Intact Financial Corporation (TSX:IFC) HOLD

A quality Canadian insurer riding higher-for-longer, but the breakout to a new high came on thin volume - a hold now, buy on confirmation.

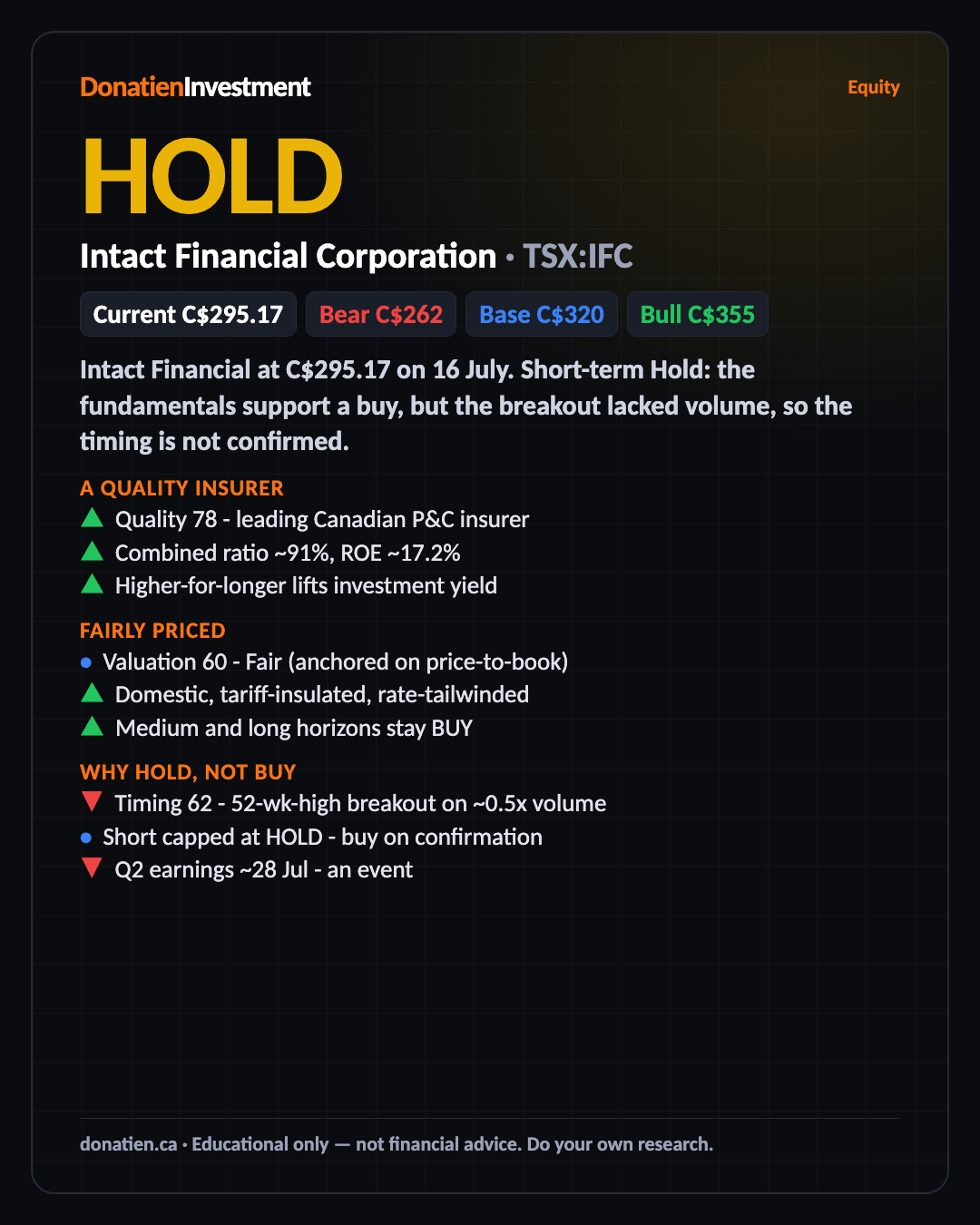

Intact Financial at C$295.17 on 16 July. Short-term Hold: the fundamentals support a buy, but the breakout lacked volume, so the timing is not confirmed. Medium and long stay Buy.

