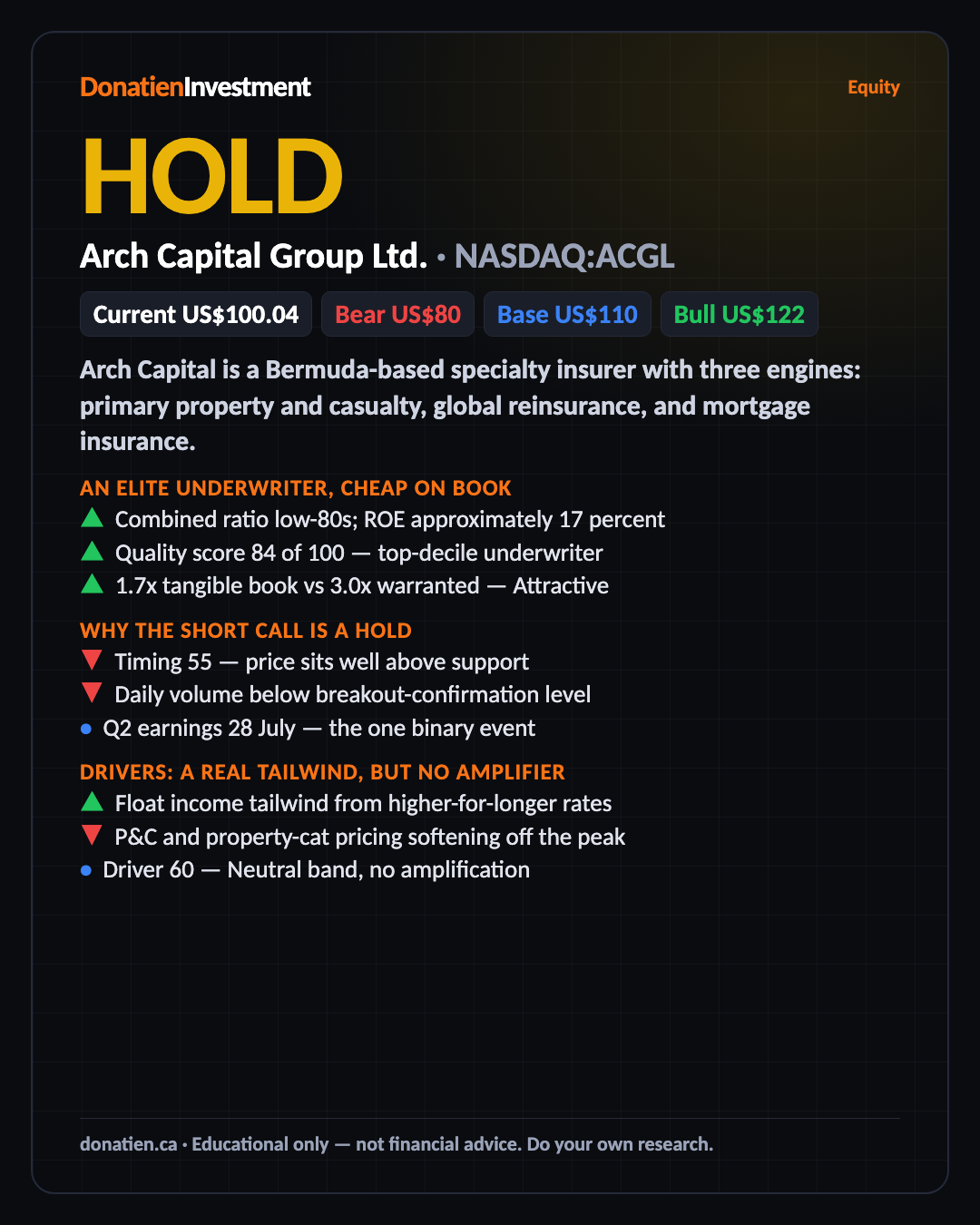

Arch Capital Group Ltd. (NASDAQ:ACGL) HOLD

Arch Capital is an elite specialty insurer trading at an attractive 1.7 times tangible book, and the medium and long calls are both BUY. But the short-term call is HOLD: the tape offers no discounted entry and a Q2 print lands on 28 July, so the near-term stance is buy on confirmation, accumulate on weakness.

Arch Capital is a Bermuda-based specialty insurer with three engines: primary property and casualty, global reinsurance, and mortgage insurance. It compounds book value through disciplined, cycle-aware underwriting and opportunistic buybacks rather than a dividend. The report rates it HOLD short-term, BUY medium and long, at a price of 100.04 US dollars.

