Macro Economics SOFT LANDING / STAGFLATION

Two of the four scenarios lead, evenly matched: a soft landing — growth cools, inflation eases, the Fed can relax — and stagflation — growth slows but inflation stays sticky. They pull opposite ways, so cover both: respect the higher-for-longer market now, and hold the structural book for later.

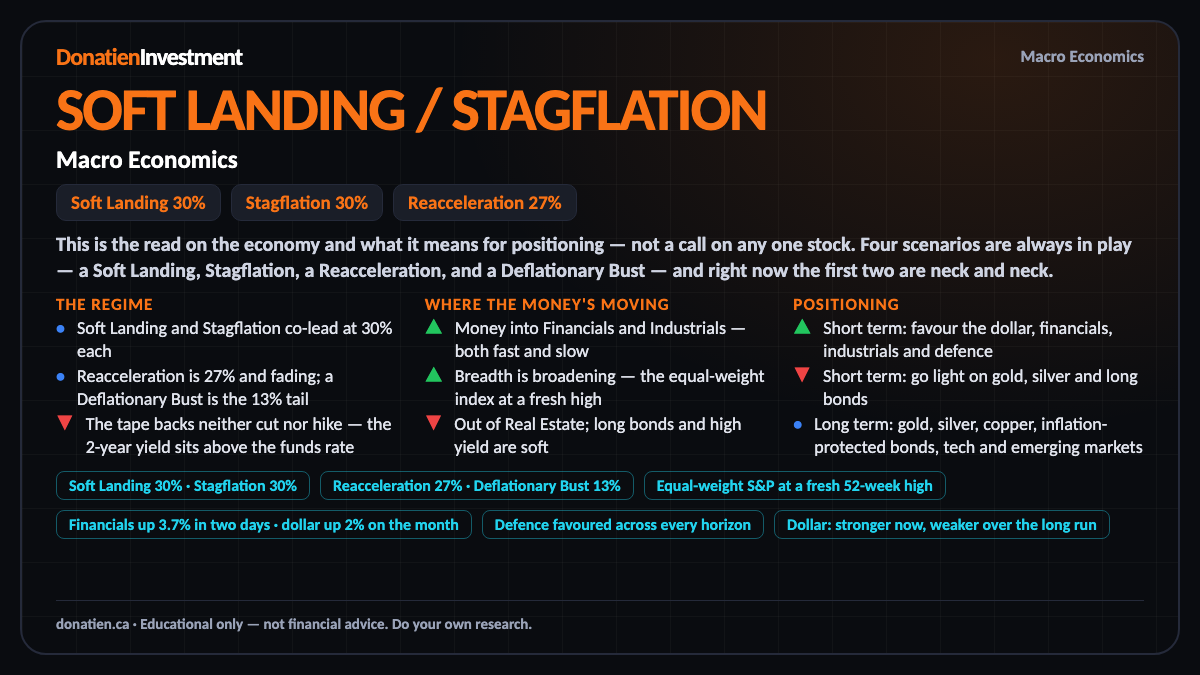

This is the read on the economy and what it means for positioning — not a call on any one stock. Four scenarios are always in play — a Soft Landing, Stagflation, a Reacceleration, and a Deflationary Bust — and right now the first two are neck and neck.

