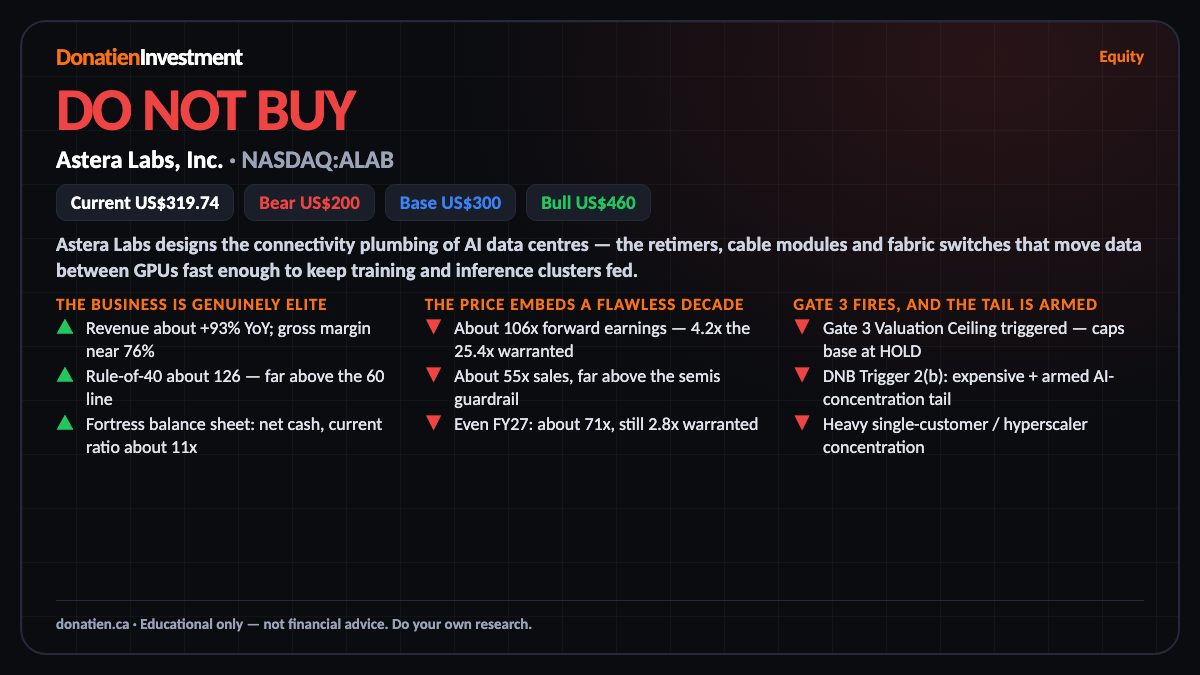

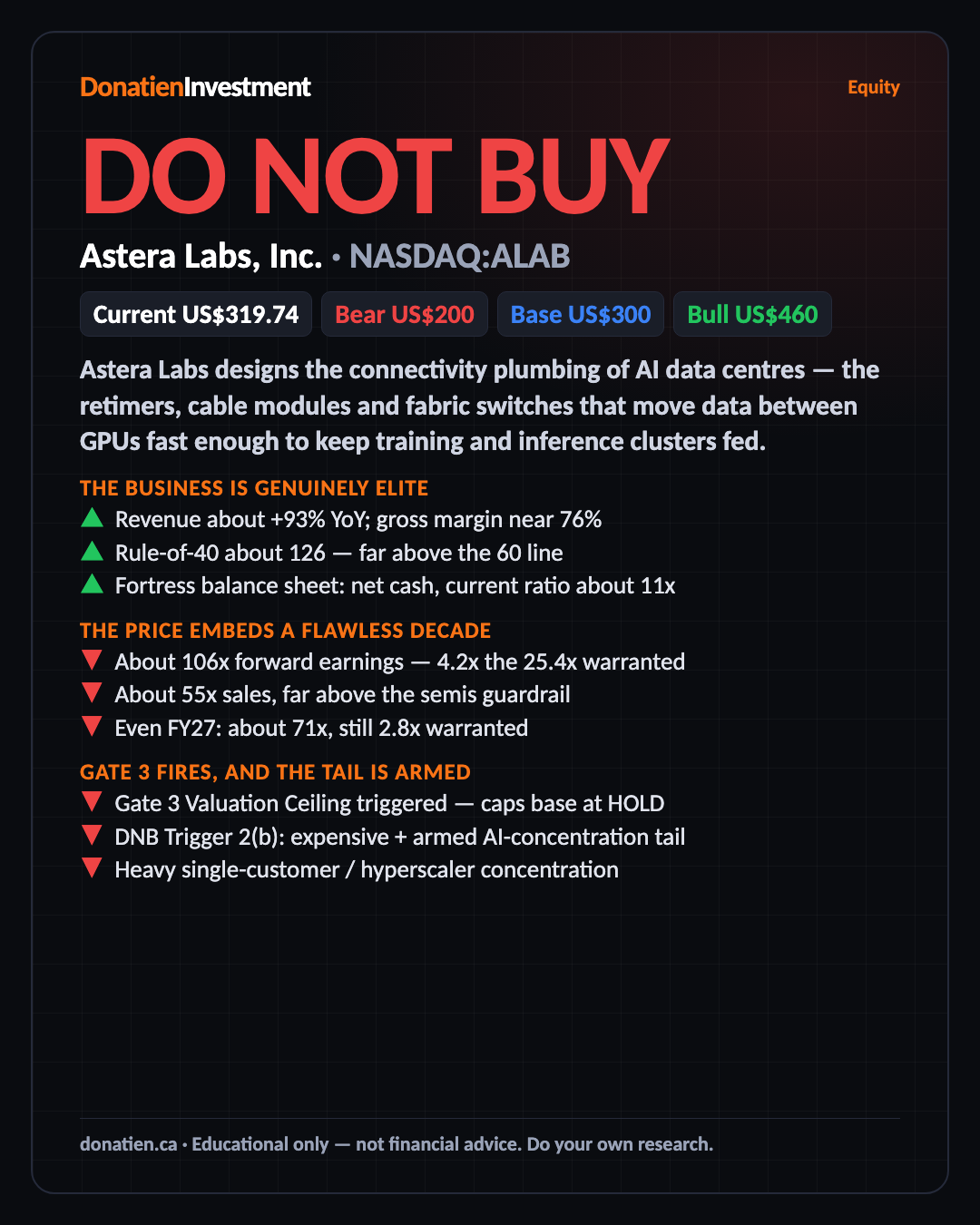

Astera Labs, Inc. (NASDAQ:ALAB) DO NOT BUY

Astera Labs is a genuinely excellent, hyper-growth AI-connectivity business — and priced at roughly four times its rate-and-growth-warranted multiple. This is a price-and-risk call, not a quality call: we are declining to buy the hype at about 106 times forward earnings, into an armed AI-concentration tail. Do not buy on any horizon.

Astera Labs designs the connectivity plumbing of AI data centres — the retimers, cable modules and fabric switches that move data between GPUs fast enough to keep training and inference clusters fed. The business is excellent. The price, at about 319.74 US dollars and roughly 55 times sales, is the problem.

