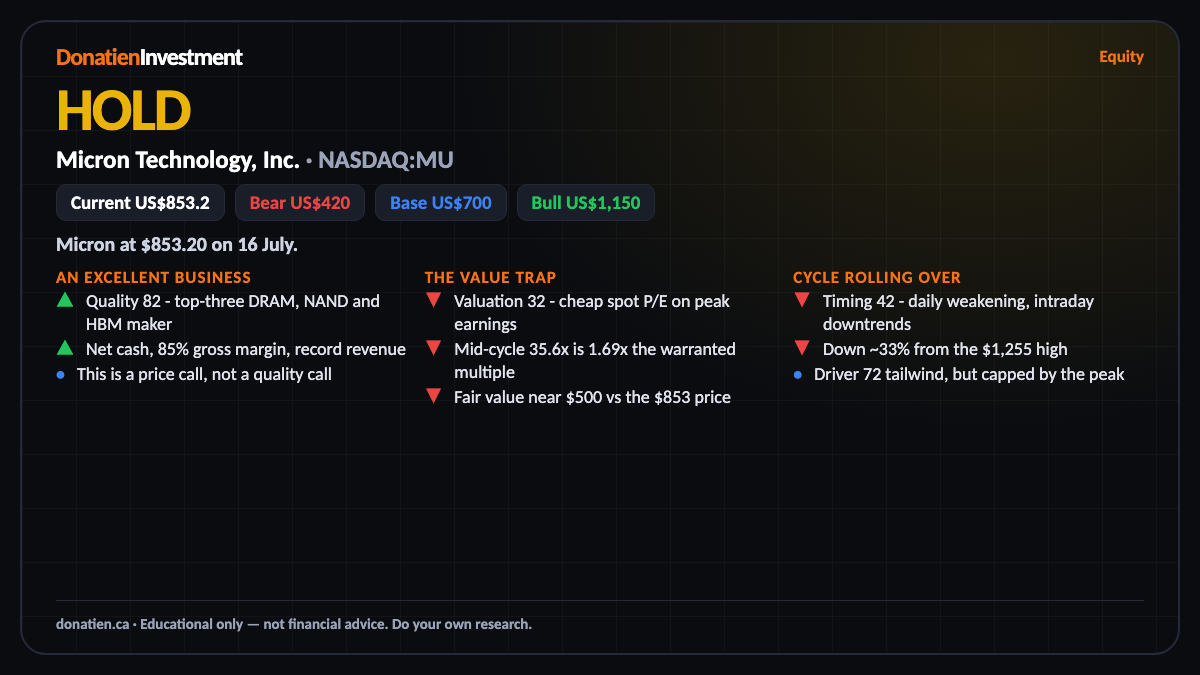

Micron Technology, Inc. (NASDAQ:MU) HOLD

An excellent, financially pristine top-three memory maker at a peak-cycle price - a cheap-looking P/E on record earnings is a value trap, not a bargain.