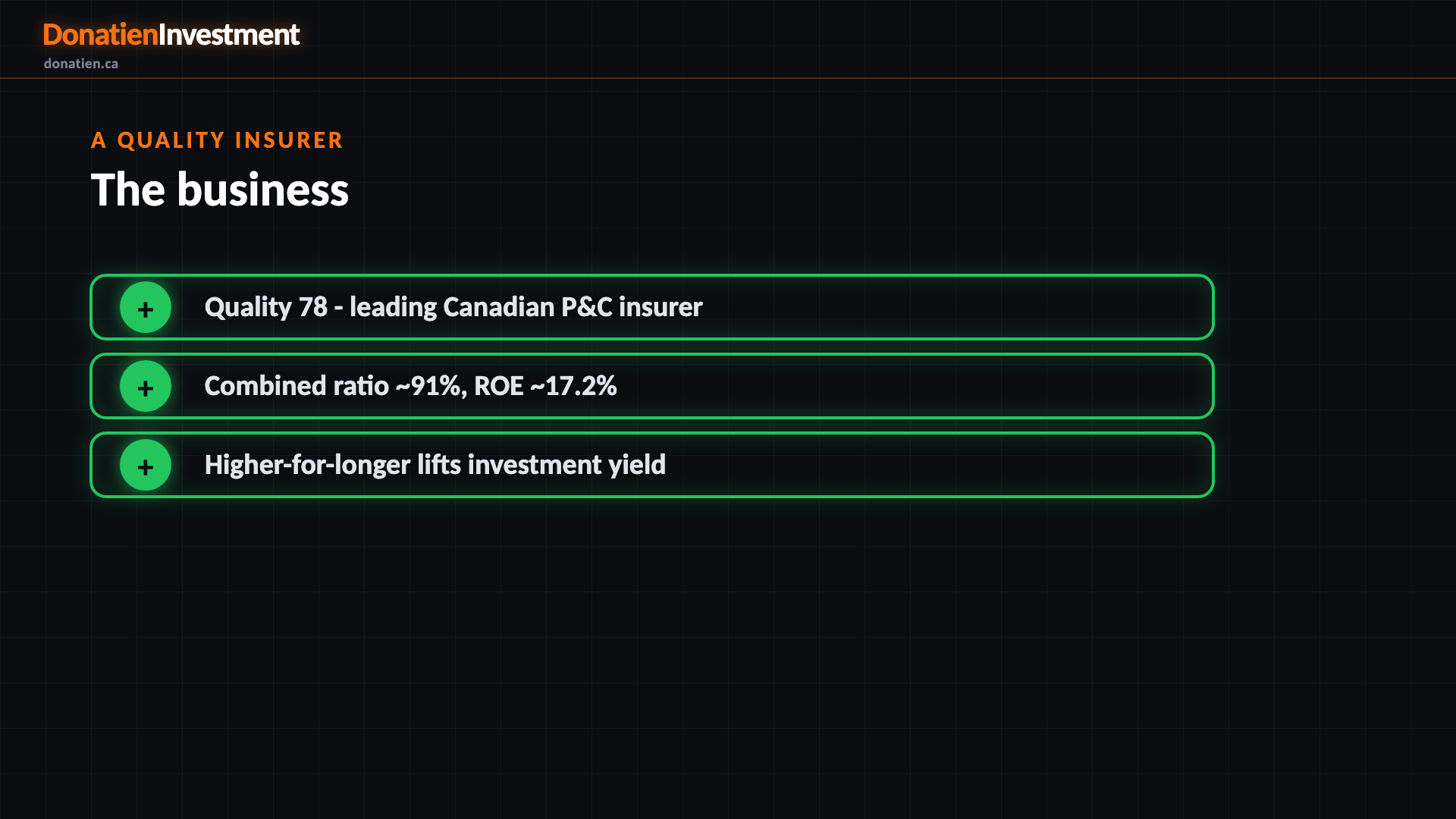

A quality insurer

Intact scores 78 on quality, Canada leading P&C insurer. Combined ratio near 91 percent, return on equity around 17.2. Higher-for-longer rates lift the yield it earns on its float, and it is domestic and tariff-insulated. A good defensive compounder - the hold is about the entry, not the business.