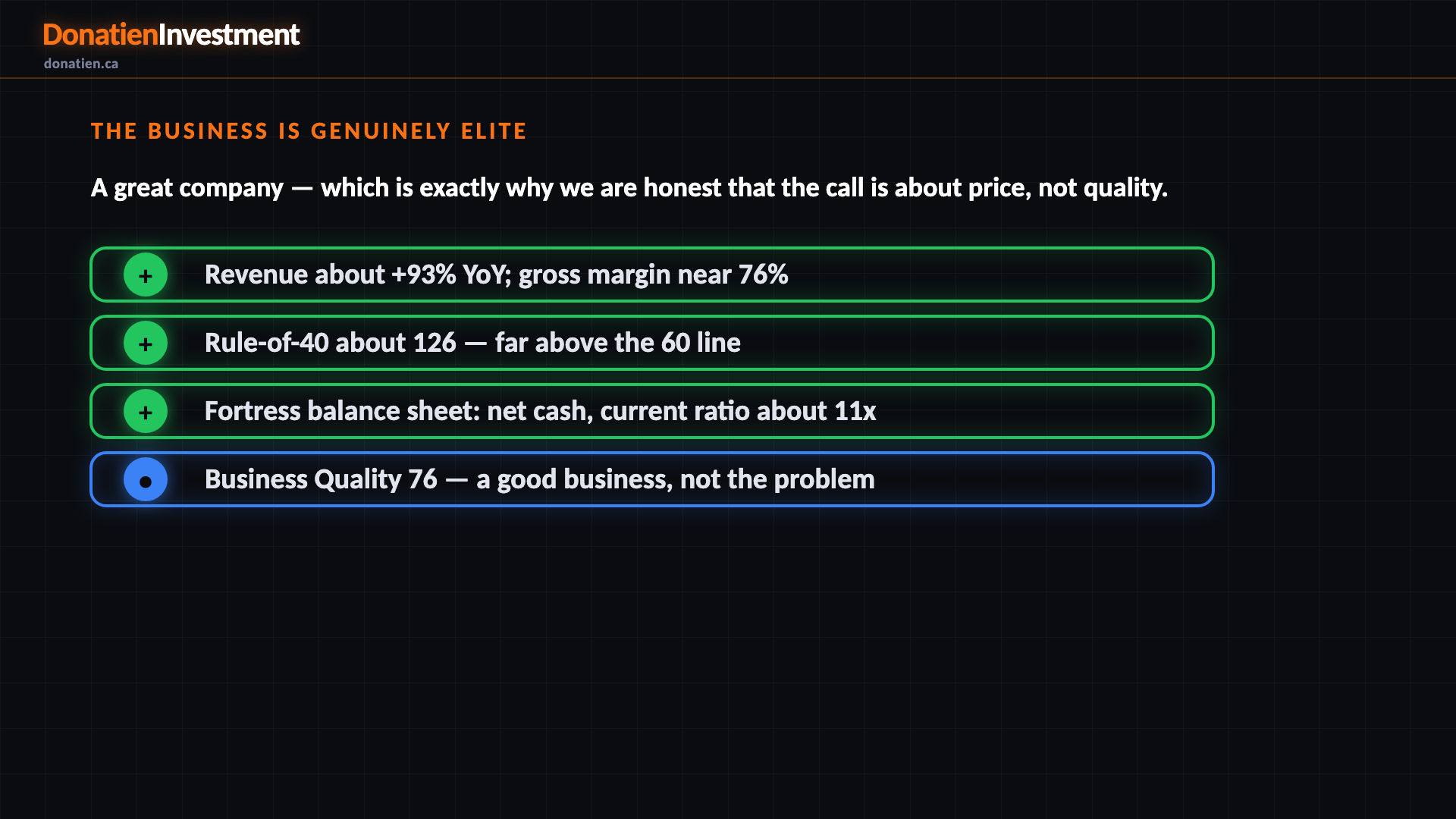

The business is genuinely elite

First, give the business its due. Revenue grew about 93 percent year on year, gross margin runs near 76 percent, and the balance sheet is a fortress — net cash, almost no debt, a current ratio around eleven times. Growth of roughly 90 percent plus a non-GAAP operating margin near 36 percent gives a Rule-of-40 score of about 126, far above the 60 line that marks exceptional. Very few semiconductor names print an operating profile this good. Business Quality scores 76. This is not the reason we say do not buy.

