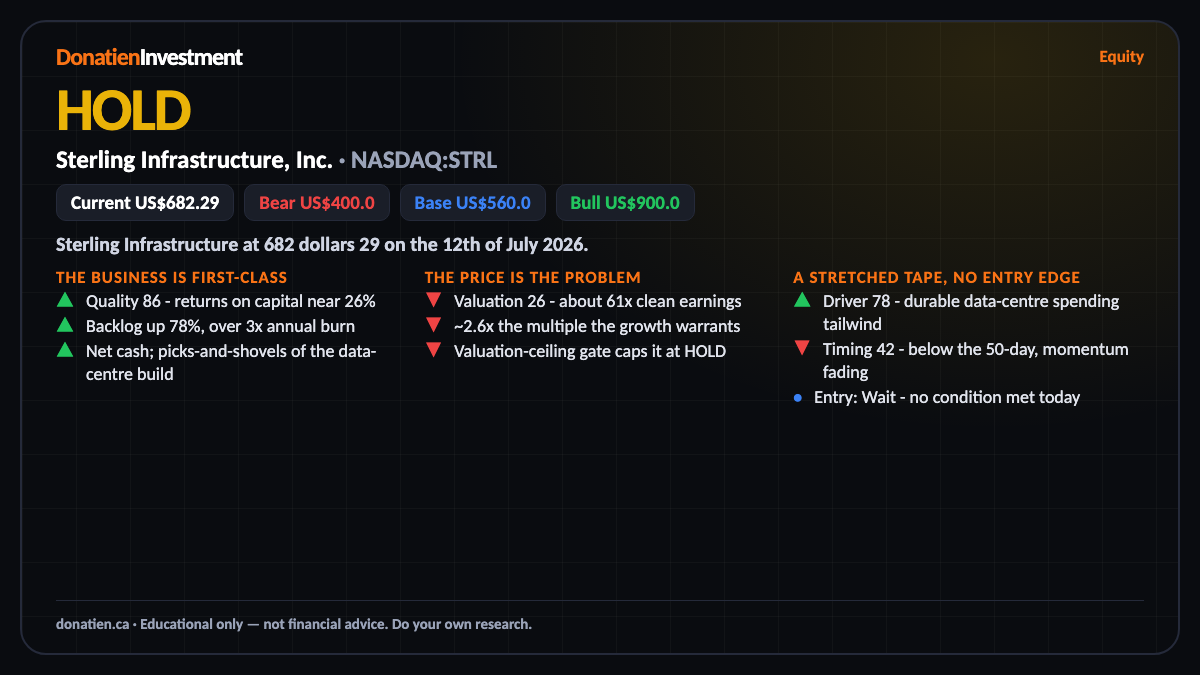

Sterling Infrastructure, Inc. (NASDAQ:STRL) HOLD

An elite infrastructure contractor riding the data-centre build - but after a round trip to a thousand dollars and back it still trades near sixty-one times earnings, well above what the growth warrants. A hold; wait for a real pullback.

Sterling Infrastructure at 682 dollars 29 on the 12th of July 2026. A top-tier American contractor doing the site and e-infrastructure work behind data centres, with returns on capital around twenty-six per cent, a backlog up seventy-eight per cent, and net cash. The business is excellent; the price is the problem. The shares have been as high as a thousand and six and as low as two hundred and thirty in the past year, and even here they price in years of flawless execution.

The business is first-class

Quality scores eighty-six. Sterling earns returns on capital near twenty-six per cent, carries net cash, and sits on a backlog up seventy-eight per cent year on year - more than three times its annual burn. Its e-infrastructure arm does the ground and site work behind data centres, so it is a genuine picks-and-shovels winner of the computing build-out. On the business alone this is one of the higher-quality names we have looked at. The reservation is not the company; it is what you pay to own it today.

