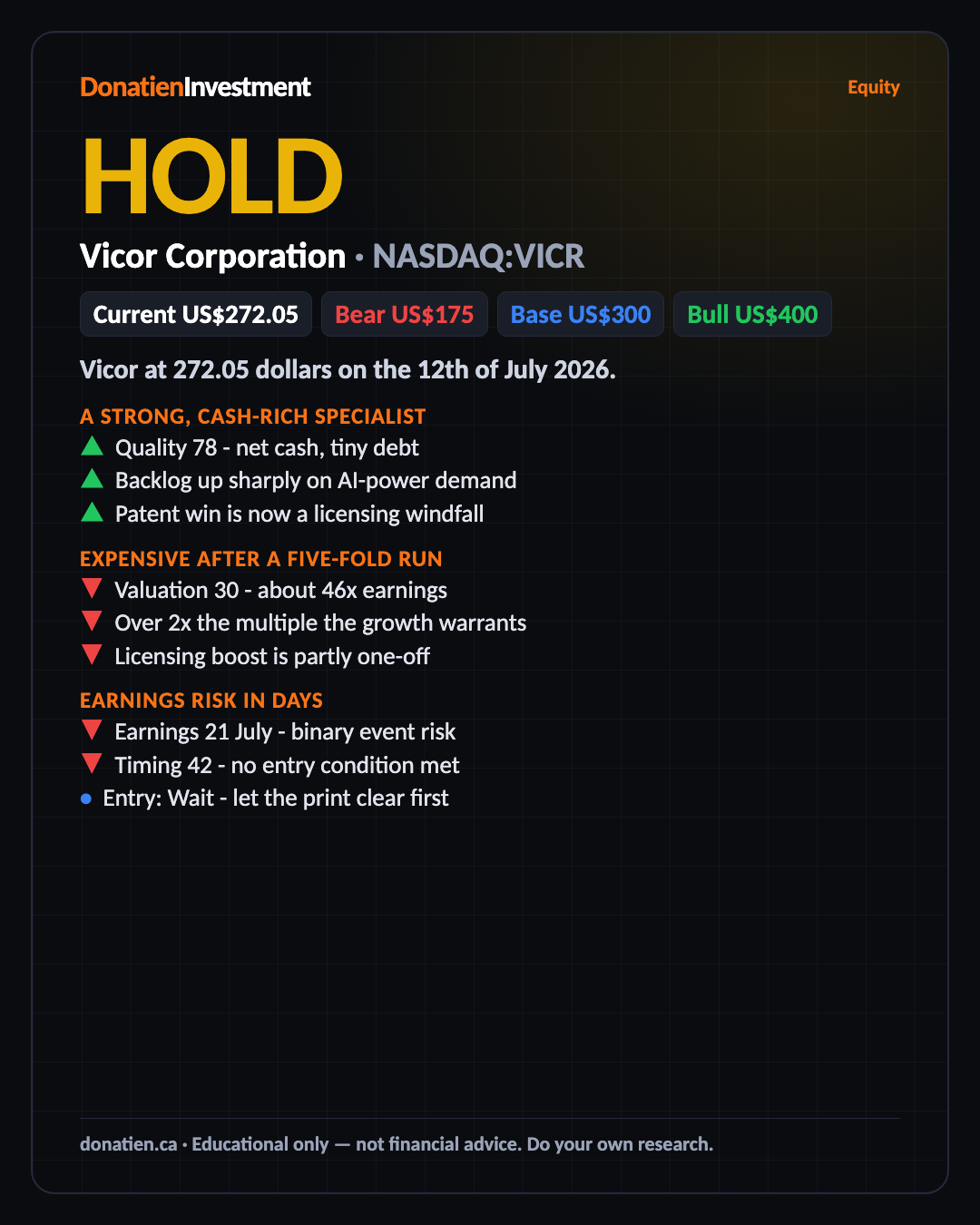

Vicor Corporation (NASDAQ:VICR) HOLD

A fortress-balance-sheet power-module specialist with a real licensing windfall - but Expensive near forty-six times earnings, with results due on the twenty-first of July. A hold; wait for the print and a better price.

Vicor at 272.05 dollars on the 12th of July 2026. Vicor designs high-density power modules that feed AI accelerators, sits on roughly four hundred million dollars of net cash with almost no debt, and has just won an important patent case that is turning into a licensing windfall. The business is strong. But the shares have run about five-fold off their low, and results are due in days.