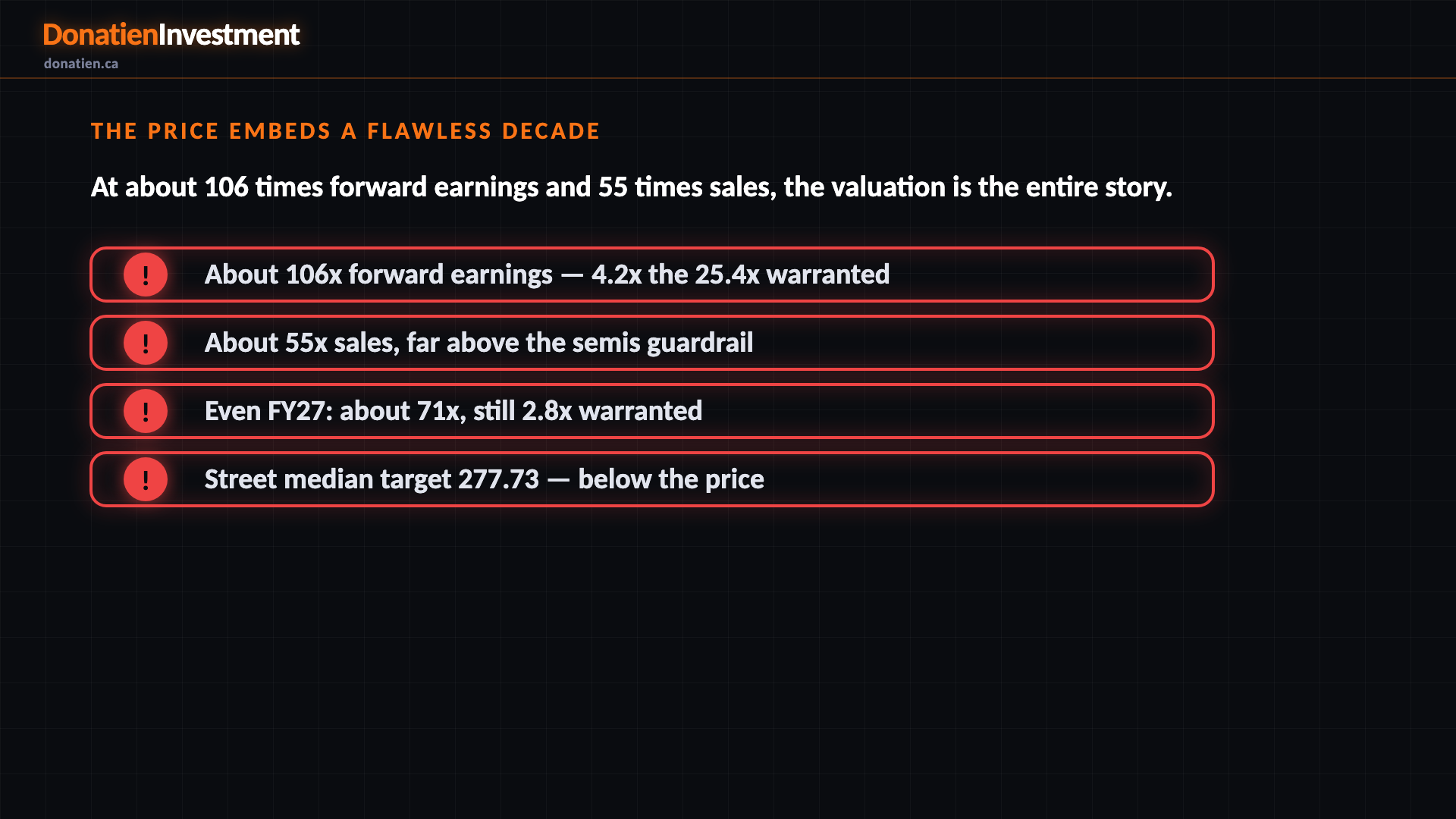

The price embeds a flawless decade

Now the price. A disciplined two-stage model warrants a multiple of about 25.4 times. The stock trades near 106 times forward non-GAAP earnings — about 4.2 times that warranted anchor — and roughly 55 times sales, far above the semiconductor guardrail. Even a year out, on FY27 estimates, it is still about 71 times, or 2.8 times warranted. A strict anchor points to about 115 US dollars; even a generous proven-grower premium struggles past 150. The Street's own median target is 277.73 US dollars — below today's price. Valuation scores 16. The price embeds a near-flawless path the business would have to deliver perfectly to justify.

