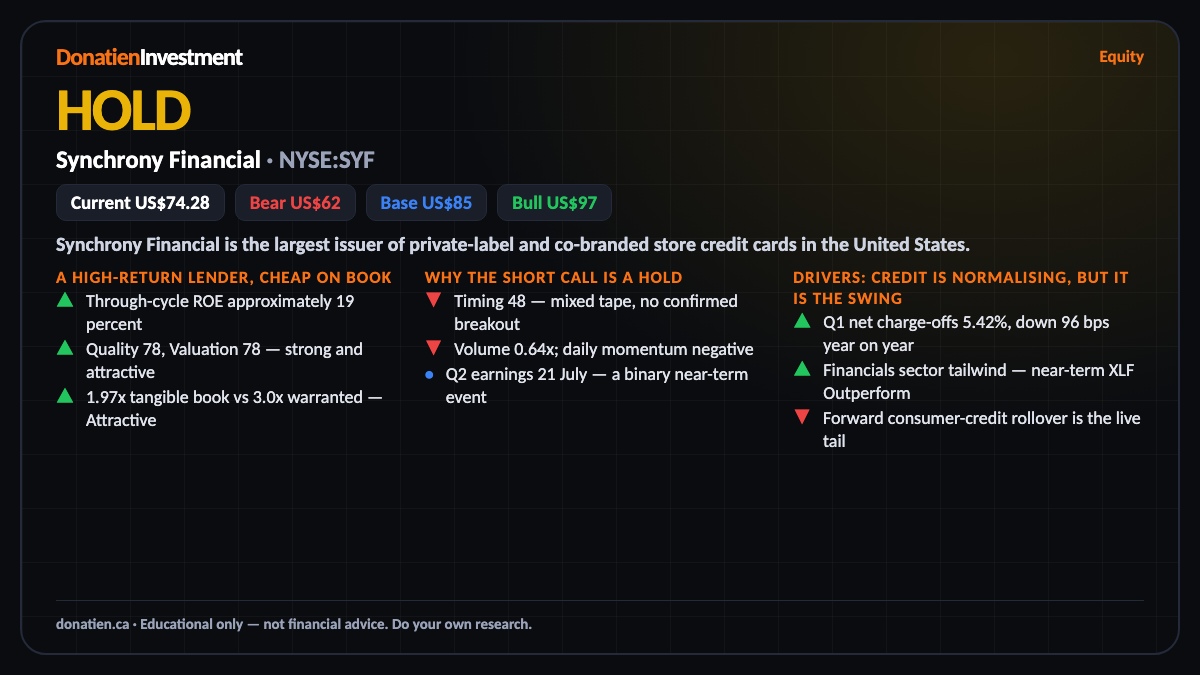

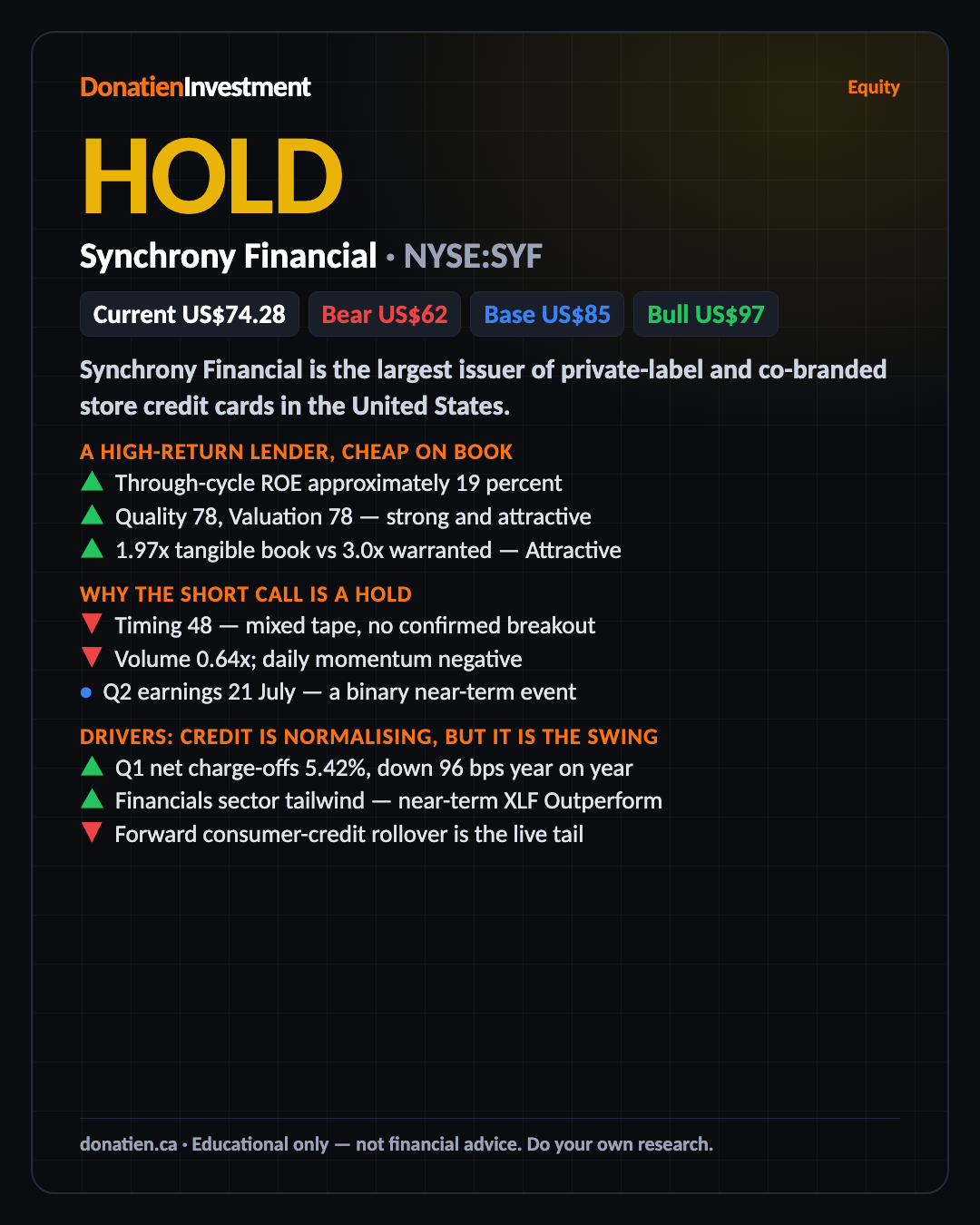

Synchrony Financial (NYSE:SYF) HOLD

Synchrony is a high-return consumer-credit franchise trading at under two times tangible book, and the medium and long calls are both BUY. But the short-term call is HOLD: Q2 earnings land on 21 July, the tape has not turned, and there is no discounted entry yet. Buy on confirmation after the print, or on a pullback into support.

Synchrony Financial is the largest issuer of private-label and co-branded store credit cards in the United States. It funds roughly one hundred billion dollars of card loans with its own online deposits and earns the spread. The report rates it HOLD short-term, BUY medium and long, at a price of 74.28 US dollars.

