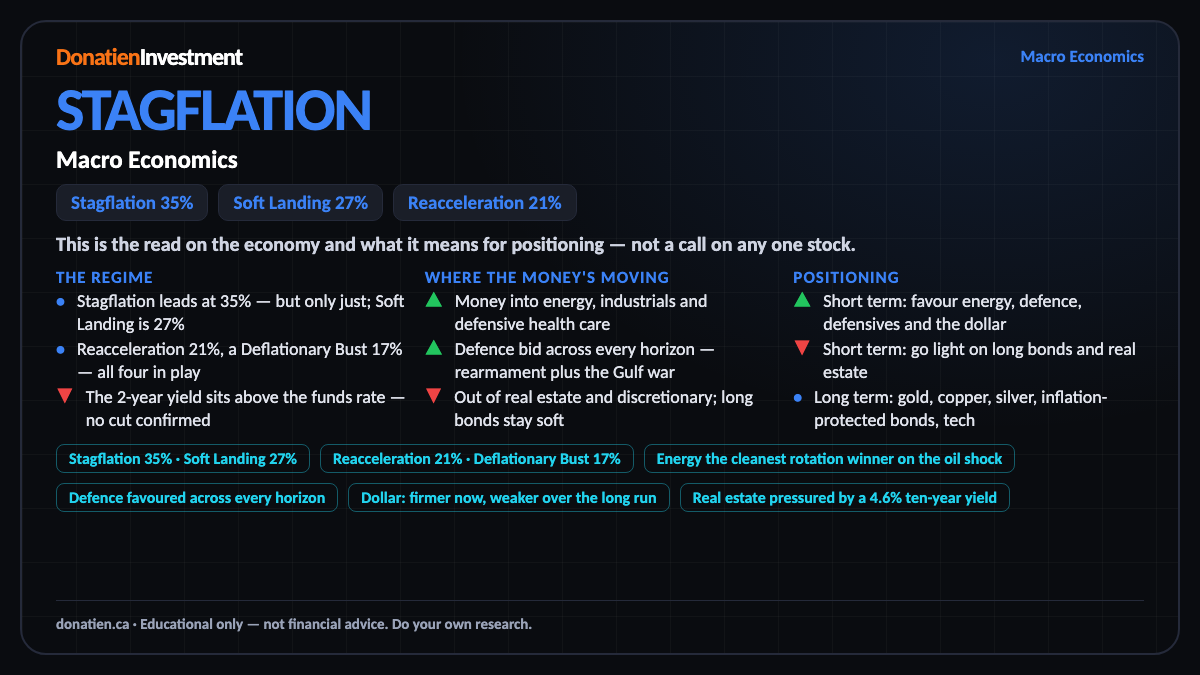

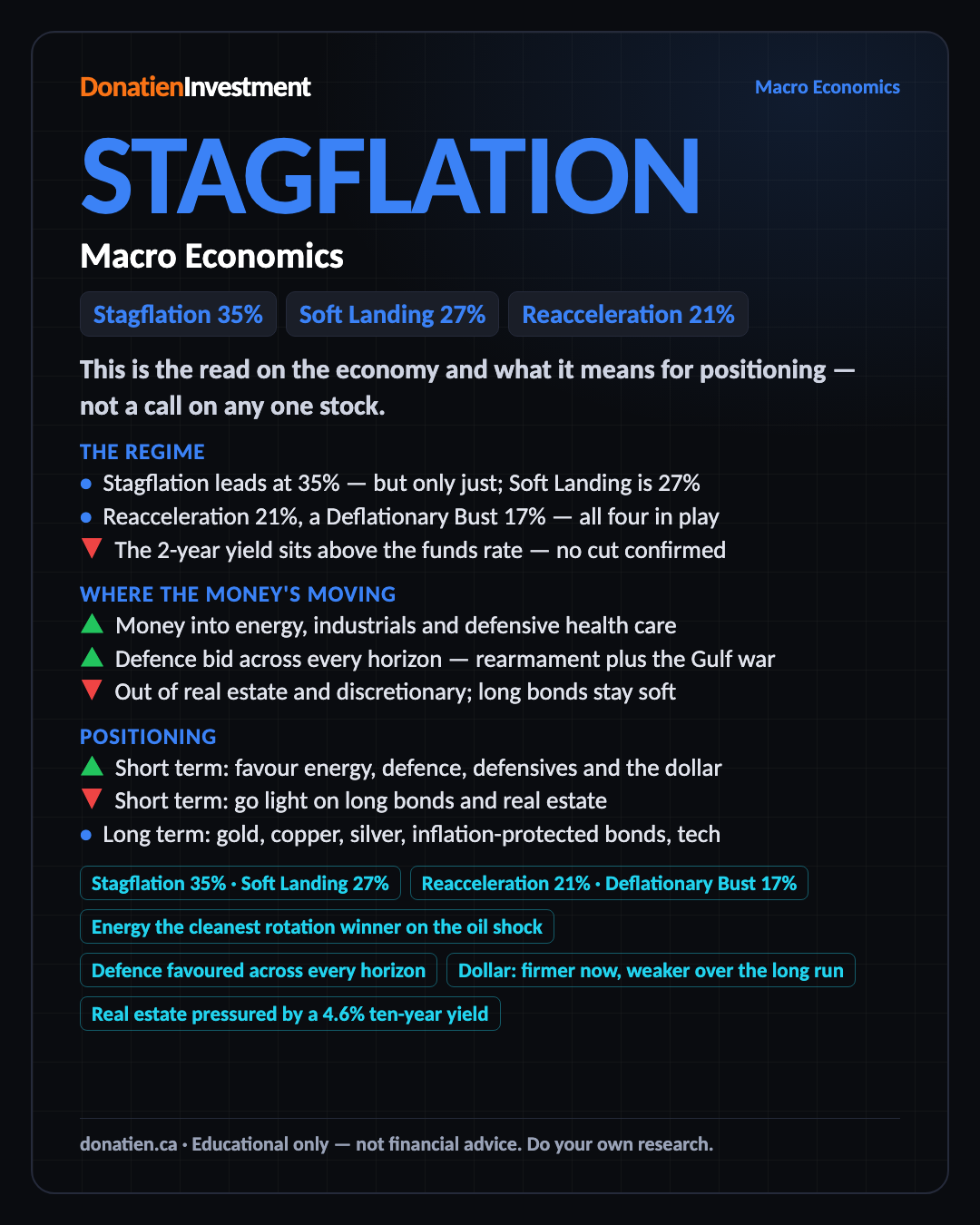

Macro Economics STAGFLATION

Stagflation holds a narrow lead — growth slows but inflation stays sticky. But the source has changed: June inflation came in soft, so the risk now comes from an Iran/Hormuz oil supply shock, not services. A Soft Landing is closing to 27%, so respect the higher-for-longer tape now and keep the disinflation case live.