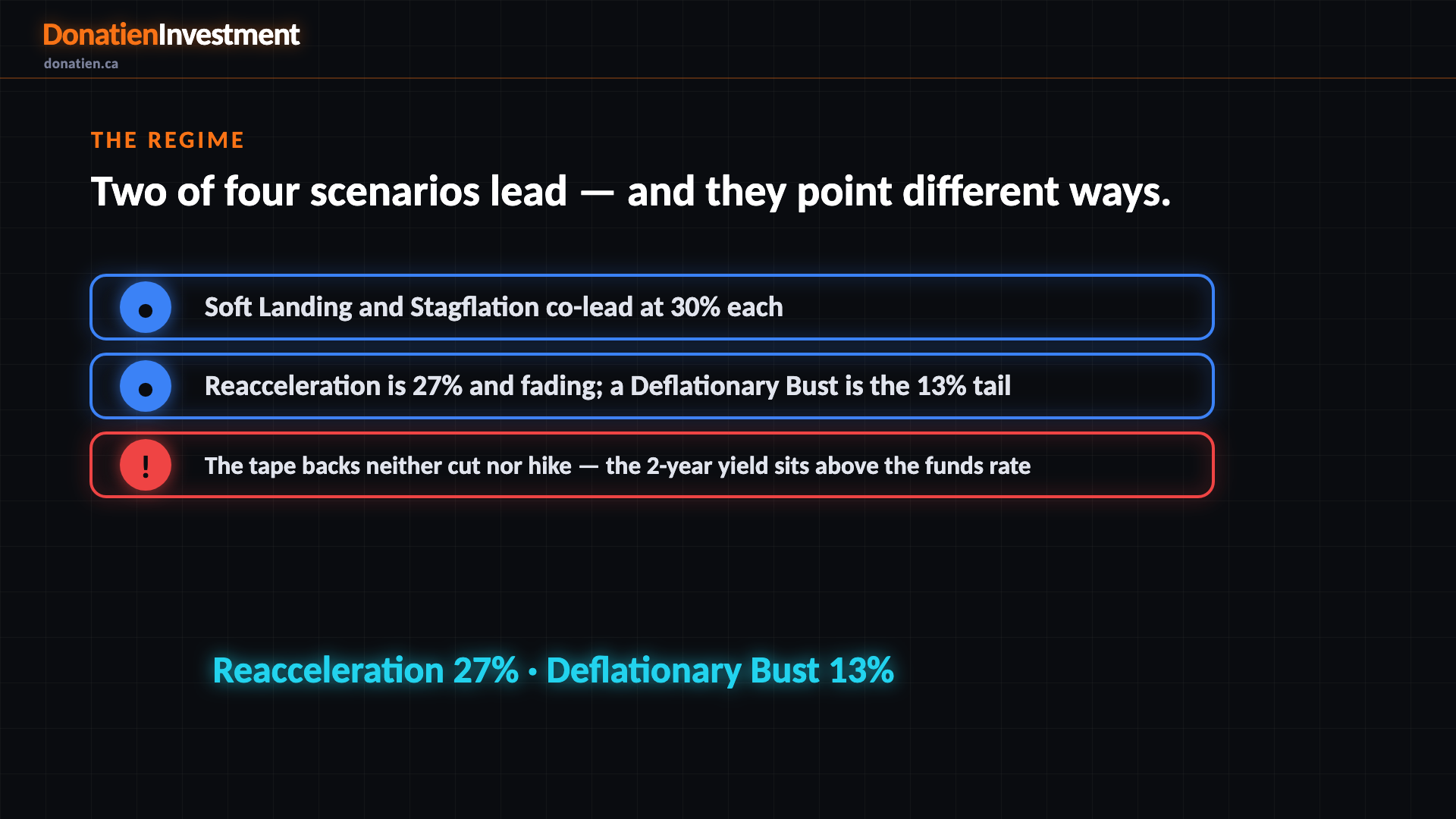

The regime

Four scenarios are always in play, and today two lead. A soft landing — where growth eases and inflation cools — and stagflation — where growth slows but inflation stays sticky — are level at 30% each. A reacceleration, the economy running hot again, is 27% and fading; a deflationary bust is the 13% tail. The two leaders point opposite ways, and the tape backs neither a cut nor a hike: the 2-year yield sits above the funds rate, the dollar is up 2%, and gold, silver and copper are falling.

