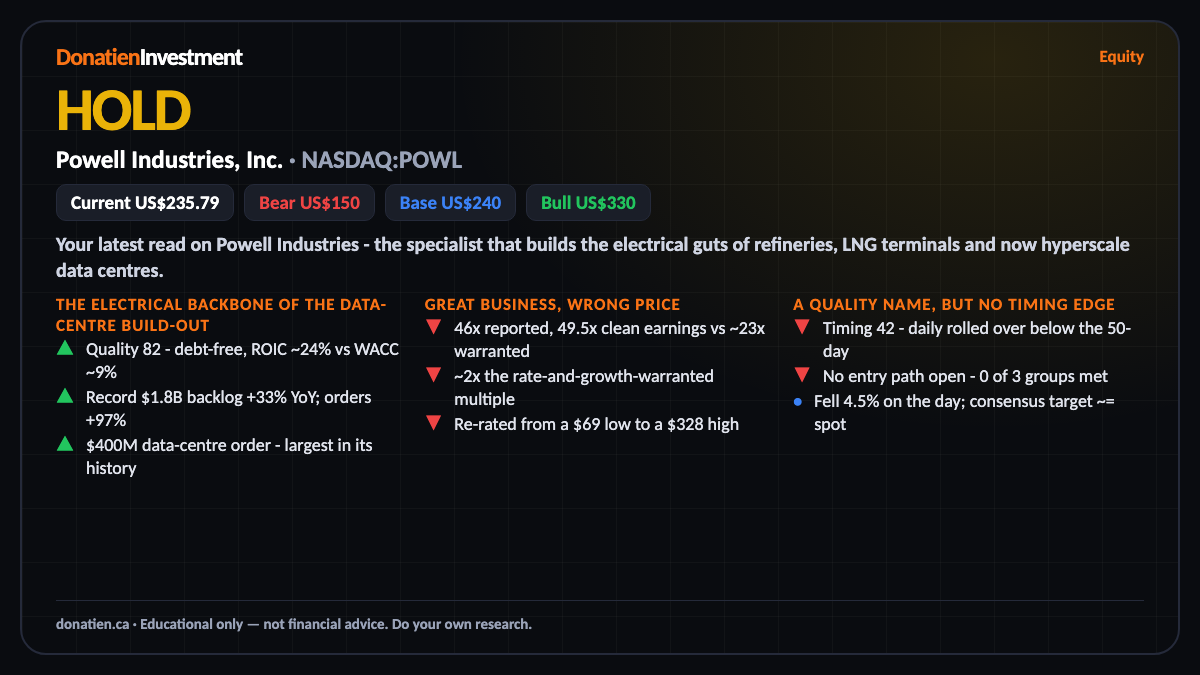

Powell Industries, Inc. (NASDAQ:POWL) HOLD

A superb, debt-free maker of the electrical backbone for data centres - but priced at roughly twice its warranted multiple, so a hold until the price comes to you.

