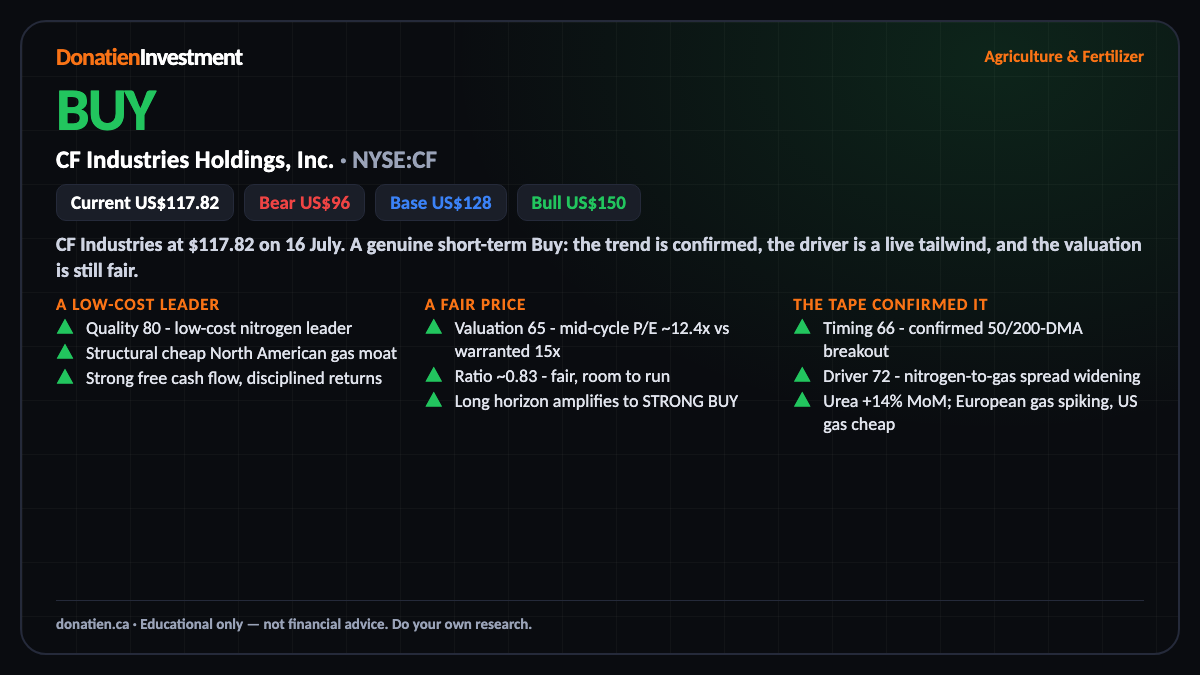

CF Industries Holdings, Inc. (NYSE:CF) BUY

A confirmed breakout on a widening nitrogen-to-gas spread - cheap US gas, dear global urea - at a fair price with a structural cost moat.

