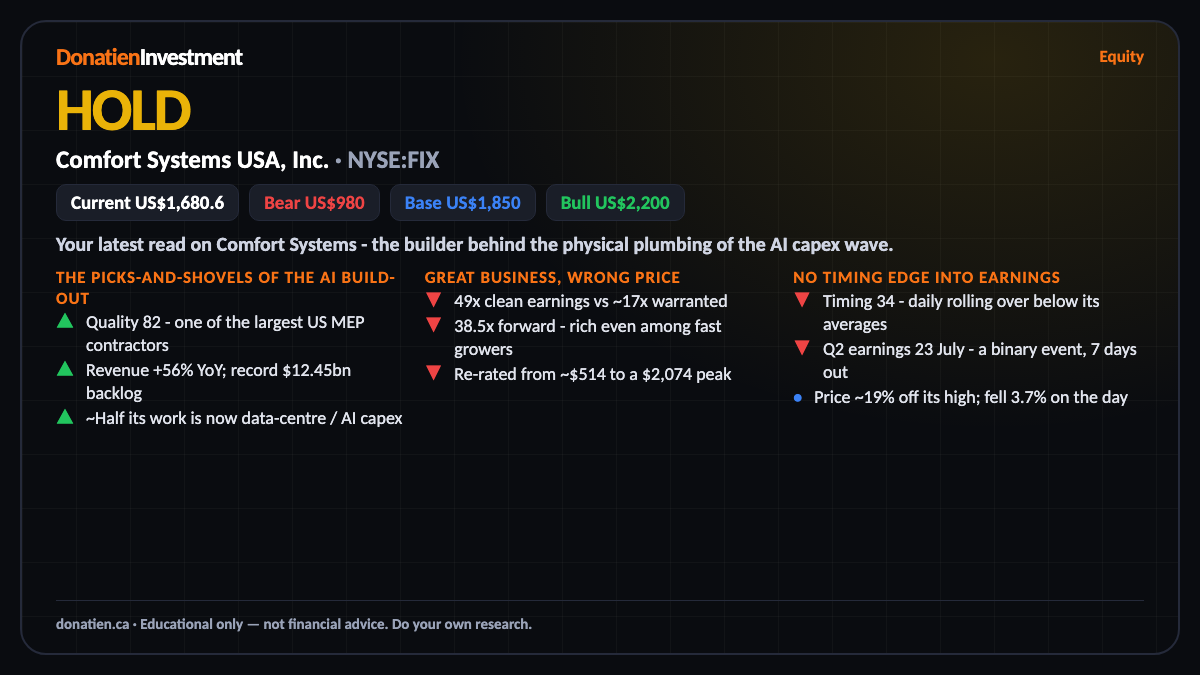

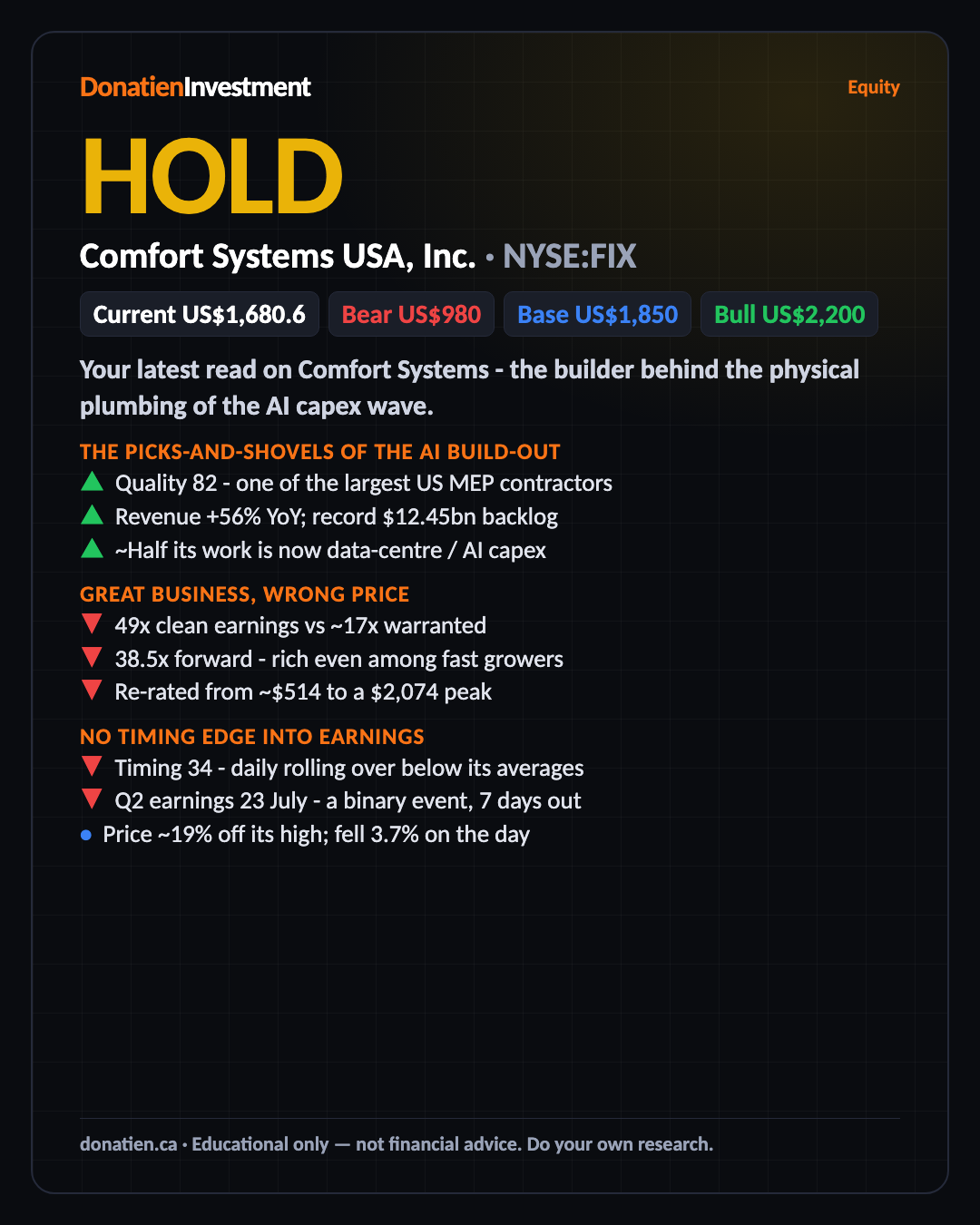

Comfort Systems USA, Inc. (NYSE:FIX) HOLD

A superb AI-infrastructure builder priced for a flawless future - 49x clean earnings against a ~17x warranted multiple, so a hold until the price comes to you.

Your latest read on Comfort Systems - the builder behind the physical plumbing of the AI capex wave.

