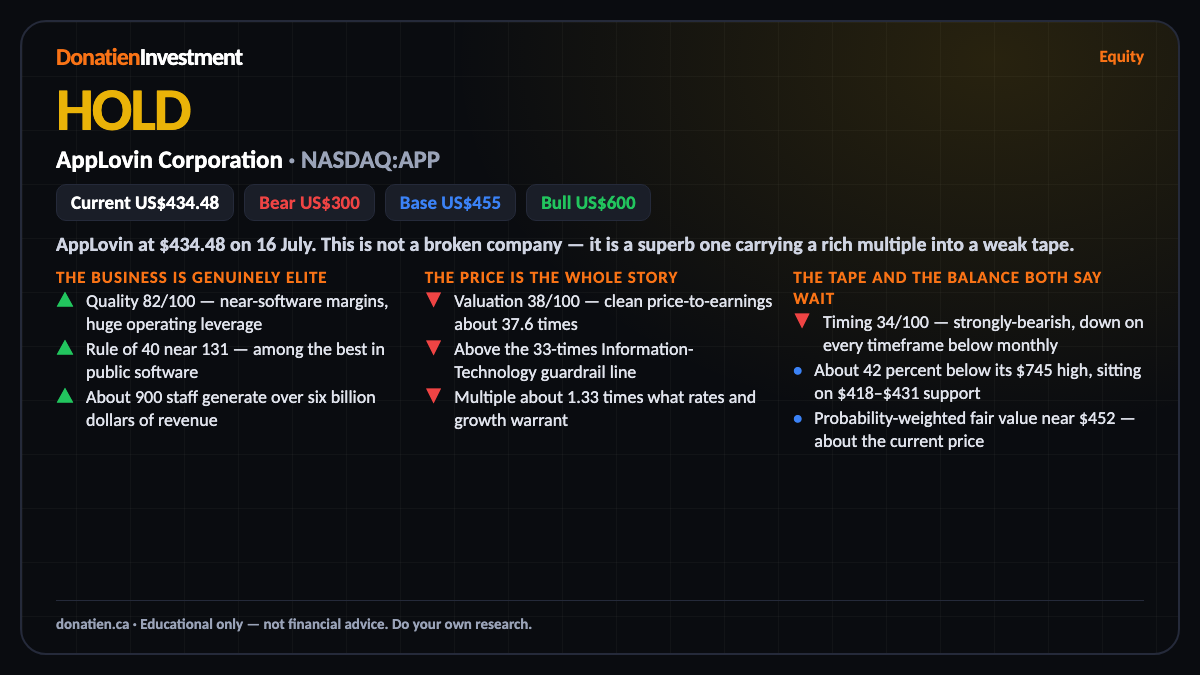

AppLovin Corporation (NASDAQ:APP) HOLD

One of the best businesses in public software, at a price that already pays for the bull case — elite quality, but the valuation ceiling caps it at Hold across every horizon.