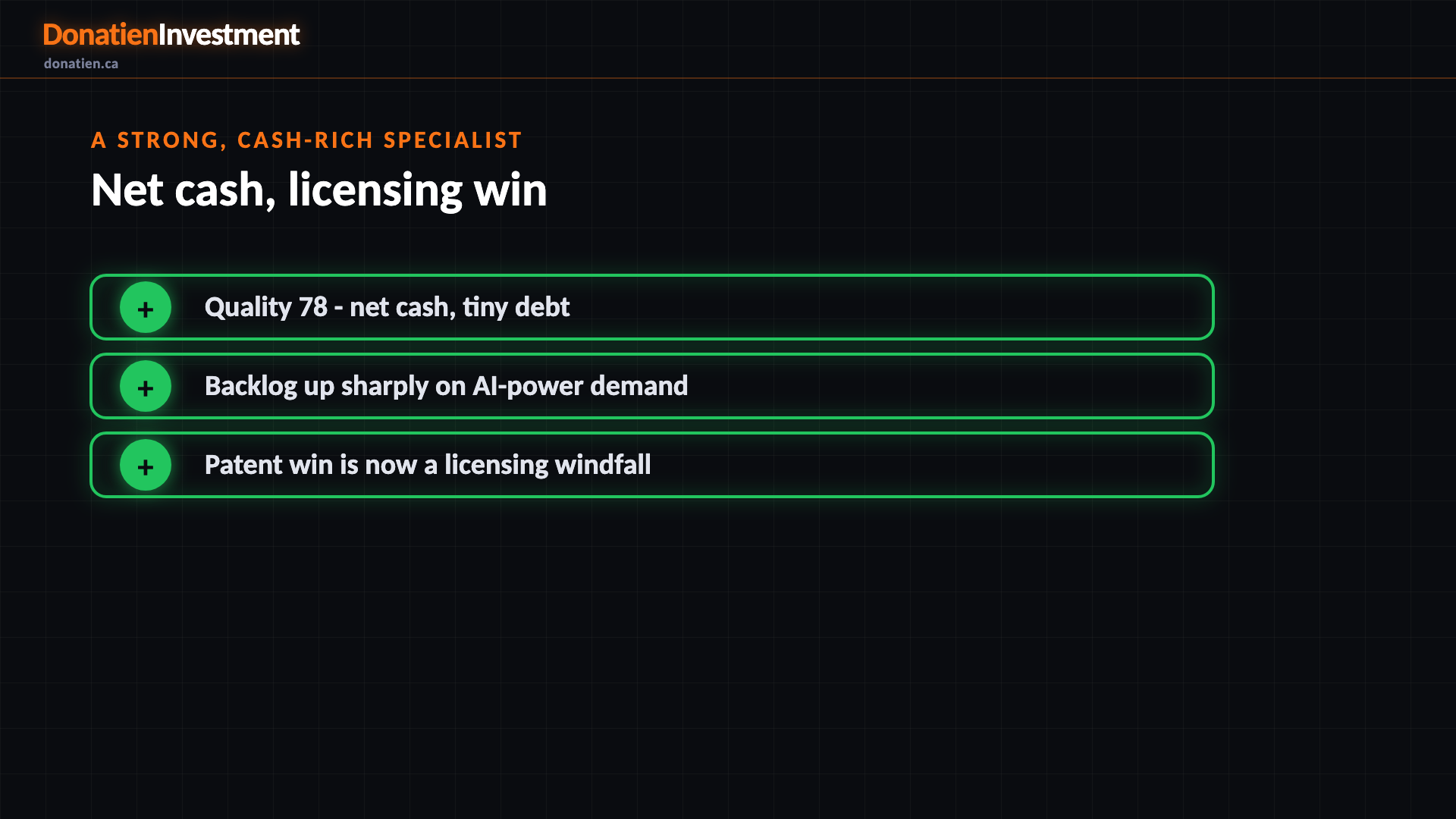

A strong, cash-rich specialist

Quality scores seventy-eight. Vicor makes the dense power-conversion modules that sit close to AI chips, carries around four hundred million dollars of net cash with almost no debt, and has a backlog that has grown sharply as computing power demand rises. On top of that, a patent win is generating a genuine licensing stream. This is a real, well-run business with an unusually clean balance sheet - the reservation is the price and the timing, not the company.

Expensive after a five-fold run

Valuation scores thirty. The shares trade near forty-six times earnings, more than twice the multiple the growth warrants, which trips our valuation-ceiling gate. Some of the current profit is a one-off licensing boost that will roll off, flattering the picture. The intrinsic value we work back to sits well below today's price. This is a cyclical hardware name that has run about five-fold off its low - a great business, but priced as if the good times are permanent.