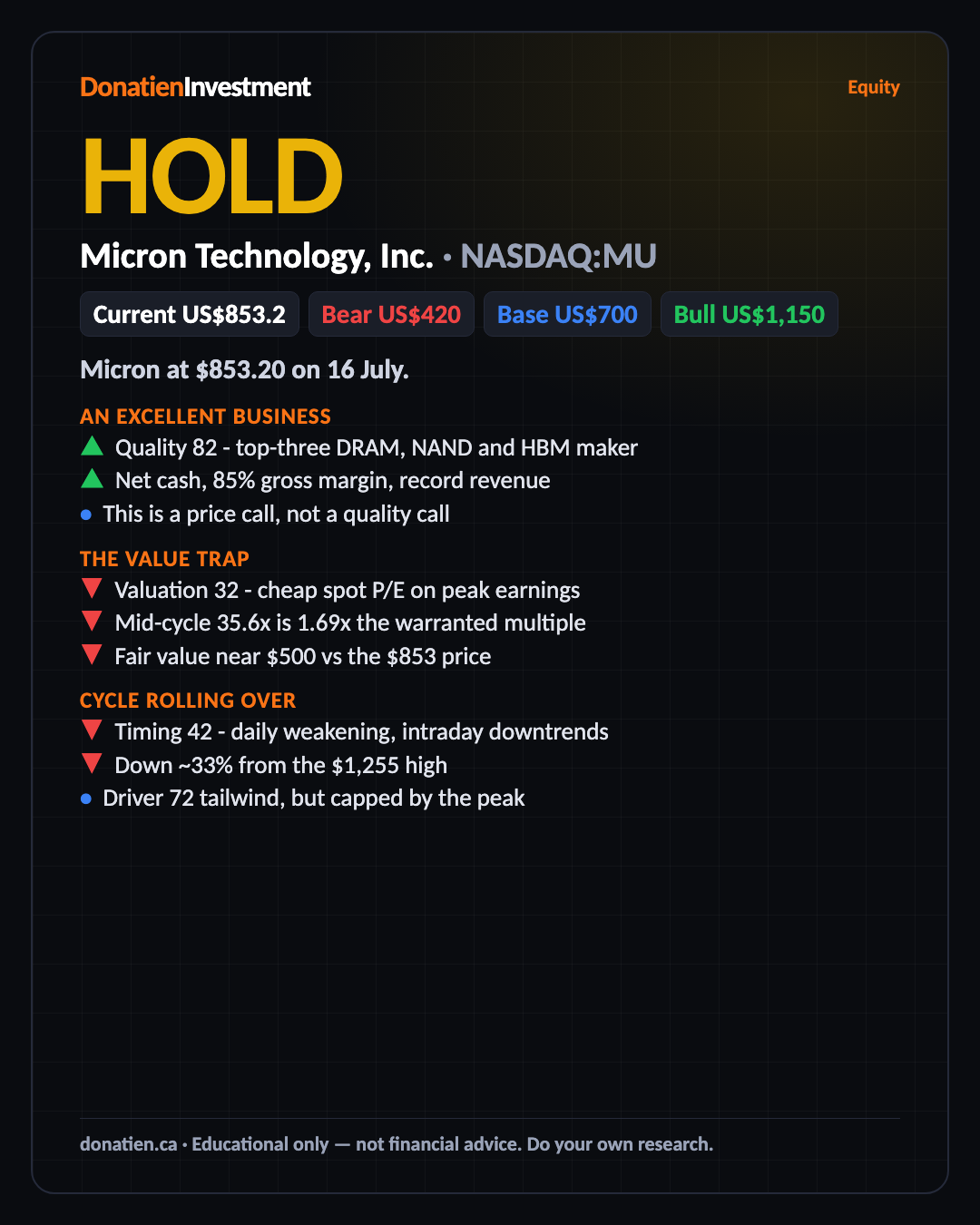

Micron at $853.20 on 16 July. This is a quality business at the wrong point in its cycle: it screens cheap at around 19 times trailing earnings, but those earnings are struck at the top of an AI-driven memory shortage. On mid-cycle earnings the framework rates it Hold in every horizon.