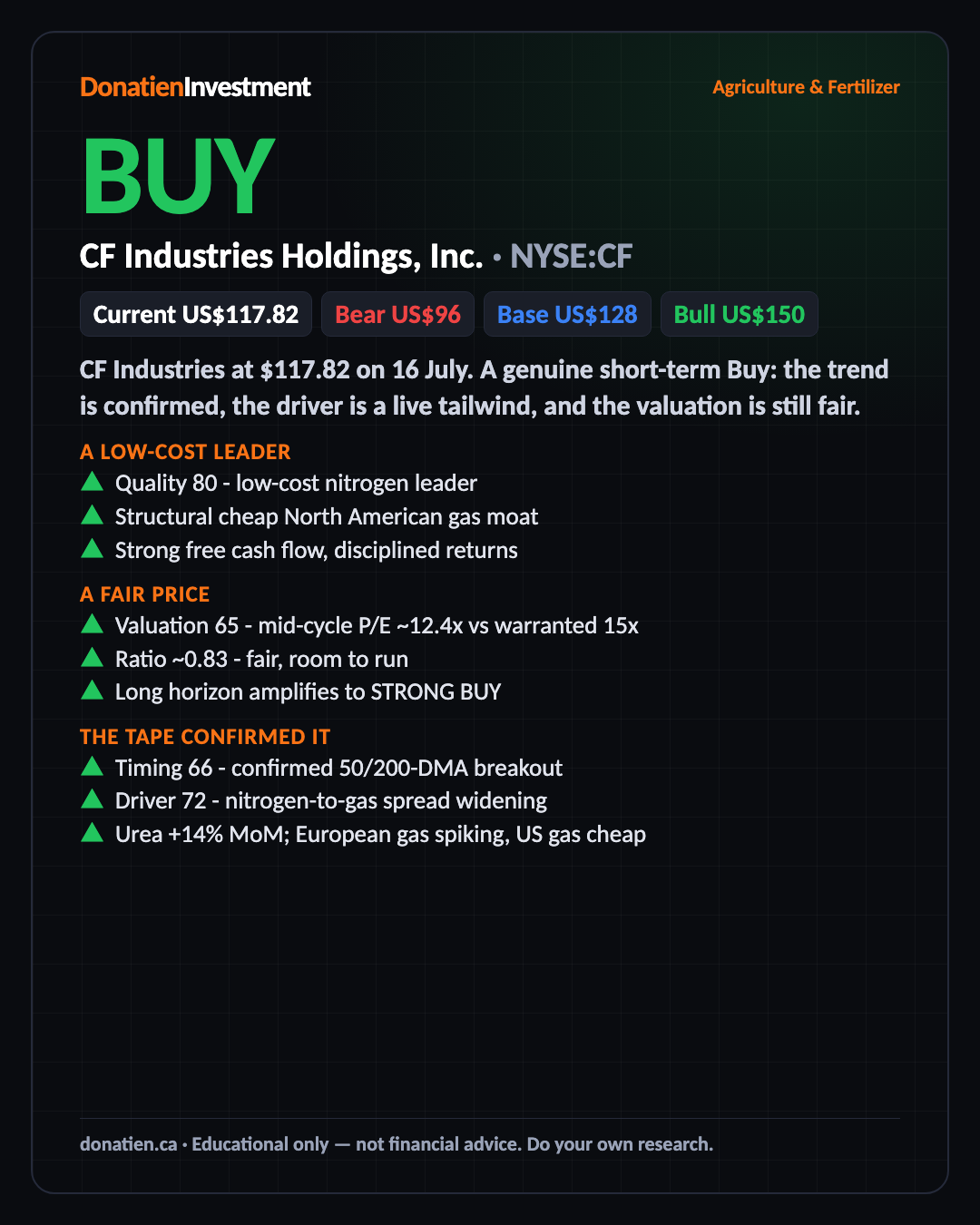

CF Industries at $117.82 on 16 July. A genuine short-term Buy: the trend is confirmed, the driver is a live tailwind, and the valuation is still fair.

A low-cost leader

CF is a low-cost nitrogen leader, scoring 80 on quality. Its edge is cheap North American gas. It turns that cheap domestic feedstock into fertilizer the rest of the world pays more to make, throws off strong free cash flow, and returns it with discipline. For once the price and the tape agree with the quality.