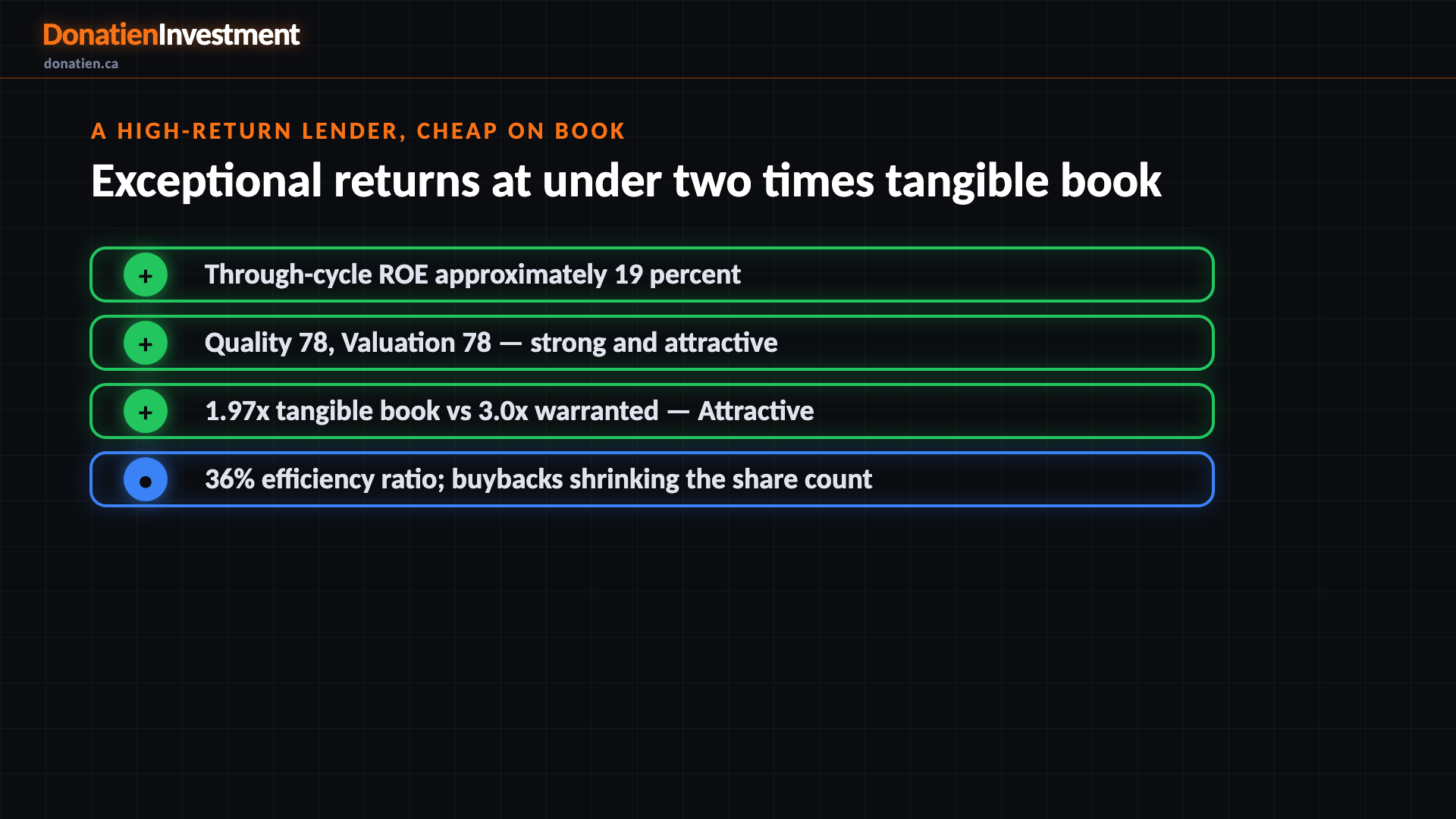

A high-return lender, cheap on book

The quality here is real. Synchrony earns a return on equity around nineteen percent through the cycle, on card economics that give it a return on assets several times a typical bank, and it runs a very lean thirty-six percent efficiency ratio. Yet the shares trade at just under two times tangible book, against a warranted multiple of three times. That is a ratio of two-thirds, squarely in the attractive band. On a clean, reserve-normalised basis the trailing price to earnings is about nine times. Cheap for the returns.

