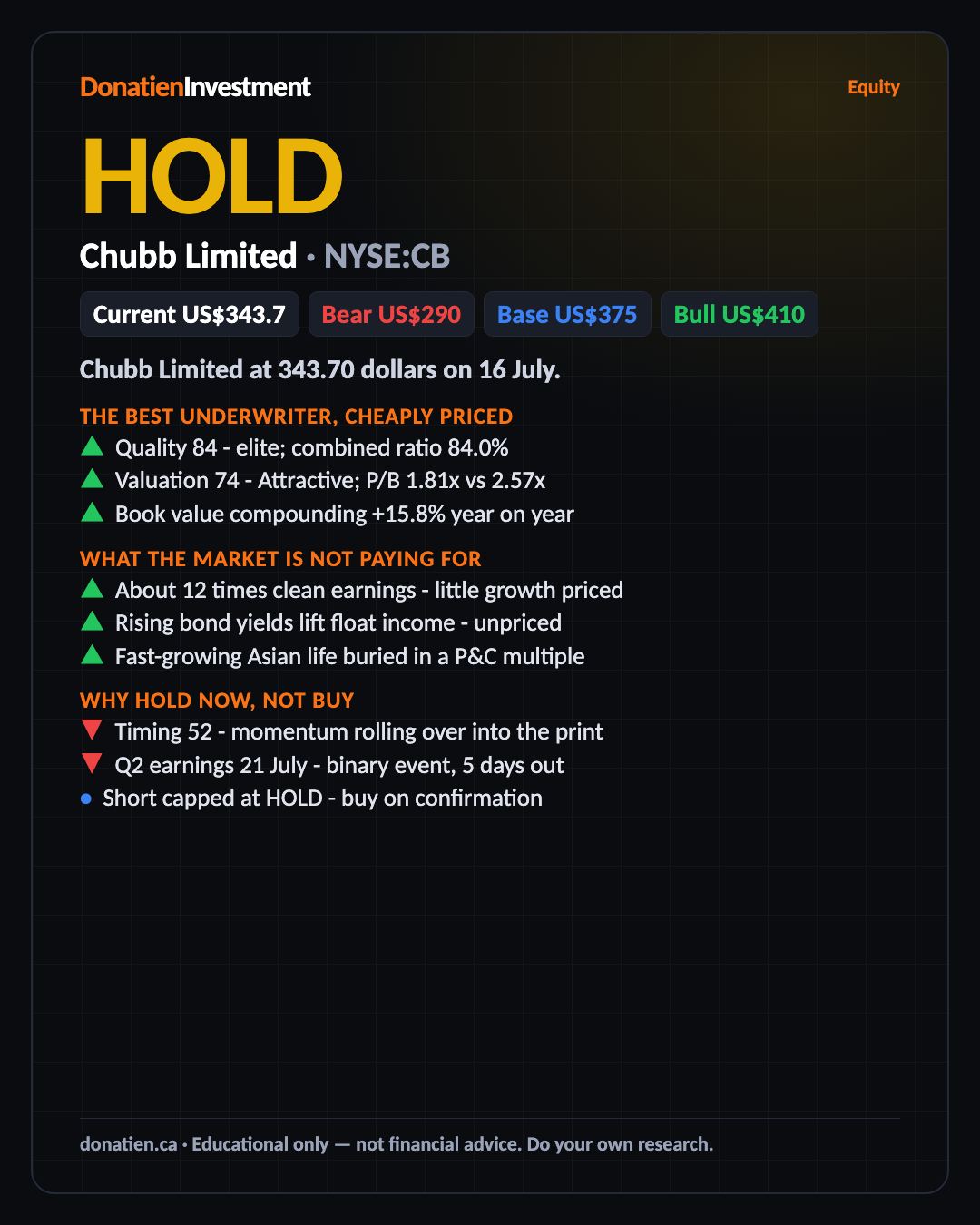

Chubb Limited (NYSE:CB) HOLD

An elite insurer, cheap on both book and earnings - but earnings land on 21 July and the short-term entry is unconfirmed, so a hold now, with the medium and long call a BUY.

Chubb Limited at 343.70 dollars on 16 July. Short-term Hold: quality and valuation are strong, but Q2 earnings land on 21 July and there is no confirmed timing edge yet - the medium and long call is a Buy.

The best underwriter, cheaply priced

Chubb scores 84 on quality - the best-in-class property and casualty underwriter. Its combined ratio was 84.0 percent last quarter, meaning it kept roughly 16 cents of underwriting profit on every premium dollar where the median rival only breaks even. And it is cheap for that quality: valuation scores 74, with the stock at 1.81 times book against a justified 2.57 times, about seventy percent of what the fundamentals warrant. Book value is compounding over fifteen percent a year. Elite business, Attractive price.