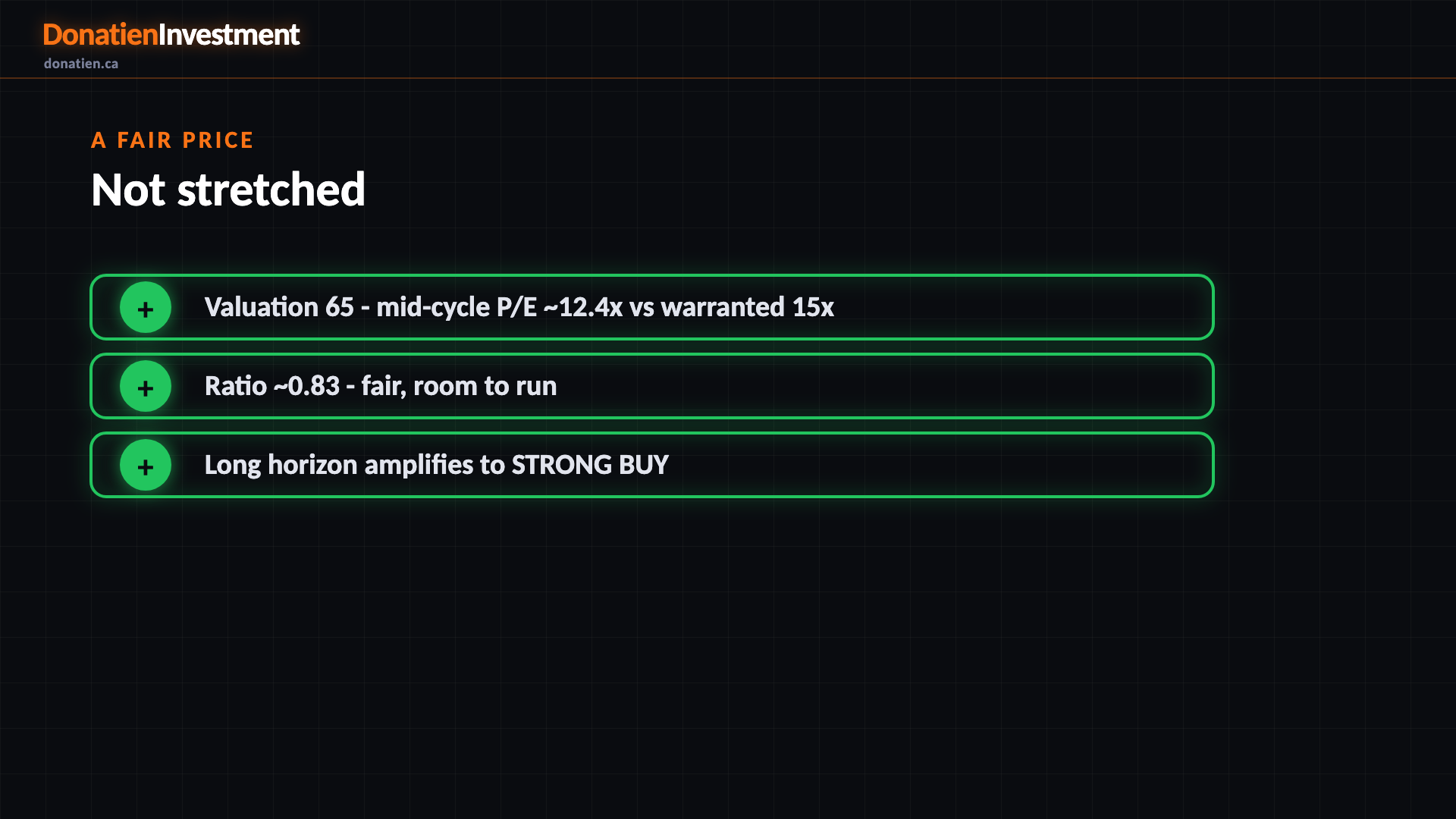

A fair price

On mid-cycle earnings CF trades near 12.4 times against a warranted 15, a fair ratio around 0.83. Room, not stretched. We score it on mid-cycle rather than peak earnings to avoid the cyclical trap. Because valuation stays fair rather than full, the long-term signal amplifies to Strong Buy on the structural cost moat and coming Blue Point capacity.