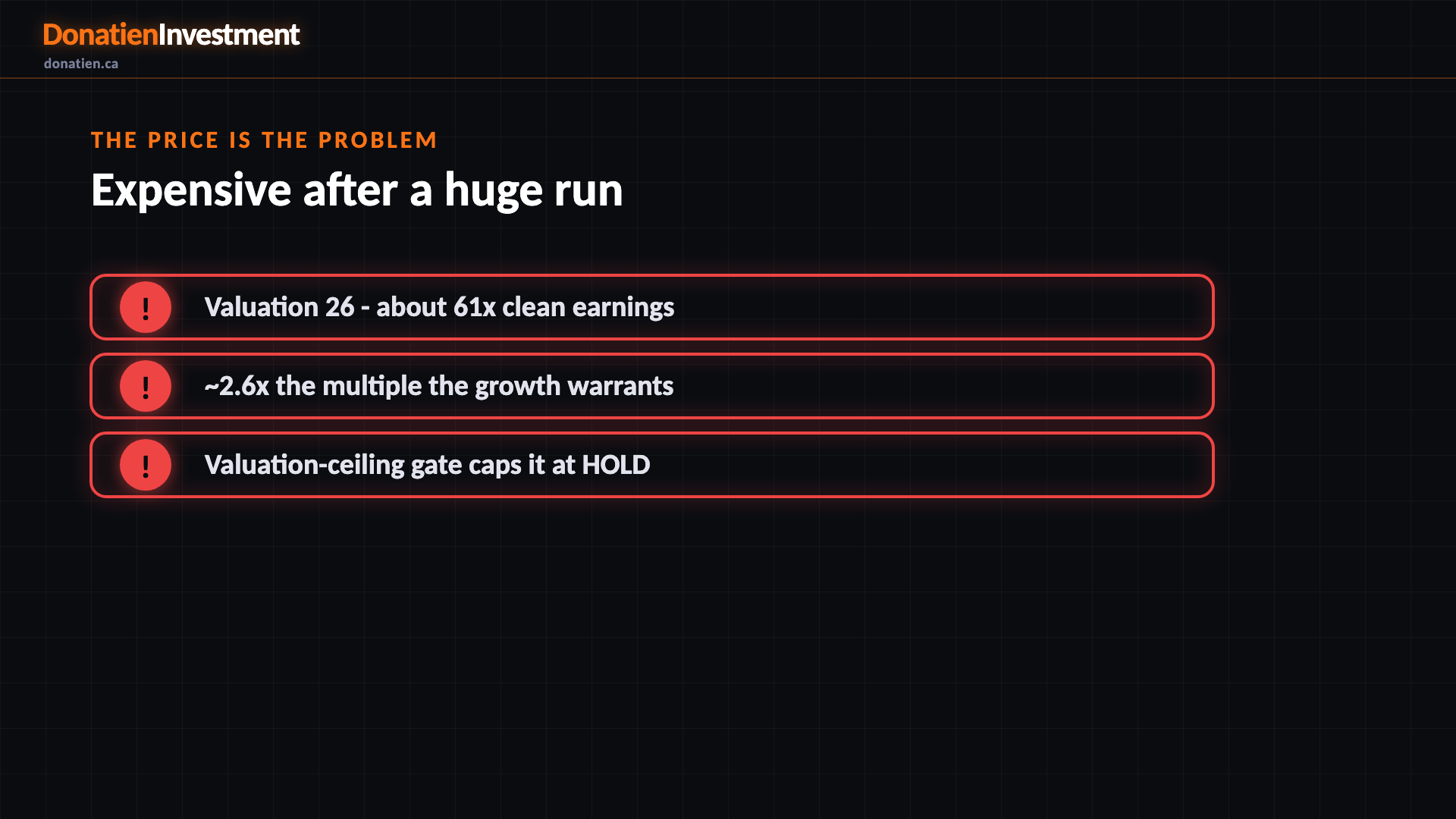

The price is the problem

Valuation scores twenty-six. On clean earnings the shares trade near sixty-one times, about two-and-a-half times the multiple its rate-and-growth backdrop actually warrants, and above the average analyst target. That trips our valuation-ceiling gate, which caps the signal at hold no matter how strong the business. The point is not that Sterling is a bad company - it plainly is not - but that the price already banks years of perfect delivery. Our base case sits around five hundred and sixty dollars, below today's price, which tells you the market has run ahead of the fundamentals.

