Credo Technology Group Holding Ltd (NASDAQ:CRDO) DO NOT BUY

A genuinely excellent, clean-earning connectivity-chip designer - but near forty-two times forward earnings and the clearest hostage of the AI-datacentre trade, with almost all its revenue in four customers. A company to own far lower.

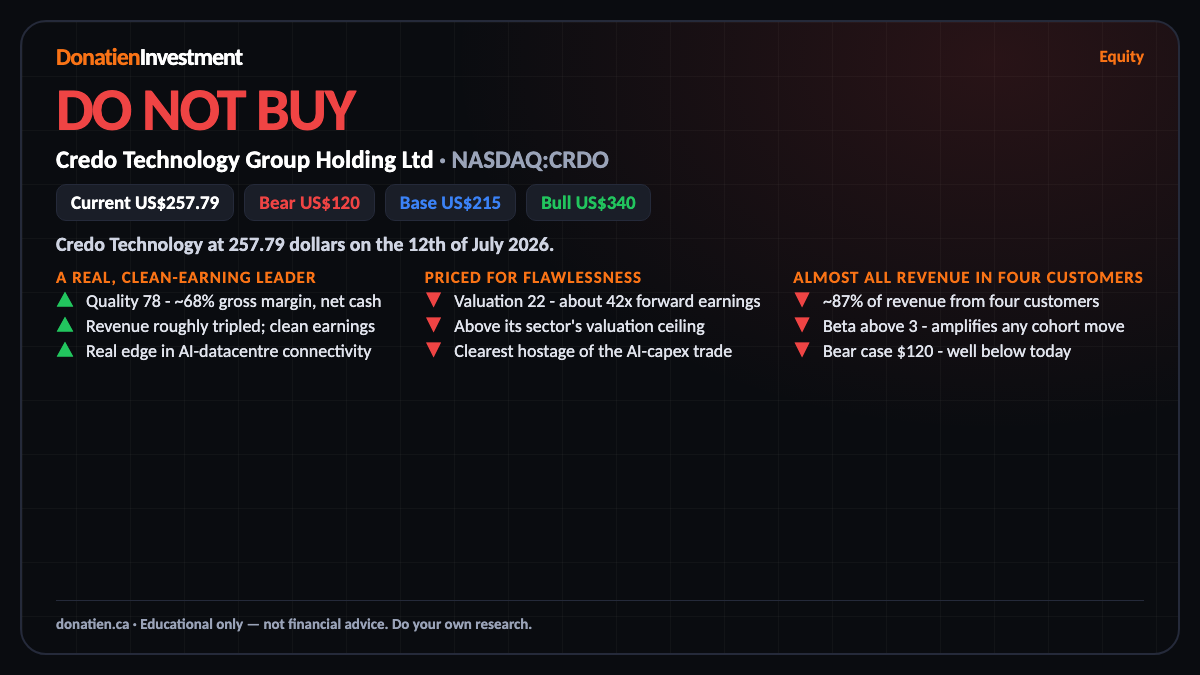

Credo Technology at 257.79 dollars on the 12th of July 2026. Credo makes the high-speed connections - active electrical cables and SerDes chips - that wire up AI data centres, at gross margins near sixty-eight per cent and with net cash. Revenue has roughly tripled. This is a real, high-quality business. The trouble is the price and the concentration risk sitting underneath it.