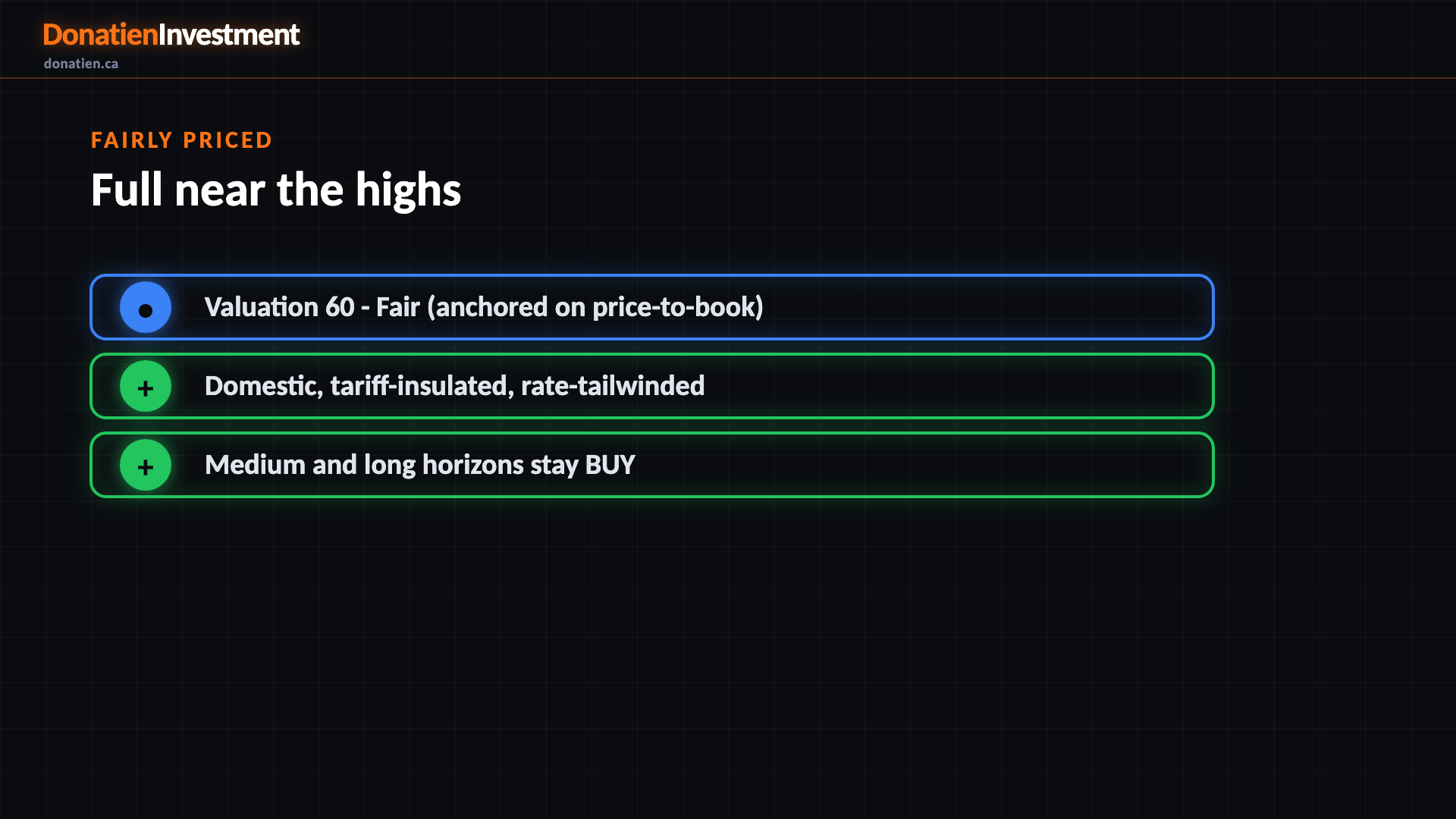

Fairly priced

Valuation is fair at 60. On price-to-book it is attractive, but pulled to fair by a full price near its highs. The business economics still support the medium and long-term Buy. So the case is intact; it is the near-term entry that is not compelling right here.