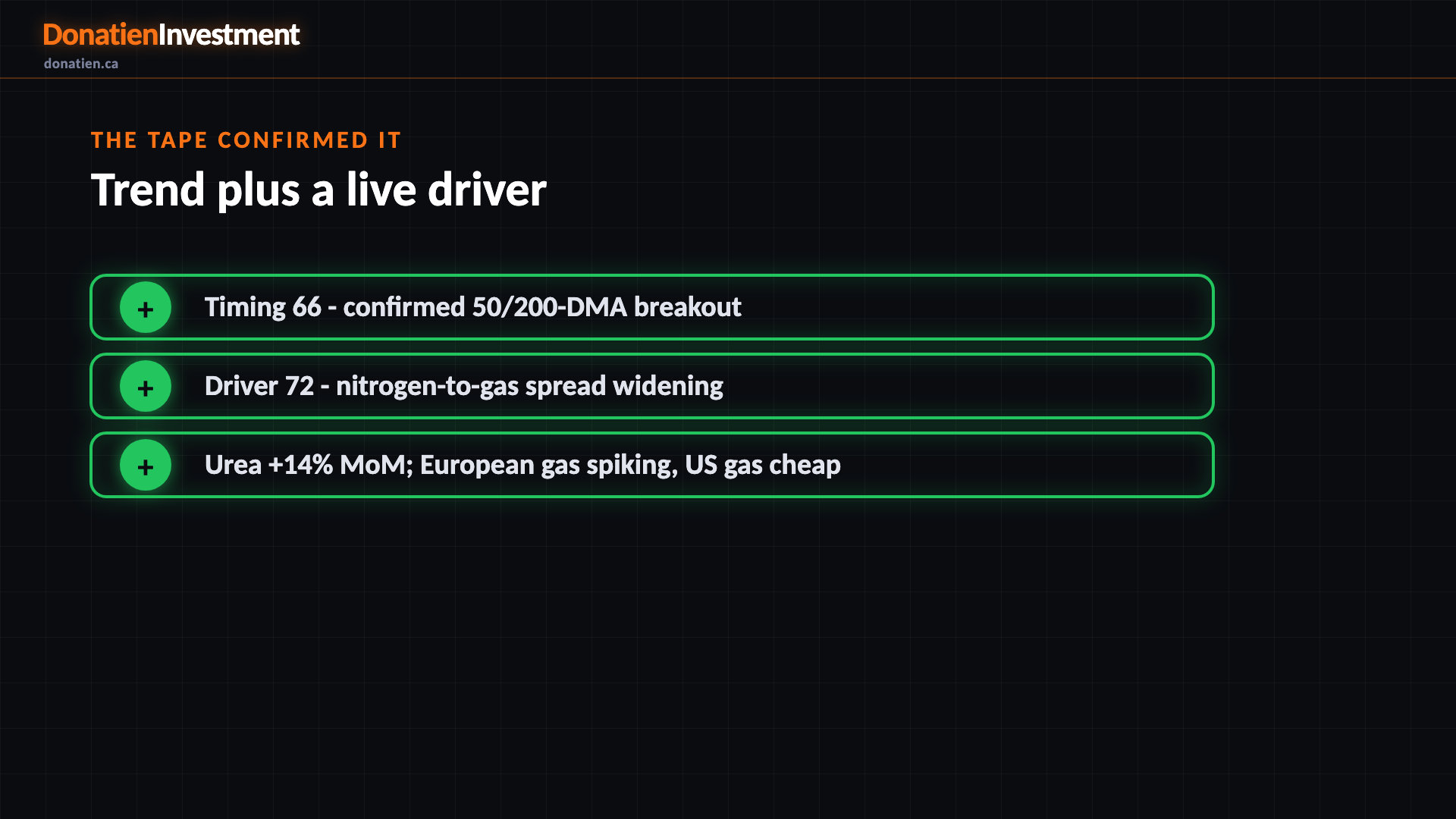

The tape confirmed it

The tape confirmed it: CF reclaimed its 50 and 200-day averages on a real breakout. The driver is live too. Urea is up about 14 percent month on month, European gas is spiking, and US feedstock gas is cheap, so the nitrogen-to-gas spread is widening in CF favour. Trend plus a live driver is a confirmed entry, not a hold.

