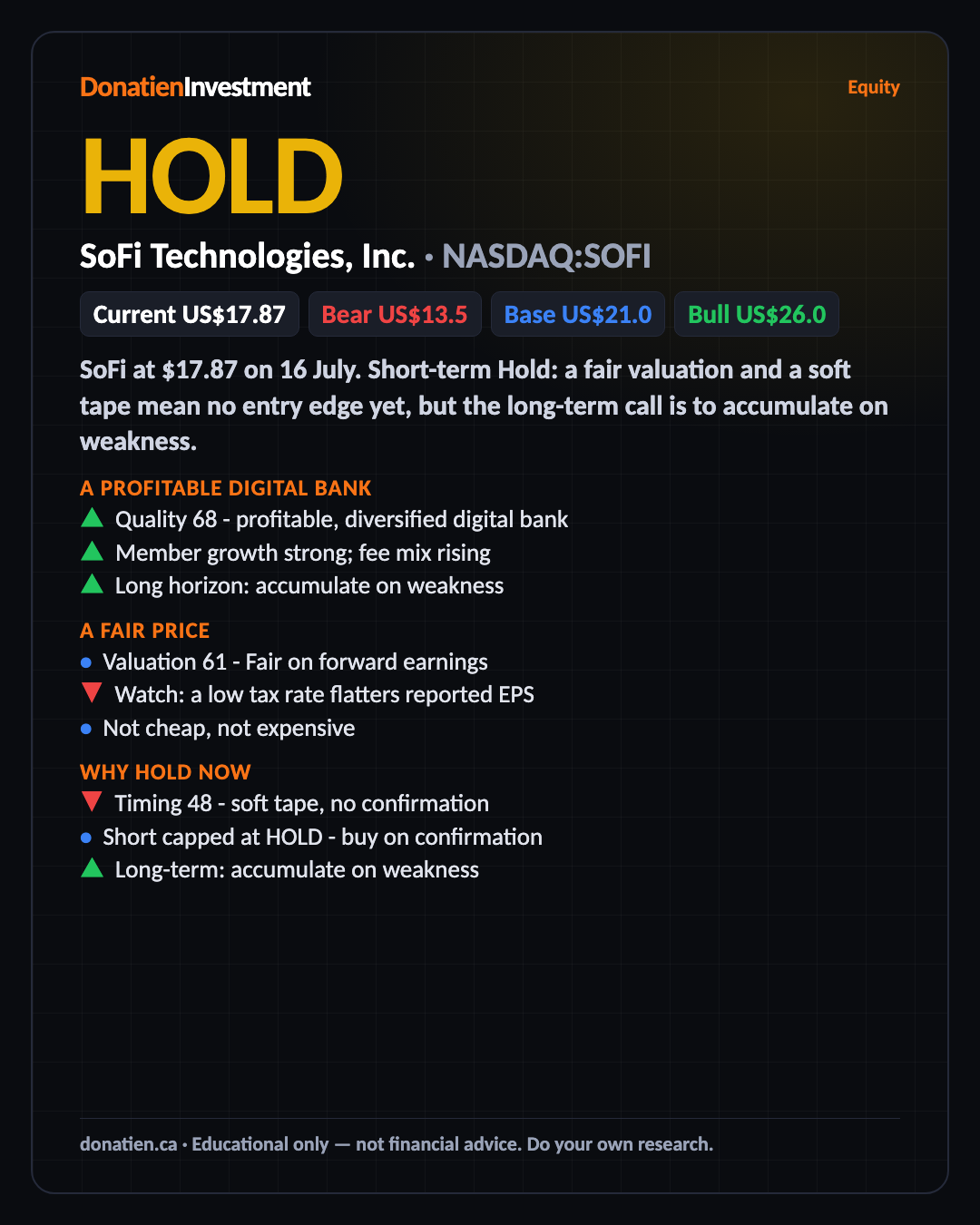

SoFi Technologies, Inc. (NASDAQ:SOFI) HOLD

A profitable, fast-growing digital bank at a fair price - a hold on the tape now, one to accumulate for the long term on weakness.

SoFi at $17.87 on 16 July. Short-term Hold: a fair valuation and a soft tape mean no entry edge yet, but the long-term call is to accumulate on weakness.

A profitable digital bank

SoFi scores 68 on quality, a profitable, fast-growing digital bank with a growing fee business. Member growth is strong. The mix is broadening beyond lending, and it is a solid, improving franchise. The long-term call is a Buy on weakness - the near-term caution is about the entry, not the business.

