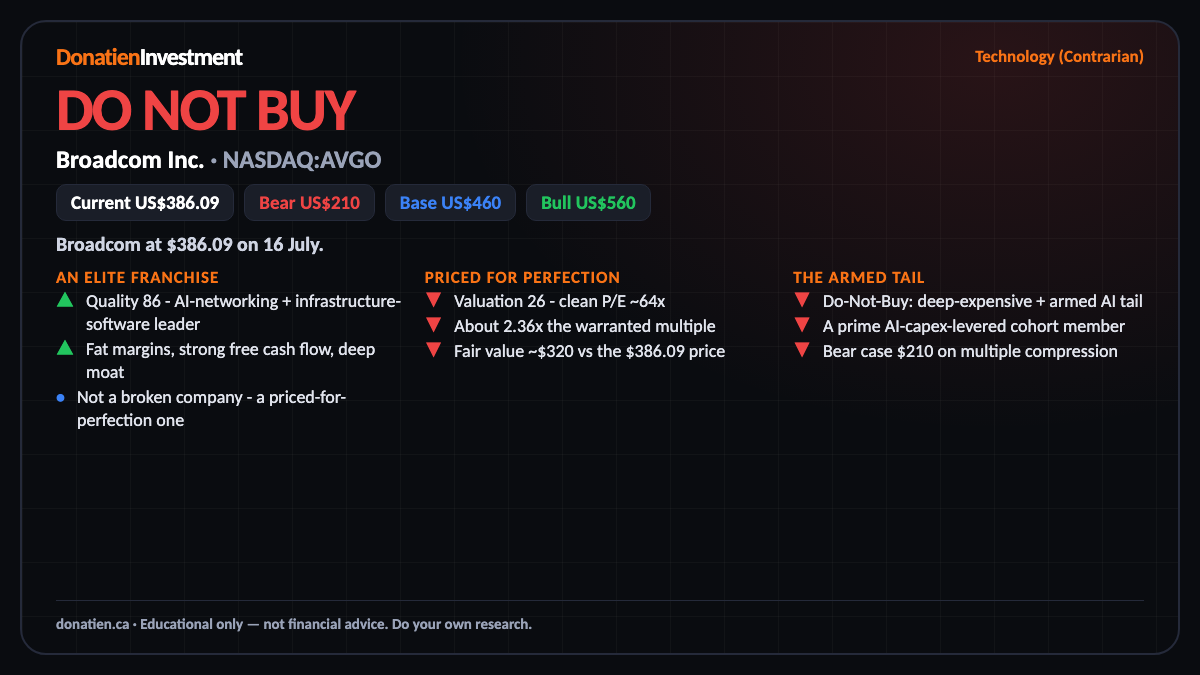

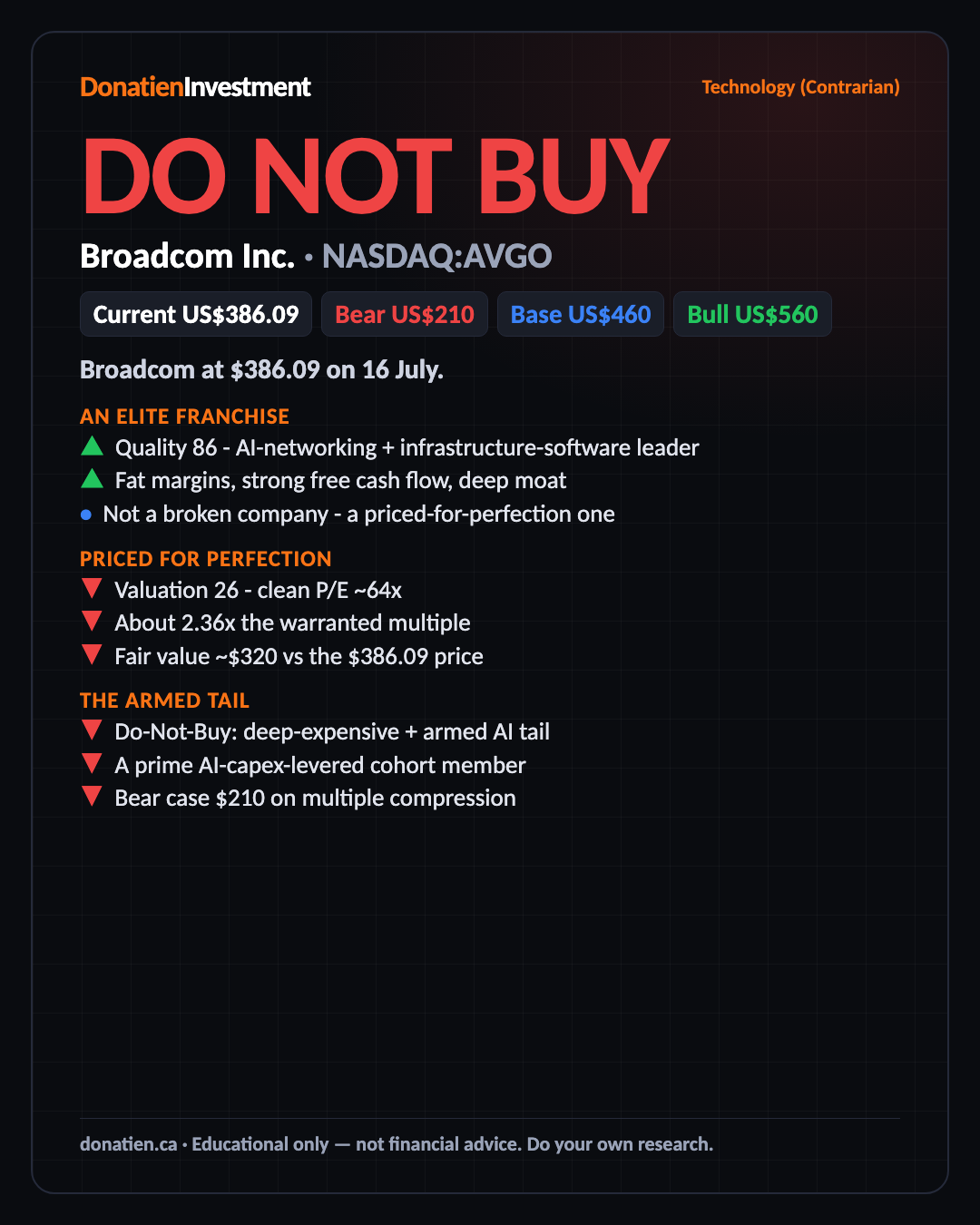

Broadcom Inc. (NASDAQ:AVGO) DO NOT BUY

A dominant AI-networking franchise priced for perfection — near 64x clean earnings — into an armed AI-concentration unwind.

Broadcom at $386.09 on 16 July. An elite business at the wrong price: near 64 times clean earnings, about 2.36 times what rates and growth warrant, the framework rates it Do-Not-Buy.

