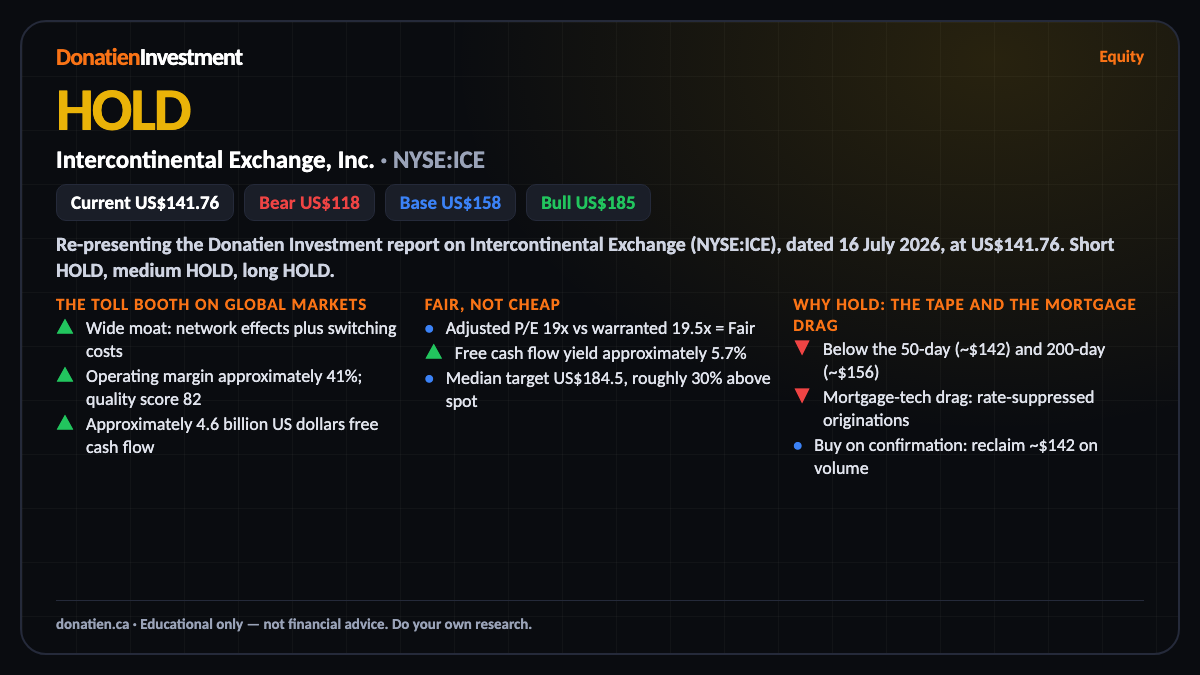

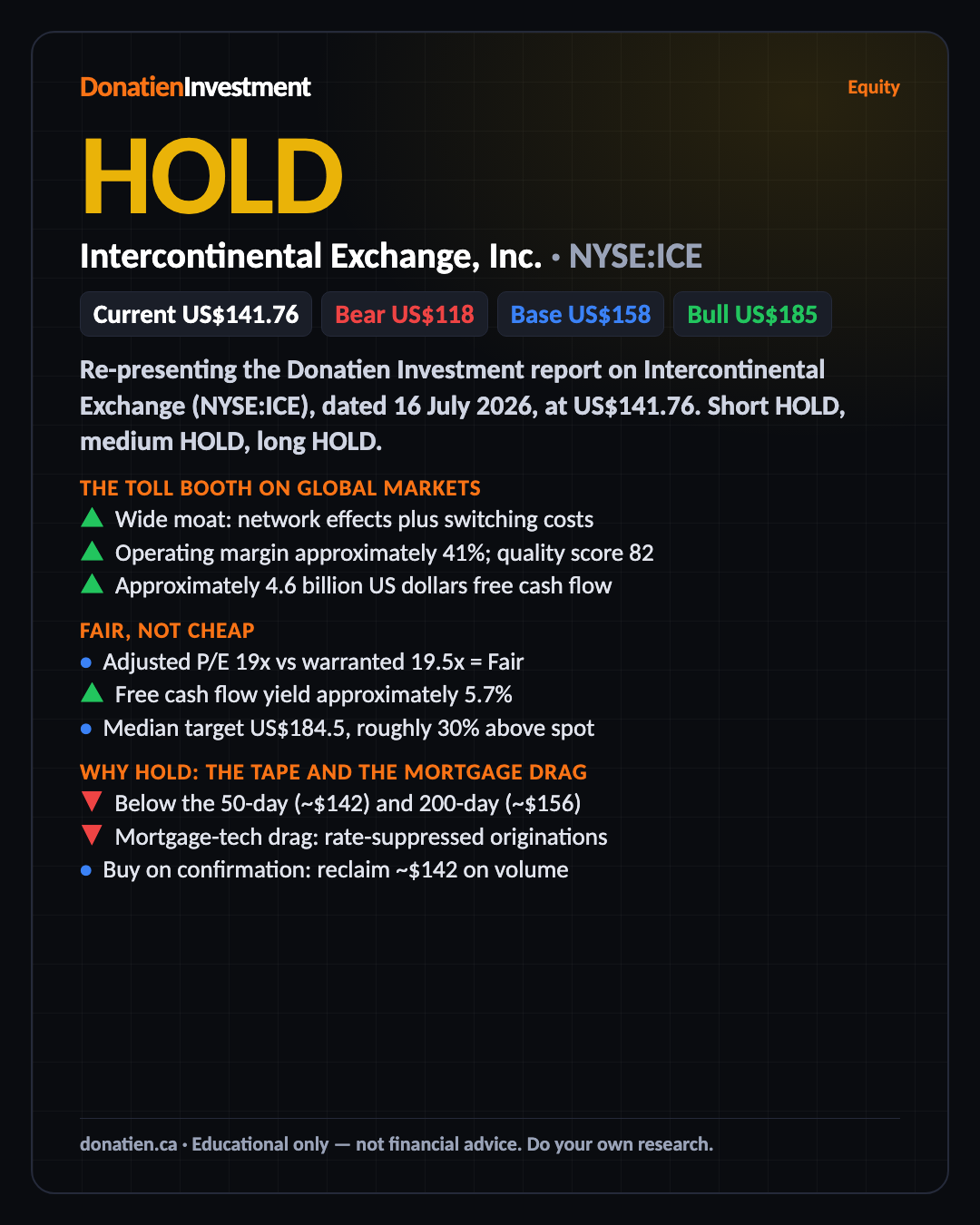

Intercontinental Exchange, Inc. (NYSE:ICE) HOLD

Intercontinental Exchange is a wide-moat, capital-light compounder — the toll booth on global markets — but after a twenty-five per cent pullback it trades at roughly fair value, and the tape sits below its key averages with no confirmed entry. Every horizon reads hold: a quality name at a fair, not attractive, price. Watch for a better entry rather than chase it here.

Re-presenting the Donatien Investment report on Intercontinental Exchange (NYSE:ICE), dated 16 July 2026, at US$141.76. Short HOLD, medium HOLD, long HOLD.