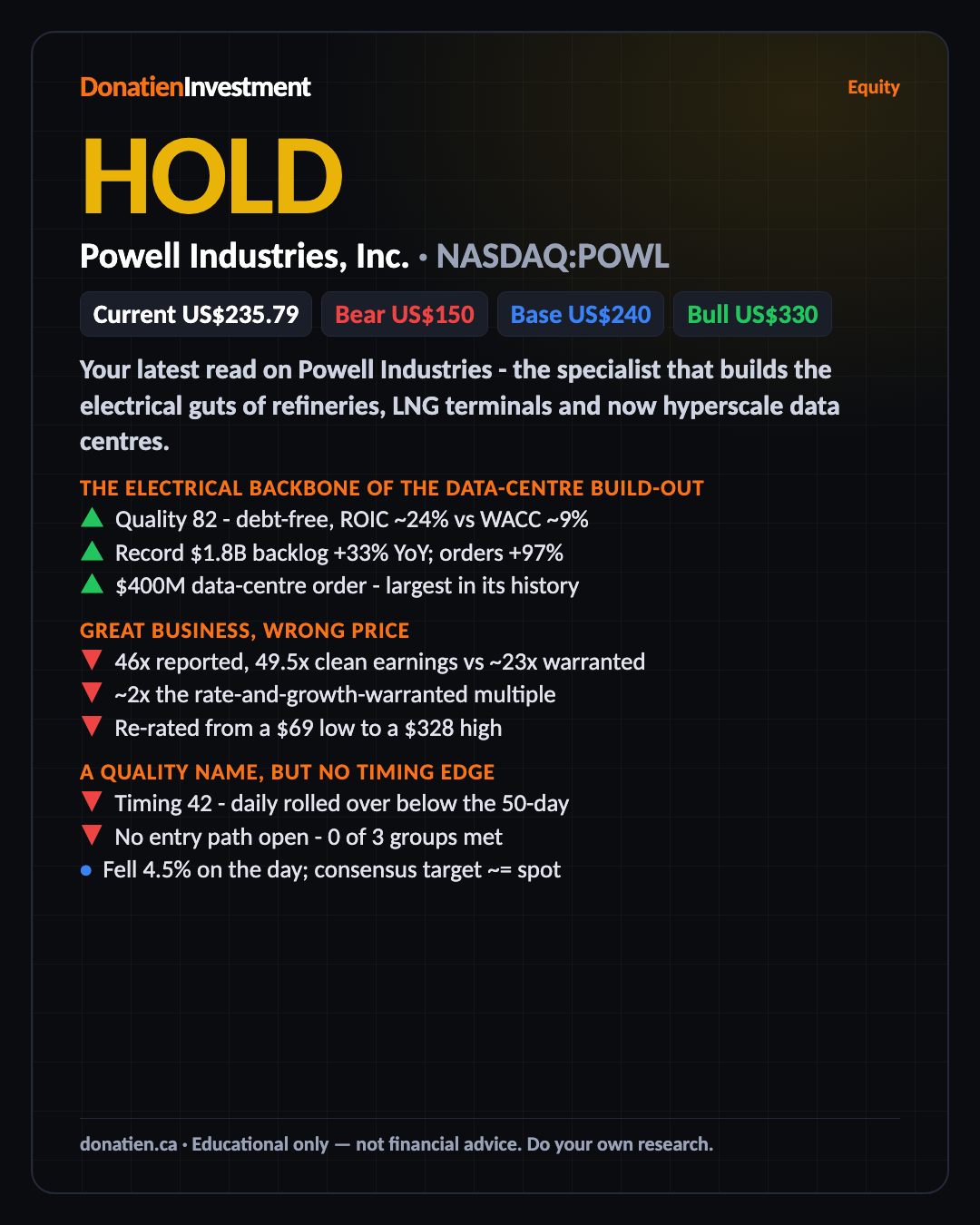

Your latest read on Powell Industries - the specialist that builds the electrical guts of refineries, LNG terminals and now hyperscale data centres.