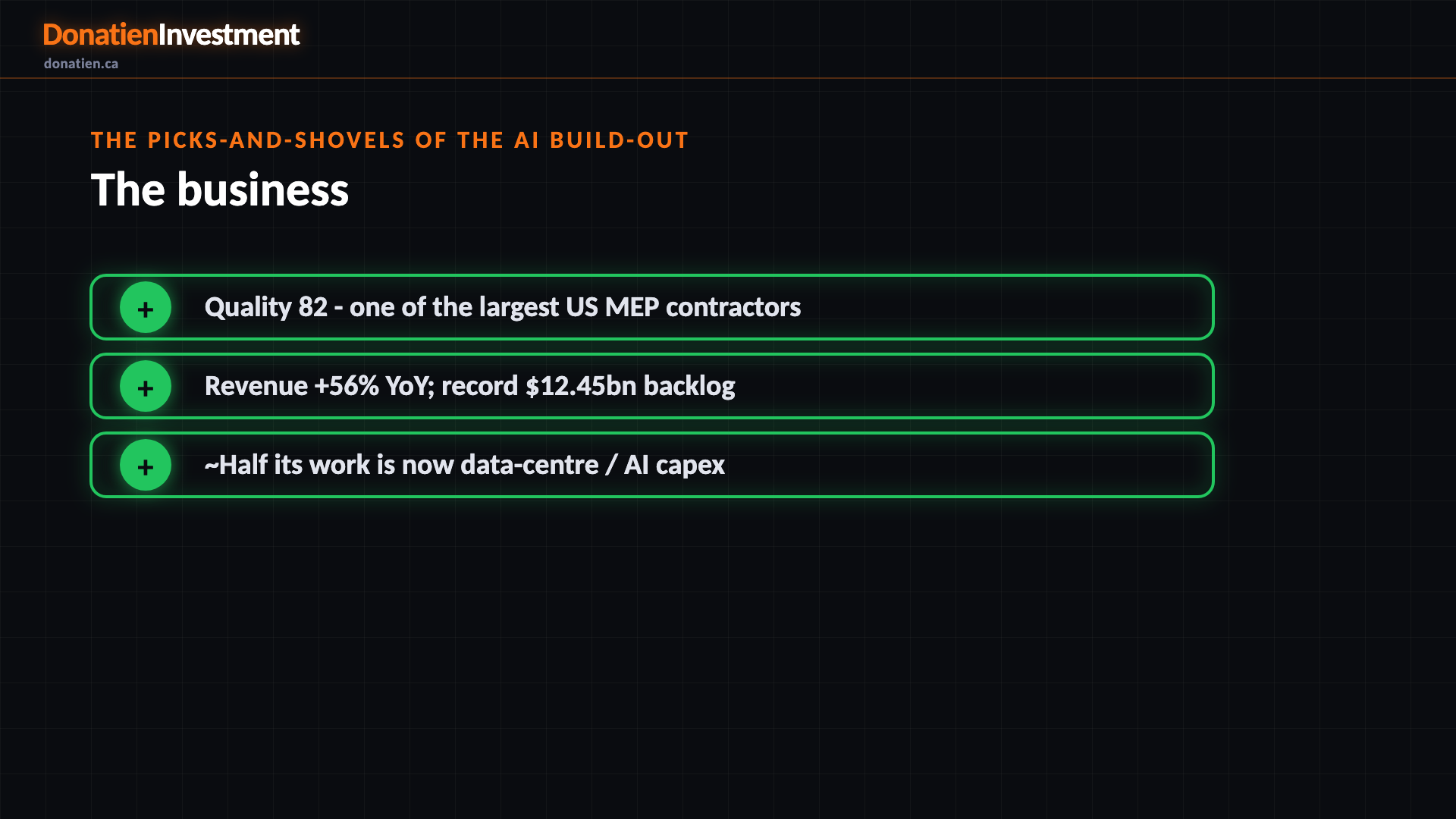

The picks-and-shovels of the AI build-out

Comfort Systems scores 82 on quality. It is one of the largest mechanical, electrical and plumbing contractors in the United States, and it builds the power, cooling and electrical guts of data centres. Revenue grew 56 percent last quarter and the backlog is a record 12.45 billion dollars. Roughly half its work is now data-centre and AI-infrastructure capex, so it is a geared bet on hyperscaler spending. This is a genuinely excellent, low-debt, cash-generative business - which is exactly the trap, because a great company is not a great investment at any price.

Great business, wrong price

Valuation scores just 22, and this is the crux of the call. The stock trades at about 49 times clean earnings against a warranted multiple near 17 - almost three times what the fundamentals justify. Even on forward earnings it is 38.5 times, rich among engineering and construction peers that trade in the twenties. The shares have re-rated from around 514 dollars to a 2,074 peak on the AI-capex theme and now sit near 1,681. The one supportive lens is analysts, whose consensus target of about 2,015 sits roughly 20 percent above the price - the reason this is a hold and not a sell.

No timing edge into earnings

Timing scores a weak 34. The higher timeframes are still uptrends, but the daily has rolled over below its 20 and 50-day averages and the intraday tape is in a downtrend. The stock is about 19 percent off its high and fell nearly 4 percent on the day of the report. On top of that, second-quarter earnings land on 23 July - a binary, high-variance event that FIX routinely moves more than 5 percent on. With the signal already a hold on valuation, there is simply no entry edge to act on here.