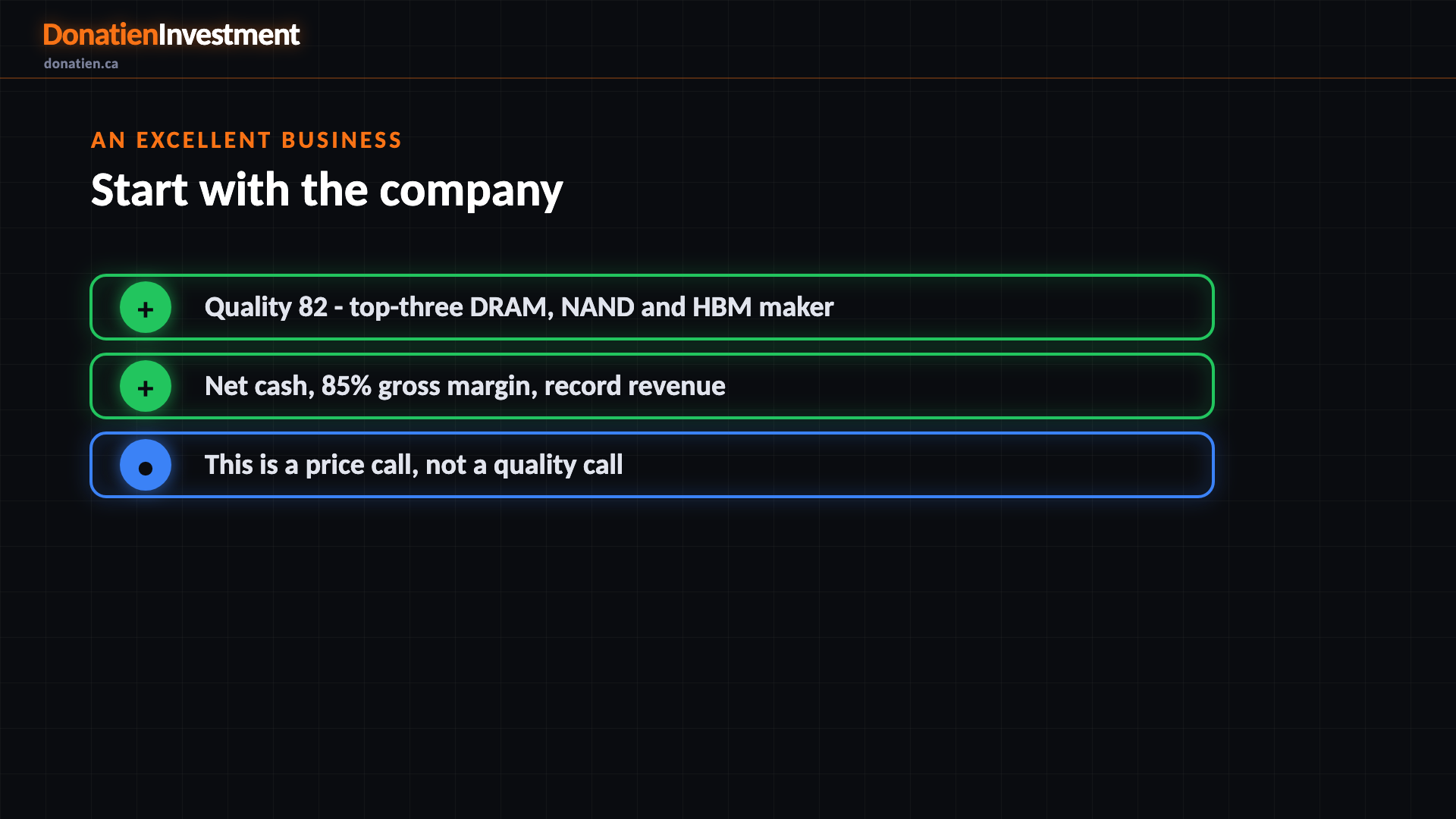

An excellent business

Micron is one of only three companies in the world that make the memory chips modern computing runs on, and right now it is enjoying the best pricing in its history. Quality scores 82. The balance sheet is pristine, net cash, with gross margins near 85 percent and record revenue on the AI build-out. Nothing here is broken. The Hold is entirely about where you are in the cycle when you buy it.