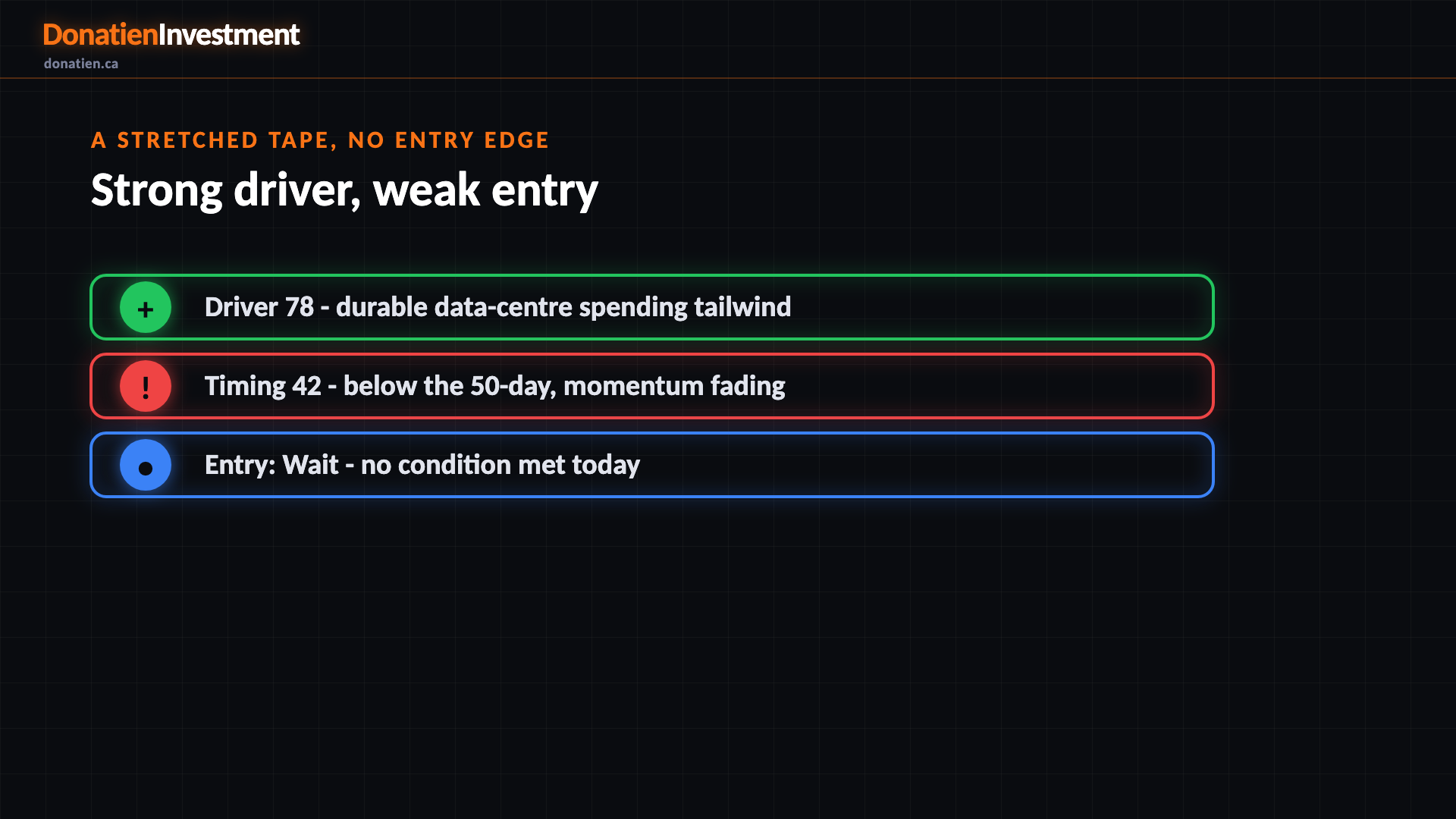

A stretched tape, no entry edge

The underlying driver scores seventy-eight - the data-centre and infrastructure spending cycle is a real, durable tailwind, and the wider economy favours industrials over the long run. But timing is weak at forty-two. The shares are below their fifty-day average with momentum rolling over after a thirty-per-cent drop from the peak, and none of our entry conditions is met. So this is a name to keep on the watchlist and buy on a genuine pullback into the low six hundreds or below, not to chase here.