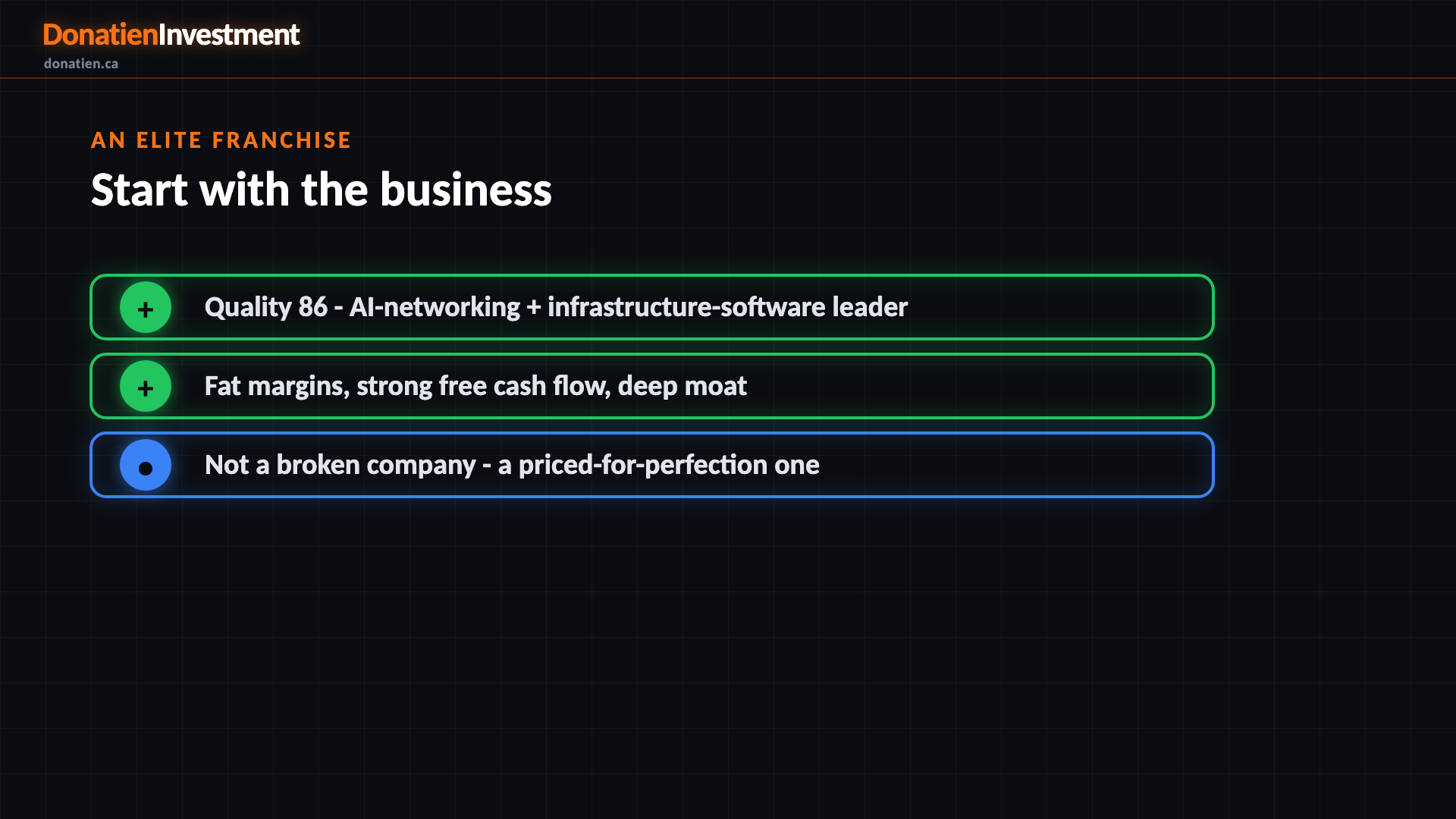

An elite franchise

Broadcom is an elite franchise, scoring 86 on quality. This Do-Not-Buy is about the price, not the business. It pairs a dominant AI-networking and custom-silicon position with high margins, strong free cash flow and a deep moat. The company is firing on every cylinder, which is exactly why the market has priced it for perfection.