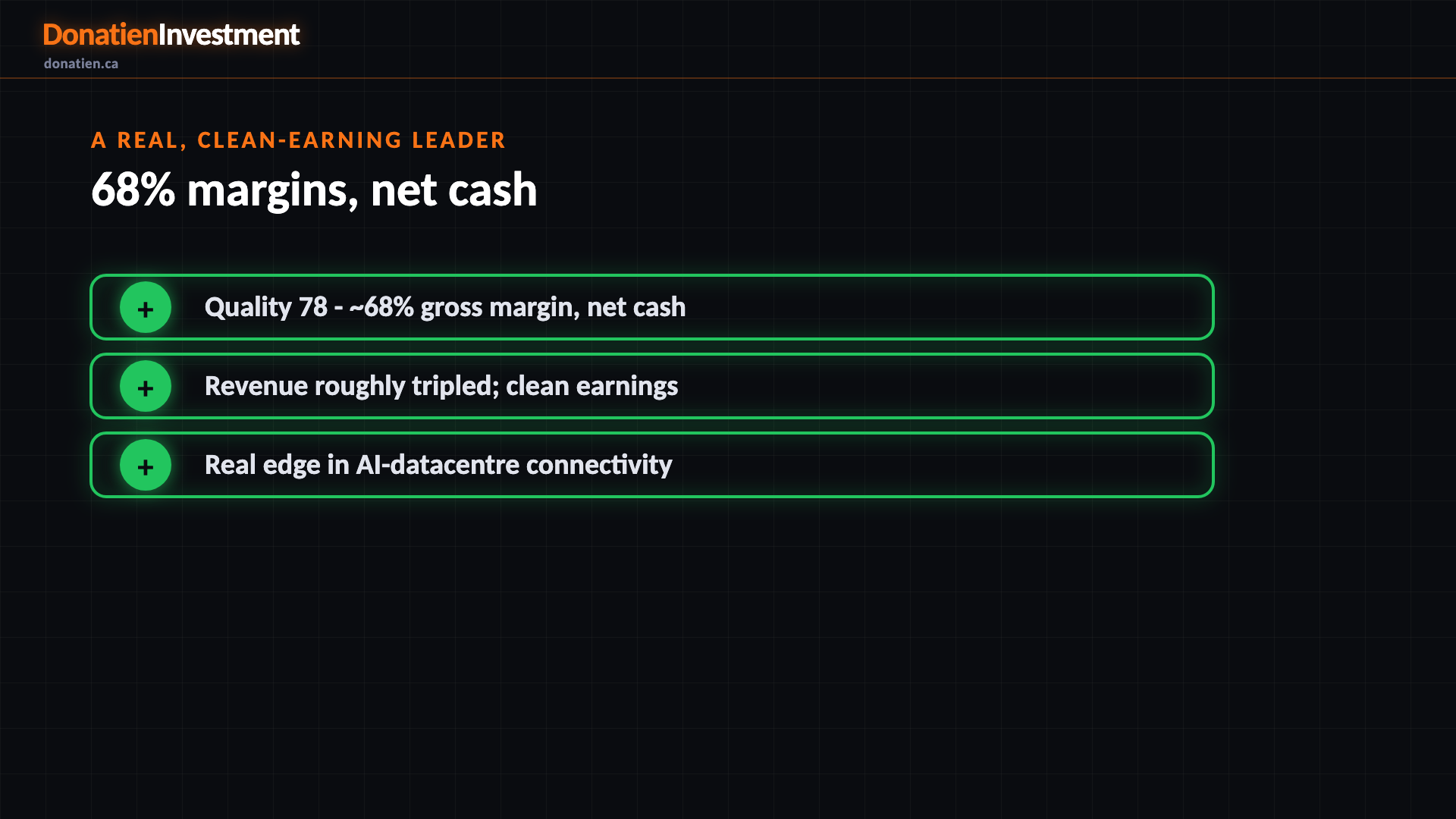

A real, clean-earning leader

Quality scores seventy-eight. Credo has a genuine edge in the cables and chips that move data around AI server racks, with gross margins near sixty-eight per cent, net cash, and revenue that has roughly tripled. Crucially, unlike some of its mega-cap peers, its earnings are clean - not inflated by paper gains on private stakes. So the caution that follows is not about accounting or business quality. It is about how much you pay, and how concentrated the customer base is.