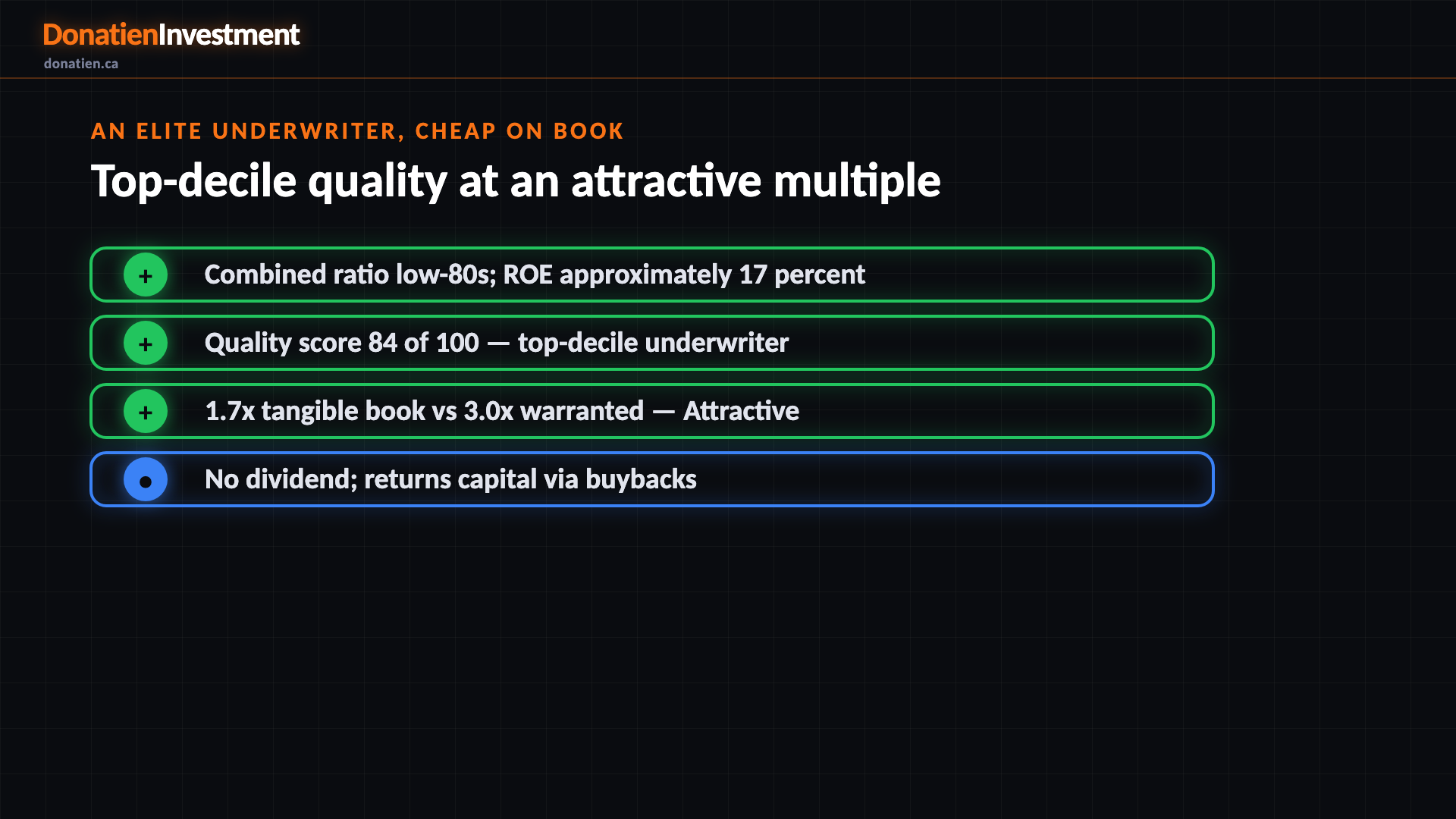

An elite underwriter, cheap on book

The quality here is genuine. Arch runs a combined ratio in the low eighties, well under the hundred-percent underwriting-profit line, and earns returns on equity in the high teens. Book value per share keeps compounding even as buybacks shrink the share count. On valuation, the shares trade at roughly 1.7 times tangible book against a warranted multiple near three times, a ratio of 0.57 that sits firmly in the attractive band. Even on a conservative growth assumption the stock still looks cheap for the quality.

