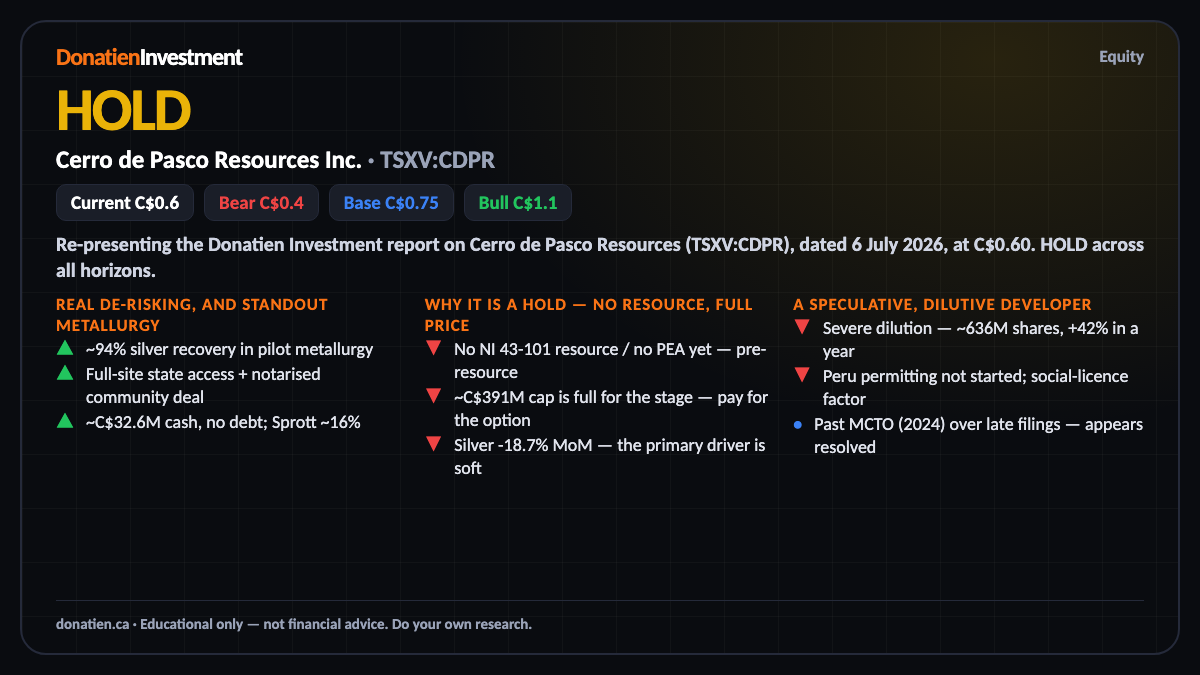

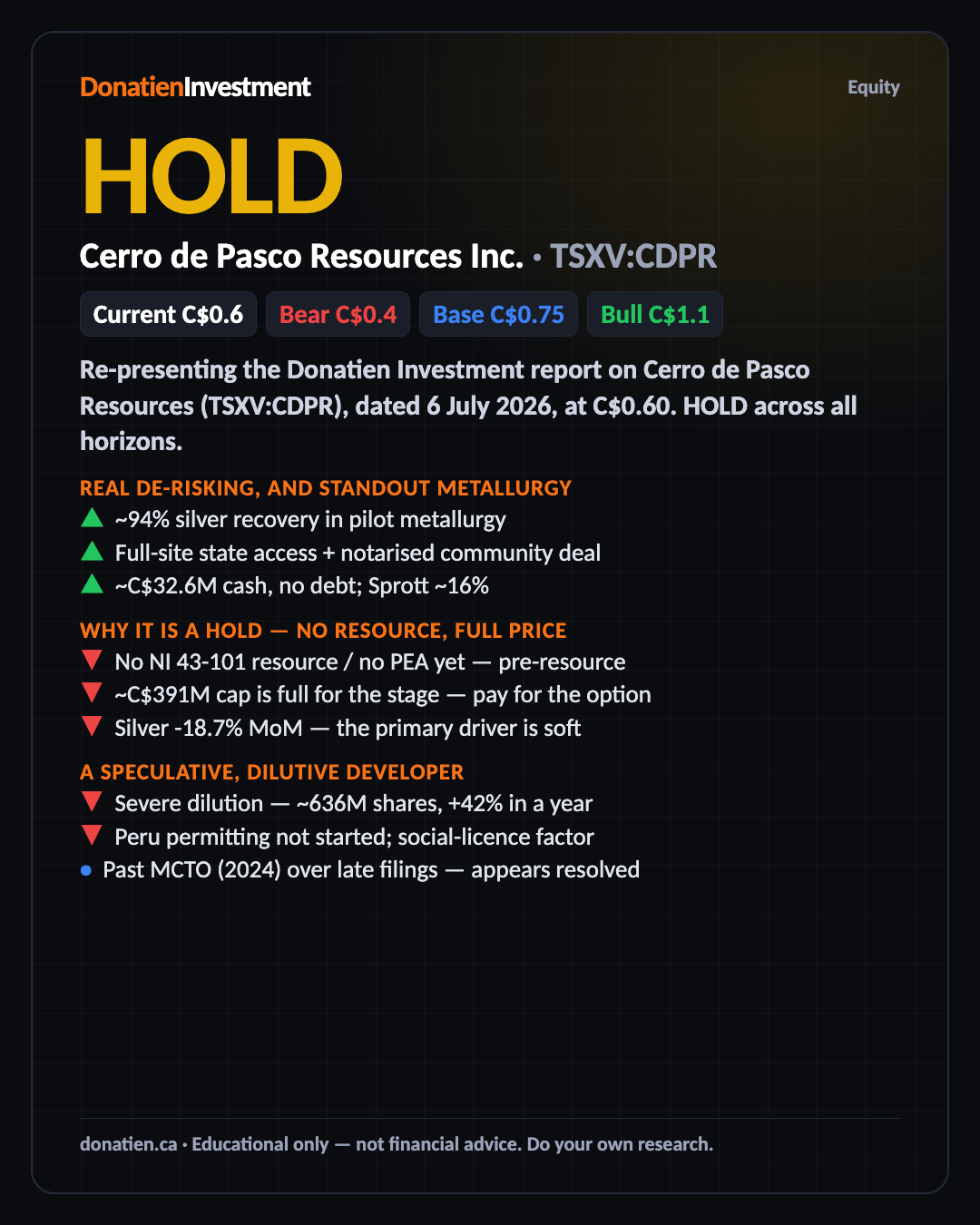

Cerro de Pasco Resources Inc. (TSXV:CDPR) HOLD

A funded, Sprott-backed silver-tailings developer with a strong 94% pilot recovery and secured site access — but still pre-resource, richly valued at ~C$391M for the stage, and into a silver downtrend. A hold with no entry edge until the maiden resource proves the ounces.

Re-presenting the Donatien Investment report on Cerro de Pasco Resources (TSXV:CDPR), dated 6 July 2026, at C$0.60. HOLD across all horizons.

Real de-risking, and standout metallurgy

There is genuine progress here. The company secured state-entity access to the entire tailings area, signed a notarised community agreement, and — the standout — returned about ninety-four per cent silver recovery in pilot metallurgical tests on a two-concentrate flowsheet. The fine tailings need little grinding, a potential cost edge. It is funded, with roughly thirty-two million dollars of cash and no debt, and Eric Sprott holds about sixteen per cent. For a tailings-reprocessing idea, the technical pieces are advancing.