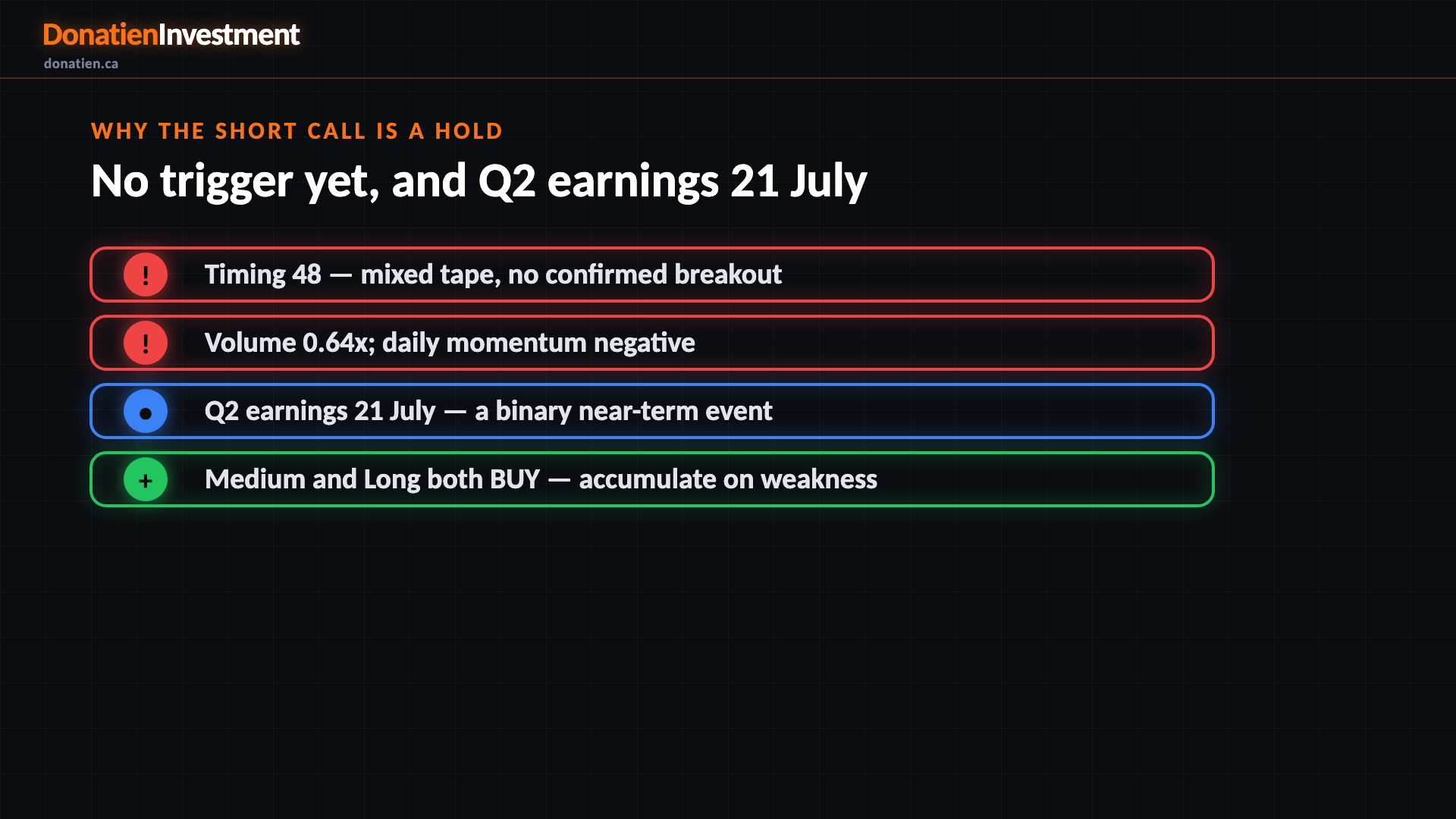

Why the short call is a hold

So why not buy today. The tape is genuinely mixed and the print in a few days dominates the near term. The monthly trend is up, but the weekly is a downtrend, the daily is only recovering, hugging its two-hundred-day average with a negative momentum reading, and volume is soft at two-thirds the twenty-day average. The price sits mid-range, a coin-flip rather than a confirmed uptrend. There is no volume-confirmed breakout, so the technical entry is unmet, and with Q2 earnings inside the window the timing is a binary event. The stock is cheap, but the entry edge is not there.

