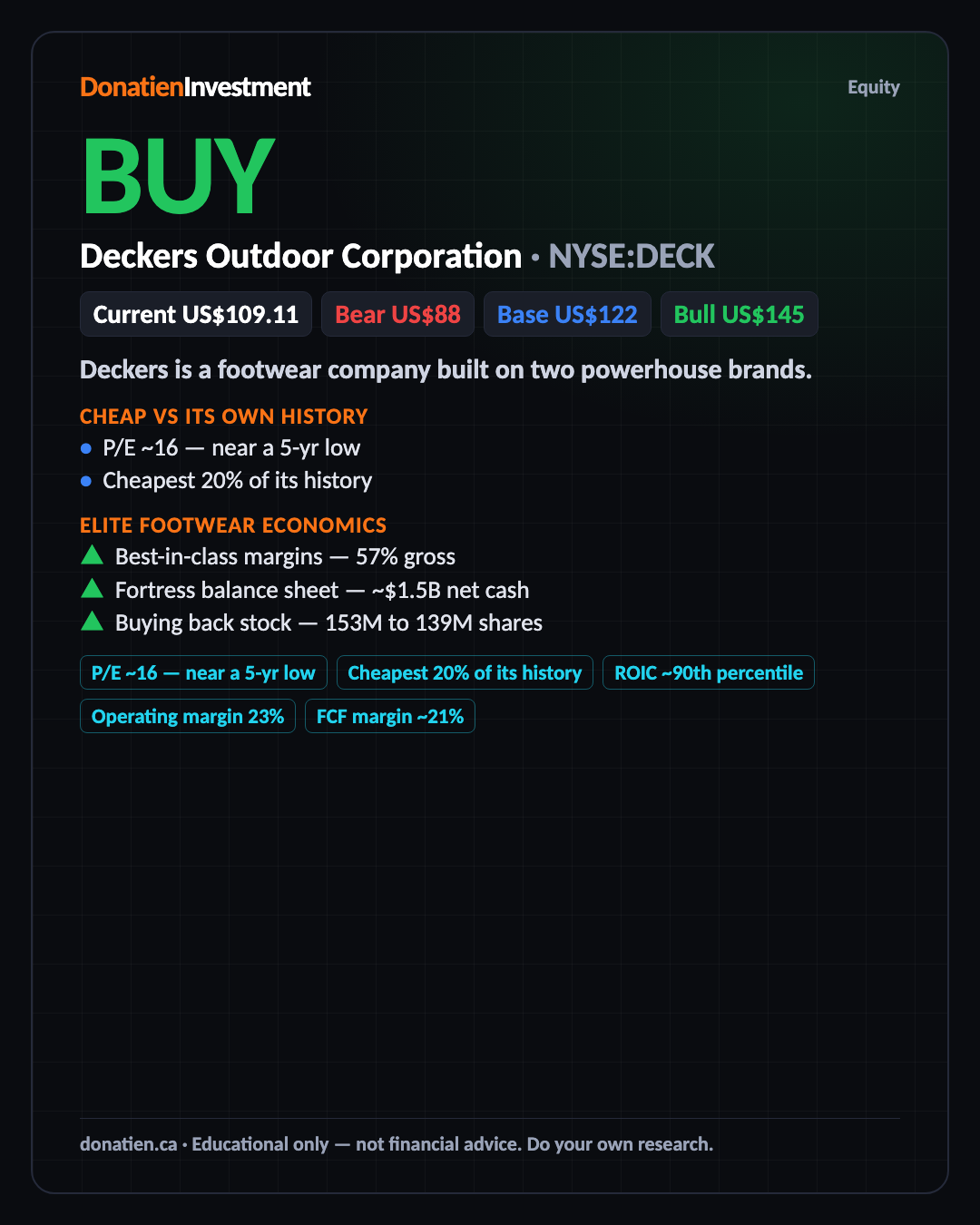

Deckers Outdoor Corporation (NYSE:DECK) BUY

an elite footwear maker behind UGG and HOKA, with fortress finances, trading near a 5-year-low valuation as the market frets about slowing growth.

So what is it? Deckers is a footwear company built on two powerhouse brands. UGG, the sheepskin boot that somehow never goes out of style, and HOKA, the chunky running shoe that's exploded with runners worldwide. It also owns Teva sandals. These are premium names that sell at full price, and Deckers turns that into extraordinary cash. It's a brand machine, not just a shoemaker.

