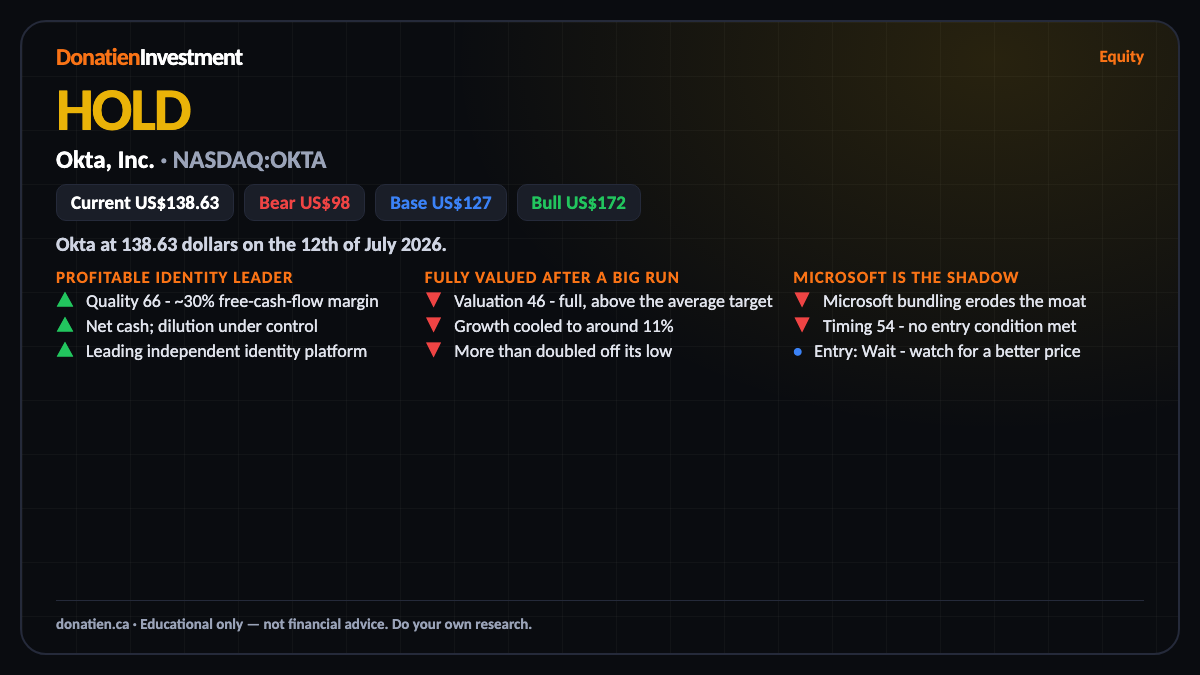

Okta, Inc. (NASDAQ:OKTA) HOLD

A profitable, cash-generative identity leader at a discount to its security peers - but fully valued after a big run, with Microsoft bundling chipping at its moat. A hold, not a chase.