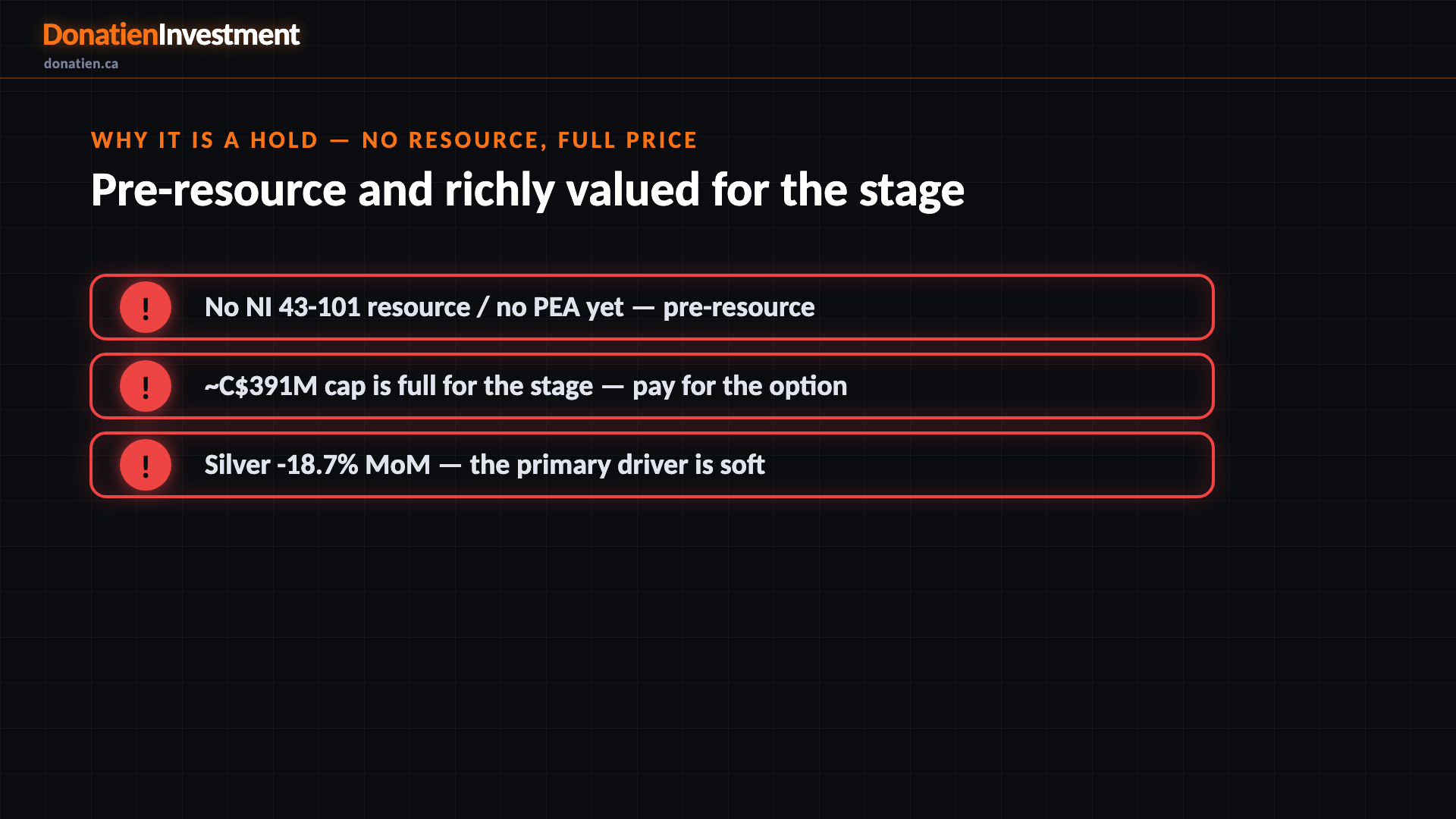

Why it is a hold — no resource, full price

Here is the discipline. There is no compliant mineral resource and no economic study yet — every scale figure, including the headline four-hundred-million-ounce silver-equivalent number, is a company estimate, not verified ounces. Yet the market already pays roughly three-hundred-and-ninety-one million dollars for it, which is full for a pre-resource name; you are paying a full price for the option, not getting it free. Add a silver price down nearly nineteen per cent on the month, and there is no entry edge until a maiden resource proves the ounces.

A speculative, dilutive developer

This is speculative. Funding is entirely by issuing shares, the count is up more than forty per cent in a year, and more raises are coming through feasibility. It operates in Peru, where permitting has not started and social licence is a live factor, though currently managed. There is also a past management cease-trade order over late financials, which appears resolved. None of this is disqualifying, but together with the missing resource it is why the honest call is a hold and the entry ladder reads wait.