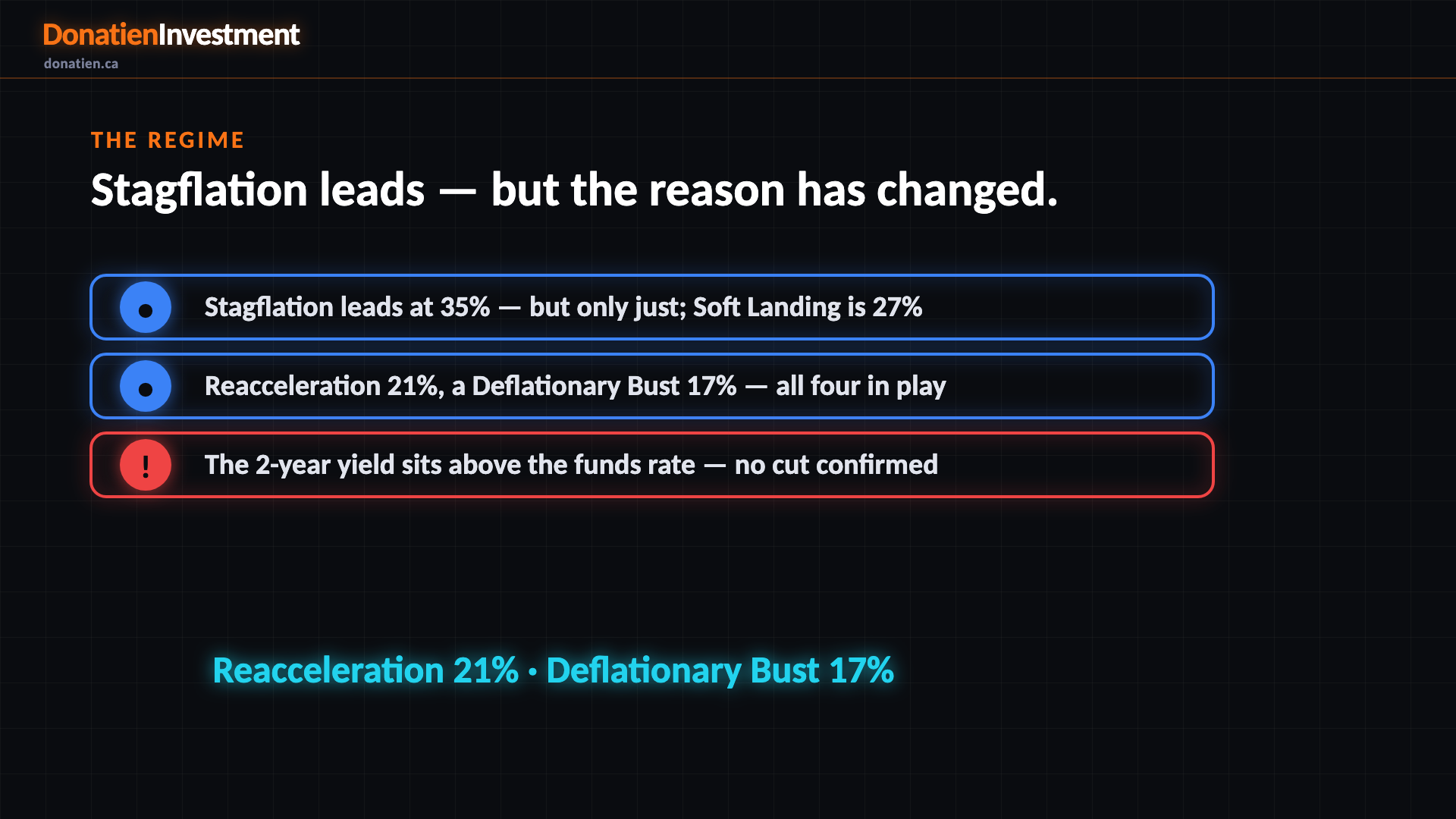

This is the read on the economy and what it means for positioning — not a call on any one stock. Four scenarios are always in play — Stagflation, a Soft Landing, a Reacceleration, and a Deflationary Bust — and right now Stagflation holds a narrow lead at 35% while a Soft Landing closes the gap at 27%.

The regime

Four scenarios are always in play, and today Stagflation leads at 35% — but only just, with a Soft Landing right behind at 27%. A Reacceleration is 21% and a Deflationary Bust 17%. What's changed is the reason. June inflation came in soft — core prices were flat on the month and rent is cooling — real disinflation. So the sticky-inflation risk has rotated: it now comes from an energy supply shock, with the Strait of Hormuz declared closed and oil up 15%. We did not flip to a soft landing on one soft print, because the tape still backs higher-for-longer: the two-year yield sits above the funds rate.