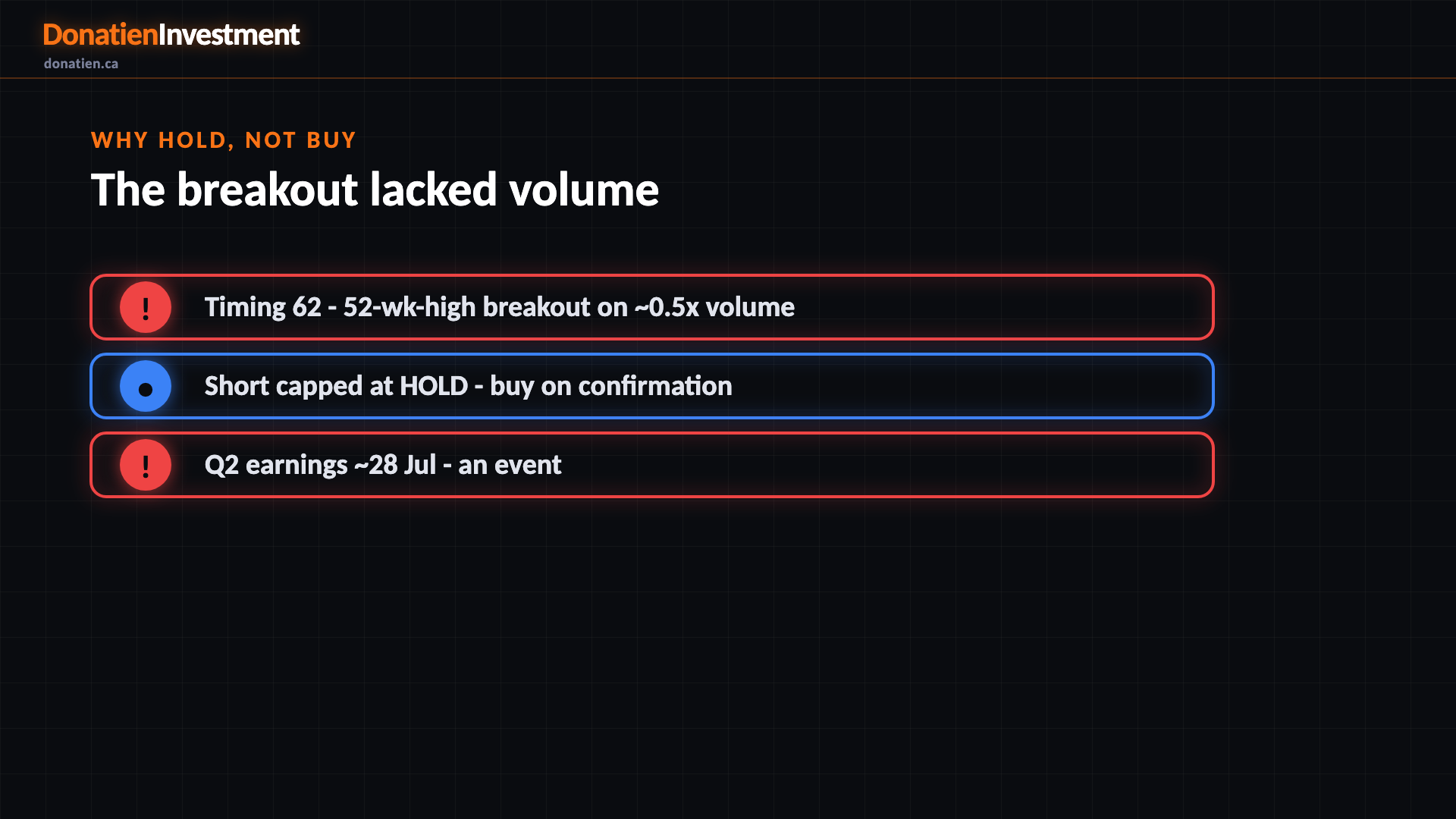

Why Hold, not Buy

So why Hold, not Buy? The breakout to a 52-week high came on thin volume, about half the average. Soft daily momentum and no catalyst in the window fail the timing test, so the short-term signal is capped at Hold - buy on confirmation. Q2 earnings around 28 July are the next event.