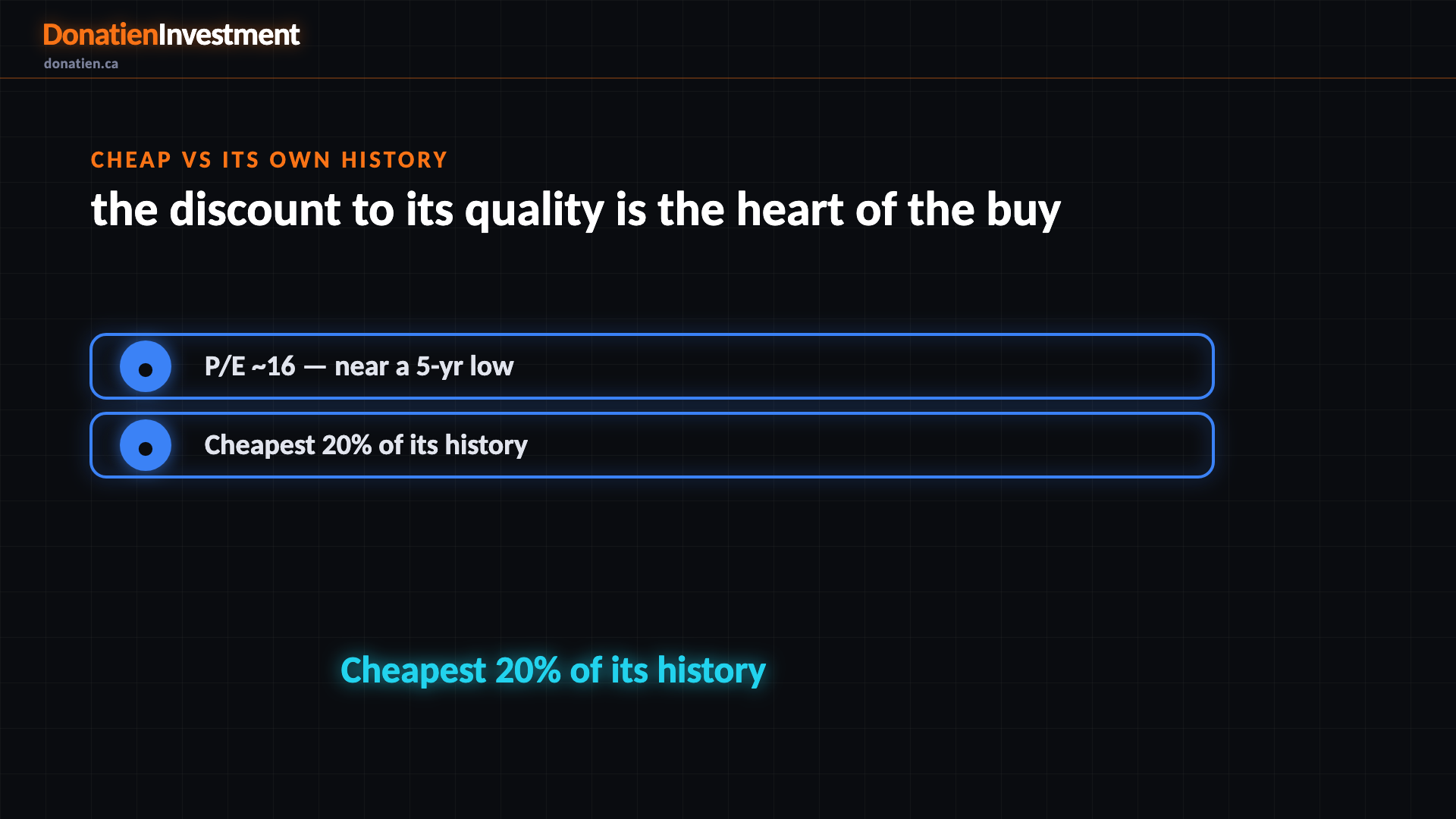

Cheap vs its own history

And here's the opportunity. Deckers throws off cash like few retailers can — a free-cash-flow yield around eight and a half percent, with margins that rival luxury goods. Yet after a recent dip, the market is valuing it near the bottom of its five-year range, worried that growth is slowing. You're being offered a top-tier business at a discount price.