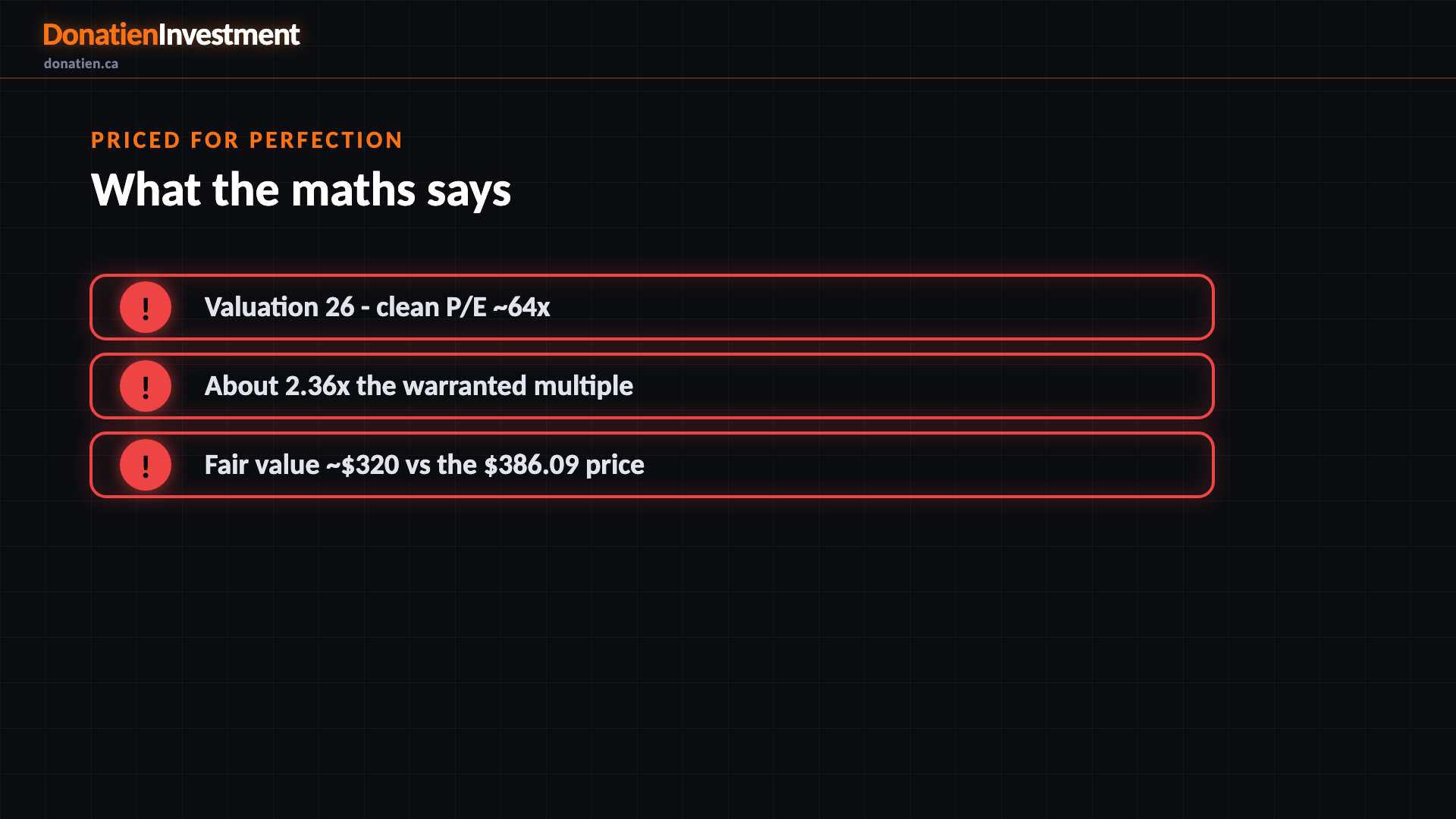

Priced for perfection

On clean earnings Broadcom trades near 64 times, about 2.36 times warranted. Fair value sits near 320, below the 386.09 price. That is comfortably into the expensive band, so the valuation ceiling caps it at Hold, and a second trigger takes it further. You are paying today for years of flawless execution.

