Sea Limited (NYSE:SE) HOLD

Sea Limited — Shopee, Garena and SeaMoney — is South-East Asia's leading internet company, newly profitable at the group level. But after a fifteen per cent run it trades at about thirty-nine times earnings, in our Expensive band, with an elevated competitive threat. A great growth story at a rich price — HOLD.

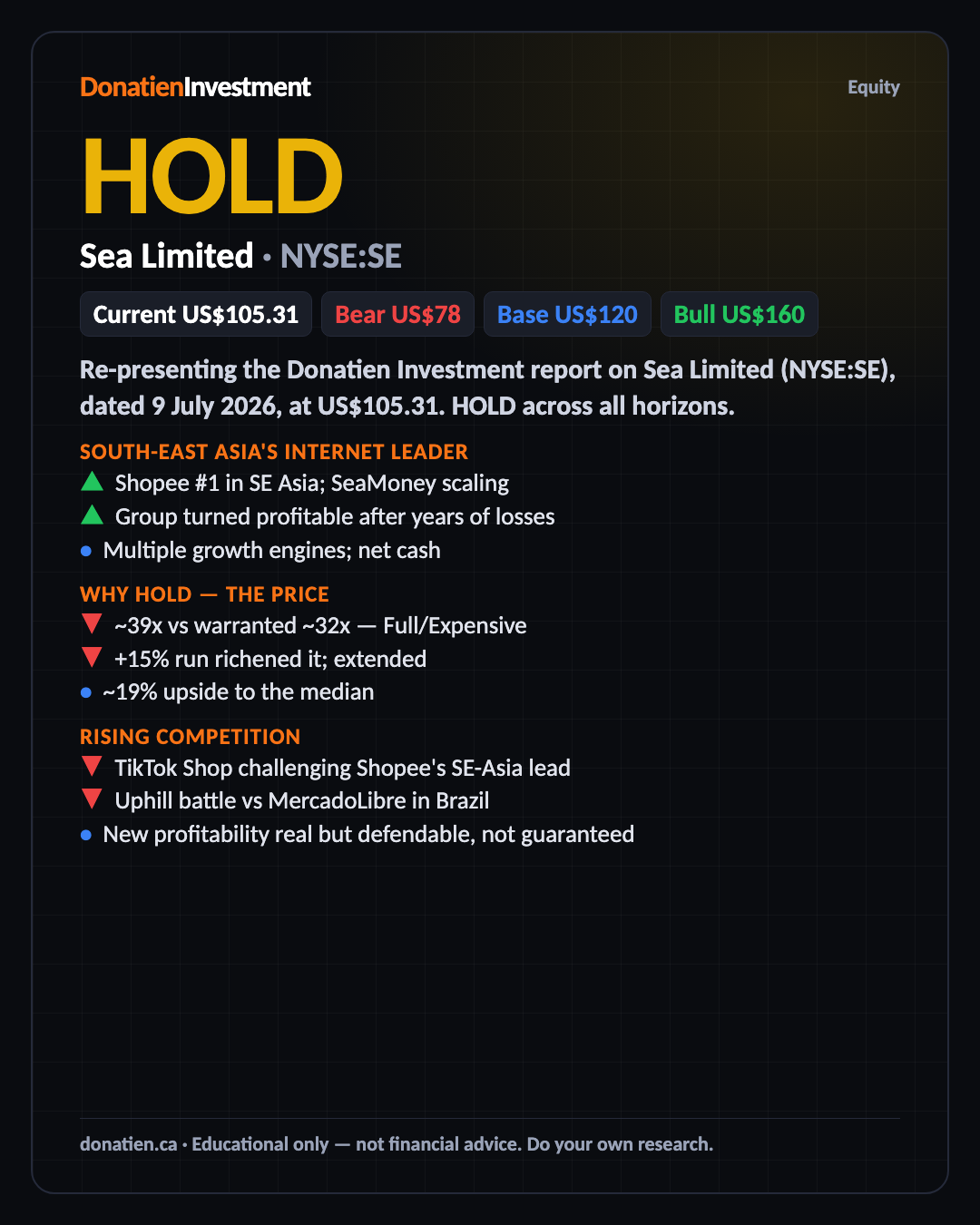

Re-presenting the Donatien Investment report on Sea Limited (NYSE:SE), dated 9 July 2026, at US$105.31. HOLD across all horizons.

South-East Asia's internet leader

Sea runs three businesses: Shopee, the region's number-one e-commerce marketplace now expanding in Brazil; Garena, its digital-entertainment and gaming arm; and SeaMoney, digital financial services. The story is Shopee scaling to profitability across a young, fast-growing, mobile-first region, funded by Garena's cash. The key positive is that the group recently turned profitable after years of losses.