P/E ~16 — near a 5-yr low · Cheapest 20% of its history

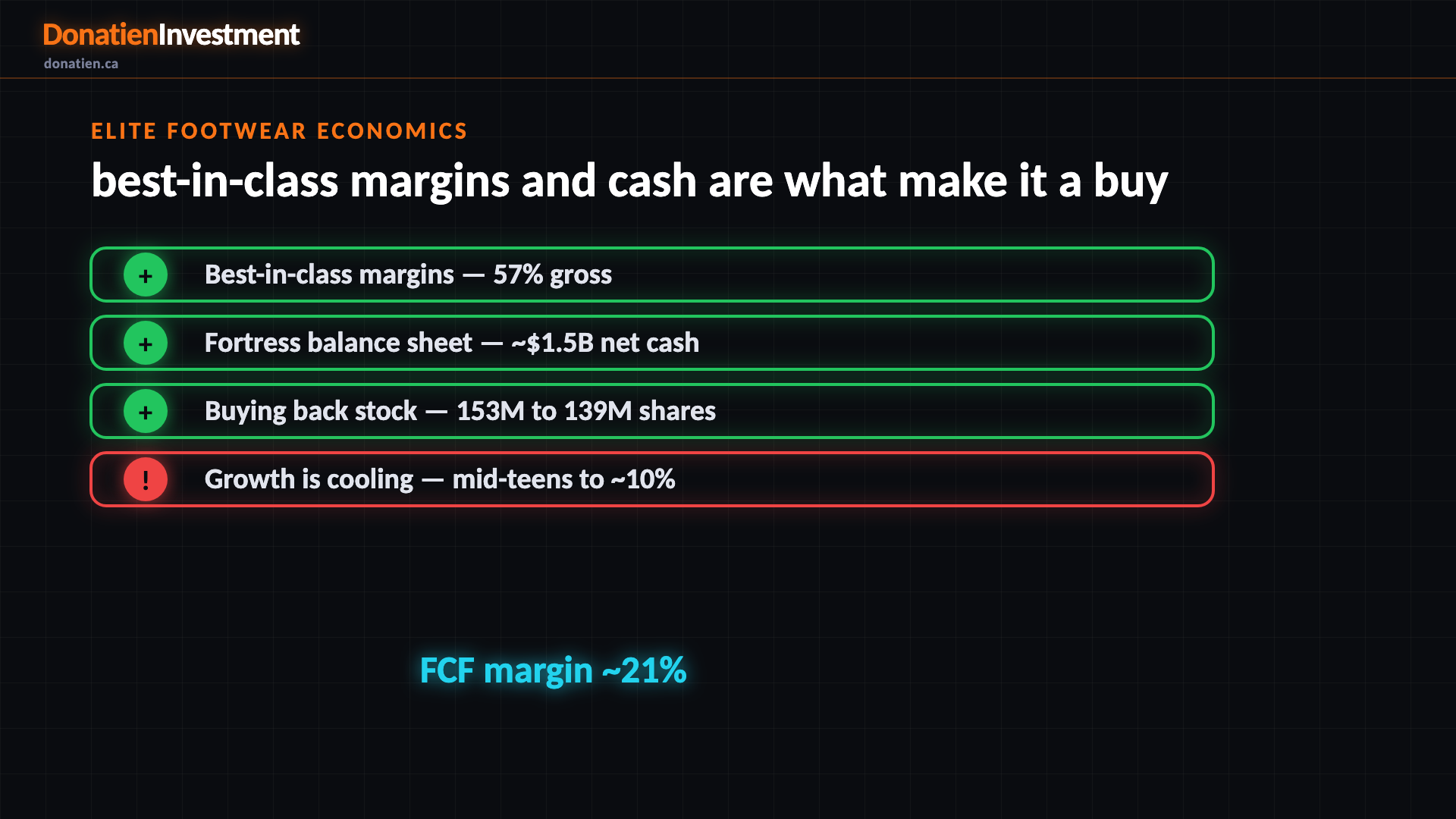

Elite footwear economics

Why do we like it? Because the economics are exceptional. Its gross margin tops fifty-seven percent — richer than Nike's — and it converts nearly all of its profit into cash. The balance sheet is a fortress, with about one and a half billion in net cash and almost no debt, and management is using that cash to buy back stock and shrink the share count. The one honest concern: after years of mid-teens growth, the top line is cooling toward ten percent.