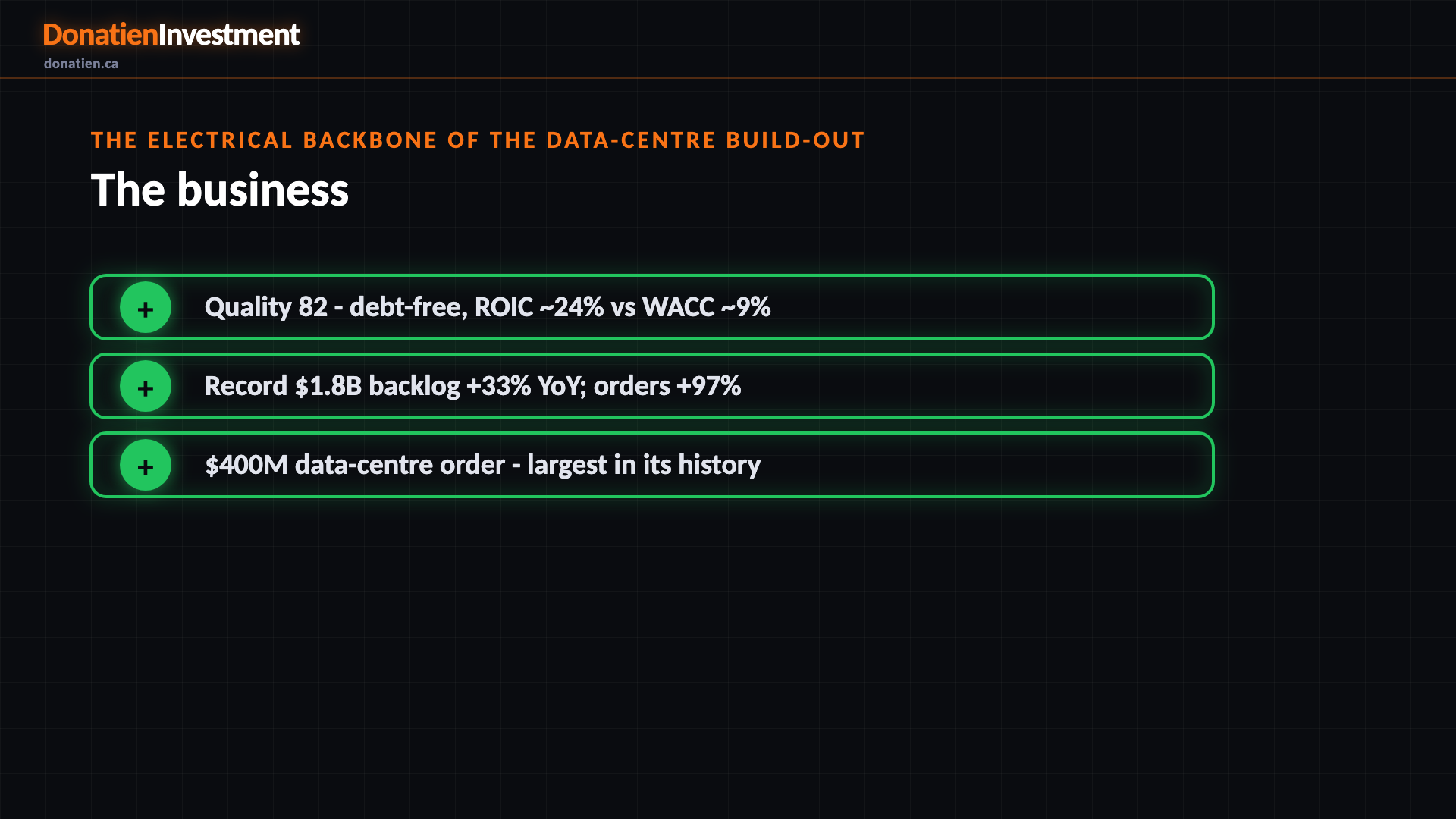

The electrical backbone of the data-centre build-out

Powell Industries scores 82 on quality. It builds custom medium-voltage switchgear and power-control systems - the electrical backbone of refineries, LNG terminals, utility substations and now hyperscale data centres. It is essentially debt-free, with a return on invested capital near 24 percent against a 9 percent cost of capital, and its backlog is a record 1.8 billion dollars, up 33 percent year on year, with new orders up 97 percent. It landed a 400 million dollar data-centre order, the largest in company history, with revenue visibility out to fiscal 2028. This is a genuinely excellent business - which is exactly the trap, because a great company is not a great investment at any price.