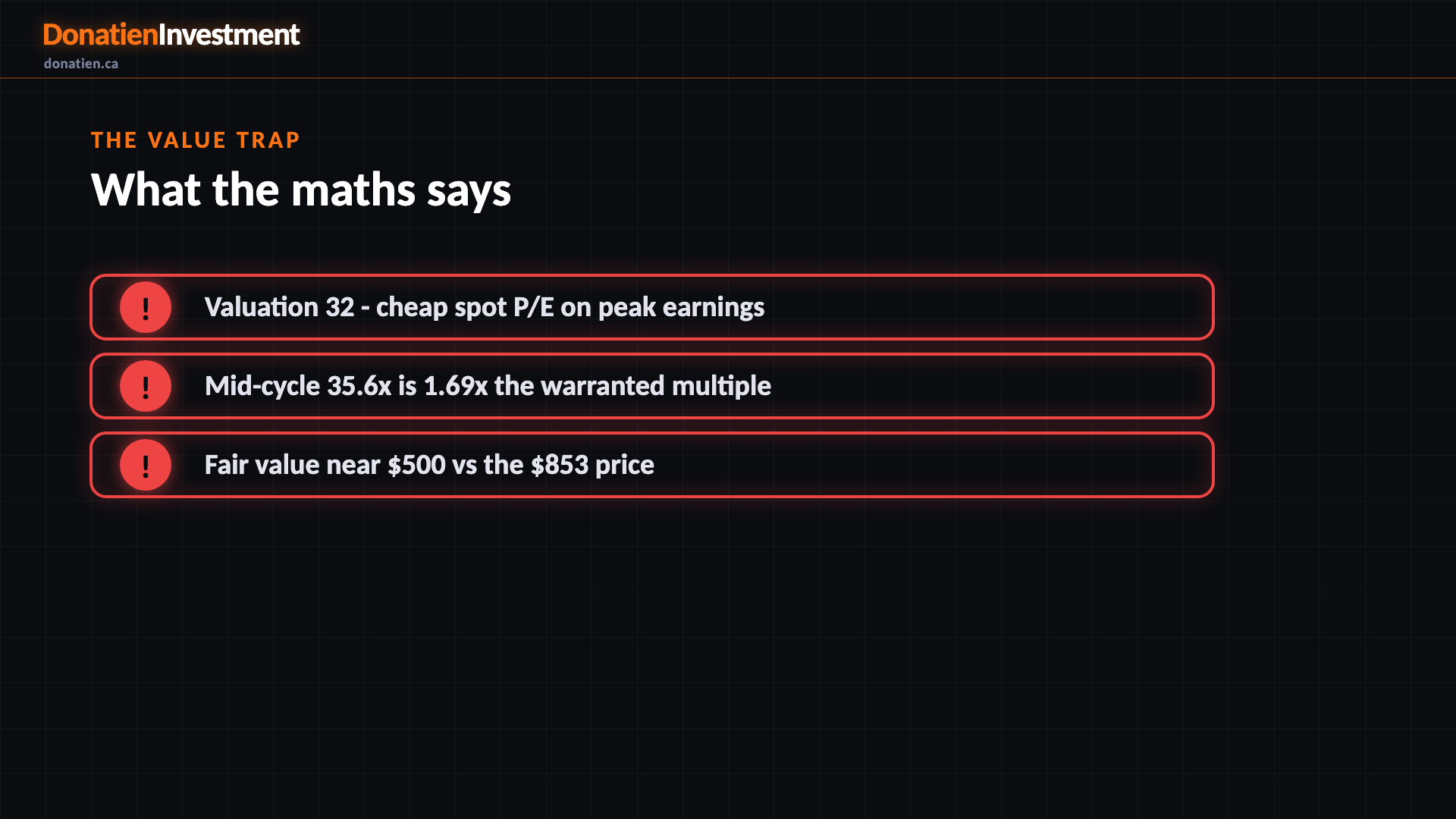

The value trap

Memory is a commodity cycle. Margins swing from the low twenties at the trough to the mid eighties at the peak, and today it sits at the peak. So the roughly 19 times trailing multiple is struck on record earnings that will not last. Score it on normalised mid-cycle earnings, around 24 dollars a share, and it trades near 36 times, about 1.69 times what rates and growth warrant. Fair value lands near 500, well below the 853 price. That is the value trap the framework exists to catch.

Cycle rolling over

The operating cycle is still hot, but the equity is turning. Micron is down about 33 percent from its 1,255 high and fell sharply into the close. The higher timeframes remain in an uptrend, yet the daily has rolled over and the intraday charts are in strong downtrends. The memory and AI up-cycle scores 72 as a driver, a real tailwind, but it sits at a peak level and cannot amplify a Hold. For a peak cyclical, a turning tape is the signal that matters.

