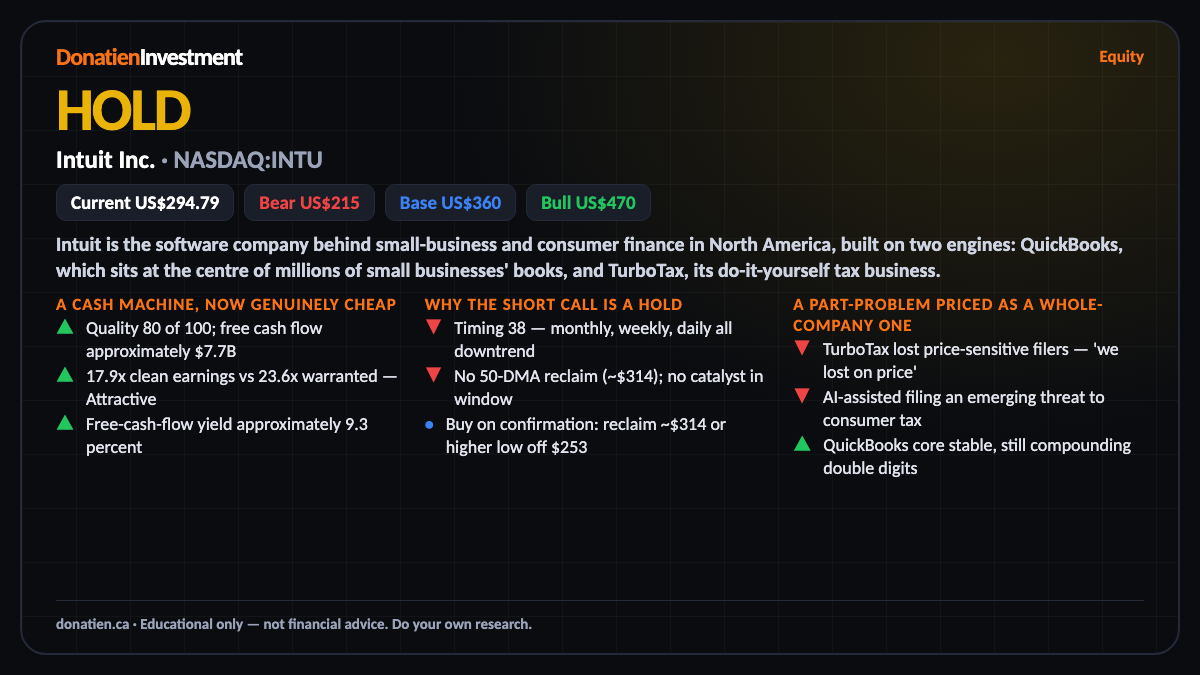

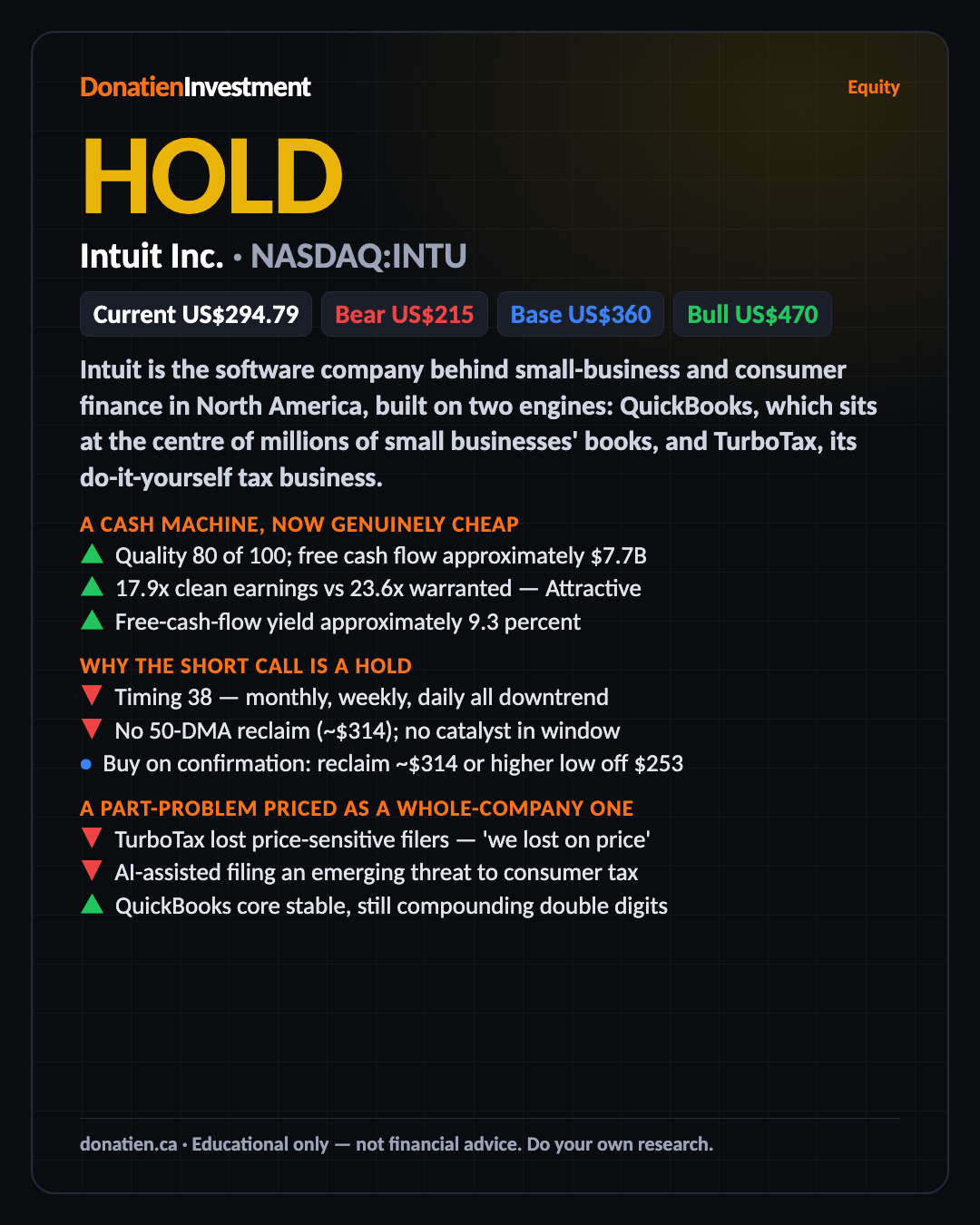

Intuit Inc. (NASDAQ:INTU) HOLD

Intuit has fallen roughly 60 percent from its high and is now genuinely cheap for its quality, which is why the medium and long calls are both BUY, accumulate. But the short-term call is HOLD: the monthly, weekly and daily trends are all still down, there is no confirmed entry, so the near-term stance is buy on confirmation, accumulate on weakness.

Intuit is the software company behind small-business and consumer finance in North America, built on two engines: QuickBooks, which sits at the centre of millions of small businesses' books, and TurboTax, its do-it-yourself tax business. A weak tax season and a pricing miss on TurboTax have taken the stock down about 60 percent from its high. The report rates it HOLD short-term, BUY accumulate medium and long, at a price of 294.79 US dollars as of the 16th of July 2026.