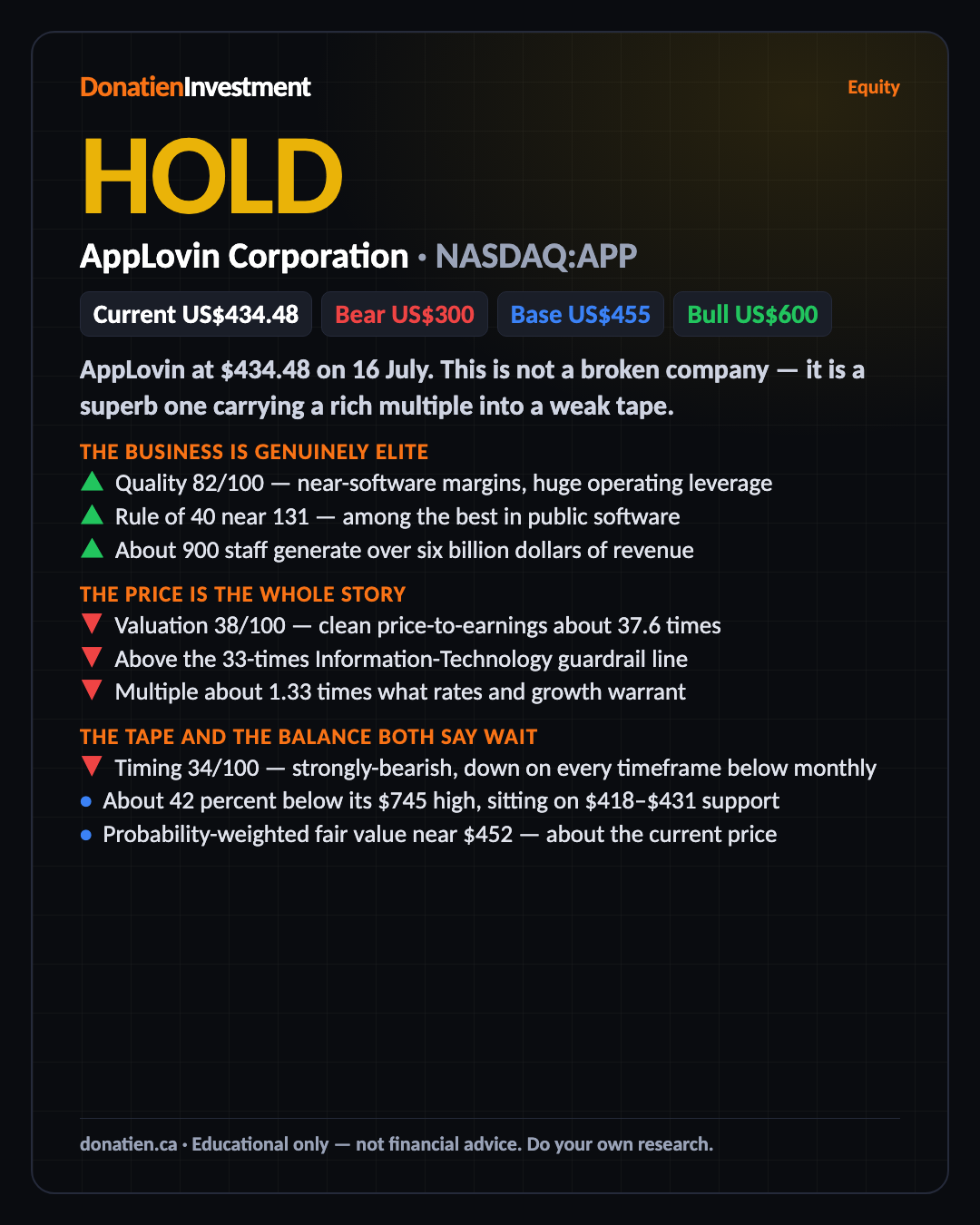

AppLovin at $434.48 on 16 July. This is not a broken company — it is a superb one carrying a rich multiple into a weak tape. The framework rates the business elite and the price expensive, and the two net out to Hold.