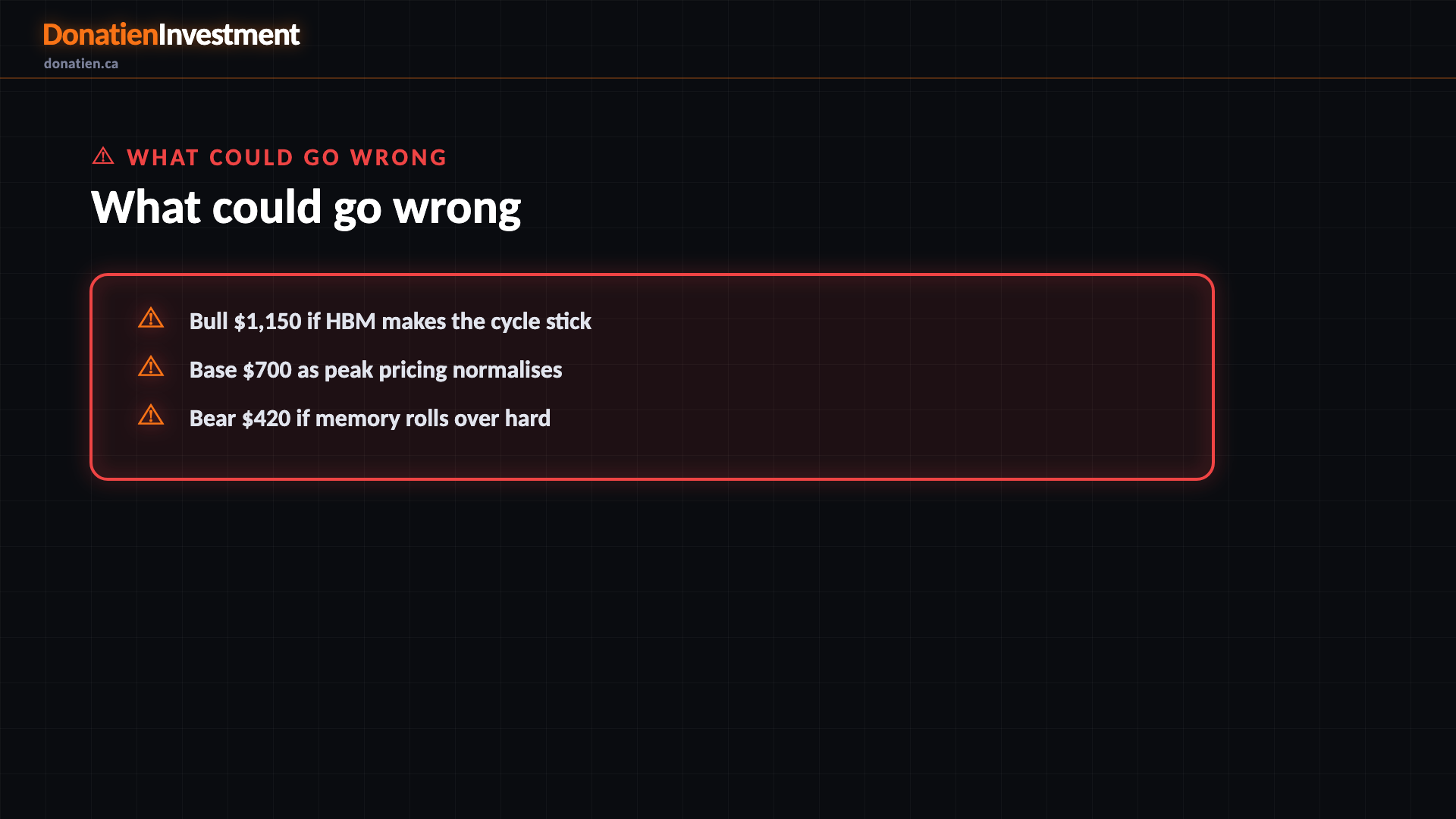

What could go wrong

The honest spread is wide. The bull case reaches 1,150 if high-bandwidth memory structurally dampens the cycle and the shortage holds into 2027. The base case of 700 has peak pricing normalising toward a still-elevated mid-cycle. But the live bear is 420, roughly a 50 percent drawdown, if a hyperscaler cuts AI capex or Samsung starts a price war and hits the number-three supplier first. This is not a short call. It is a wait: excellent business, wrong price, at the top of the cycle.

Risk vs Reward

Against the current US$853.2, the report frames a bull case at US$1,150 (+35%), a base case at US$700 (-18%) and a bear case at US$420 (-51%). See the full report for the probability weight behind each path.

The verdict

An excellent, financially pristine top-three memory maker at a peak-cycle price - a cheap-looking P/E on record earnings is a value trap, not a bargain.

Read the full report on donatien.ca →{kind=link}

{kind=link}