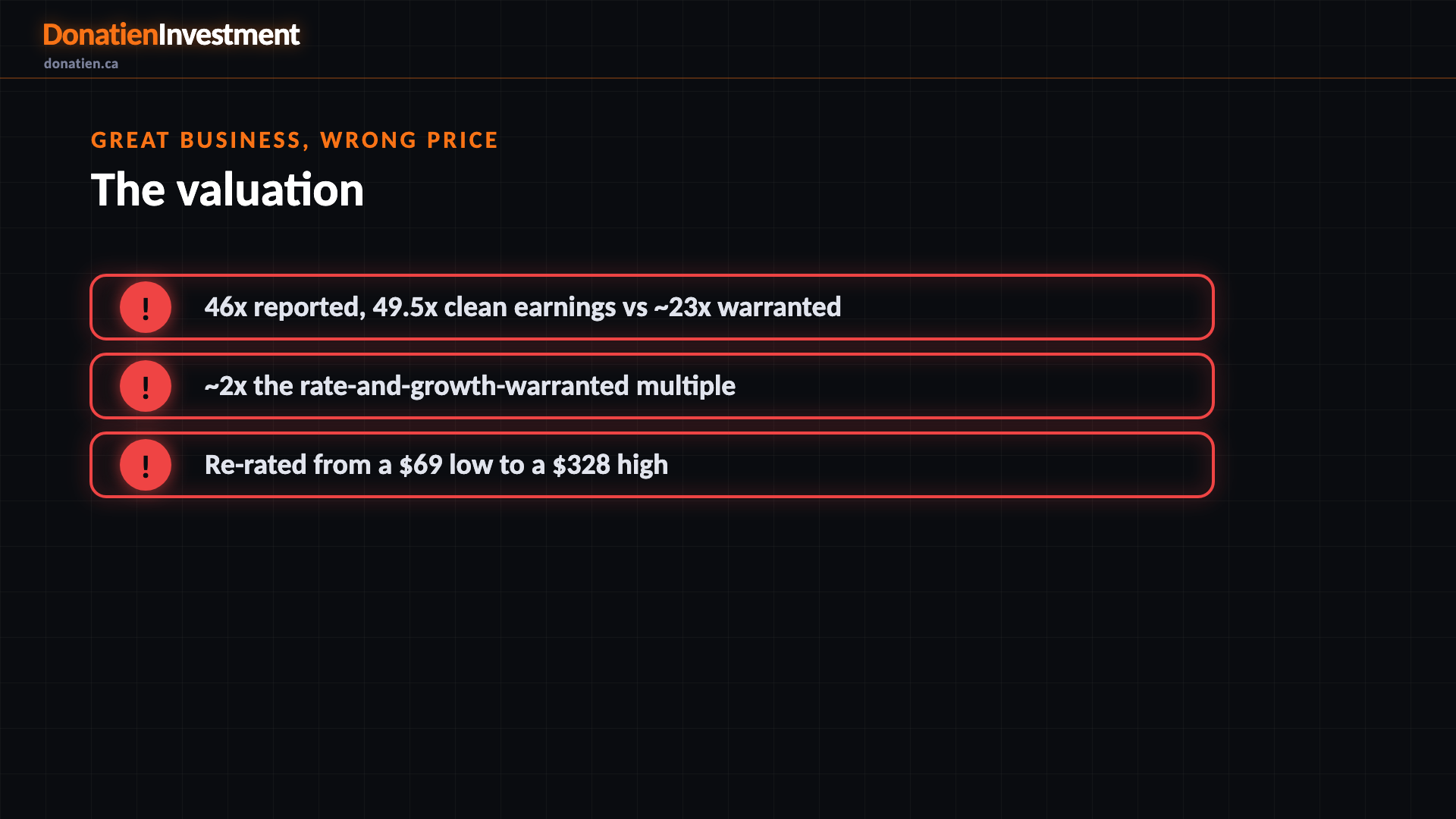

Great business, wrong price

Valuation scores just 30, and this is the crux of the call. The stock trades at about 46 times reported earnings, and closer to 49 and a half times once you strip out non-operating interest income - against a warranted multiple near 23. That is roughly twice what the fundamentals justify, and it sits above the Industrials guardrail even a year out on forward earnings. The shares have re-rated hard on the electrification and data-centre theme, from a 52-week low of 69 dollars to a high of 328, and now sit near 236. At that price the market is treating the data-centre order surge as a permanent step-change rather than a cyclical spike.

A quality name, but no timing edge

Timing scores a weak 42. The monthly and weekly trends are still up from the big re-rate, but the daily has rolled over below its 50-day average near 281 dollars, momentum has turned negative, and the stock fell four and a half percent on the day of the report. None of the three entry paths are open, so the conviction ladder reads wait. And unlike some expensive names, there is no analyst cushion here - the consensus target of 237.67 sits right on top of the current price, so the tape offers no implied upside to lean on. The cleaner entry is a tested bounce off the 223 shelf, or a reclaim of the 50-day on volume.