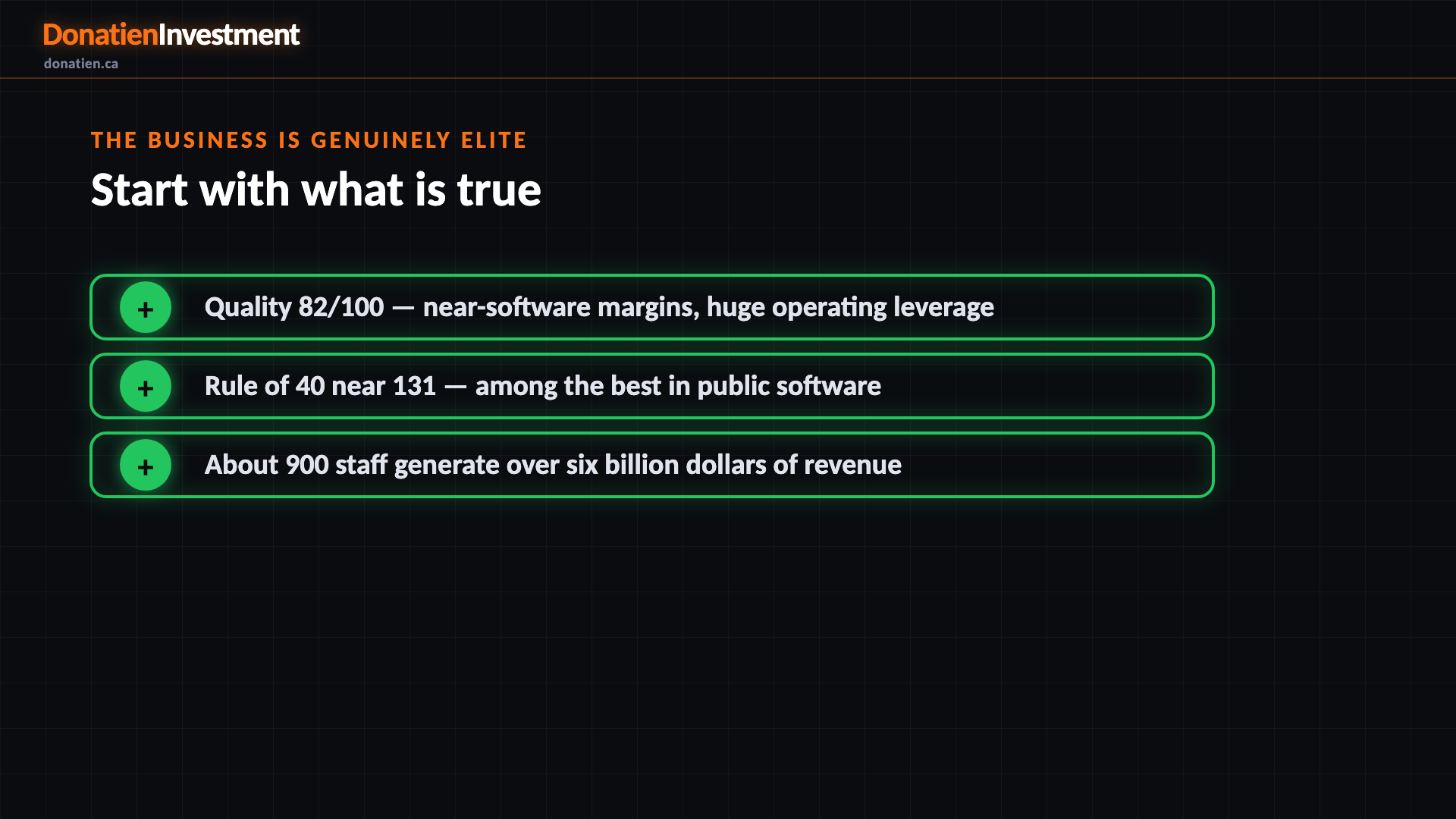

The business is genuinely elite

AppLovin scores 82 on quality, and that is well earned. Its AXON advertising engine runs at gross margins near 88 percent, and a company of roughly 900 people generates over six billion US dollars of nearly-all-software revenue. Growth plus cash-flow margin puts its Rule of 40 near 131, one of the highest readings in public software. This Hold is not a verdict on the company. It is a superb business — the whole debate is the price you pay for it.