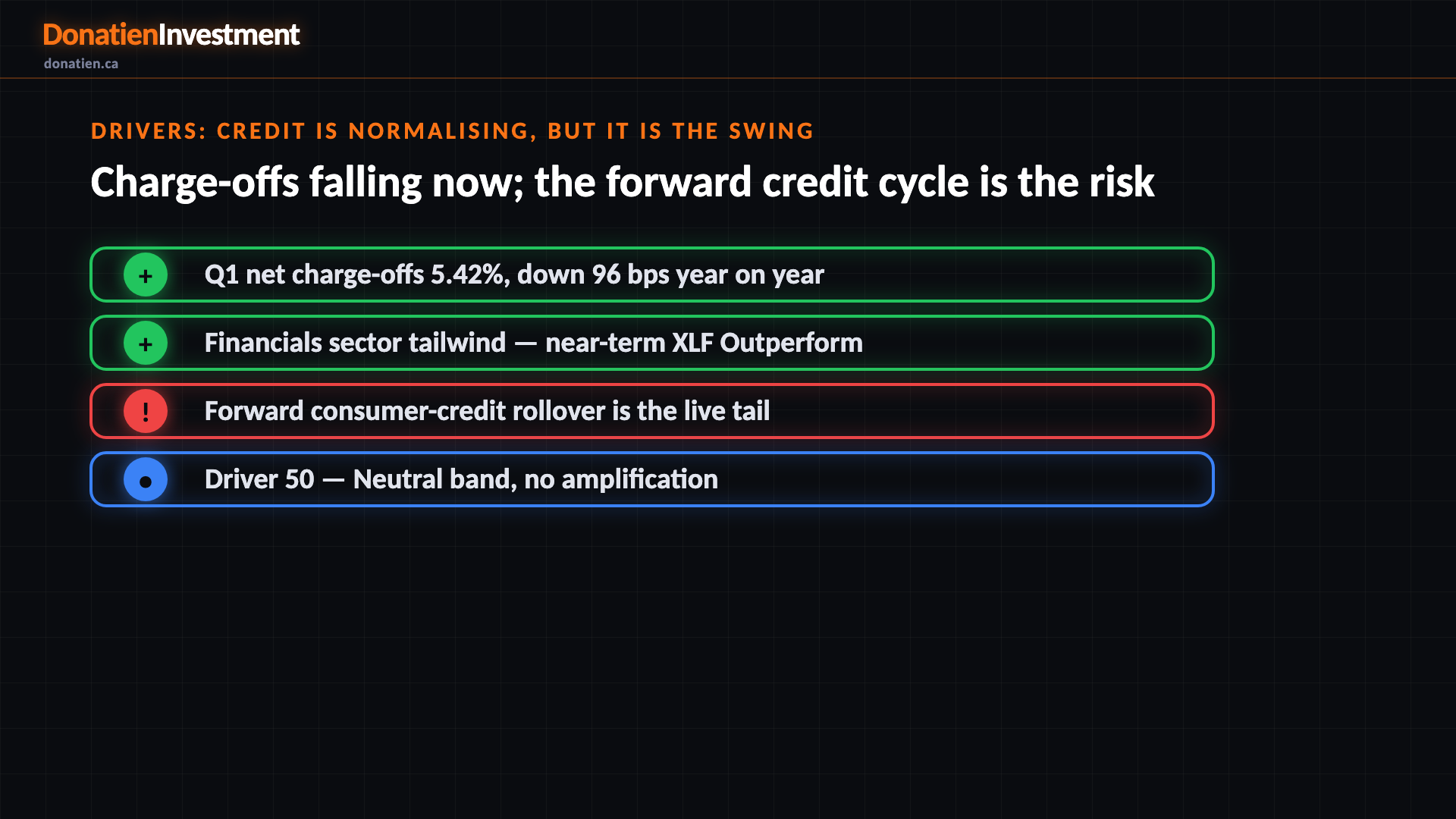

Drivers: credit is normalising, but it is the swing

The driver is the health of the everyday American consumer, and right now it is genuinely contested rather than a headwind. First-quarter net charge-offs came in at five and a half percent, down almost a full point year on year, delinquencies stabilised, and purchase volume hit a record. So credit is normalising favourably, which is why the driver scores a neutral fifty. But it is the un-hedged swing factor: the macro report flags a consumer rollover and private-credit stress as the live tail. A neutral driver does not amplify, so even with the sector tailwind this is a plain BUY, not a stronger one.