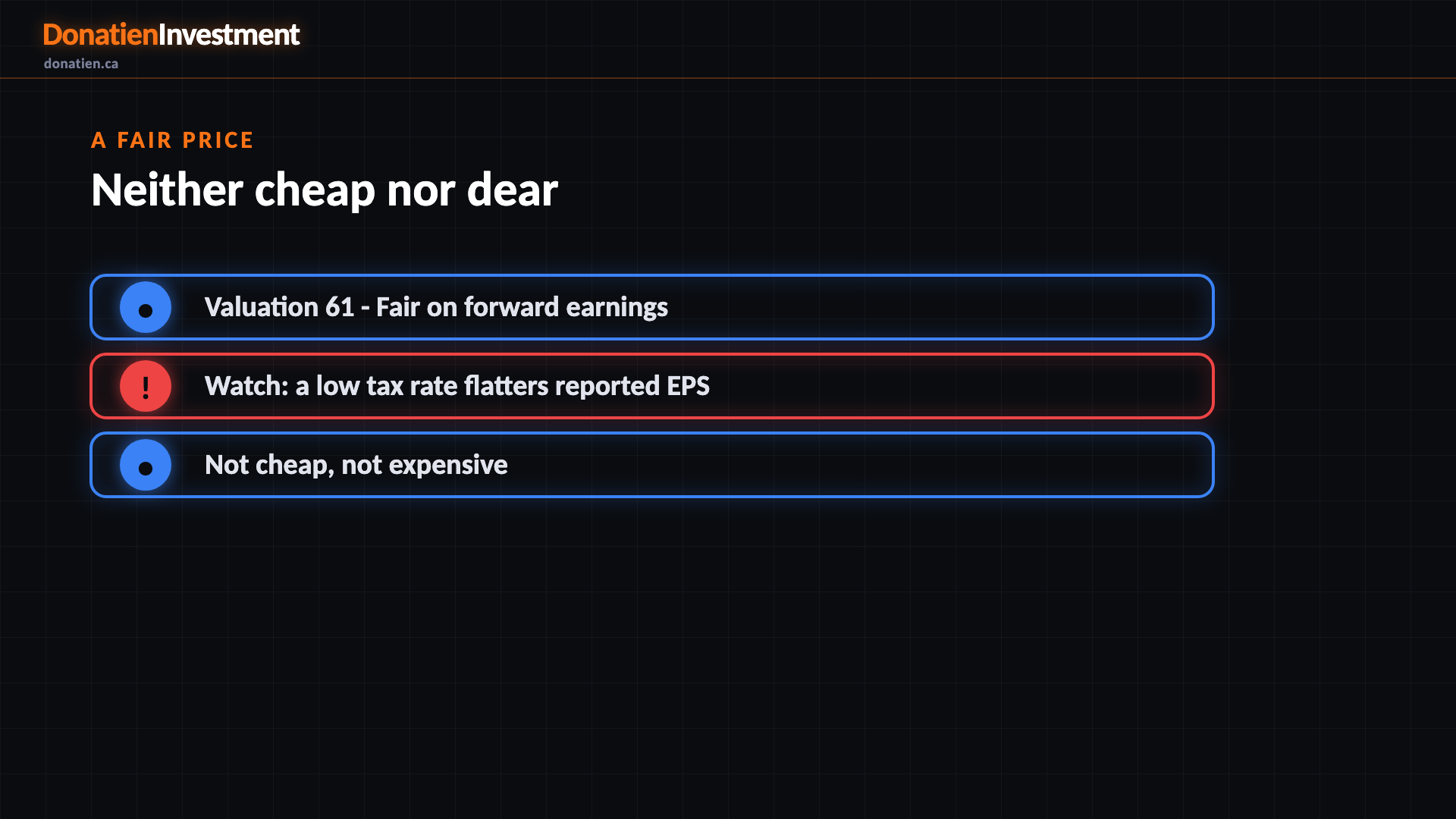

A fair price

The valuation is fair at 61, trading close to where a compounder like this should trade on forward earnings. One honest caveat: an unusually low tax rate is flattering the trailing earnings, so we normalise it and lean on forward numbers. On that basis it is neither cheap nor expensive - fairly priced for the growth. That is why it is a Hold rather than a Buy on valuation alone.