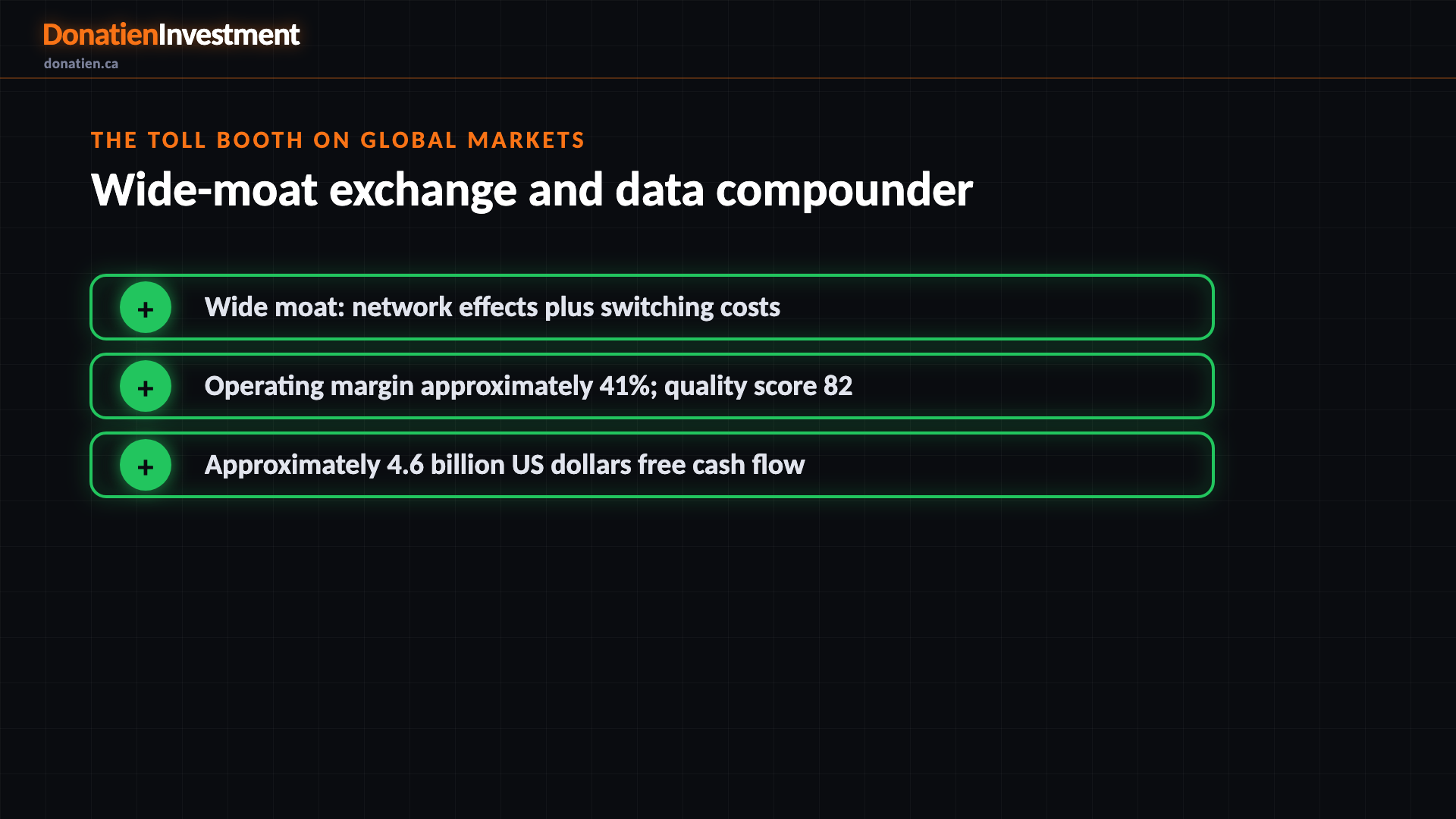

The toll booth on global markets

Intercontinental Exchange owns thirteen exchanges and six clearing houses across energy, agriculture, metals and financial futures, plus the New York Stock Exchange and a large fixed-income data business. It earns fees on activity and data rather than taking market risk itself. The economics are excellent: operating margins around forty-one per cent, free cash flow near four-and-a-half billion US dollars, and roughly half of revenue recurring. The moat rests on network effects and switching costs — liquidity and clearing pools concentrate on one venue, and embedded data feeds are hard to unplug. Quality scores eighty-two, a top-tier capital-light compounder.