Soft Landing 30% · Stagflation 30% · Reacceleration 27% · Deflationary Bust 13%

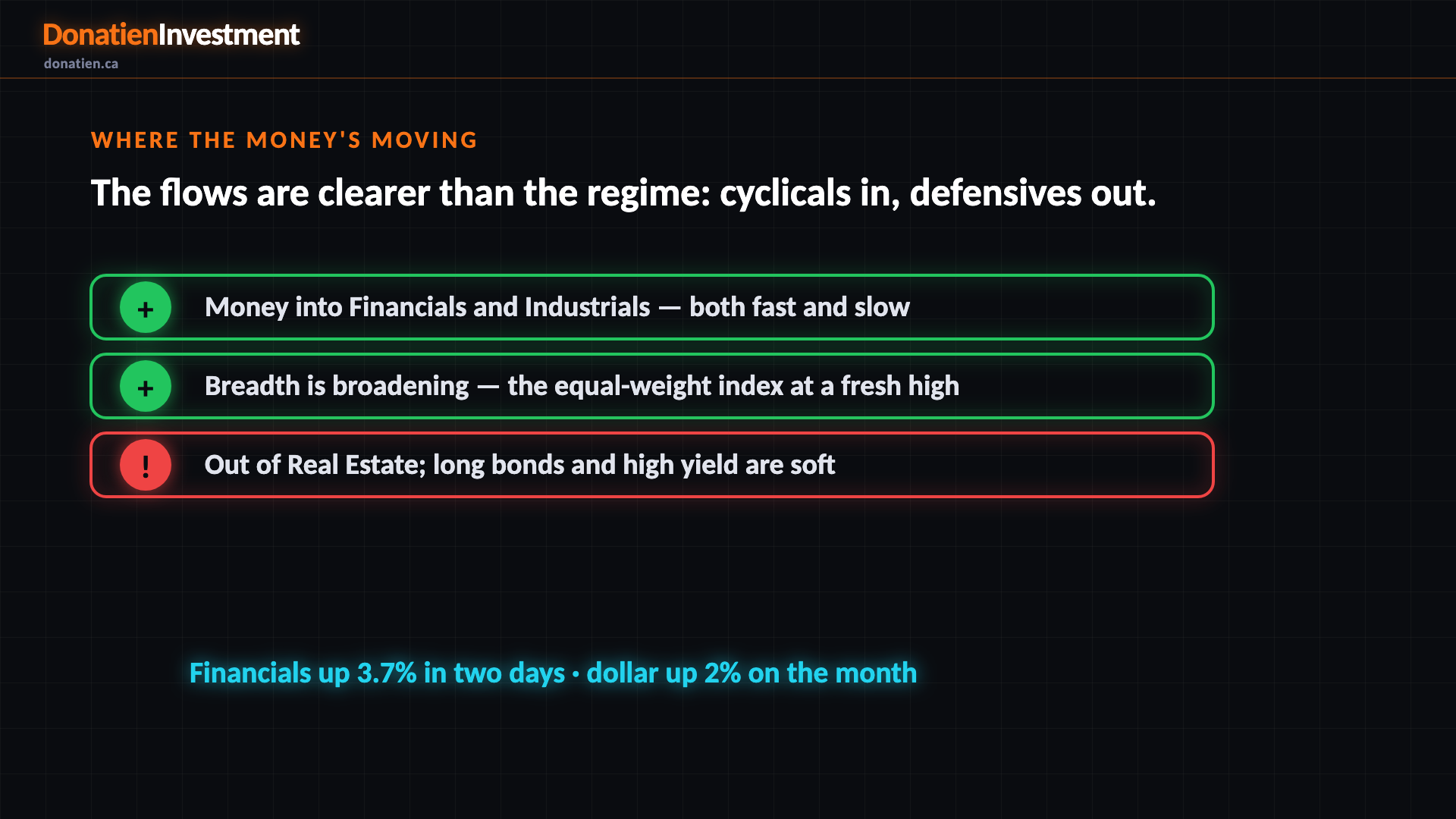

Where the money's moving

Capital is doing something clearer than the regime. Both slow, structural money and fast, tactical money are flowing into financials and industrials. Breadth is broadening — the equal-weight index just made a fresh high while the headline index hasn't — which lowers the risk of a top-heavy market. Money is leaving real estate, and long bonds and high yield are soft on the higher-for-longer tape.

Equal-weight S&P at a fresh 52-week high · Financials up 3.7% in two days · dollar up 2% on the month