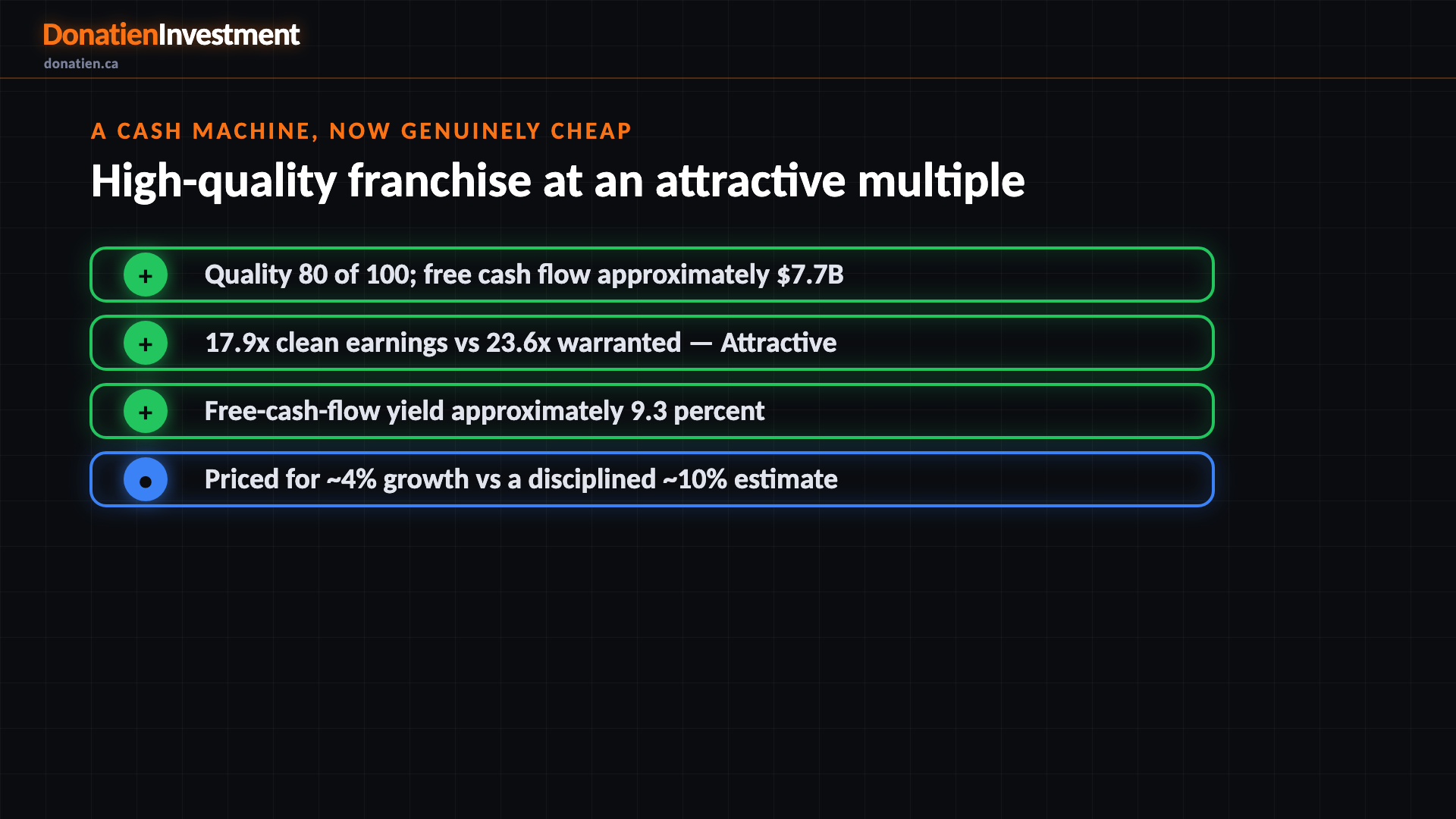

A cash machine, now genuinely cheap

The quality here is real. Intuit runs an 81 percent gross margin, throws off about 7.7 billion US dollars of free cash flow a year, and holds a fortress balance sheet. Its QuickBooks franchise is deeply entrenched, because switching away means re-plumbing a whole company's books. On valuation, the shares trade at about 17.9 times clean earnings against a warranted multiple of 23.6, a ratio of 0.76 that sits firmly in the attractive band. The free-cash-flow yield is about 9.3 percent. The market is pricing it as if growth slows to roughly 4 percent, well below what the business has delivered.