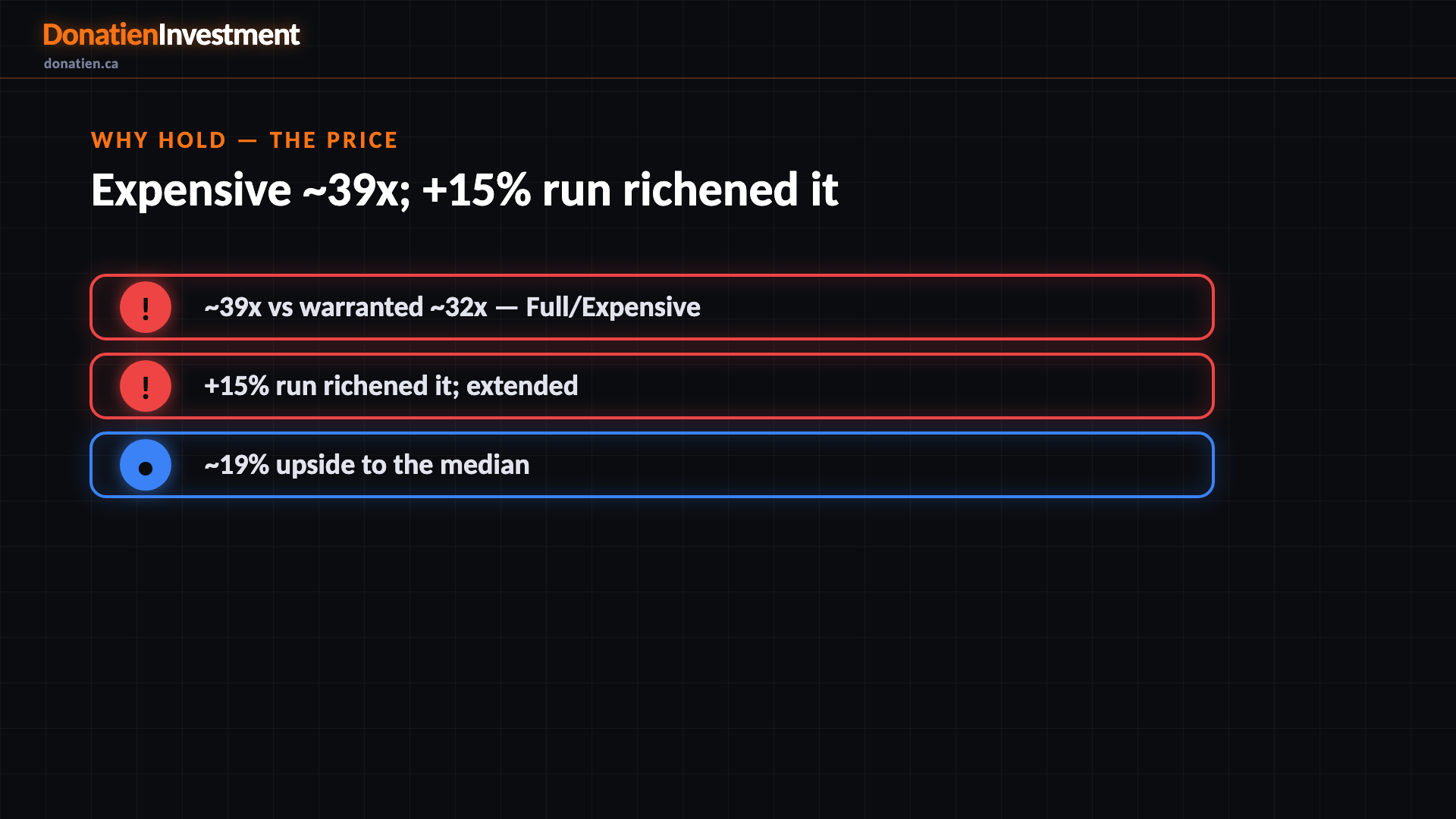

Why hold — the price

Here's what caps it. At about thirty-nine times earnings against a warranted multiple near thirty-two, Sea sits in our Full-to-Expensive band — and the recent fifteen per cent momentum run richened it further, with only about nineteen per cent upside to the analyst median. The price-earnings-to-growth ratio looks fair only if you credit the full hyper-growth; the disciplined anchor deliberately haircuts it.