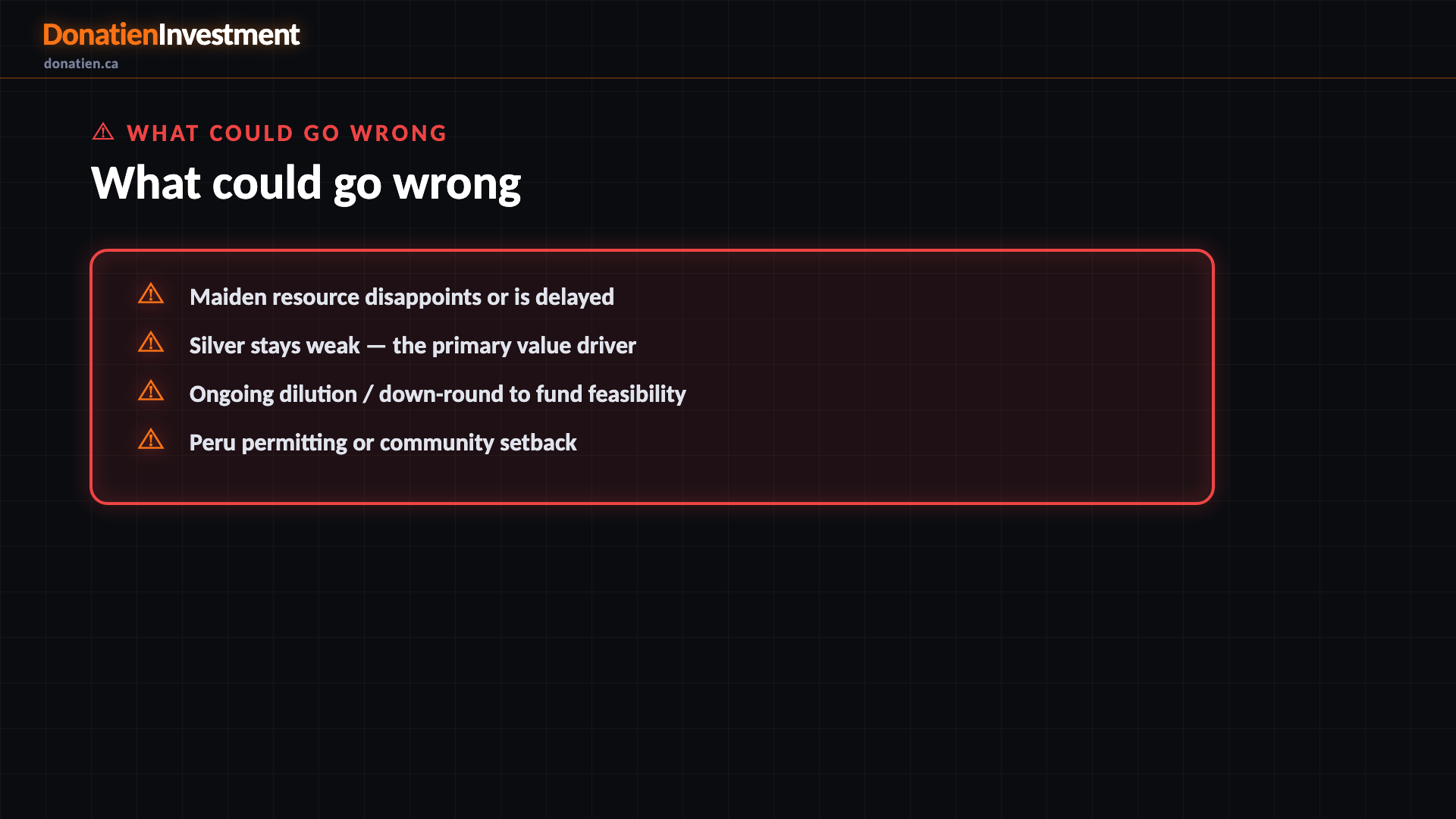

What could go wrong

Maiden resource disappoints or is delayed. Silver stays weak — the primary value driver. Ongoing dilution / down-round to fund feasibility. Peru permitting or community setback.

Risk vs Reward

The report weights three twelve-month paths, and the distribution is wide and binary around the pending resource. The base case — most likely at 50% — puts it around C$0.75 as drilling and metallurgy progress; that barely clears today's price on a full valuation, which is why it is a hold. The bull case (25%) reaches C$1.10 if a maiden resource confirms the scale story and silver recovers. The bear (25%) takes it to C$0.40 if silver stays weak or the resource slips. No entry edge until those ounces are proven.

The verdict

The bottom line: the technical story is genuinely improving — a 94% silver recovery, secured site access, a funded balance sheet and Sprott behind it. But there is still no compliant resource to value it on, the price is full for that stage, and silver is weak. So it stays a hold with the entry ladder at wait: the maiden resource is the event that decides whether this re-rates.

Read the full report on donatien.ca →{kind=link}

{kind=link}