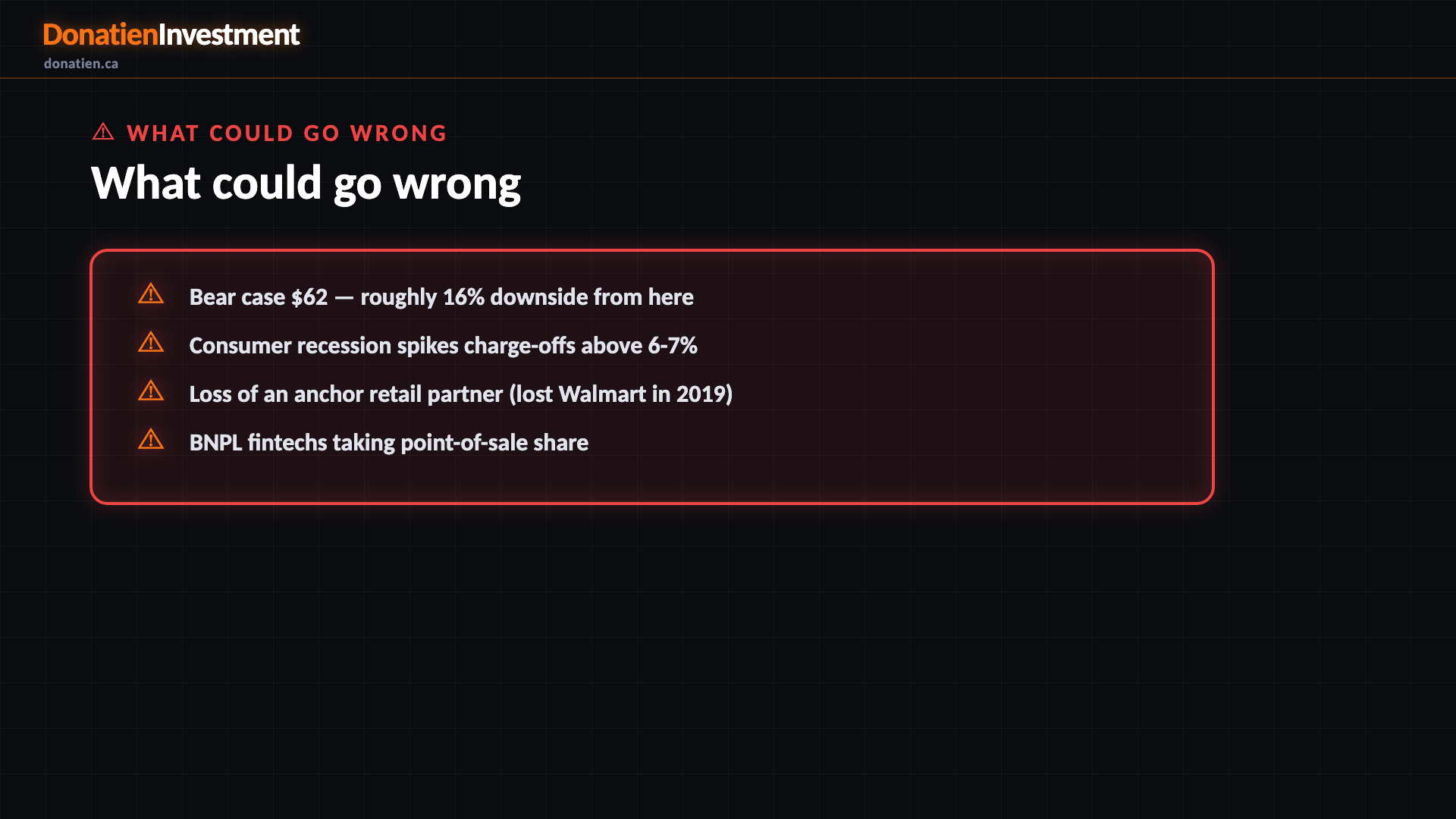

What could go wrong

The risk here is cyclical, and it is the reason the stock is cheap. The bear case sees the shares fall to about sixty-two US dollars, roughly sixteen percent below today. That takes a consumer recession spiking net charge-offs back above six or seven percent, forcing a large reserve build that craters near-term earnings, while the multiple stays cheap because the market will not pay up for a lender heading into rising losses. On top of that, Synchrony depends on a finite set of large retail-partner contracts, and losing one is a step change, not a trickle. It lost the Walmart program to Capital One in 2019, and buy-now-pay-later fintechs are chipping at the point-of-sale frontier. This is a real risk, not a distant tail.

Risk vs Reward

The base case is eighty-five US dollars at fifty-five percent, a modest re-rate toward the analyst consensus as high-teens returns compound on tangible book. The bull case is ninety-seven US dollars at twenty-five percent if credit keeps normalising and the cyclical discount narrows. The bear case is sixty-two US dollars at twenty percent if the consumer-credit cycle turns. The probability-weighted centre of gravity is the base case, about twelve percent above today.

The verdict

The honest read is a hold now, a buy later. Synchrony is a genuinely high-return consumer lender, and at under two times tangible book it is cheap for the quality, which is why the medium and long calls are both buy. But the short-term stance is hold: the tape has not turned, there is no volume-confirmed trigger, and Q2 earnings land on the twenty-first of July. The plan is to accumulate on weakness or buy on confirmation after the print, not to chase it into the event. This is analysis, not financial advice.

Analysis, not financial advice. Financial Freedom. Together.

Read the full report on donatien.ca →{kind=link}

{kind=link}