What could go wrong

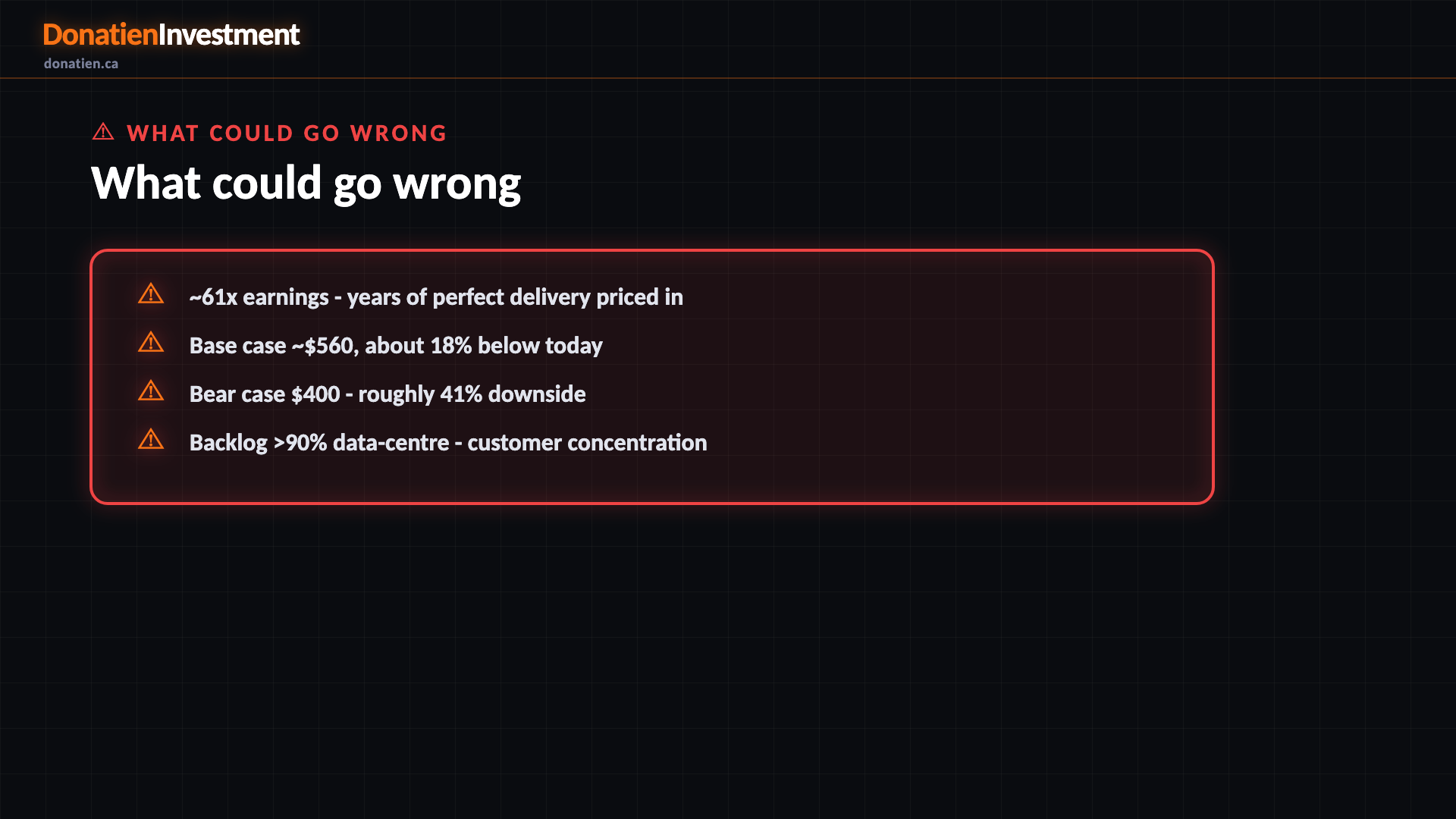

~61x earnings - years of perfect delivery priced in. Base case ~$560, about 18% below today. Bear case $400 - roughly 41% downside. Backlog >90% data-centre - customer concentration. High beta - swings harder than the broad market.

Risk vs Reward

Against the current US$682.29, the report frames a bull case at US$900.0 (+32%), a base case at US$560.0 (-18%) and a bear case at US$400.0 (-41%). See the full report for the probability weight behind each path.

The verdict

An elite infrastructure contractor riding the data-centre build - but after a round trip to a thousand dollars and back it still trades near sixty-one times earnings, well above what the growth warrants. A hold; wait for a real pullback.

Read the full report on donatien.ca →{kind=link}

{kind=link}