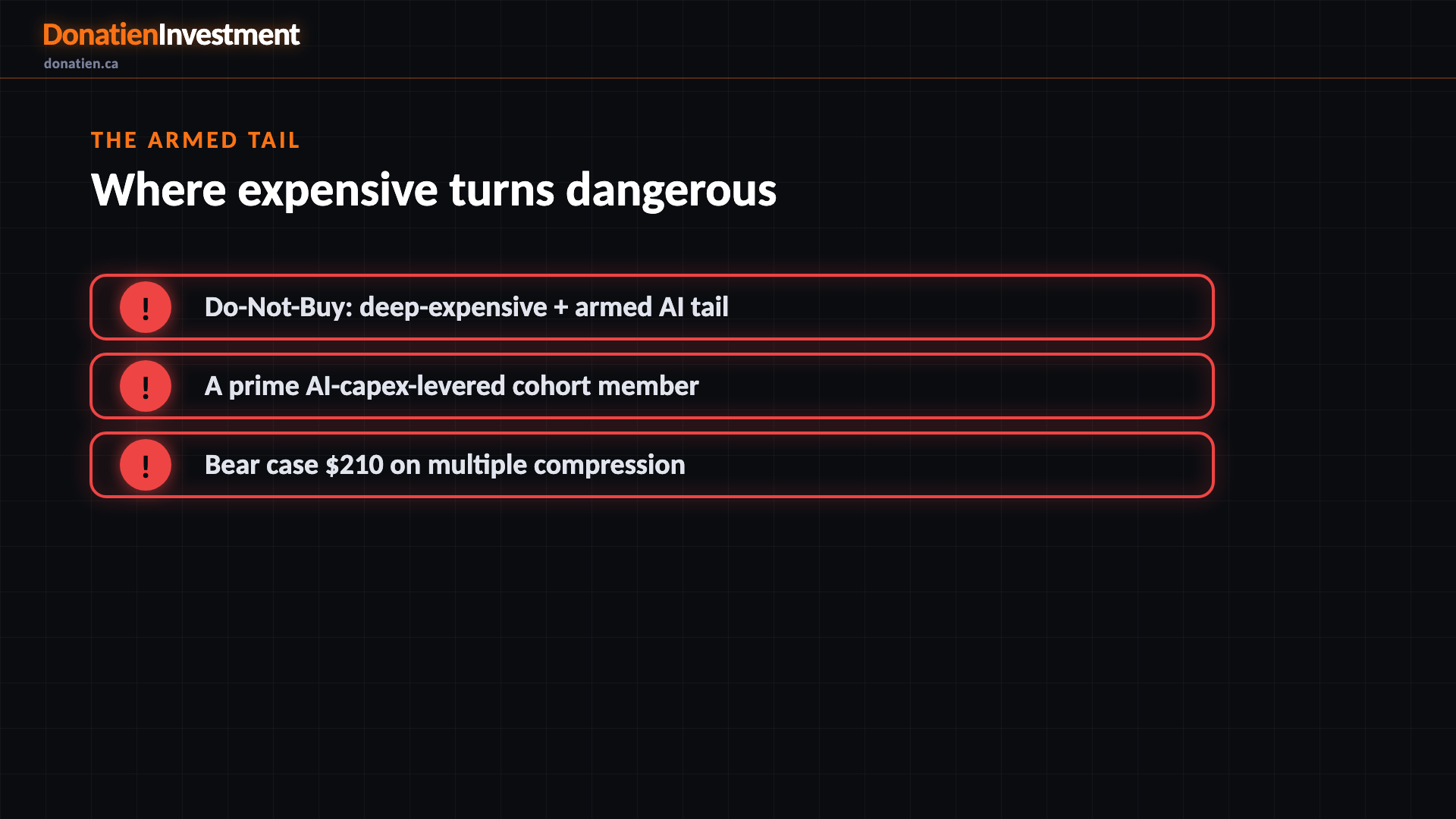

The armed tail

Broadcom is a prime AI-capex-levered name into an armed concentration unwind. If that trade turns, the bear case sits near 210. It is driven by the multiple compressing rather than the business breaking, and the de-rating would be market-wide as a handful of AI mega-caps dominate the index. Deeply expensive and exposed to a live systemic tail is what pushes this to Do-Not-Buy.