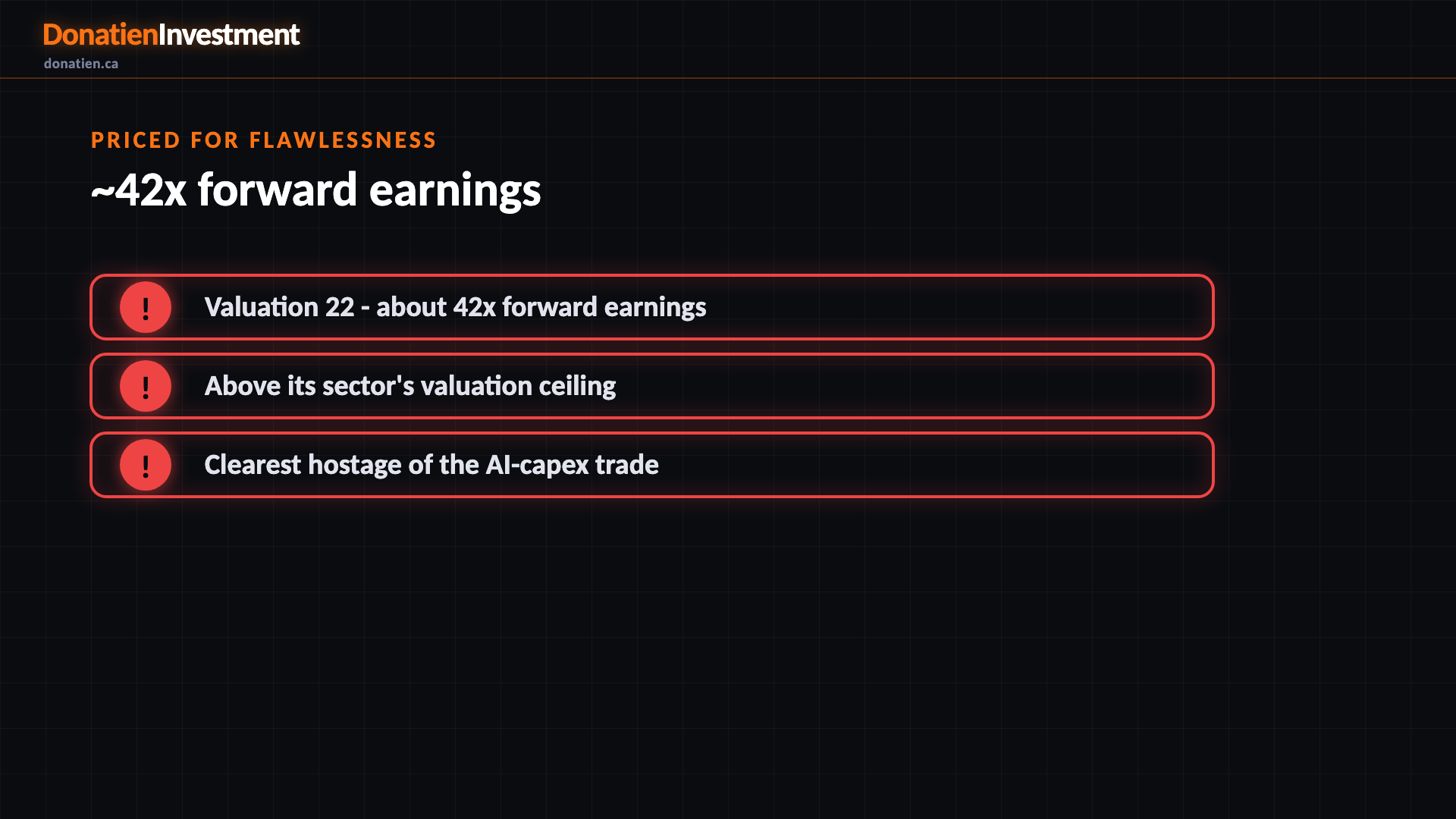

Priced for flawlessness

Valuation scores twenty-two. The shares trade near forty-two times forward earnings, well above both the multiple the growth warrants and the ceiling for its sector. There is essentially no margin of safety - the price assumes a flawless future. On top of that, Credo is the clearest member of the market's most crowded trade: names whose value is levered directly to hyperscaler AI spending. If that spending pauses, the whole cohort re-rates together, and a stock like this, with a beta above three, moves hardest of all.