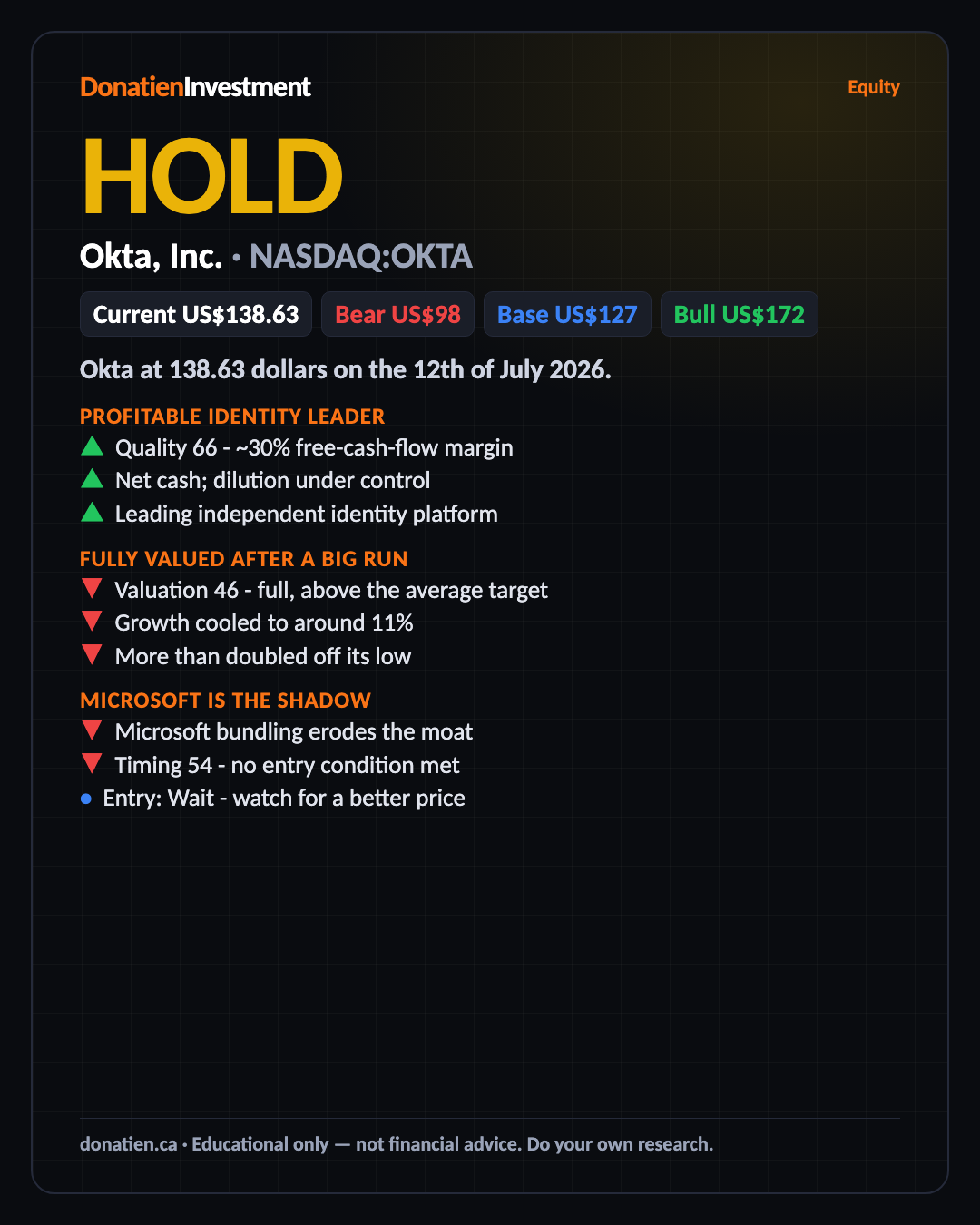

Okta at 138.63 dollars on the 12th of July 2026. Okta is the leading independent identity platform - the login and access layer that lets employees and customers sign in securely. It is profitable, generates strong free cash flow, and carries net cash. But growth has cooled, the shares have more than doubled off their low, and Microsoft's bundled identity product is a real competitive shadow.