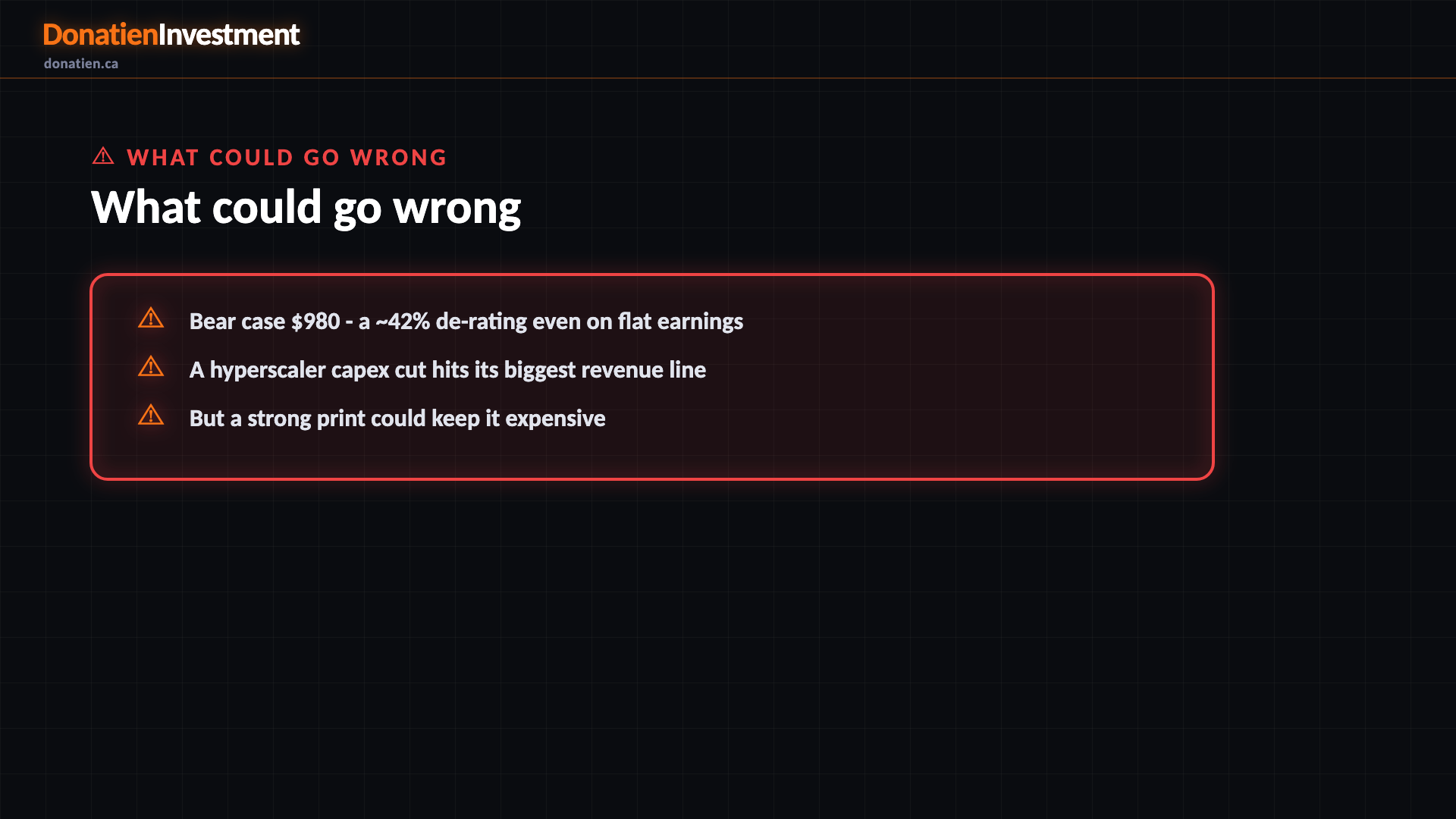

What could go wrong

The risk here is unusually two-sided. The bear case is a big one - a de-rating from 49 times back toward the warranted range is roughly a 42 percent drawdown to around 980 dollars, even on flat earnings, and the live trigger is a hyperscaler capex cut hitting its biggest revenue line. But the other side is just as real: a strong print could keep the multiple high and leave a patient buyer behind, with a bull case up at 2,200. That symmetry, on a name whose base case is only about flat, is exactly why the call is hold.

Risk vs Reward

Against the current US$1,680.6, the report frames a bull case at US$2,200 (+31%), a base case at US$1,850 (+10%) and a bear case at US$980 (-42%). See the full report for the probability weight behind each path.

The verdict

A superb AI-infrastructure builder priced for a flawless future - 49x clean earnings against a ~17x warranted multiple, so a hold until the price comes to you.

Read the full report on donatien.ca →{kind=link}

{kind=link}