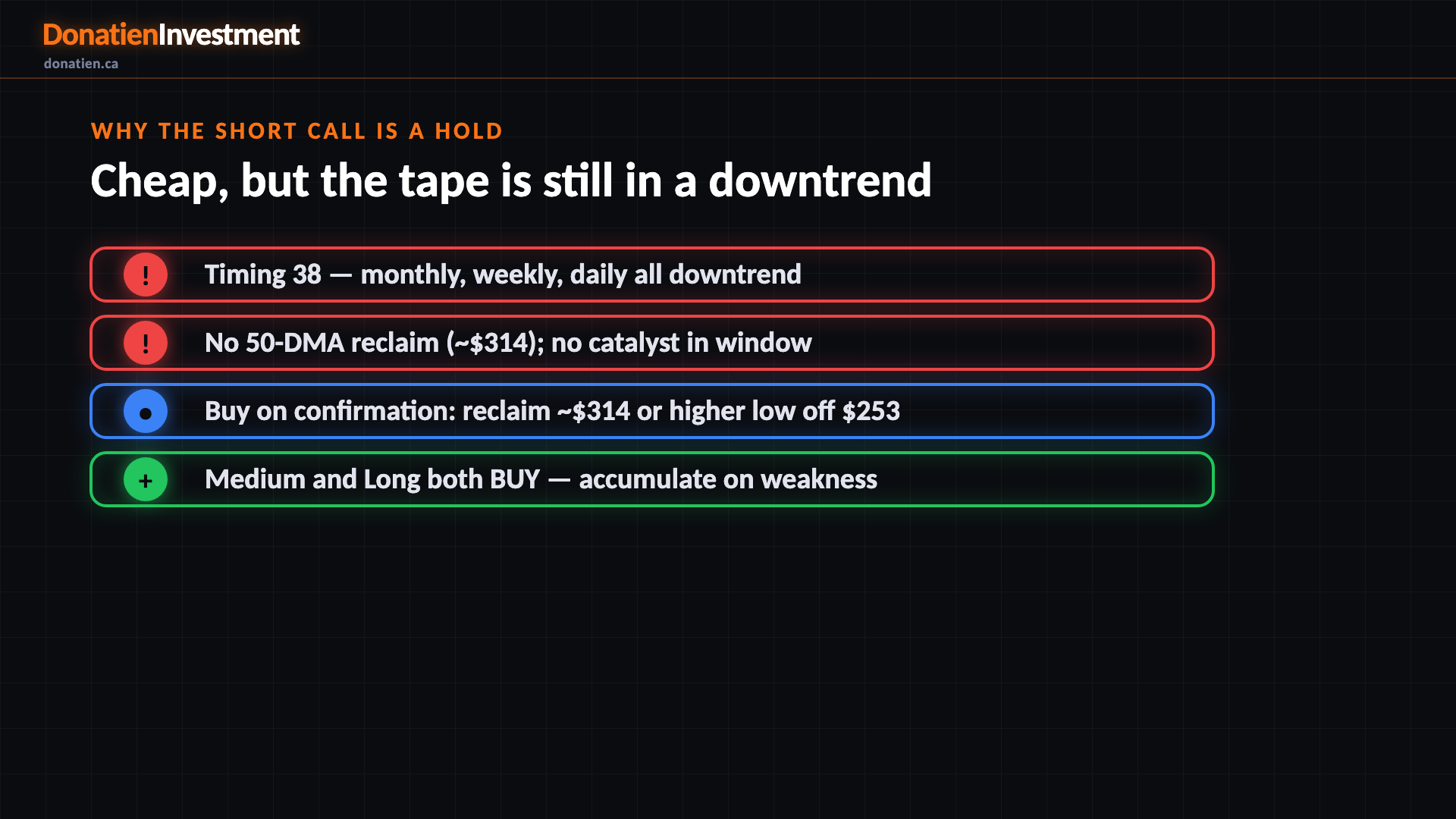

Why the short call is a hold

So why not buy today. The near-term tape gives no confirmed entry. The monthly, weekly and daily trends are all down after a roughly 60 percent decline, and today's bounce is only an intraday attempt, not a trend change. The stock has not reclaimed its 50-day average near 314, and there is no catalyst inside the window. The fundamental case is met, the stock is cheap, but with neither technical nor catalyst confirmation the timing score is just 38 and the short horizon is capped to hold. Buy on confirmation: a daily reclaim of about 314, or a confirmed higher low off the 253 area.