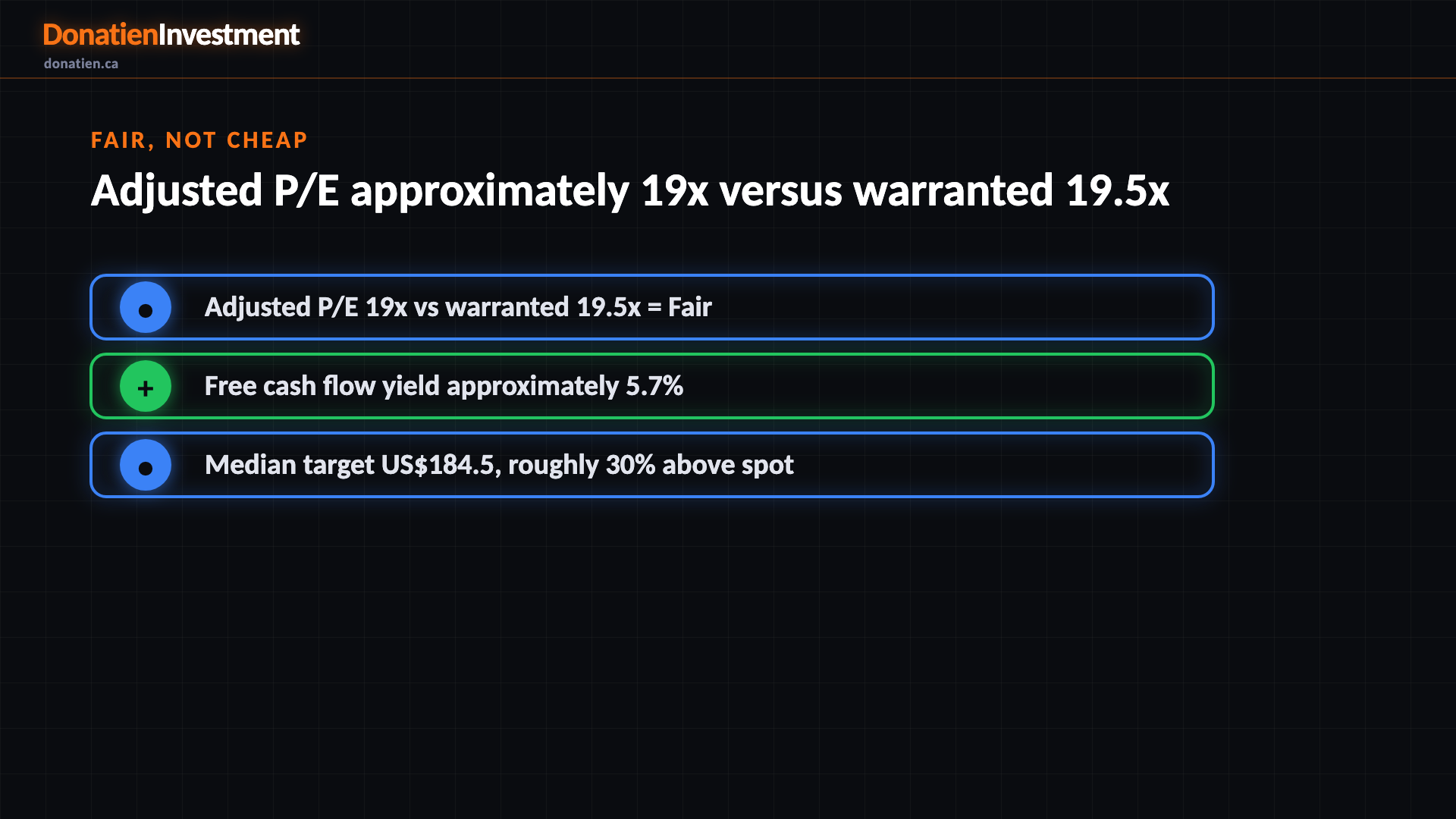

Fair, not cheap

On valuation the quality is roughly priced in. The adjusted price-to-earnings multiple is about nineteen times against a warranted multiple of nineteen-and-a-half, a ratio of zero-point-nine-seven, which lands squarely in the fair band — the forward multiple of seventeen-point-six is a shade cheaper. Free cash flow yield near five-point-seven per cent is attractive for a compounder, but the price-earnings-to-growth ratio of about three says you are paying for durability, not growth. Analysts see a median target of one-hundred-eighty-four-and-a-half dollars, some thirty per cent above spot. A fair-band name is not a valuation entry until it gets cheaper.