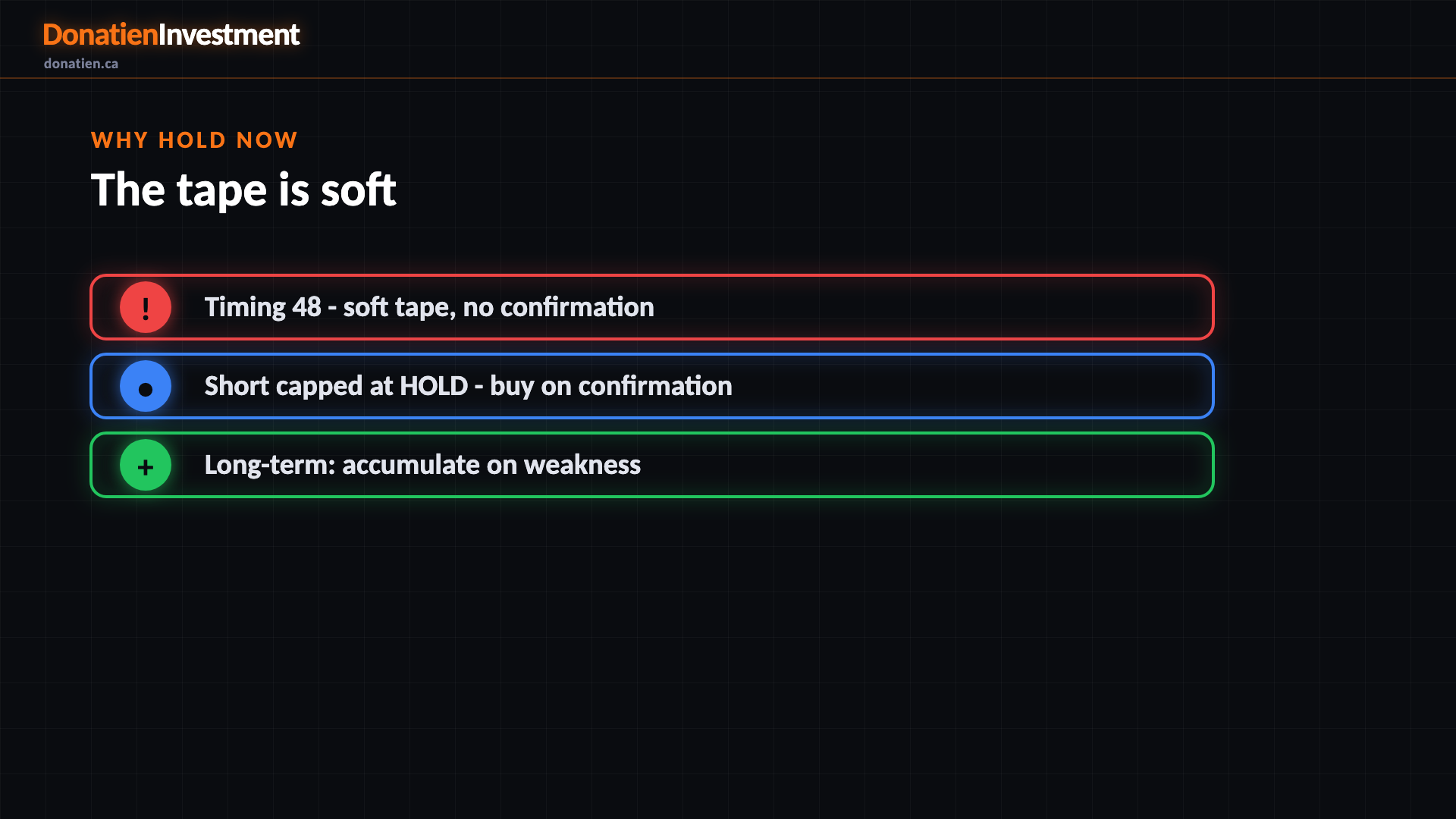

Why Hold now

So why Hold right now? The tape is soft, with bearish confluence and no confirmed entry trigger in the window. So the short-term signal is capped at Hold rather than a Buy. The longer-term plan is different and clear: accumulate on weakness. This is a name to build patiently on dips, not to chase on a soft chart.