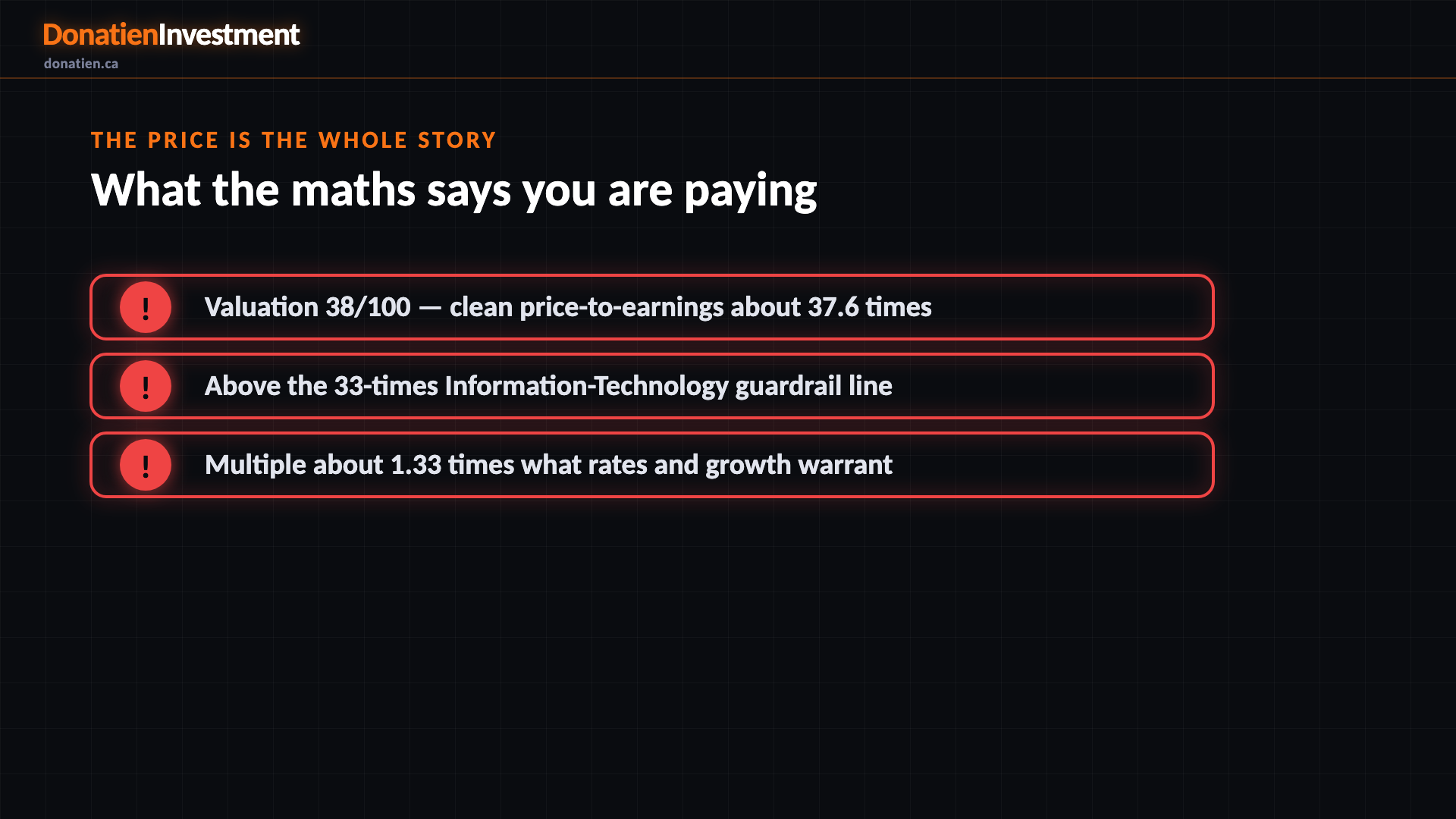

The price is the whole story

On clean earnings AppLovin trades near 37.6 times, above the 33-times line the framework treats as rich for Information Technology, and about 1.33 times the multiple that current rates and disciplined growth actually warrant. That trips the valuation-ceiling gate, which caps the signal at Hold at every horizon regardless of momentum. At this price you are underwriting years of thirty-percent-plus compounding and a successful move into e-commerce. That is possible — but it is the bull case being paid for today, not a margin of safety.

The tape and the balance both say wait

The tape is the weakest part of the picture. AppLovin is about 42 percent below its high of 745 dollars and in a downtrend on every timeframe below the monthly, pressing support around 418 to 431. No entry path is open yet, so this is buy-on-confirmation territory. And the arithmetic agrees: weight the scenarios and fair value lands near 452 dollars, essentially the current price. When the reward for being right is already in the stock, the honest call is Hold and wait for a better entry, not chase.