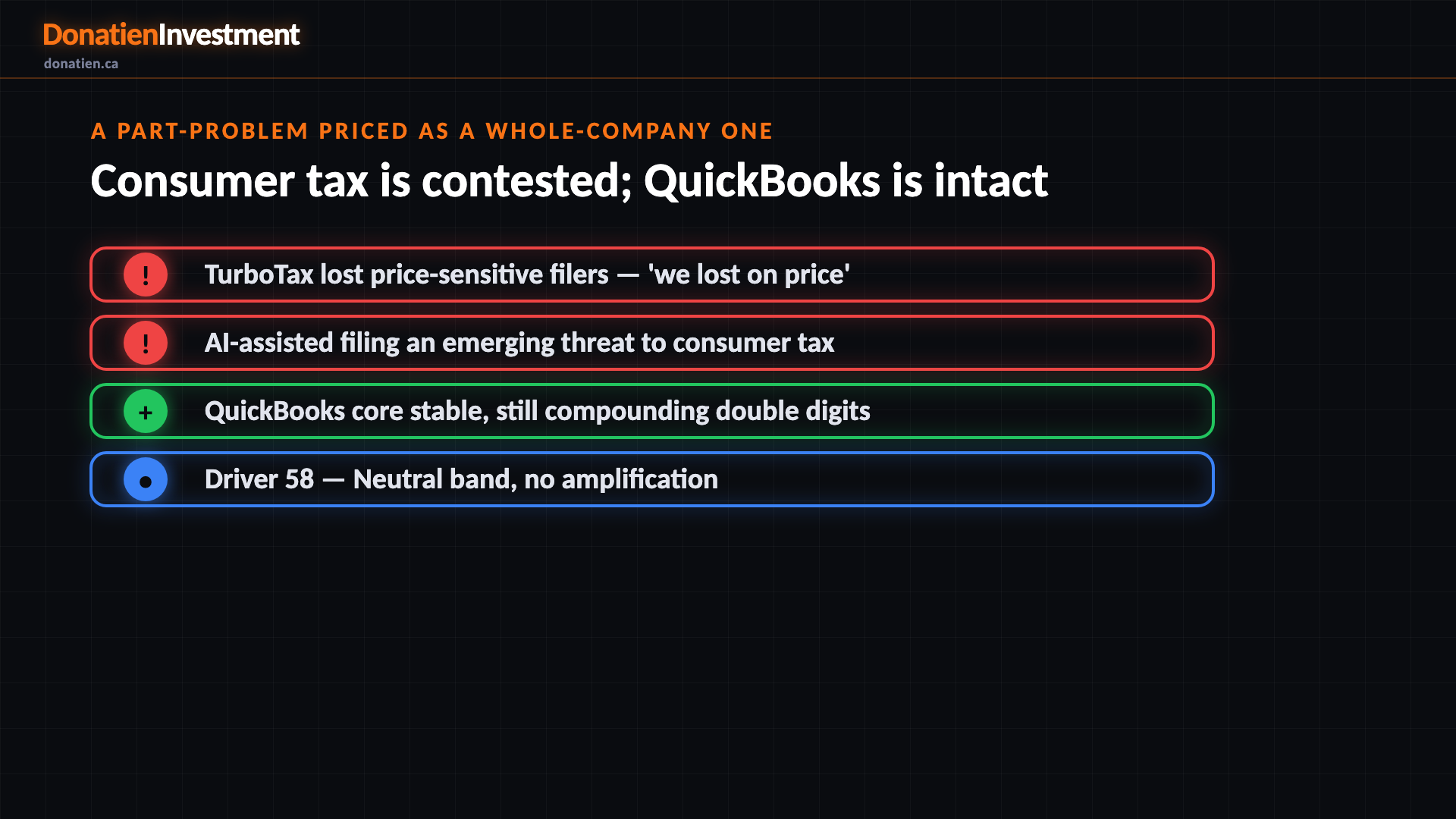

A part-problem priced as a whole-company one

The decline is a competitive story, not a balance-sheet one. On the 20 May earnings call management said flatly, we lost on price: TurboTax shed price-sensitive do-it-yourself filers, the low-end filer pool is shrinking, and AI-assisted filing is an emerging threat. That is the live pressure. But it hits the Consumer segment, while the larger, stickier QuickBooks engine keeps compounding double digits. The whole investment case is that the market has re-priced the entire company for a threat that mainly hits part of it. The driver score of 58 sits in the neutral band, so it does not amplify the signal — the report does not manufacture a stronger buy.