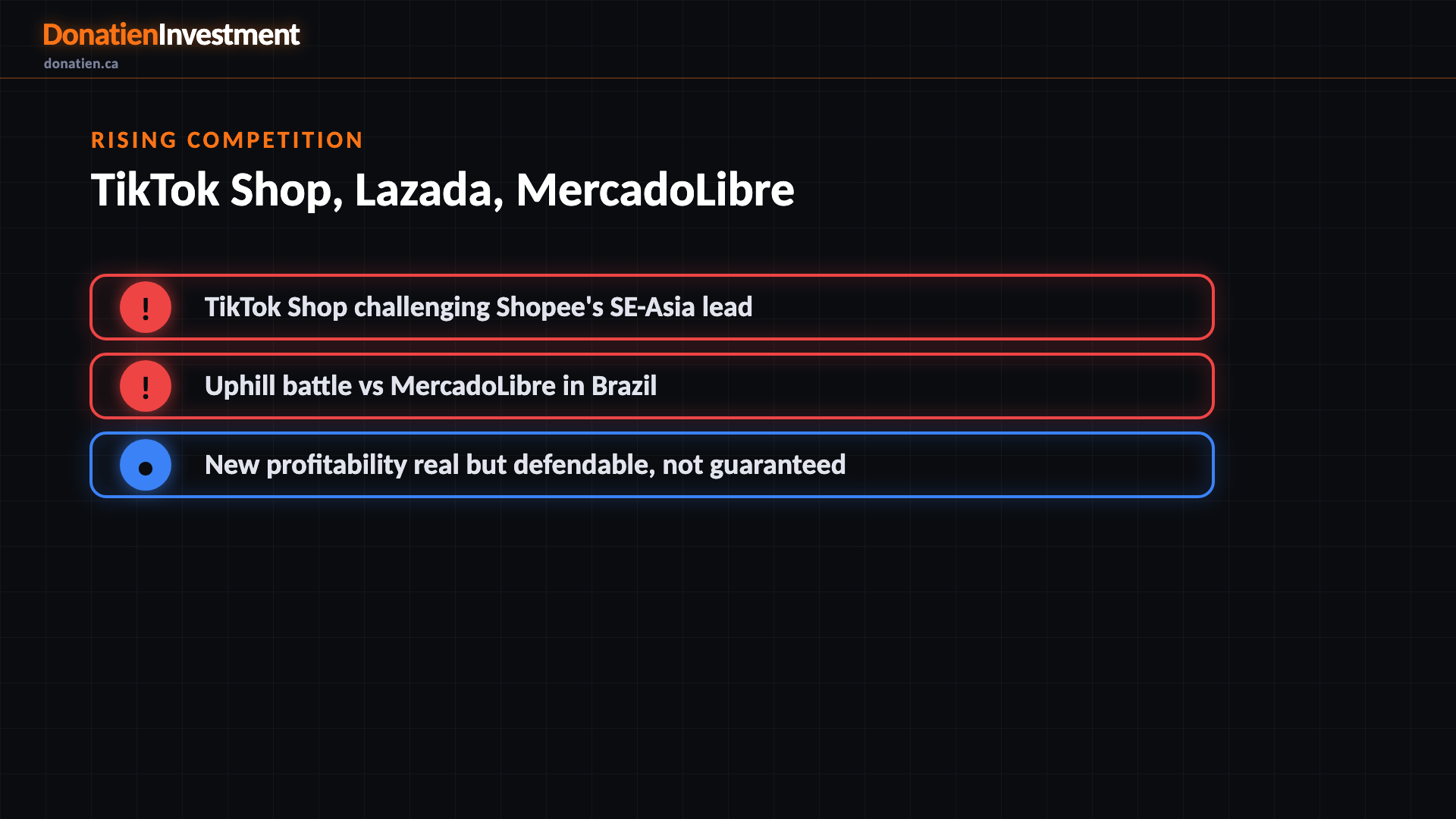

Rising competition

The competitive threat is elevated. TikTok Shop is the key challenger to Shopee's South-East Asia lead; Lazada remains a well-funded rival; and in Brazil, Sea is investing against a strong MercadoLibre incumbent. The new profitability is real but not guaranteed — it could be competed away. Paired with an expensive multiple, that makes the risk-reward at this price capped.