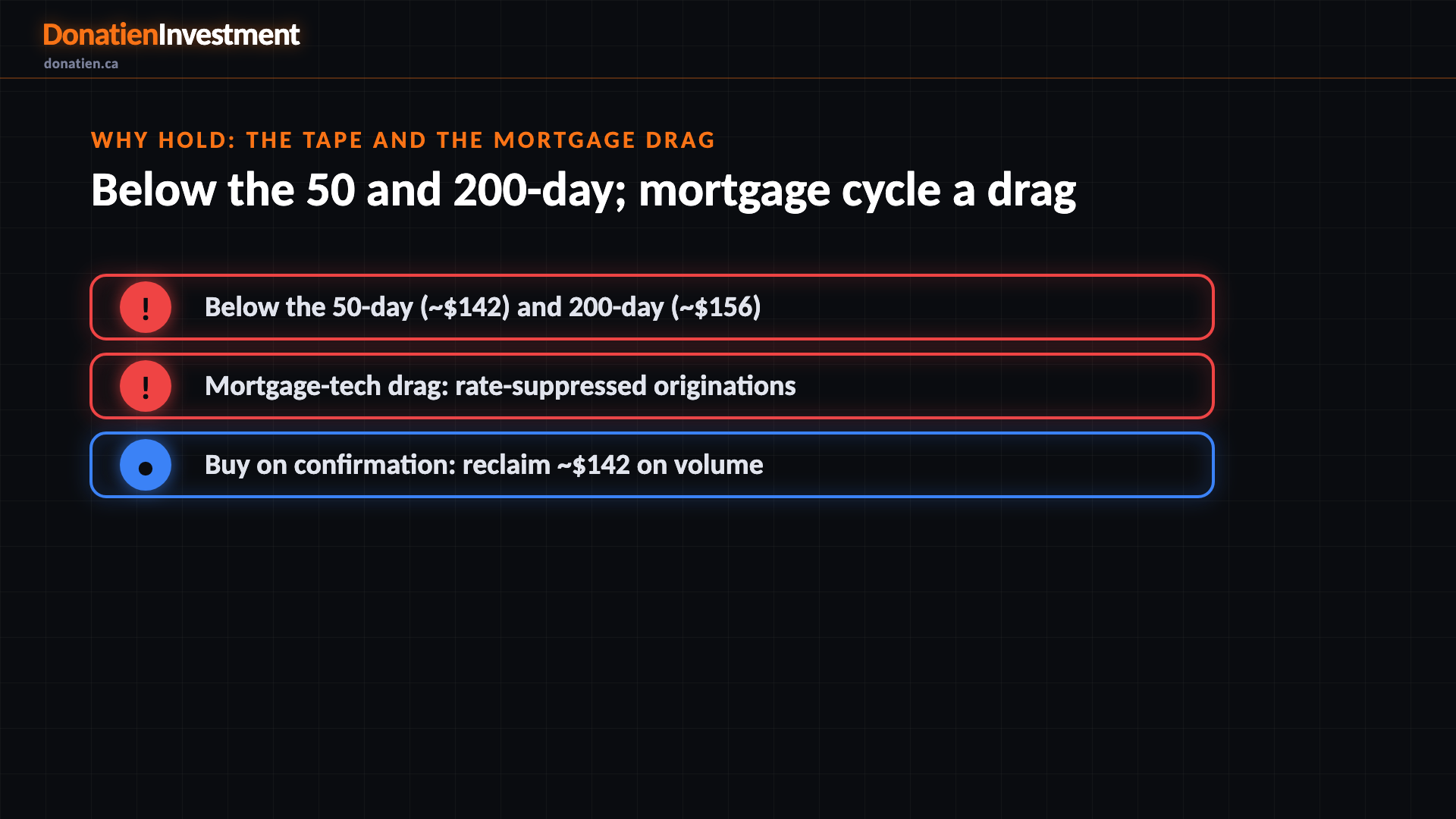

Why hold: the tape and the mortgage drag

Two things hold the signal. First, the tape: the shares have de-rated about twenty-five per cent from a hundred-and-eighty-nine dollar high, and while the monthly structure is intact, the weekly and daily trends are downtrends below both the fifty-day near a hundred-and-forty-two and the two-hundred-day near a hundred-and-fifty-six. No technical entry group is met. Second, the mortgage-technology segment: higher-for-longer rates suppress US home-loan originations, and June pending home sales fell five-point-four per cent, so that engine is a drag. The exchange and data engine outweighs it, but it caps the driver and holds every horizon.