ROIC ~90th percentile · Operating margin 23% · FCF margin ~21%

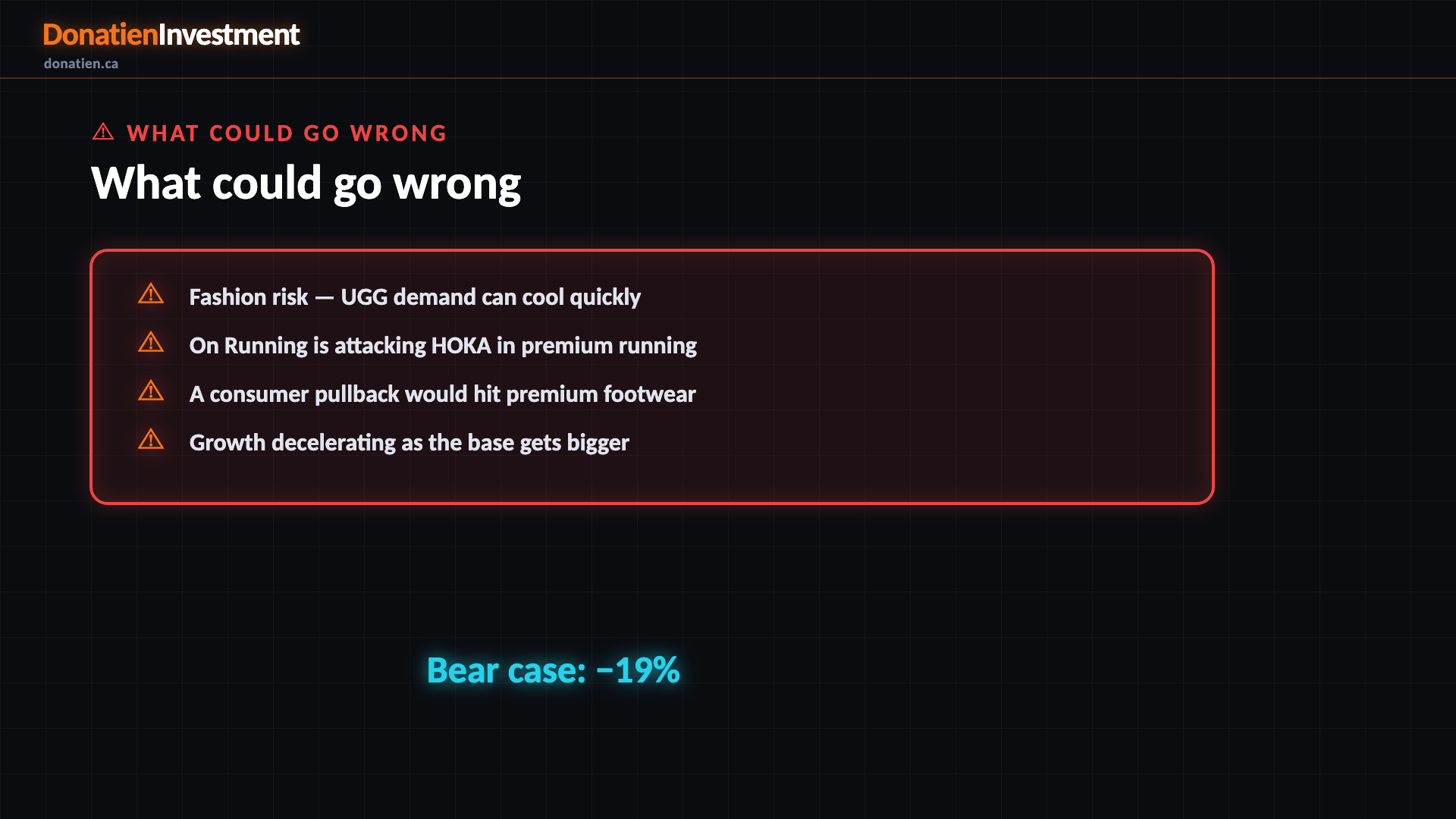

What could go wrong

Now the risks, and they are real. These are fashion brands as much as franchises — UGG in particular rides trends, and shoppers switch shoes easily. In running, the upstart On is fighting HOKA hard for the premium runner. And because these are pricey, discretionary purchases, a genuine downturn in consumer spending would bite. None of these break the story today, but they're why you size it sensibly and watch it closely.

Risk vs Reward

So weigh the risk against the reward. From around a hundred and nine dollars today, our base case — and the most likely — sees Deckers near a hundred and twenty-two, roughly twelve percent higher, on steady growth and held margins. The bull case reaches a hundred and forty-five, up about a third, if HOKA reaccelerates abroad. And the downside case is near eighty-eight, down nineteen percent, if the brands cool and spending contracts. Blend those together and the odds tilt in your favour — for a quality business you are buying cheap.

The verdict

So, the bottom line. Deckers is one of the best-run businesses in footwear — two powerful brands, fortress finances, and a shrinking share count — on offer near a five-year-low valuation because the market is fixated on slowing growth. We rate it a buy across every horizon: accumulate on weakness and let the cash compounding work. Remember, this is for education, not financial advice; always do your own research. This analysis is by Donatien Investment, at donatien.ca. The link to the full report is in the video notes below. Have a great day.

Read the full report on donatien.ca →{kind=link}

{kind=link}