Stagflation 35% · Soft Landing 27% · Reacceleration 21% · Deflationary Bust 17%

Where the money's moving

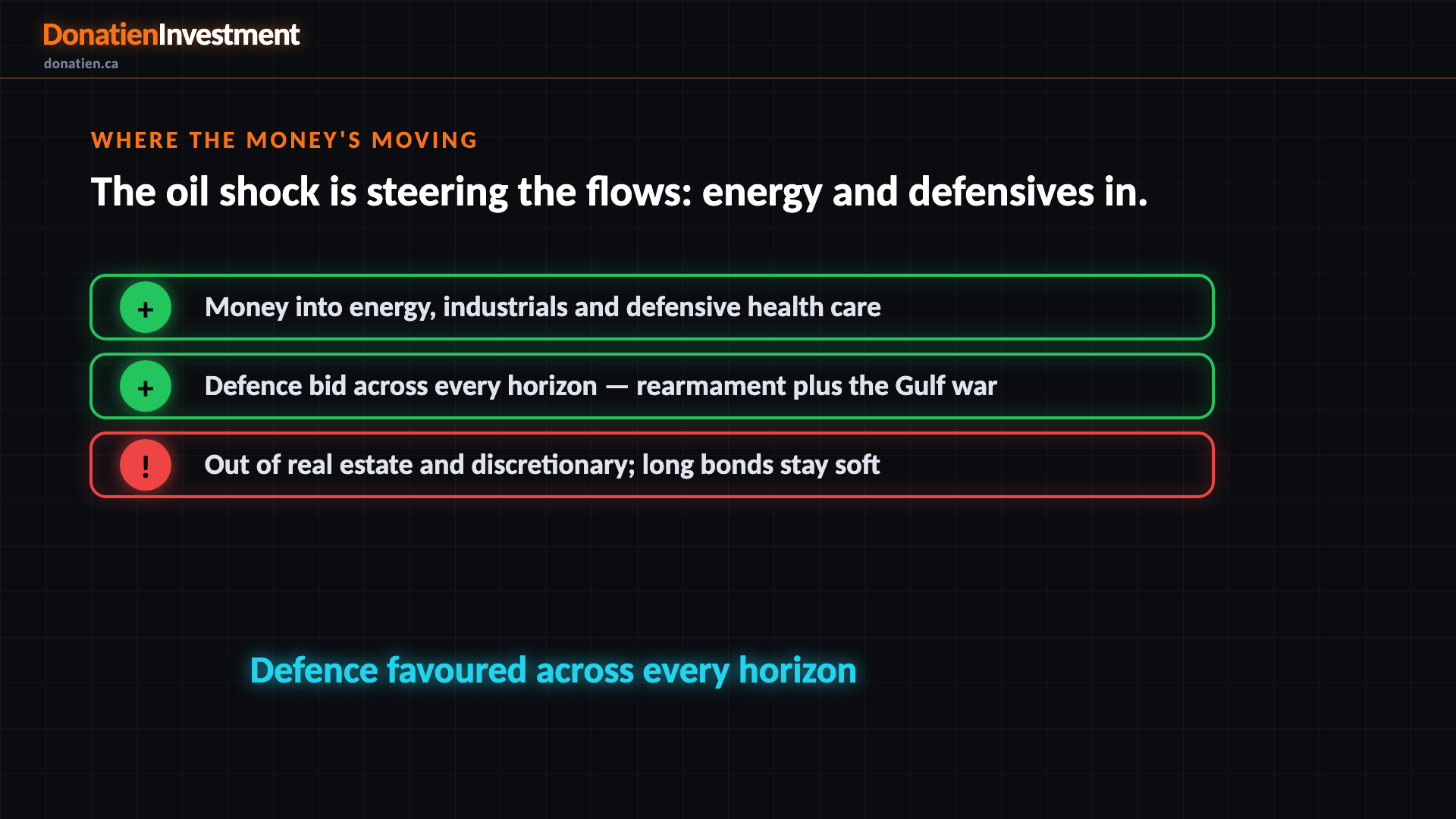

Capital is following the shock. The clearest inflow is into energy, the direct beneficiary of the oil spike, alongside industrials and defensive sectors like health care and staples. Defence is bid across every horizon, on the rearmament build-out and the live Gulf war. Money is leaving real estate and consumer discretionary, squeezed by a ten-year yield back above four-and-a-half percent. Long bonds and high yield stay soft on that higher-for-longer tape.

Energy the cleanest rotation winner on the oil shock · Defence favoured across every horizon