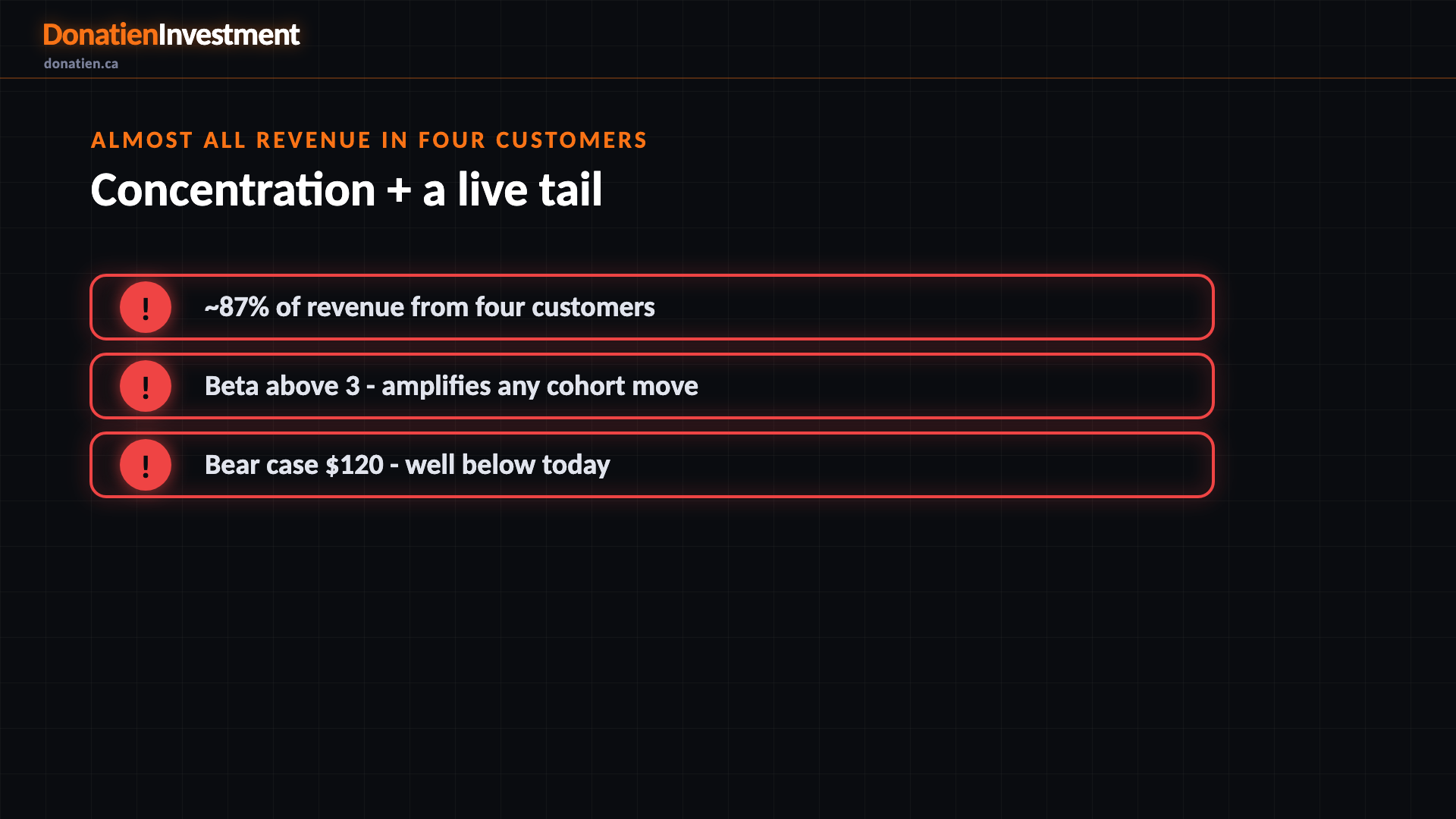

Almost all revenue in four customers

About eighty-seven per cent of Credo's revenue comes from just four hyperscale customers. That is enormous single-customer risk: one large buyer cutting orders, or shifting to optical or in-house parts, would hit revenue hard. Combine an expensive multiple with that concentration and a live risk that the AI-spending cohort de-rates, and the expected value of buying here turns negative. This is a do-not-buy on price and risk - a superb business we would happily own much lower, not a criticism of the company.