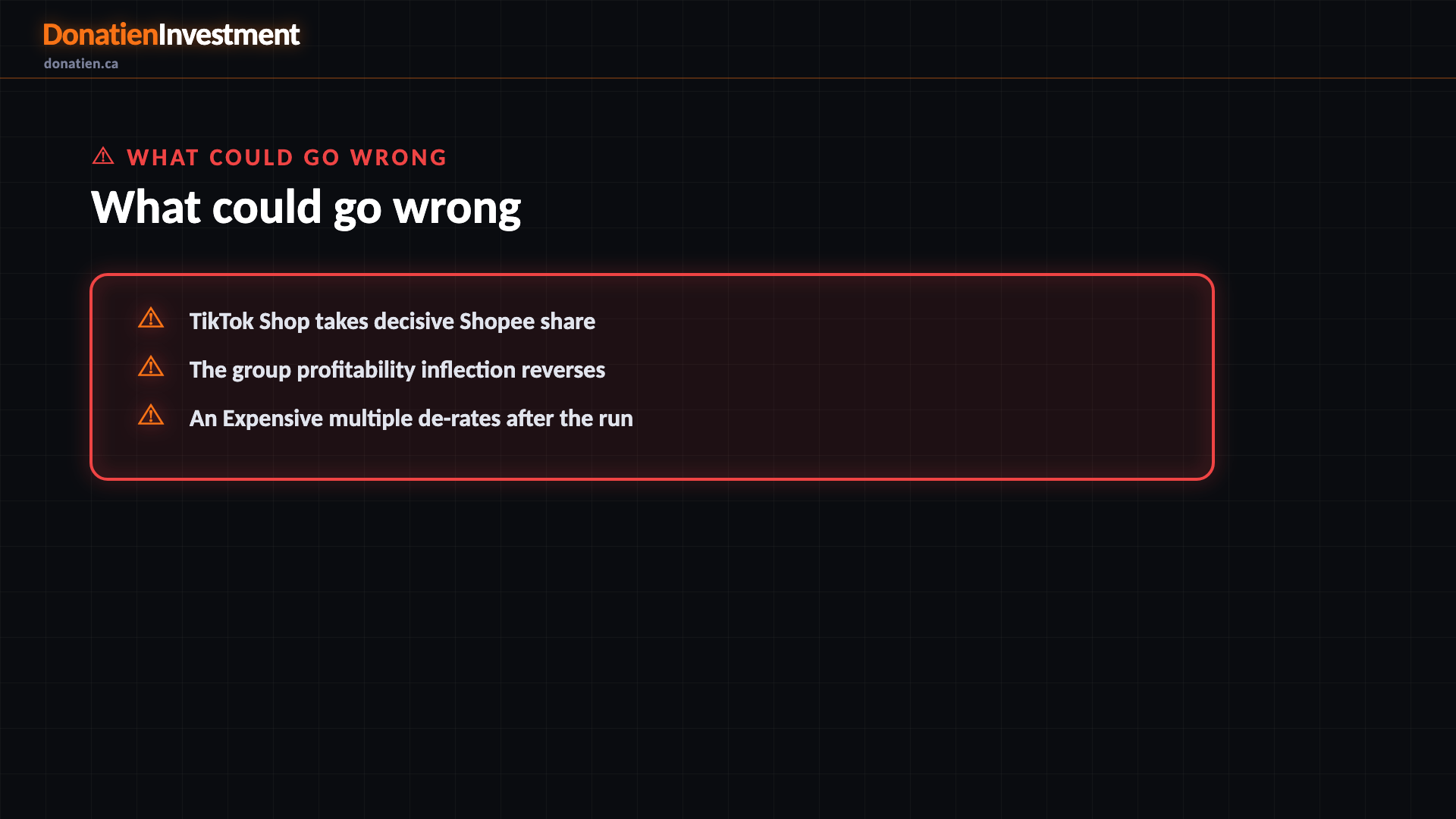

What could go wrong

TikTok Shop takes decisive Shopee share. The group profitability inflection reverses. An Expensive multiple de-rates after the run.

Risk vs Reward

The report weights three twelve-month paths. The base case — most likely at 50% — sees Sea around US$120 on steady growth and widening profits, but a rich multiple caps the re-rate, about 14% above today. The bull at 25% reaches US$160 if Shopee accelerates, SeaMoney scales, and Brazil turns. The bear at 25% takes it to US$78 if TikTok Shop takes share or the profitability inflection stalls and the Expensive multiple de-rates.

The verdict

The bottom line: a real growth story with a genuine profitability inflection — but at about thirty-nine times earnings after a fifteen per cent run, with an elevated competitive threat and only nineteen per cent upside to the median, the risk-reward at this price is capped. It's a hold. The story is good; the price and the timing aren't — wait for a pullback or a de-rate rather than chasing the momentum.

Read the full report on donatien.ca →{kind=link}

{kind=link}