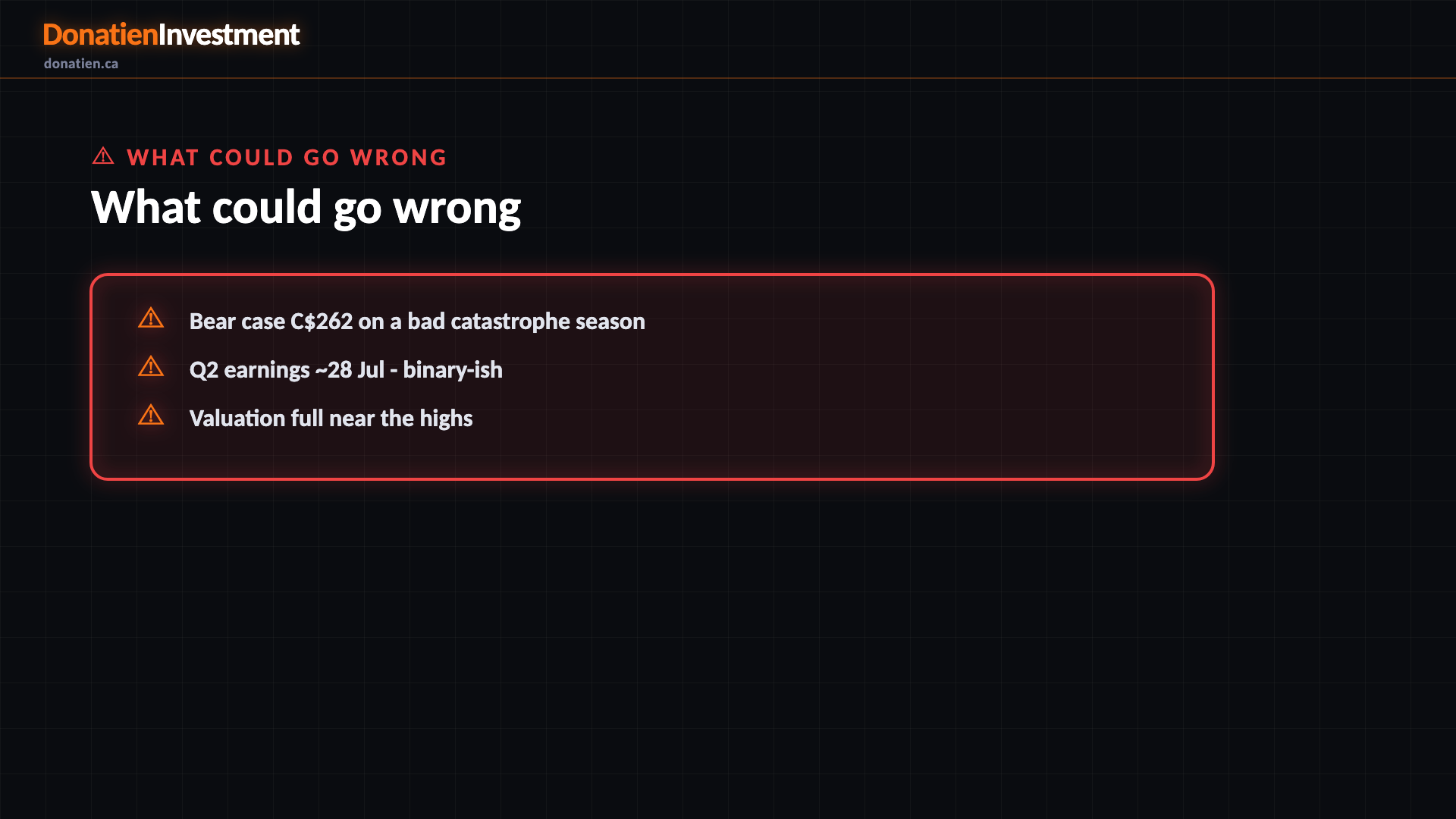

What could go wrong

The risk is event-driven. Catastrophe losses can swing a P&C insurer, and the bear case sits near C$262. Q2 earnings land around 28 July, a near-term binary, and the price is full near its highs. Hold is the honest read - a quality name to own, just not to chase today; base C$320, bull C$355.

Risk vs Reward

Against the current C$295.17, the report frames a bull case at C$355 (+20%), a base case at C$320 (+8%) and a bear case at C$262 (-11%). See the full report for the probability weight behind each path.

The verdict

A quality Canadian insurer riding higher-for-longer, but the breakout to a new high came on thin volume - a hold now, buy on confirmation.

Read the full report on donatien.ca →{kind=link}

{kind=link}