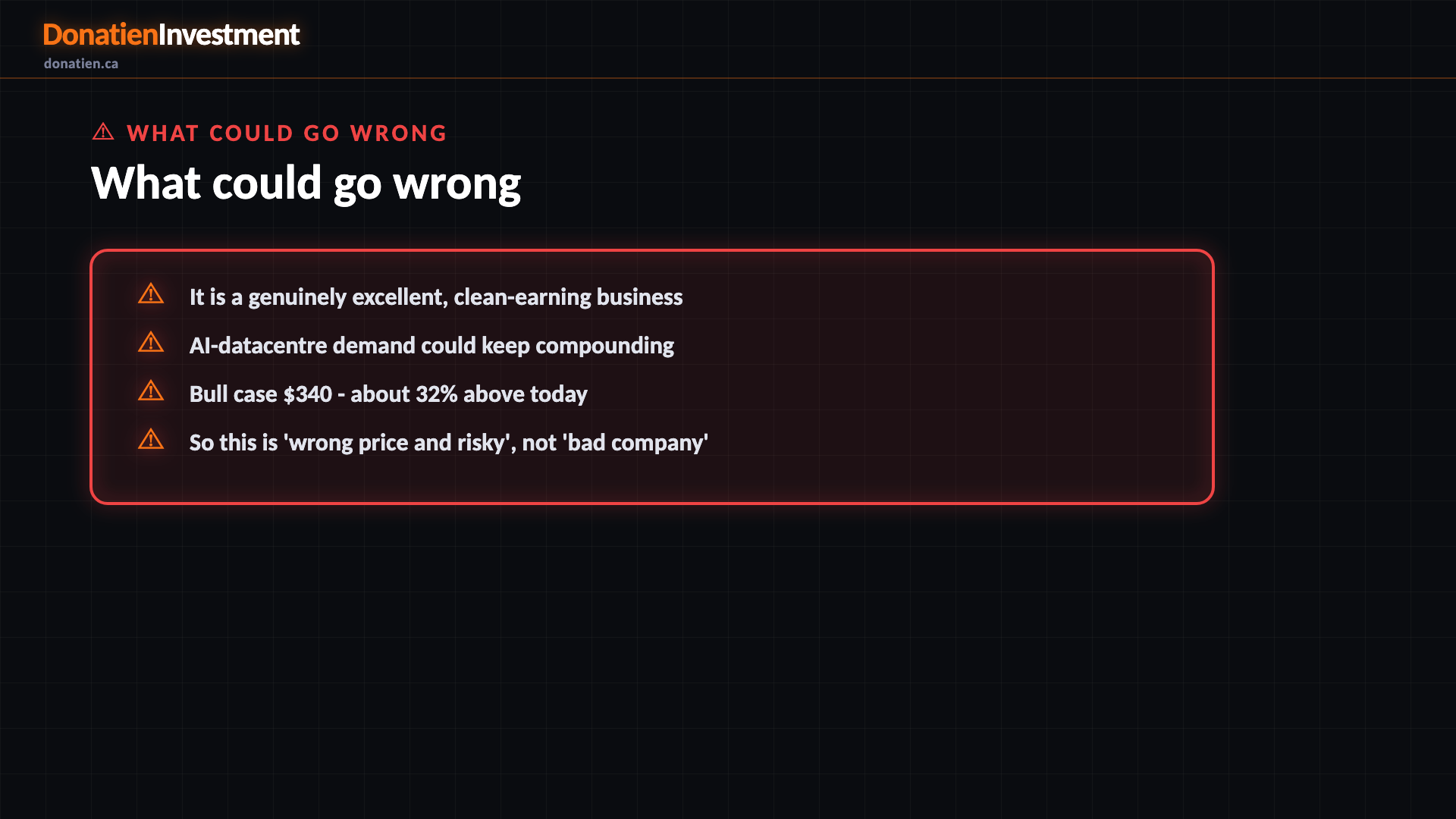

What could go wrong

It is a genuinely excellent, clean-earning business. AI-datacentre demand could keep compounding. Bull case $340 - about 32% above today. So this is 'wrong price and risky', not 'bad company'.

Risk vs Reward

Against the current US$257.79, the report frames a bull case at US$340 (+32%), a base case at US$215 (-17%) and a bear case at US$120 (-53%). See the full report for the probability weight behind each path.

The verdict

A genuinely excellent, clean-earning connectivity-chip designer - but near forty-two times forward earnings and the clearest hostage of the AI-datacentre trade, with almost all its revenue in four customers. A company to own far lower.

Read the full report on donatien.ca →{kind=link}

{kind=link}