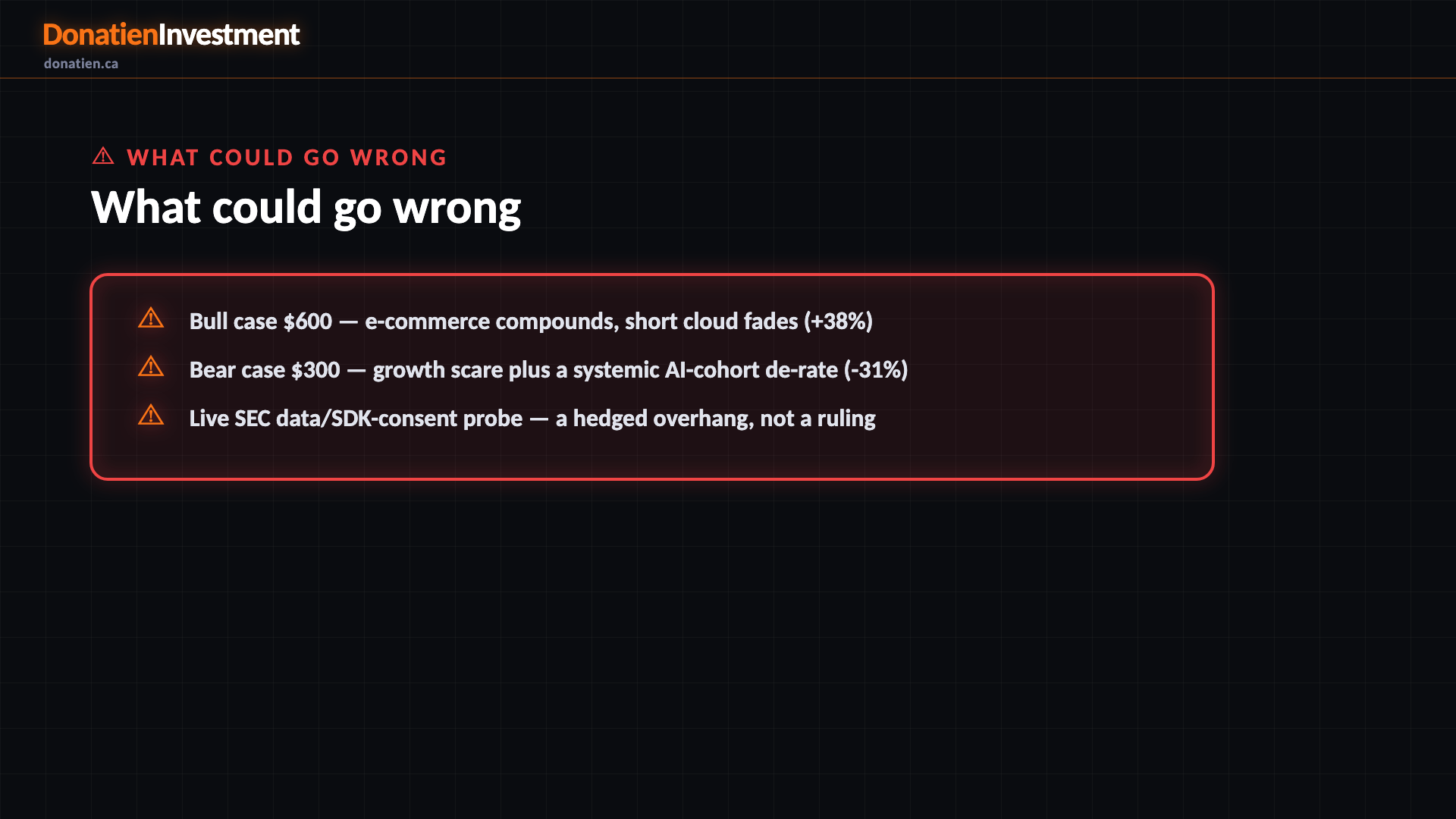

What could go wrong

The distribution is roughly symmetric with fat tails on both sides. The bull case reaches 600 dollars if e-commerce compounds and the short-seller cloud fades. The bear case near 300 has two legs — a company-specific growth scare, and a market-wide de-rate of the AI cohort that would hit the multiple regardless of results. One genuine overhang: there is an active SEC investigation into the company's data-collection and SDK-consent practices, ongoing since late 2025. It is an investigation, not a ruling — no charge has been filed and nothing is proven, and one short-seller report was retracted with an apology. It is carried as a live risk, not the reason for the call.

Risk vs Reward

Against the current US$434.48, the report frames a bull case at US$600 (+38%), a base case at US$455 (+5%) and a bear case at US$300 (-31%). See the full report for the probability weight behind each path.

The verdict

One of the best businesses in public software, at a price that already pays for the bull case — elite quality, but the valuation ceiling caps it at Hold across every horizon.

Read the full report on donatien.ca →{kind=link}

{kind=link}