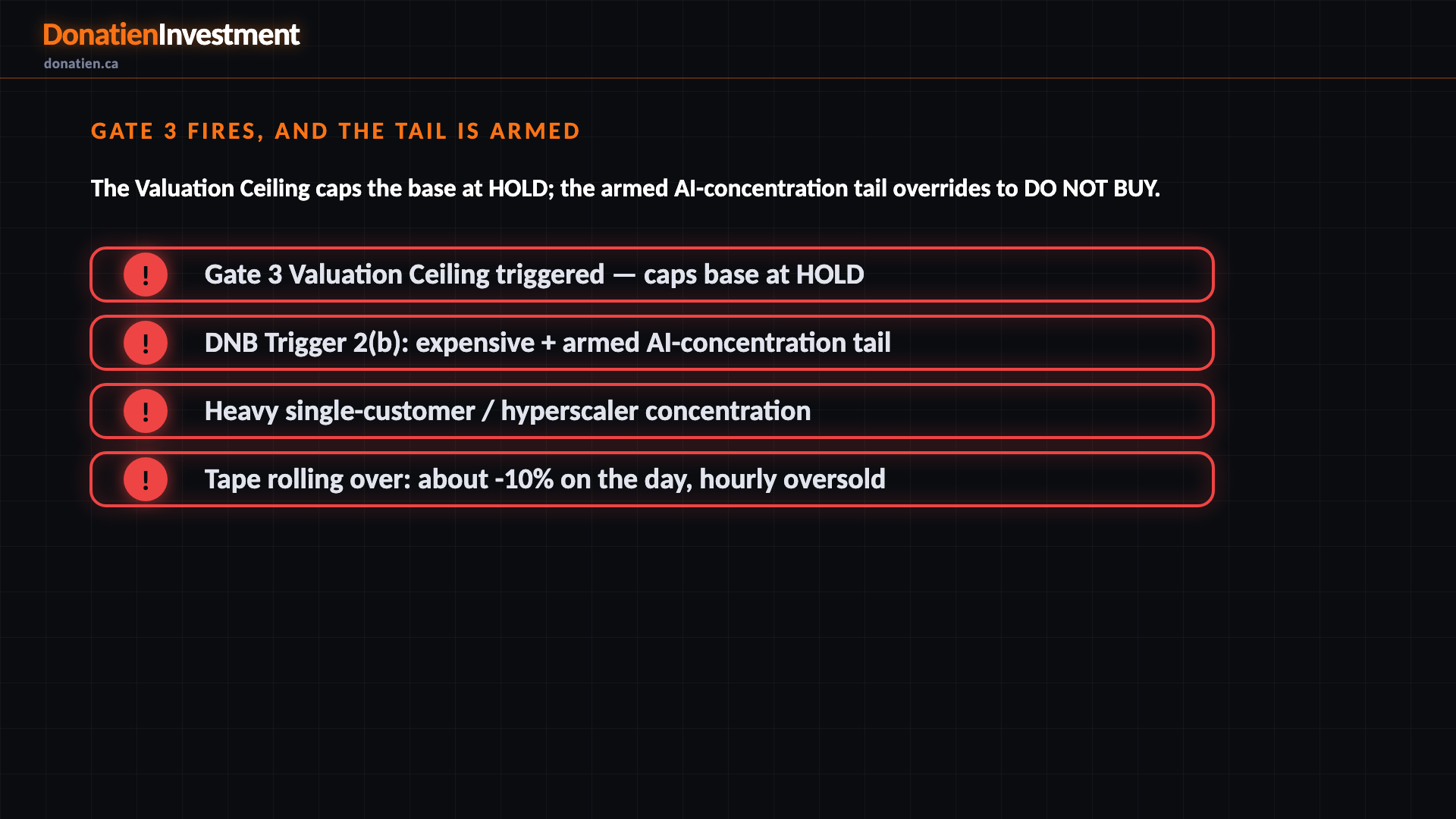

Gate 3 fires, and the tail is armed

Two things stack. The Valuation-Ceiling gate triggers on that extreme multiple, capping the base signal at hold. Then Do-Not-Buy Trigger 2, arm (b), fires: an expensive name that is a genuine AI-capex-cohort member, into an armed systemic tail the macro report flags — the S&P 500 concentration and AI earnings-quality unwind, with the top ten names about 41 percent of the index. The near-term tape has also cracked, down about 10 percent on the day, with the hourly chart oversold. Timing scores 38. The honest counter-case for a mere hold is real — the named tail triggers have not yet pulled — but expensive plus armed plus a true cohort member is exactly what the rule exists to catch.