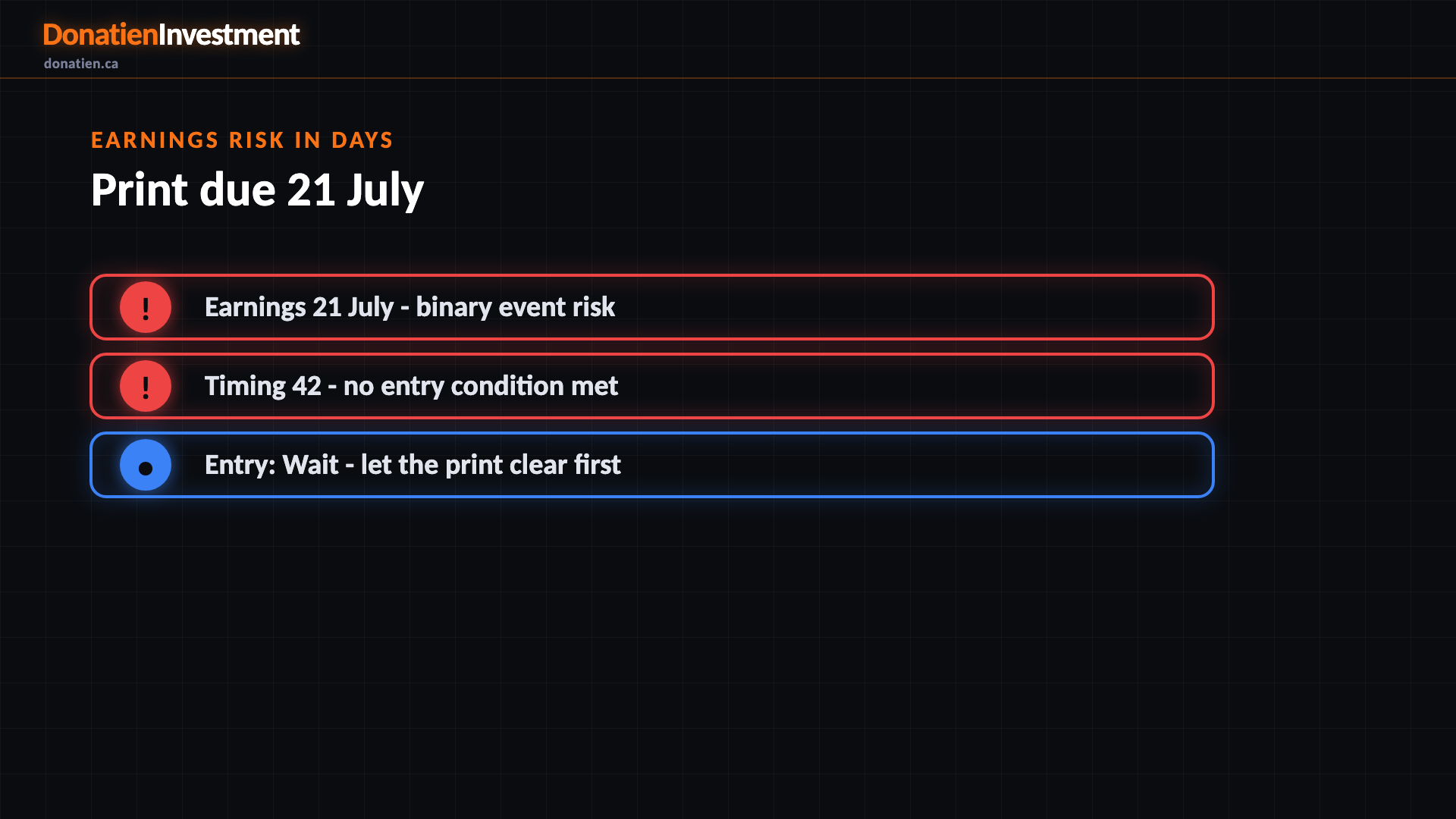

Earnings risk in days

There is a second reason to wait: Vicor reports on the twenty-first of July, and a rich, high-beta stock into a binary event is exactly where surprises hurt most. Timing scores forty-two, and none of our entry conditions is met. So this is a hold - a fine business we would like to own, but only after the print clears the event risk and, ideally, at a price closer to what the fundamentals support.