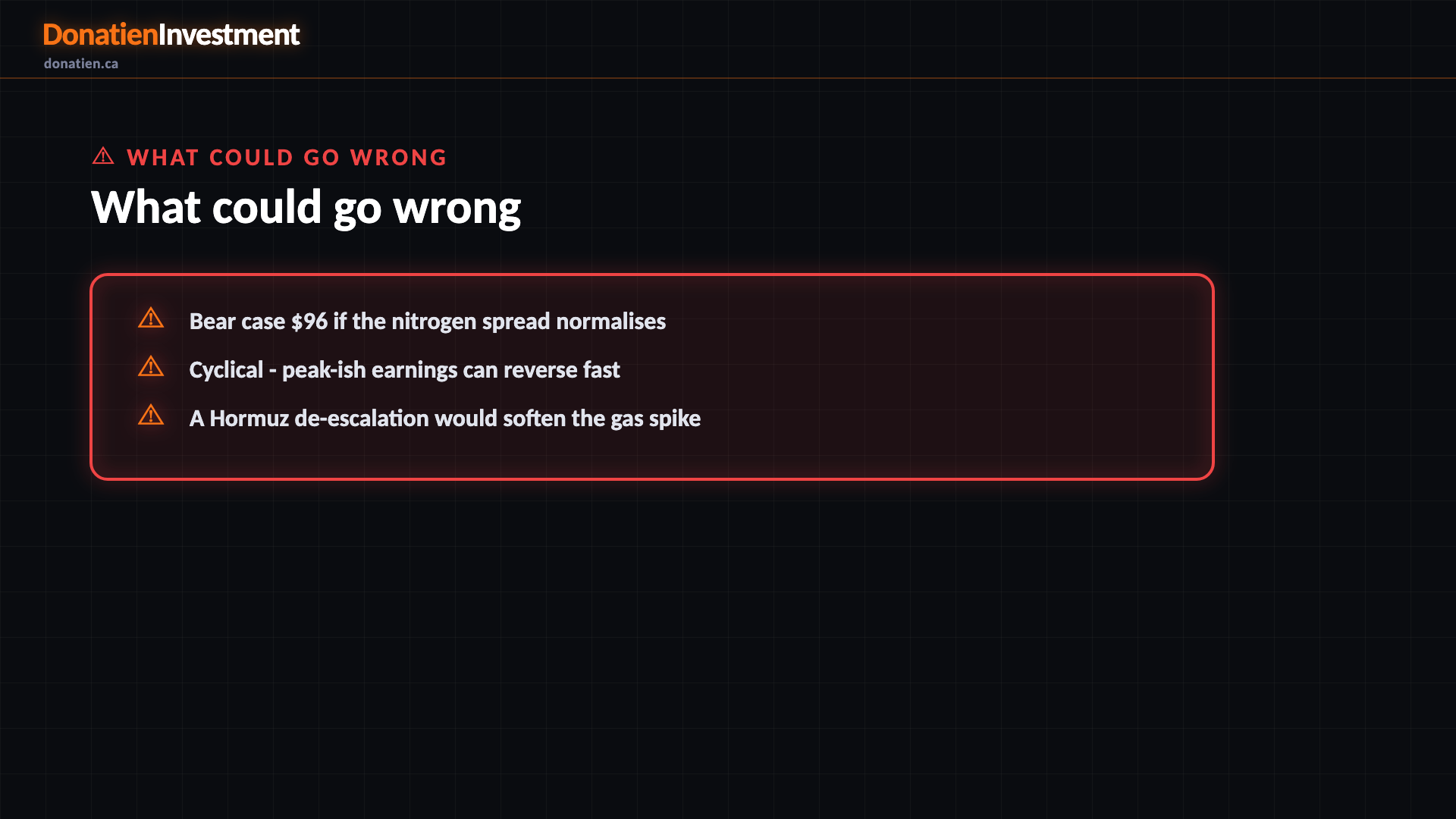

What could go wrong

The honest downside, shown loud. Nitrogen and gas are cyclical, and the bear case sits near 96 if the spread normalises. Much of the near-term driver rests on an energy-supply spike a Hormuz de-escalation would soften. This is a Buy on a confirmed trend, not a permanent holding - size it as the cyclical it is, base 128 and bull 150.

Risk vs Reward

Against the current US$117.82, the report frames a bull case at US$150 (+27%), a base case at US$128 (+9%) and a bear case at US$96 (-19%). See the full report for the probability weight behind each path.

The verdict

A confirmed breakout on a widening nitrogen-to-gas spread - cheap US gas, dear global urea - at a fair price with a structural cost moat.

Read the full report on donatien.ca →{kind=link}

{kind=link}