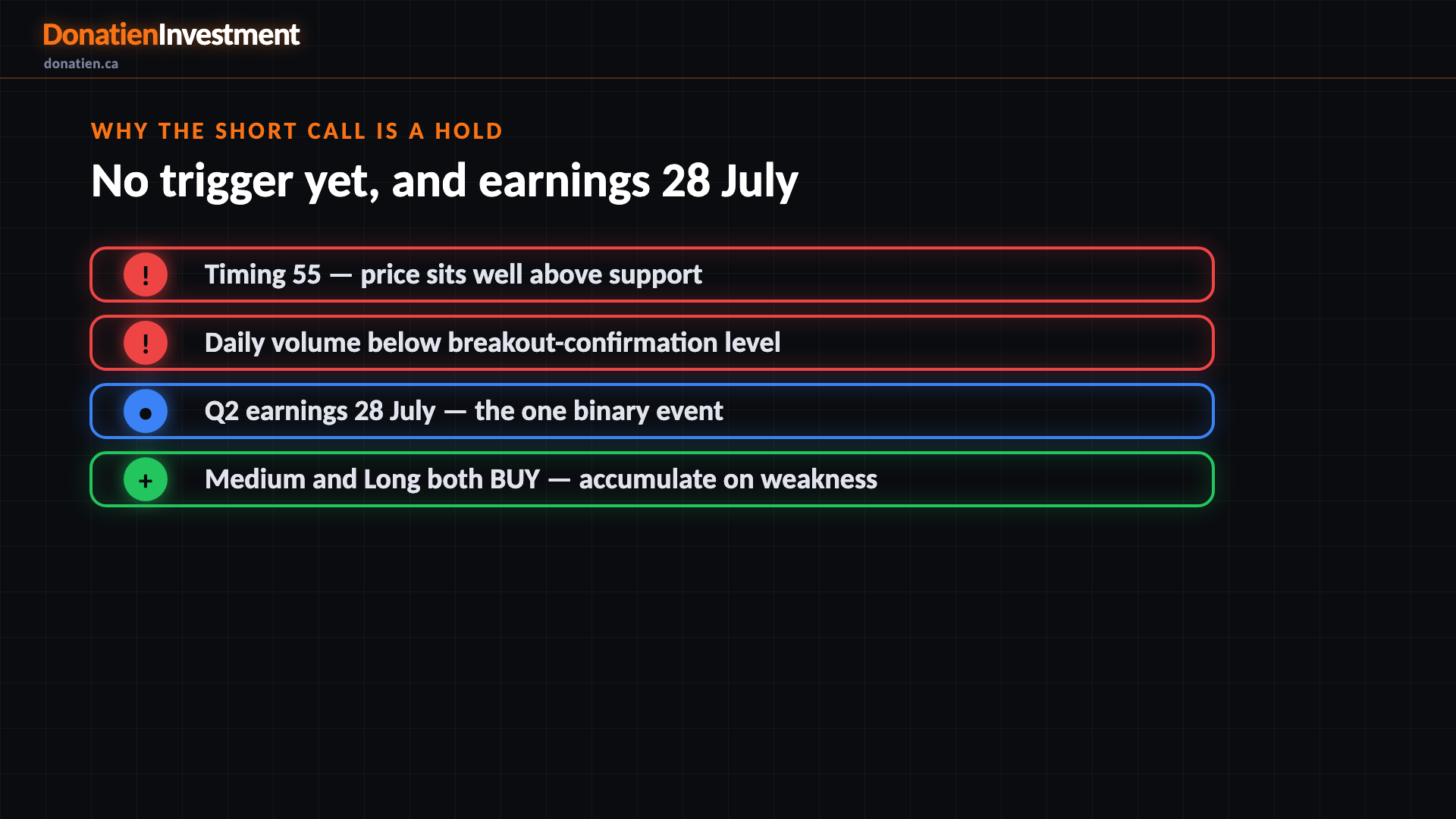

Why the short call is a hold

So why not buy today. The near-term tape gives no discounted entry: the price sits about 14 percent above weekly support, daily volume is running below the level needed to confirm a breakout, and there is no fresh trigger. On top of that, a Q2 print lands on 28 July, the one binary event for this name. The fundamental case is already met — the stock is cheap — but with no technical or catalyst confirmation, the timing score is only 55 and the short horizon is capped to hold. Buy on confirmation.