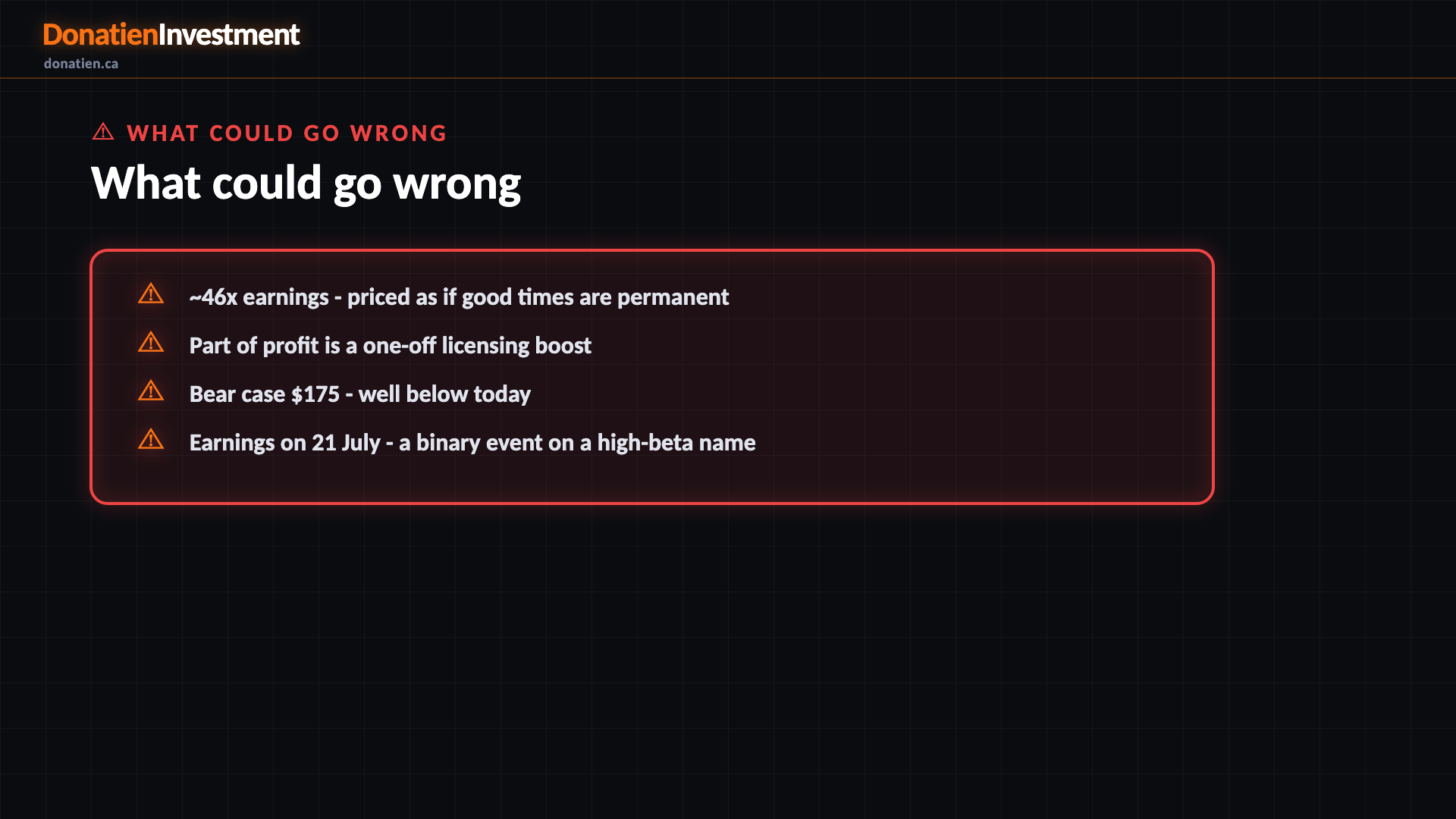

What could go wrong

~46x earnings - priced as if good times are permanent. Part of profit is a one-off licensing boost. Bear case $175 - well below today. Earnings on 21 July - a binary event on a high-beta name. Cyclical hardware - demand can turn quickly.

Risk vs Reward

Against the current US$272.05, the report frames a bull case at US$400 (+47%), a base case at US$300 (+10%) and a bear case at US$175 (-36%). See the full report for the probability weight behind each path.

The verdict

A fortress-balance-sheet power-module specialist with a real licensing windfall - but Expensive near forty-six times earnings, with results due on the twenty-first of July. A hold; wait for the print and a better price.

Read the full report on donatien.ca →{kind=link}

{kind=link}