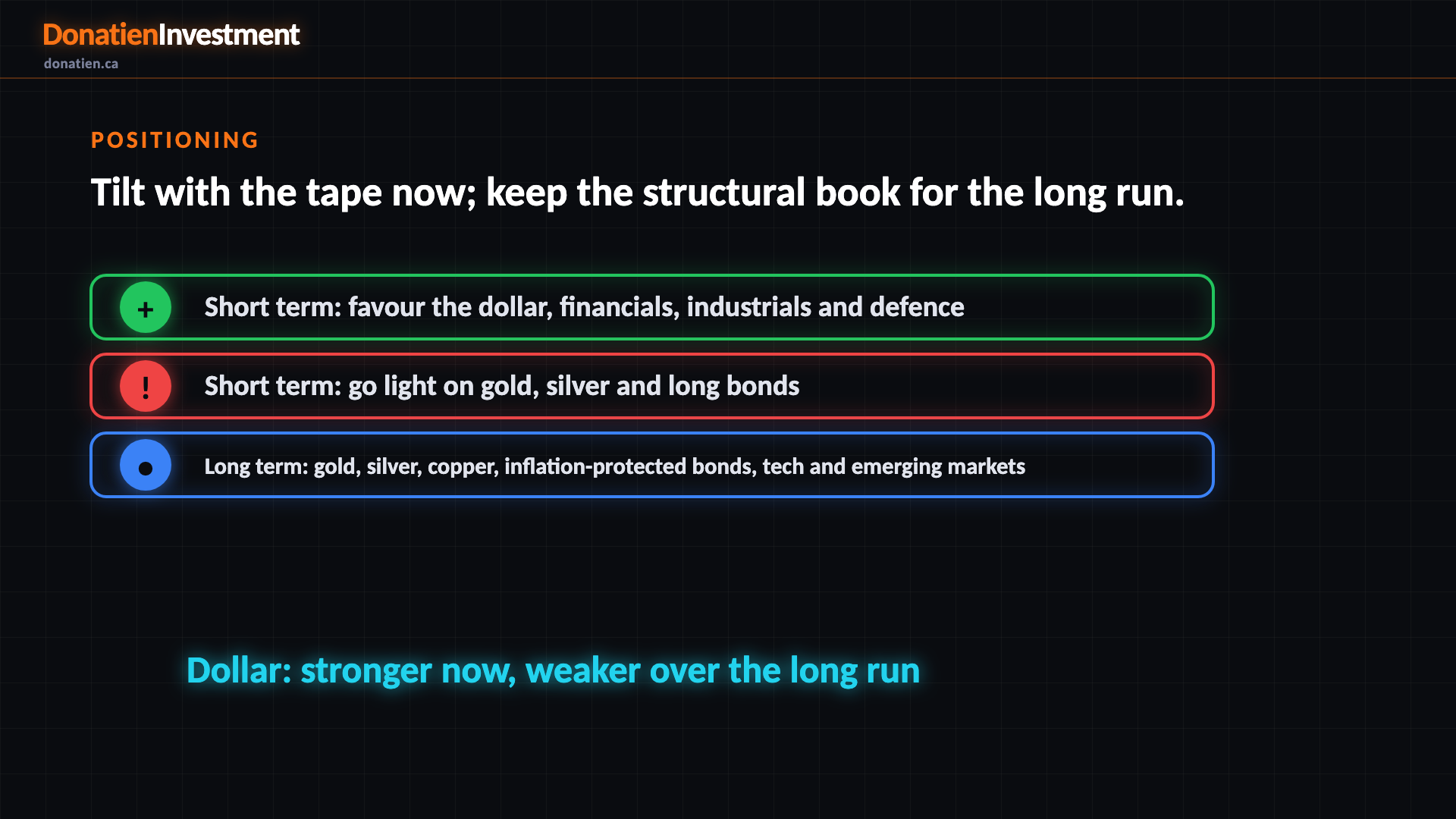

Positioning

So positioning splits by horizon. Near term, tilt with the tape: favour the dollar, financials, industrials and defence, and go light on the precious metals and long bonds while the downtrend runs. But the long book is unchanged — gold, silver, copper, inflation-protected bonds, technology and emerging markets all screen well over years, and the dollar screens weak long term as de-dollarisation grinds on.

Defence favoured across every horizon · Dollar: stronger now, weaker over the long run