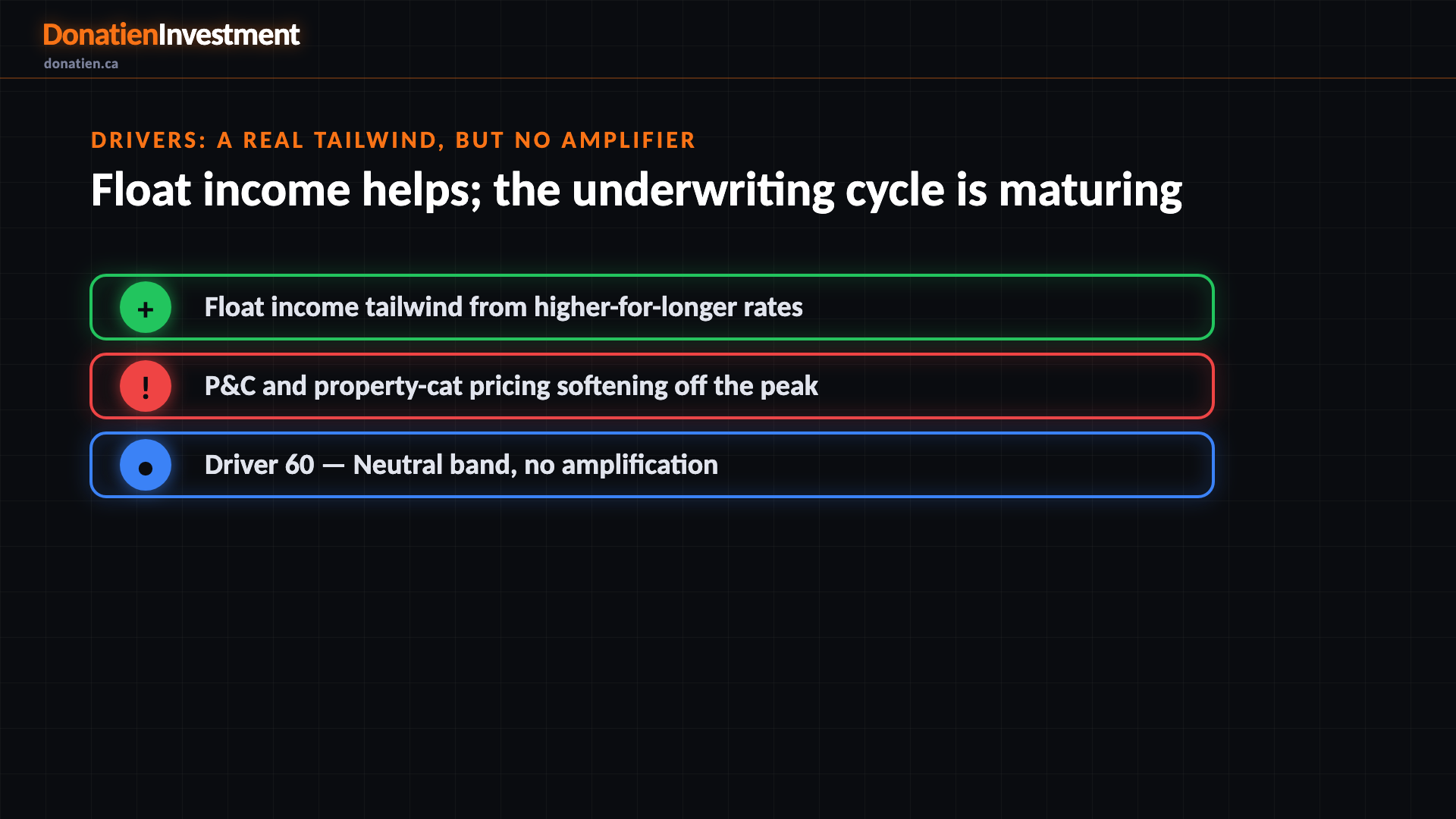

Drivers: a real tailwind, but no amplifier

The underlying drivers are balanced. Higher-for-longer rates let Arch reinvest its float at attractive yields, a genuine tailwind for investment income. But property-catastrophe and P&C pricing are softening off the the hard-market peak, and mortgage earnings are near cycle highs. The driver score of 60 sits in the neutral band, which means it is not eligible to amplify the signal. The report is honest about this: it does not manufacture a stronger buy. Quality carries the longer-horizon case, not a cyclical push.