Positioning

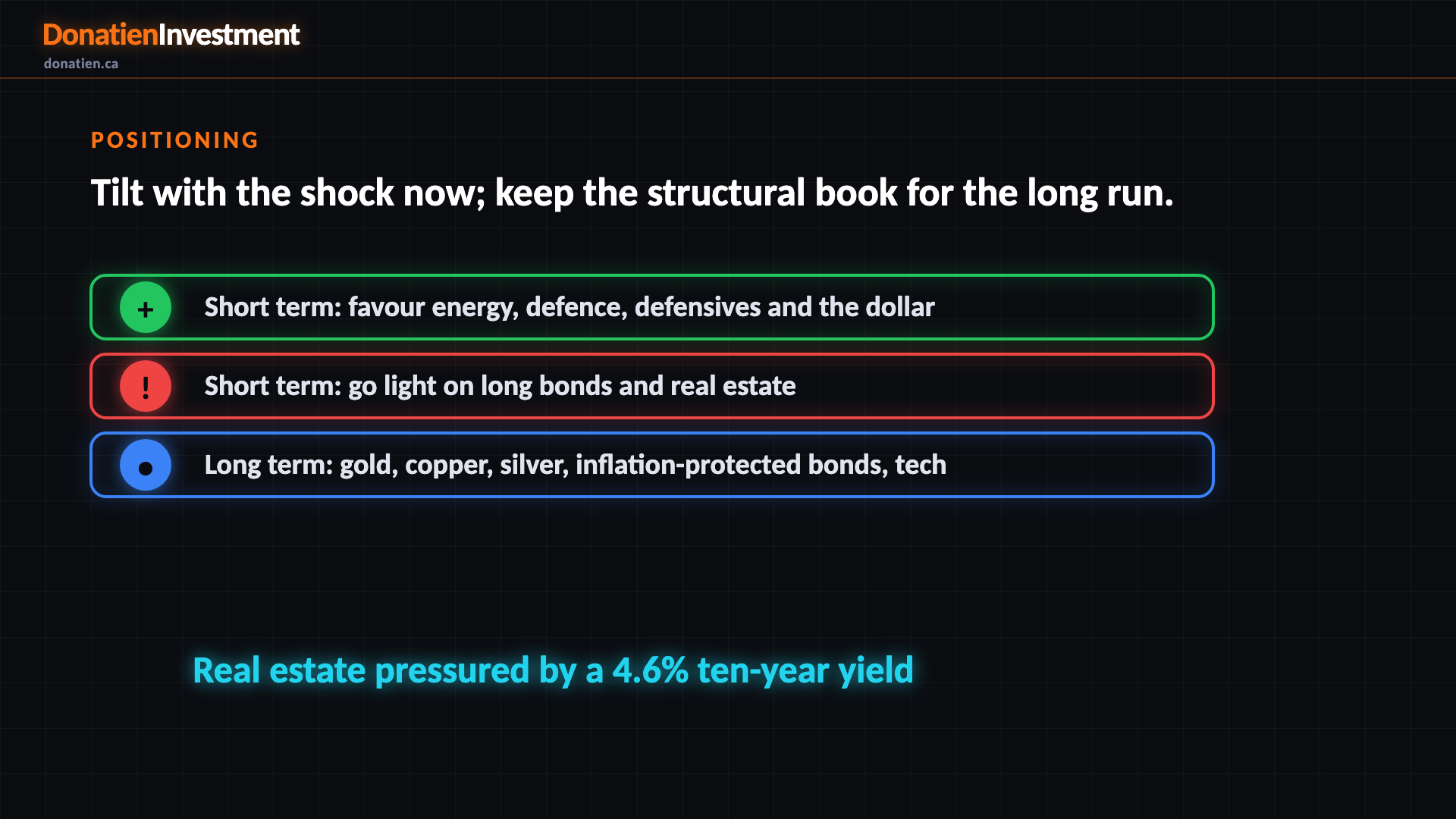

So positioning splits by horizon. Near term, tilt with the energy shock and the firm tape: favour energy, defence, the defensive sectors and the dollar, and go light on long bonds and real estate. Over the long run the structural book is unchanged — gold, copper, silver, inflation-protected bonds and technology all screen well over years, and the dollar screens weak as de-dollarisation grinds on. The soft core reading gives technology a little near-term rate relief.

Dollar: firmer now, weaker over the long run · Real estate pressured by a 4.6% ten-year yield