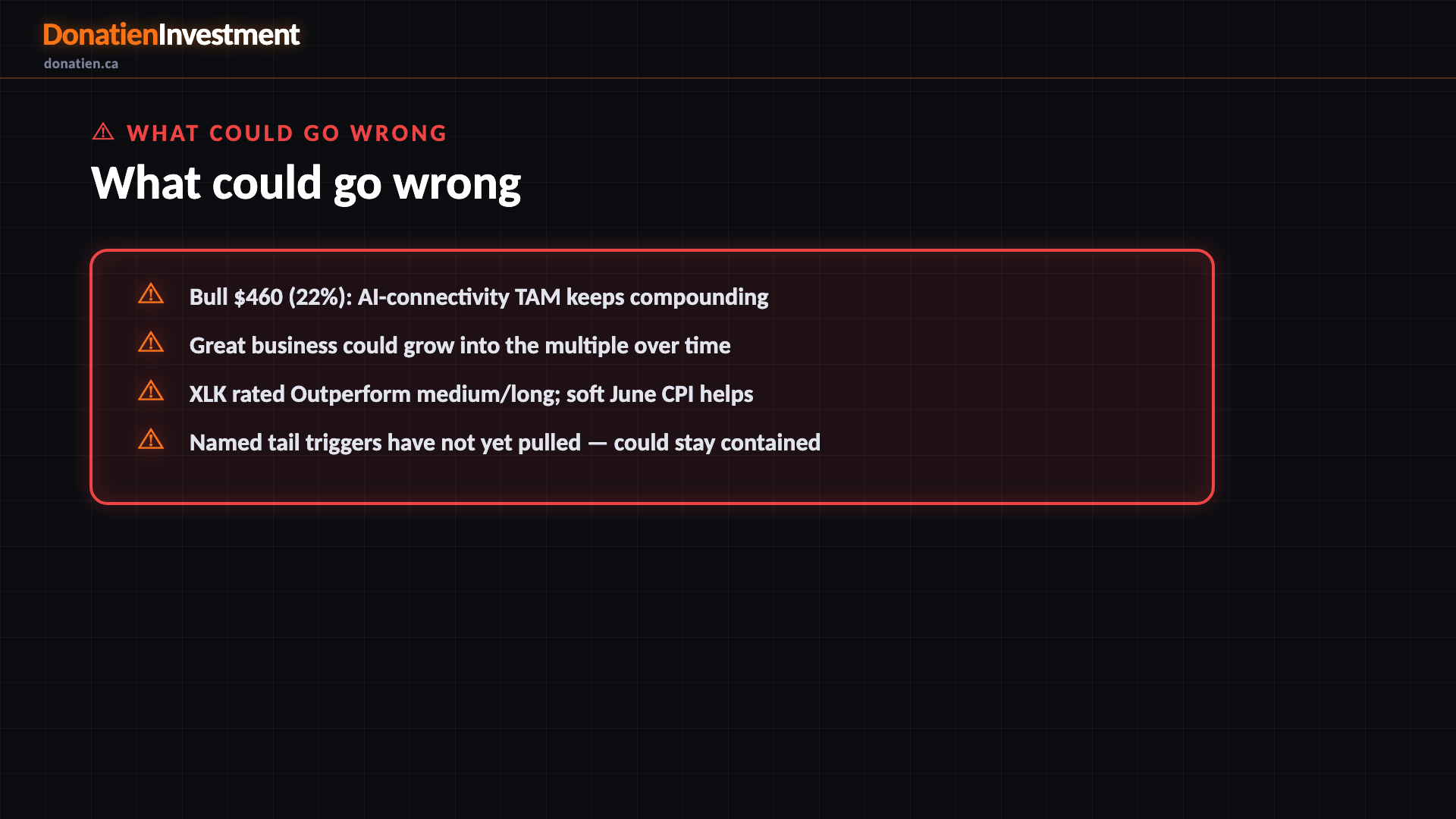

What could go wrong

Bull $460 (22%): AI-connectivity TAM keeps compounding. Great business could grow into the multiple over time. XLK rated Outperform medium/long; soft June CPI helps. Named tail triggers have not yet pulled — could stay contained.

Risk vs Reward

Against the current US$319.74, the report frames a bull case at US$460 (+44%), a base case at US$300 (-6%) and a bear case at US$200 (-37%). See the full report for the probability weight behind each path.

The verdict

Astera Labs is a genuinely excellent, hyper-growth AI-connectivity business — and priced at roughly four times its rate-and-growth-warranted multiple. This is a price-and-risk call, not a quality call: we are declining to buy the hype at about 106 times forward earnings, into an armed AI-concentration tail. Do not buy on any horizon.

Read the full report on donatien.ca →{kind=link}

{kind=link}