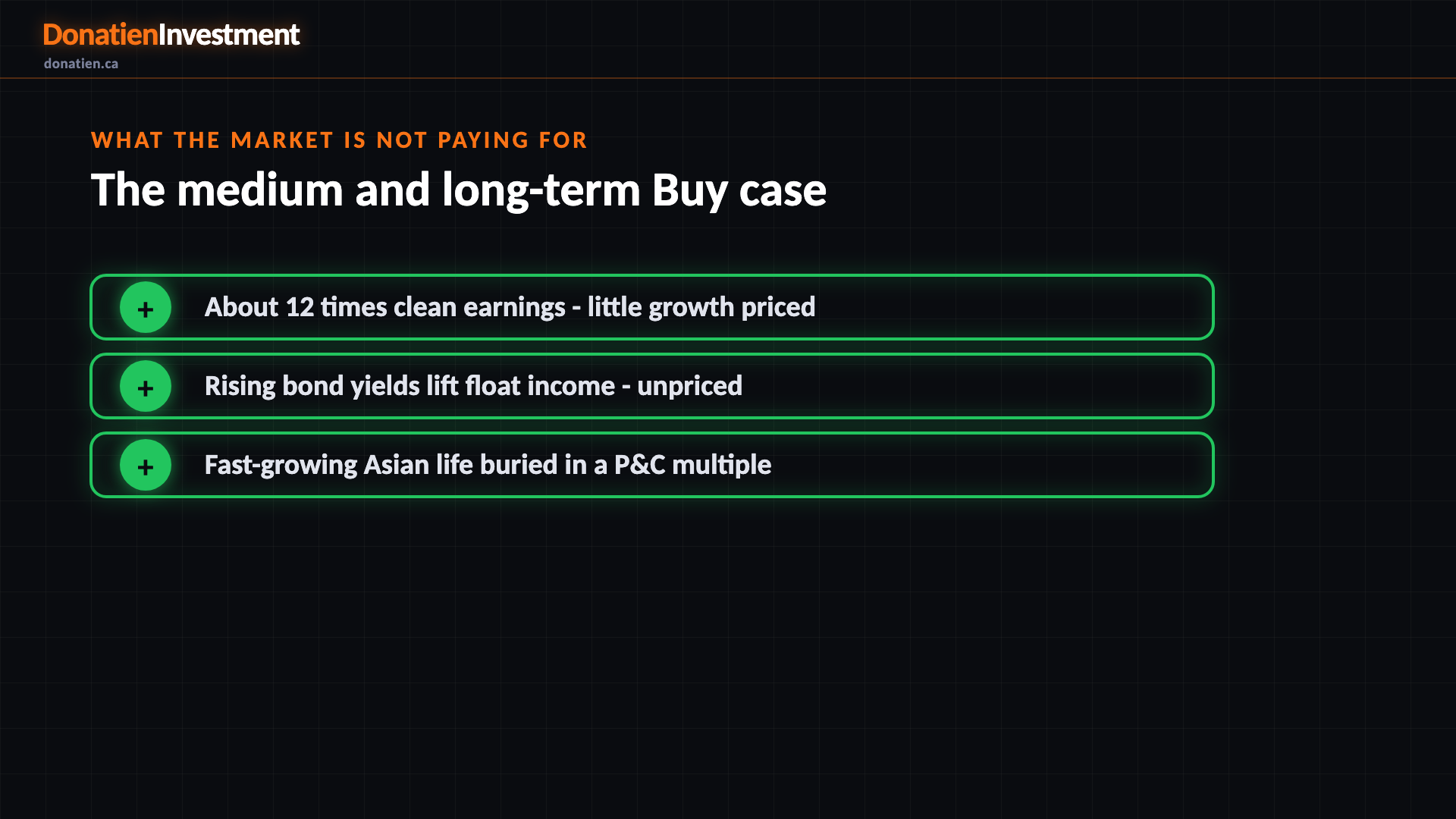

What the market is not paying for

At around twelve times clean earnings, the market is pricing Chubb for very little real growth - no premium at all for its best-in-class discipline. Two things it is not paying for: the higher-for-longer rate regime is quietly re-pricing Chubbs large bond portfolio upward as each maturity reinvests at a higher yield, a multi-year tailwind to investment income; and the fast-growing Asian life business, up thirty-three percent in the first quarter, sits buried inside a property and casualty multiple. That gap between price and fundamentals is why the medium and long call is a Buy.

Why Hold now, not Buy

So why Hold? The longer-term trend is up, but near-term momentum is fading - the daily indicator has rolled over and price sits just under its twenty-day average. On top of that, Q2 earnings land on the twenty-first of July, a binary event only five days out that caps our timing confidence. A short-term buy needs a confirmed technical or catalyst path, and neither is open yet, so the short signal is capped at Hold. The cleaner entry is a pullback into 333 or 321 support, or a reclaim on volume after the print - buy on confirmation.

What could go wrong

The main risk is the pricing cycle. The commercial property market has turned soft, with rates falling ten to thirty percent as record reinsurance capital chases share - a real growth headwind, though casualty lines stay firm. The bear case sits near 290, well below todays price, and it triggers if that soft market deepens or a bad hurricane season pushes the combined ratio above ninety-five percent. Hold is the honest read: own the quality and the value for the medium and long term, but let the 21 July print clear before adding. Base 375, bull 410, bear 290.

Risk vs Reward

Against the current US$343.7, the report frames a bull case at US$410 (+19%), a base case at US$375 (+9%) and a bear case at US$290 (-16%). See the full report for the probability weight behind each path.

The verdict

An elite insurer, cheap on both book and earnings - but earnings land on 21 July and the short-term entry is unconfirmed, so a hold now, with the medium and long call a BUY.

Read the full report on donatien.ca →{kind=link}

{kind=link}