What could go wrong

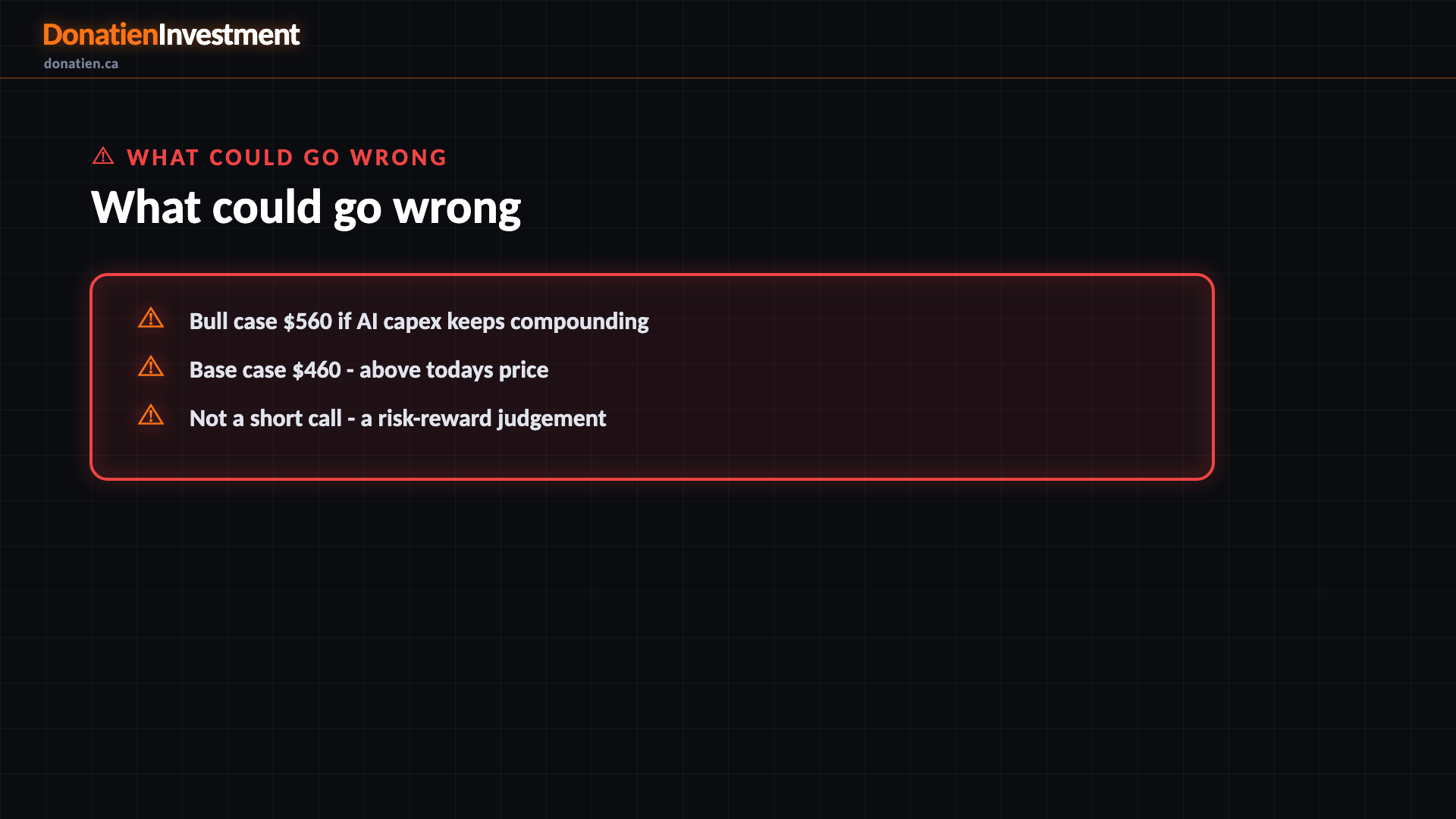

The honest other side: the base case of 460 sits above today price, and the bull reaches 560 if AI capex compounds. So this is not a forecast of collapse. The Do-Not-Buy reflects the shape of the risk: a fat left tail to 210 against a multiple already 2.36 times warranted. From 386.09 the model will not back the truck up.

Risk vs Reward

Against the current US$386.09, the report frames a bull case at US$560 (+45%), a base case at US$460 (+19%) and a bear case at US$210 (-46%). See the full report for the probability weight behind each path.

The verdict

A dominant AI-networking franchise priced for perfection — near 64x clean earnings — into an armed AI-concentration unwind.

Read the full report on donatien.ca →{kind=link}

{kind=link}