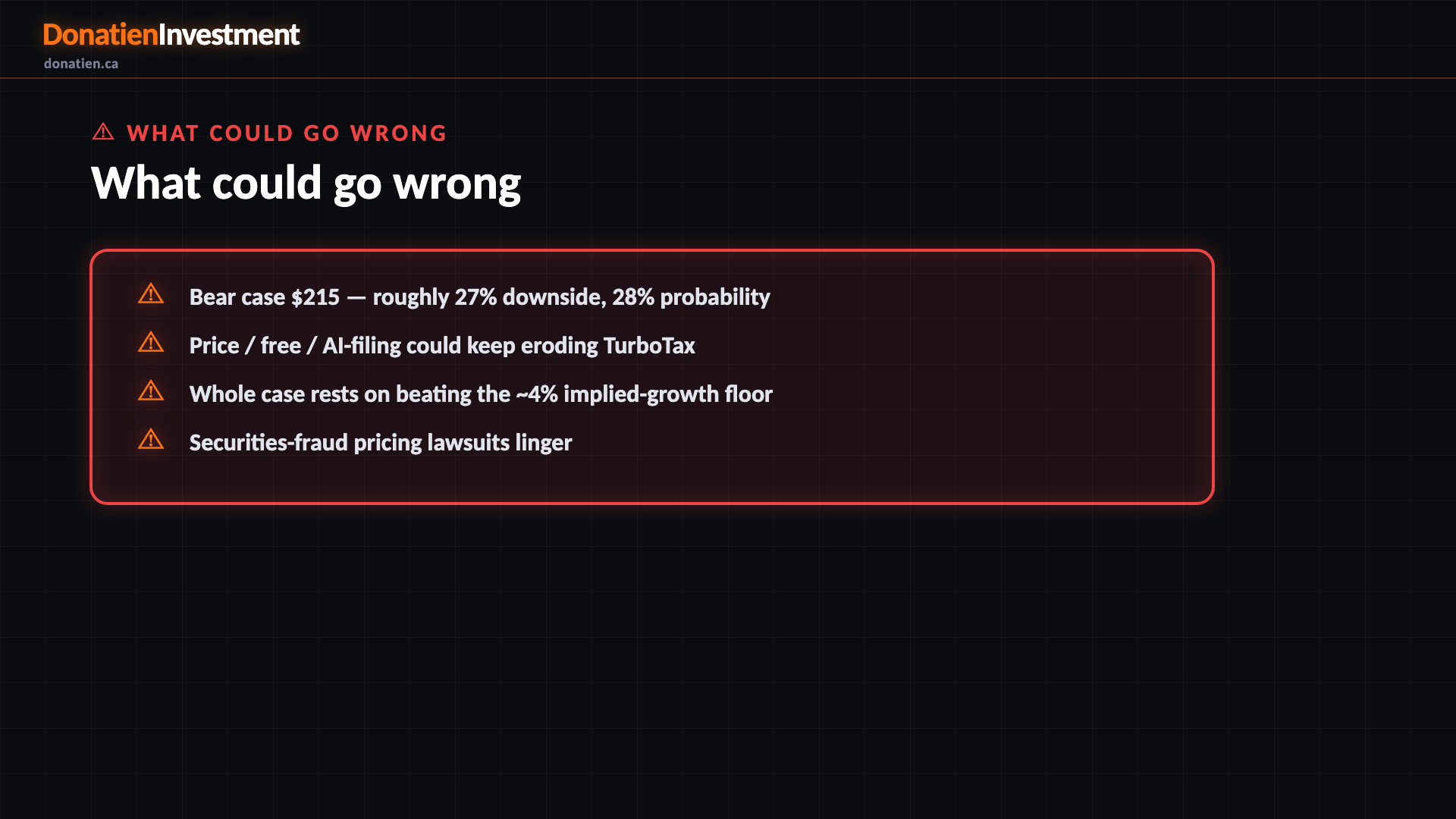

What could go wrong

The risks are competitive, and they are live, not a distant tail. The bear case sees the stock fall to about 215 US dollars, roughly 27 percent below today, at a 28 percent probability. That would take the price competition and low-end filer contraction spreading, AI-assisted filing eroding TurboTax further, and Mailchimp keeping losing ground, so group growth compresses toward the 4 percent the price already implies. The securities-fraud pricing lawsuits linger. And the whole attractive call rests on Intuit beating that 4 percent floor. The 20 August earnings print is the read on whether the QuickBooks core is intact. This is a real risk, not a tail.

Risk vs Reward

The base case is 360 US dollars at 50 percent — the growth scare fades but does not reverse, QuickBooks stays resilient, and cash generation plus buybacks do the heavy lifting, about 22 percent above spot. The bull case is 470 US dollars at 22 percent if the TurboTax miss proves a one-off and Intuit's AI layer re-accelerates growth. The bear case is 215 US dollars at 28 percent if the competitive pressure spreads. The probability-weighted centre of gravity is the base case.

The verdict

The honest read is a hold now, a buy later. Intuit is a genuine cash-machine franchise, and after a 60 percent fall it is cheap for the quality, which is why the medium and long calls are both buy, accumulate. But the short-term stance is hold: the tape is still in a downtrend, there is no confirmed entry, and the 20 August print is the near-term read on the core. The plan is to accumulate on weakness or buy on confirmation, not to catch a falling knife. This is analysis, not financial advice.

Analysis, not financial advice. Financial Freedom. Together.

Read the full report on donatien.ca →{kind=link}

{kind=link}