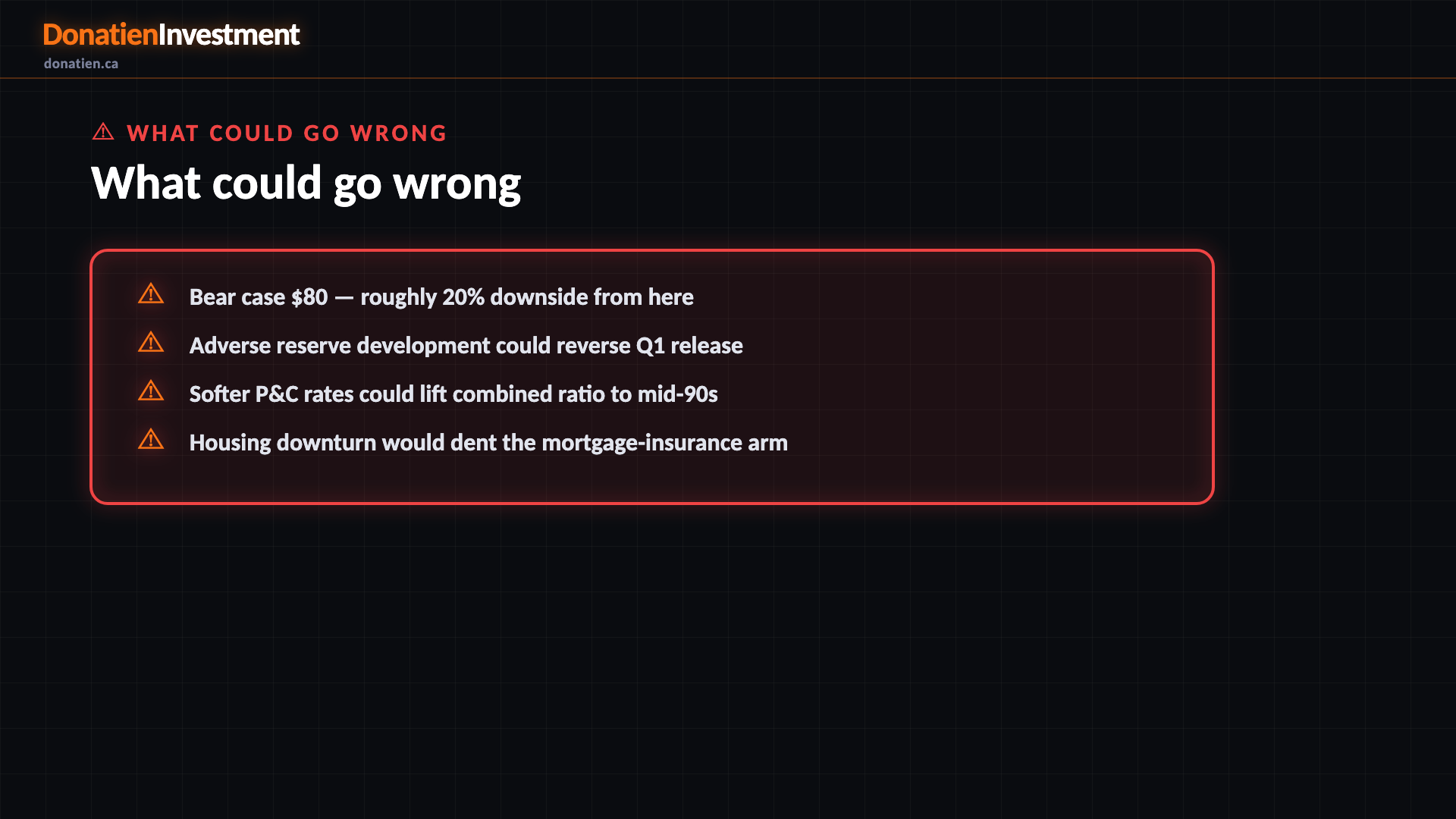

What could go wrong

The risks here are cyclical, not solvency. The bear case sees the stock fall to about 80 US dollars, roughly 20 percent below today. That would take an adverse reserve-development quarter reversing the Q1 release, softer P&C rates lifting the combined ratio back toward the mid-90s, a heavy catastrophe season, and a housing downturn denting the mortgage arm. And the 28 July print is a live, binary near-term event. This is a real risk, not a distant tail.

Risk vs Reward

The base case is 110 US dollars at 55 percent — mid-single-digit book-value growth plus buybacks and a small re-rating toward the analyst consensus. The bull case is 122 US dollars at 25 percent if pricing holds and float income compounds. The bear case is 80 US dollars at 20 percent on a cycle-driven de-rating. The probability-weighted centre of gravity is the base case.

The verdict

The honest read is a hold now, a buy later. Arch Capital is one of the best-run specialty insurers in the world, and at 1.7 times tangible book it is genuinely cheap for the quality — which is why the medium and long calls are both buy. But the short-term stance is hold: there is no discounted entry, no volume-confirmed trigger, and a Q2 print on 28 July. The plan is to accumulate on weakness or buy on confirmation, not to chase it near the top of its range. This is analysis, not financial advice.

Analysis, not financial advice. Financial Freedom. Together.

Read the full report on donatien.ca →{kind=link}

{kind=link}