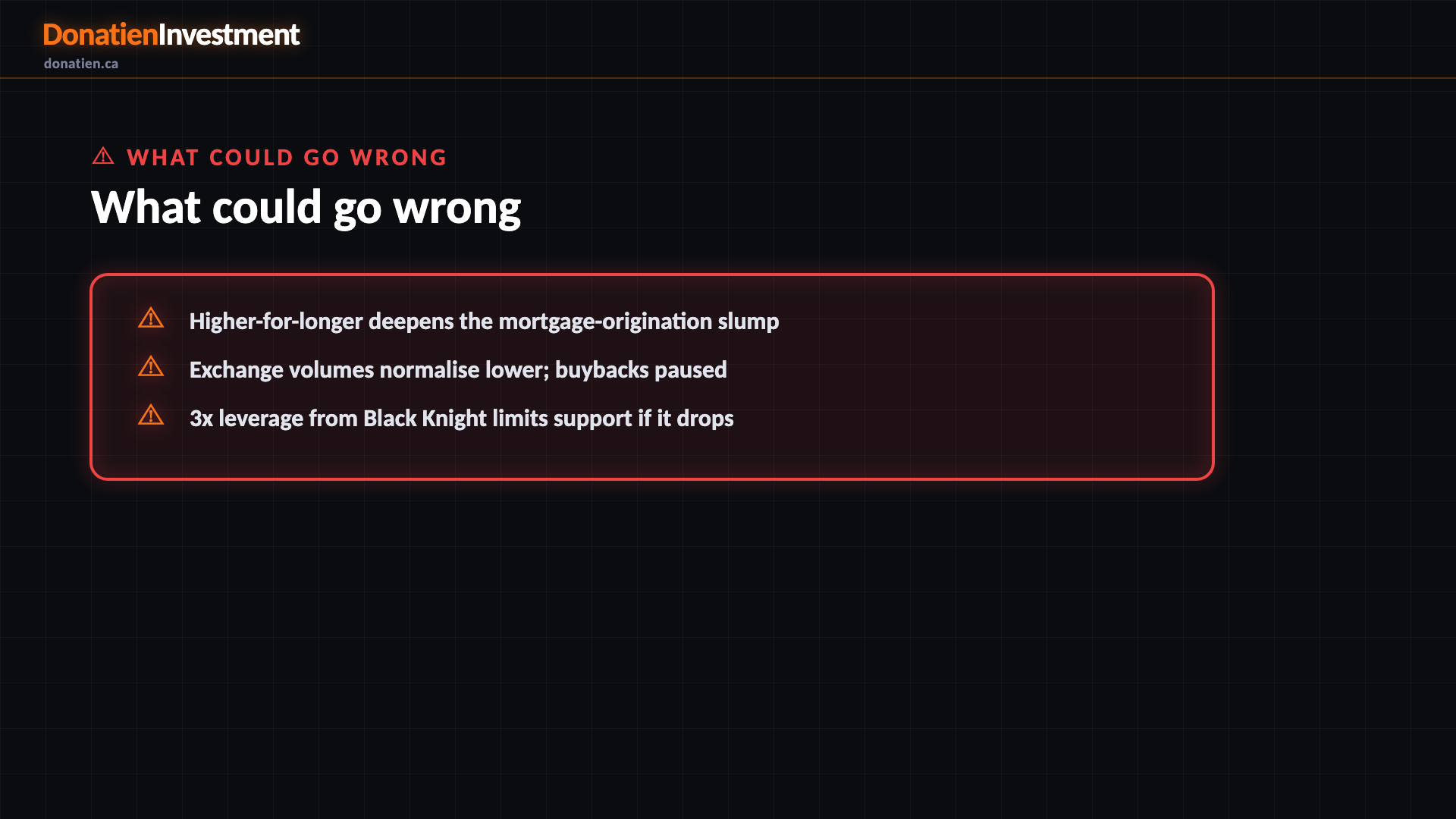

What could go wrong

Higher-for-longer deepens the mortgage-origination slump. Exchange volumes normalise lower; buybacks paused. 3x leverage from Black Knight limits support if it drops.

Risk vs Reward

The report weights three twelve-month paths. The base case, most likely at fifty-five per cent, sees ICE around a hundred-and-fifty-eight dollars as the quality compounder grinds toward its two-hundred-day on mid-single-digit earnings growth, about eleven per cent above today. The bull at twenty-five per cent reaches a hundred-and-eighty-five dollars if the fifty-day is reclaimed, Q2 beats on exchange volume, and mortgage stabilises — where the analyst target sits. The bear at twenty per cent takes it to a hundred-and-eighteen dollars if higher-for-longer deepens the mortgage slump and volumes normalise lower. The probability-weighted fair value is about a hundred-and-fifty-eight dollars, a positive but modest return that leans on the base case, which is why every horizon reads hold rather than buy.

The verdict

The bottom line: a wide-moat, capital-light compounder at a fair, not cheap, valuation, in a downtrend below its key moving averages, with a real mortgage-cycle drag and Q2 earnings on the thirtieth of July. A quality name, but no entry edge right now. It is a hold across every horizon; the disciplined move is to wait for a better entry — a fifty-day reclaim on volume or a tested bounce off support near a hundred-and-thirty-six — rather than chase it here. This is analysis, not financial advice — always do your own research.

Read the full report on donatien.ca →{kind=link}

{kind=link}