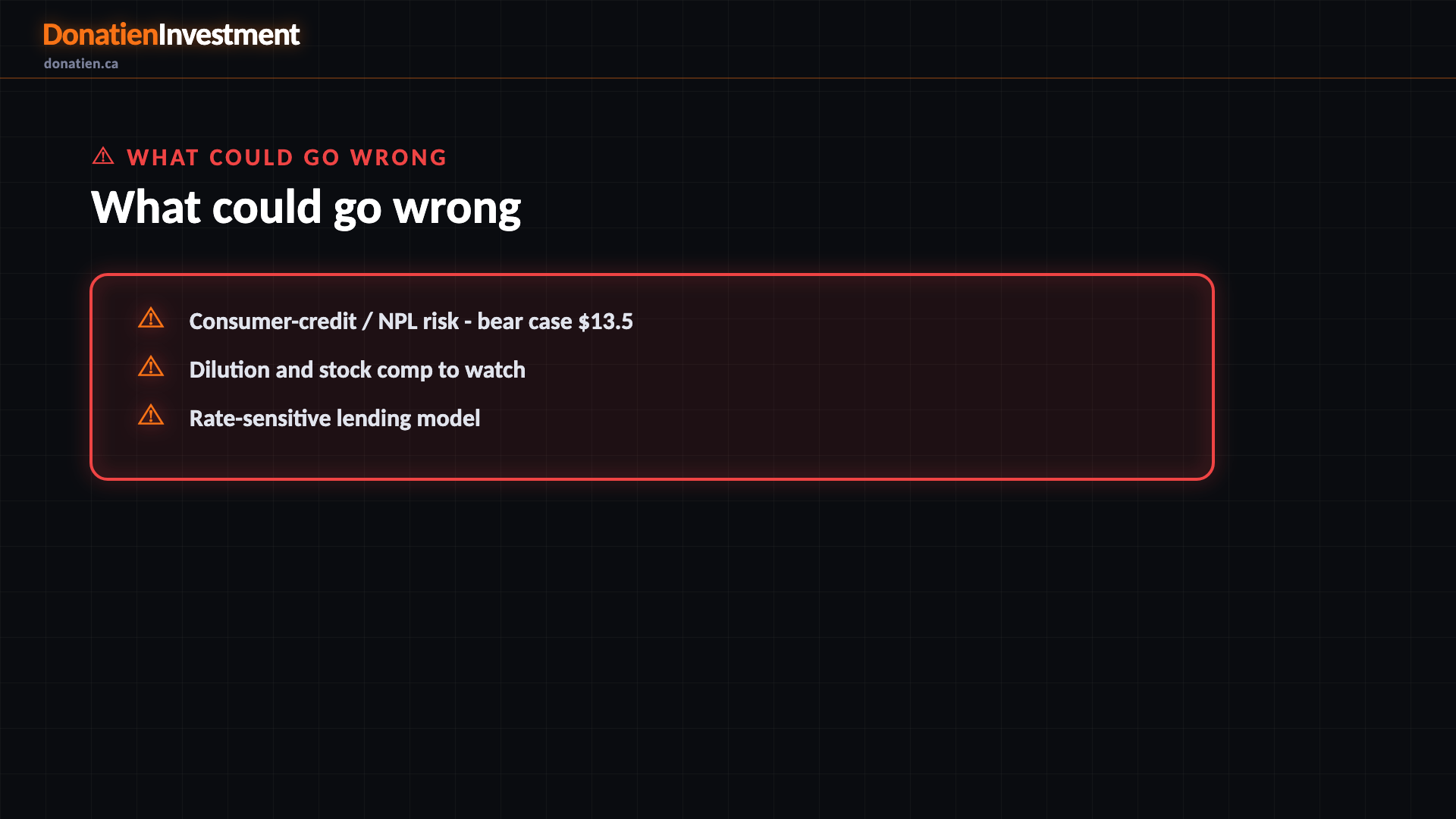

What could go wrong

The risks are consumer credit and dilution. A softening consumer could lift loan losses, and the bear case sits near 13.50. Share issuance and stock compensation are a watch-item, and the lending model is rate-sensitive. Hold reflects that near-term uncertainty and the soft tape - a quality name to accumulate on weakness for the long term; base case 21, bull 26.

Risk vs Reward

Against the current US$17.87, the report frames a bull case at US$26.0 (+45%), a base case at US$21.0 (+18%) and a bear case at US$13.5 (-24%). See the full report for the probability weight behind each path.

The verdict

A profitable, fast-growing digital bank at a fair price - a hold on the tape now, one to accumulate for the long term on weakness.

Read the full report on donatien.ca →{kind=link}

{kind=link}