What could go wrong

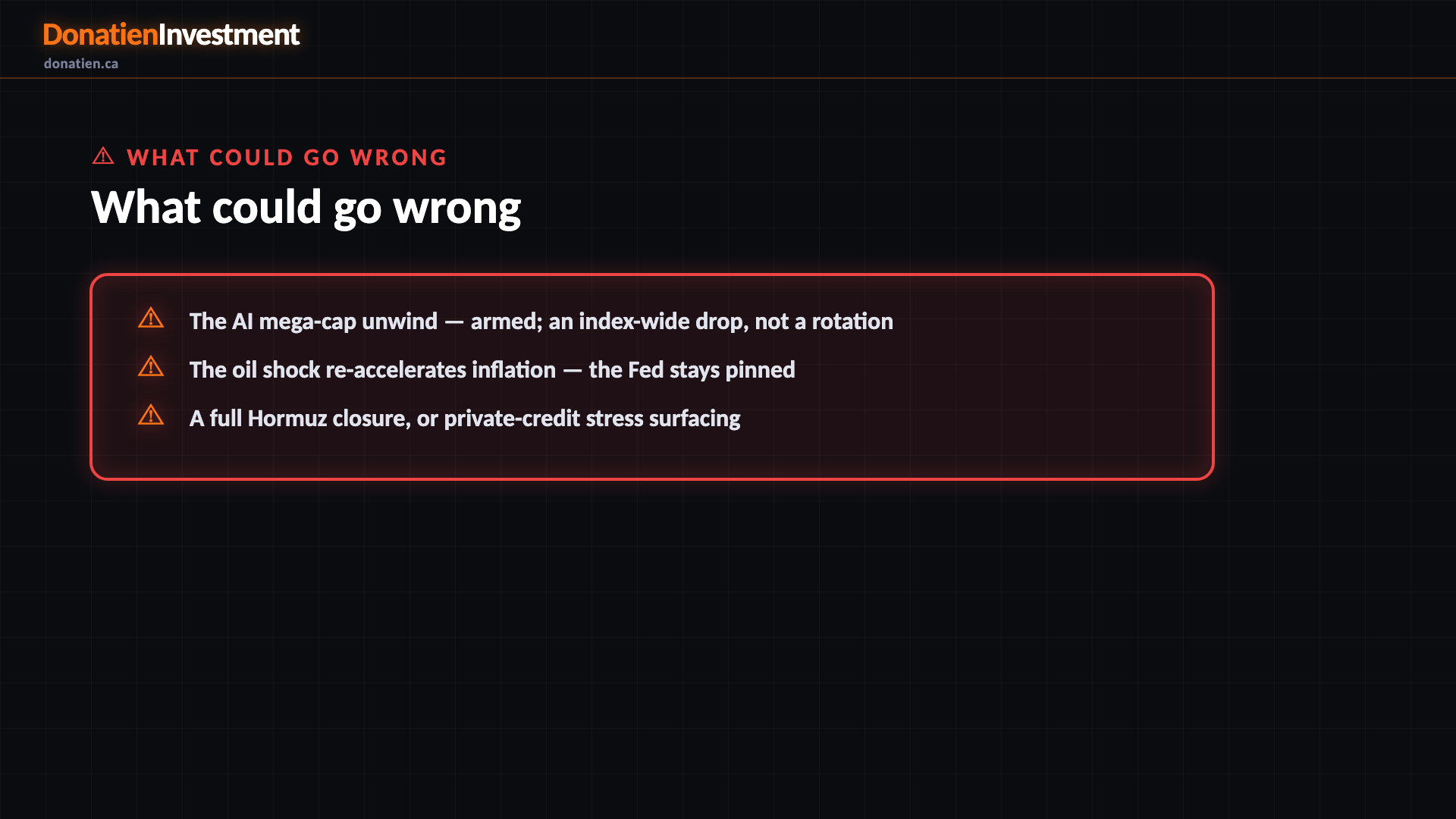

The biggest tail risk is the one that's armed but not triggering. The top of the market is a handful of AI mega-caps — the ten largest names are over forty percent of the index on a price-to-earnings ratio near fifty — so a reversal there is an index-wide drop, not a neat rotation. Beyond that: the very oil shock driving this report could re-accelerate inflation and keep the Fed pinned; a full closure of the Strait of Hormuz would spike oil and hit growth together; and the two-trillion-dollar private-credit market remains an untested fault line as rates stay high.

Risk vs Reward

The four scenarios sit closer than the lead suggests. Stagflation is 35%, a Soft Landing 27%, a Reacceleration 21% and a Deflationary Bust 17%. It is a narrow lead, not a verdict — a genuinely contested picture. The soft June inflation print pulled the Soft Landing up five points; the Iran energy shock is what keeps Stagflation in front rather than letting disinflation take over.

The verdict

Stagflation holds a narrow lead, with a Soft Landing closing — one wants inflation hedges, the other wants you leaning into risk — so cover both rather than lean hard on one. Near term, respect the tape and the energy shock: the dollar is firm, energy and defence are bid, and long bonds and real estate are soft. Longer term, hold the structural book — gold, copper, silver, inflation-protected bonds and technology. The next tells are US retail sales on the sixteenth, then the Federal Reserve decision on the twenty-ninth.

Read the full report on donatien.ca →{kind=link}

{kind=link}