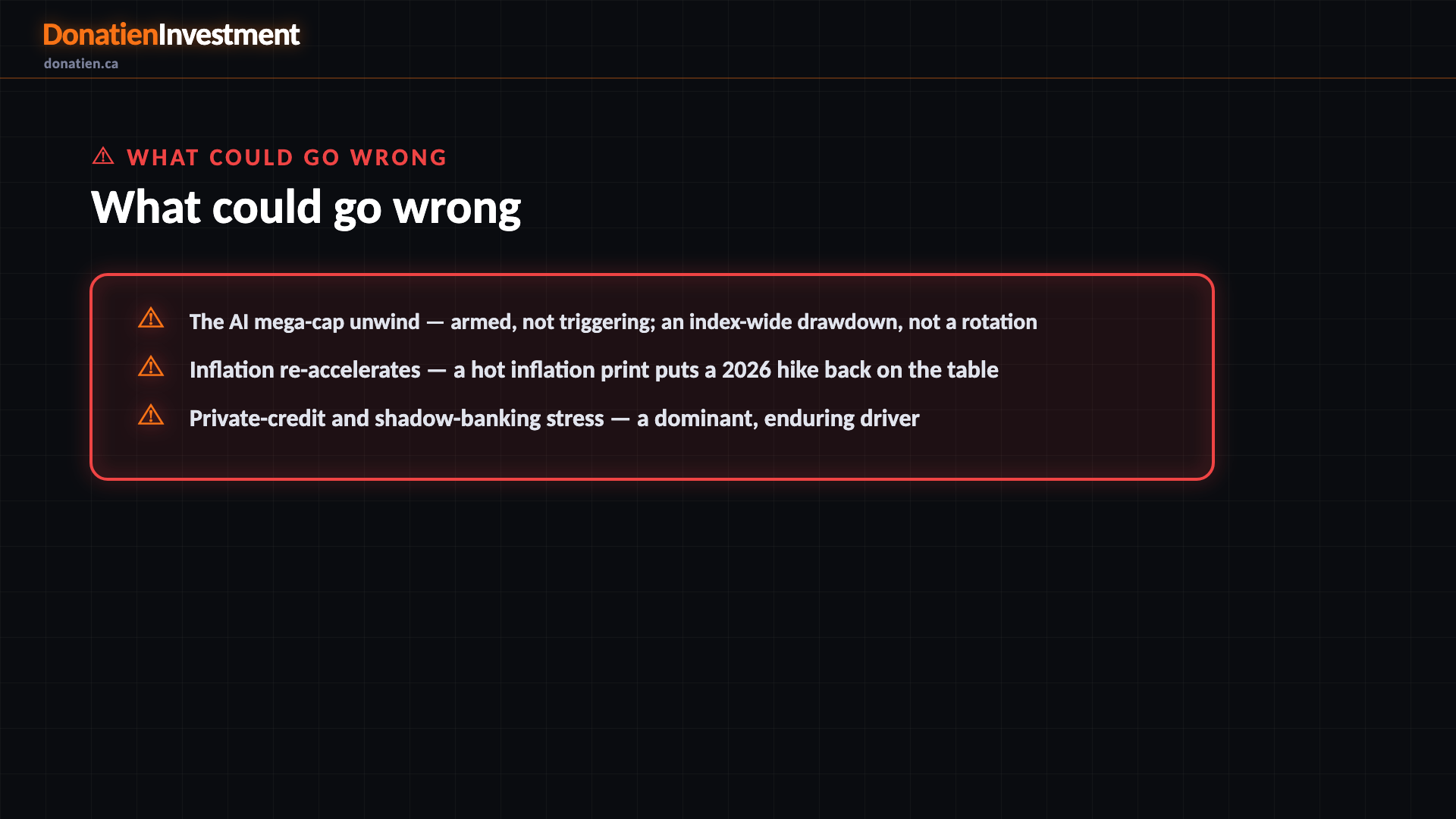

What could go wrong

The biggest tail risk is the one that's armed but not triggering. The S&P 500 is led by a handful of AI mega-caps on partly non-operating earnings, so it has no diversification cushion — a reversal there is an index-wide drawdown, not a rotation. For now breadth is broadening, which holds it off. Beyond that: inflation re-accelerating and putting a 2026 hike back in play, and stress in private credit.

Risk vs Reward

The four scenarios sit close together. Soft Landing and Stagflation co-lead at 30% each; Reacceleration is 27% and fading; a Deflationary Bust is 13%. Nothing has separated — the top two just point opposite ways, which is why you cover both rather than lean hard on one.

The verdict

The two live scenarios are a soft landing and stagflation, evenly matched — one wants you leaning into risk, the other into inflation hedges — so the honest answer is to cover both. Near term, respect the tape: the dollar is firm, precious metals are soft, and cyclicals and financials are bid. Longer term, hold the structural book — gold, silver, copper, inflation-protected bonds, technology and emerging markets. The next tells are the ISM Services survey, then the inflation print on the 14th.

Read the full report on donatien.ca →{kind=link}

{kind=link}