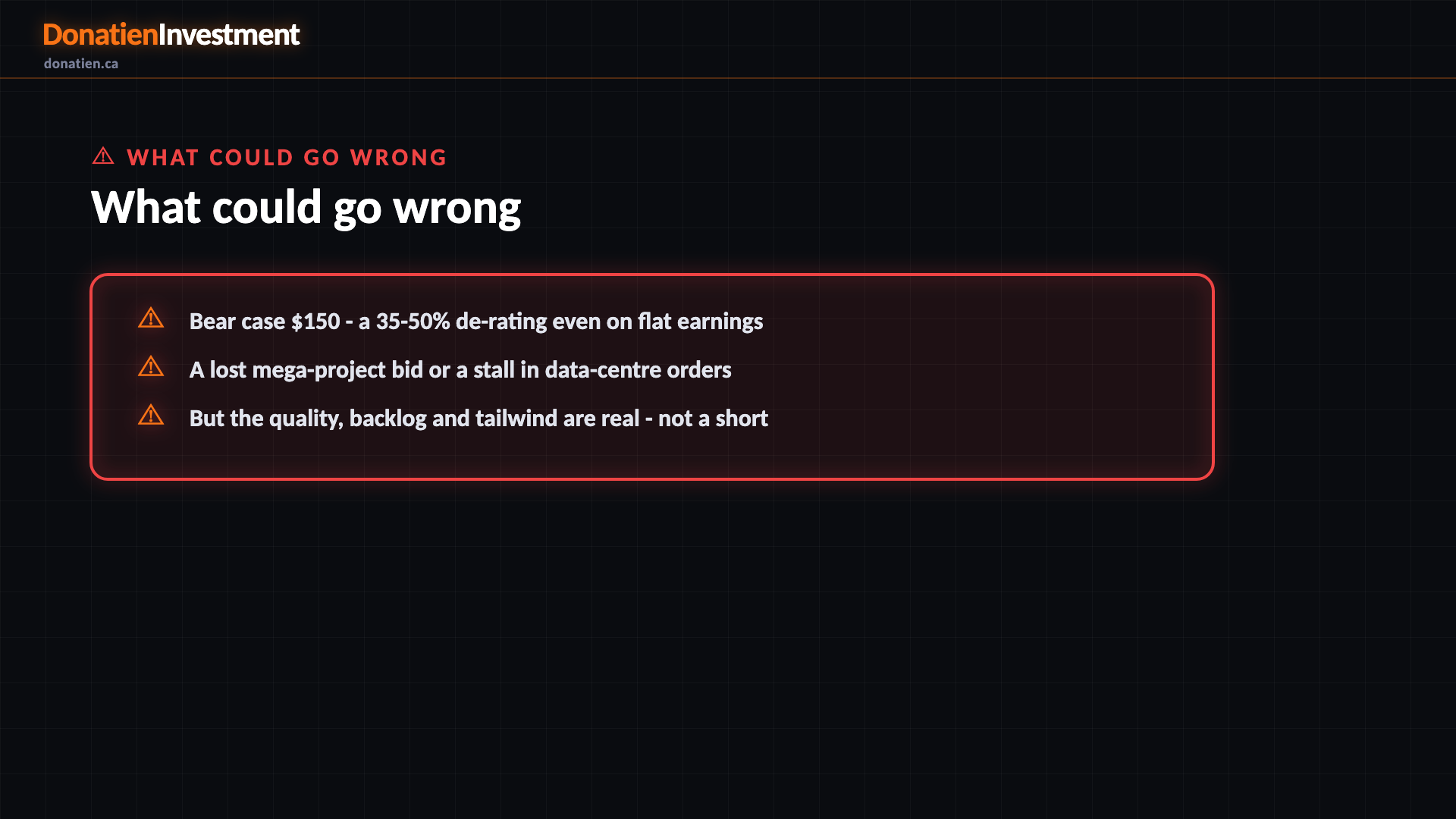

What could go wrong

The main risk is the same multiple working in reverse. The bear case takes the stock to 150 dollars - a 35 to 50 percent de-rating as a 46 times multiple compresses back toward the 23 times warranted line, even if earnings stay flat. The live triggers are a stall in data-centre and utility order intake for a couple of quarters, or a flagship mega-project bid lost to a giant like Eaton or Schneider. But this is a hold, not a short: the quality, the record backlog and the secular data-centre tailwind are all genuine, the balance sheet is a fortress, and the growth is proven and durable - so the sensible move is to wait for a better price, not to bet against the business.

Risk vs Reward

Against the current US$235.79, the report frames a bull case at US$330 (+40%), a base case at US$240 (+2%) and a bear case at US$150 (-36%). See the full report for the probability weight behind each path.

The verdict

A superb, debt-free maker of the electrical backbone for data centres - but priced at roughly twice its warranted multiple, so a hold until the price comes to you.

Read the full report on donatien.ca →{kind=link}

{kind=link}