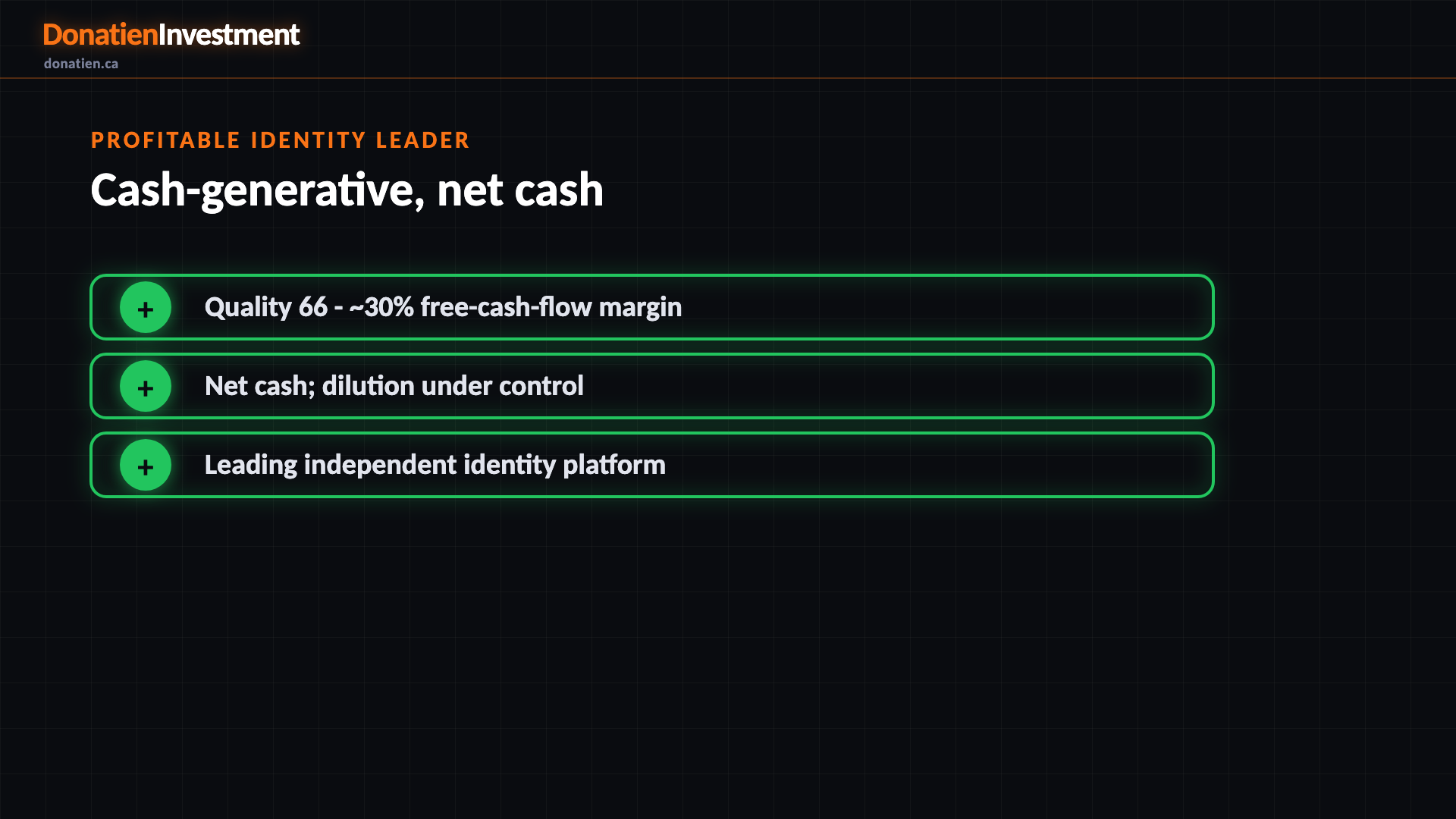

Profitable identity leader

Quality scores sixty-six. Okta runs the identity layer for thousands of organisations, converts around thirty per cent of revenue into free cash flow, and carries net cash. Its share-based pay, a common worry for software names, sits under twenty per cent of revenue and is falling - low enough that it does not trip our dilution gate. This is a solid, profitable business. The question is not quality; it is price and competition.

Fully valued after a big run

Valuation scores forty-six - fairly valued, not cheap. Okta looks inexpensive against other security names, but on its own cash flows it sits in our full band after more than doubling off the low, and it trades above the average analyst target. So the reward for buying today is limited: you are paying up for a business whose growth has slowed to around eleven per cent. That is a hold - a fine company, but the entry price does not offer much of an edge.

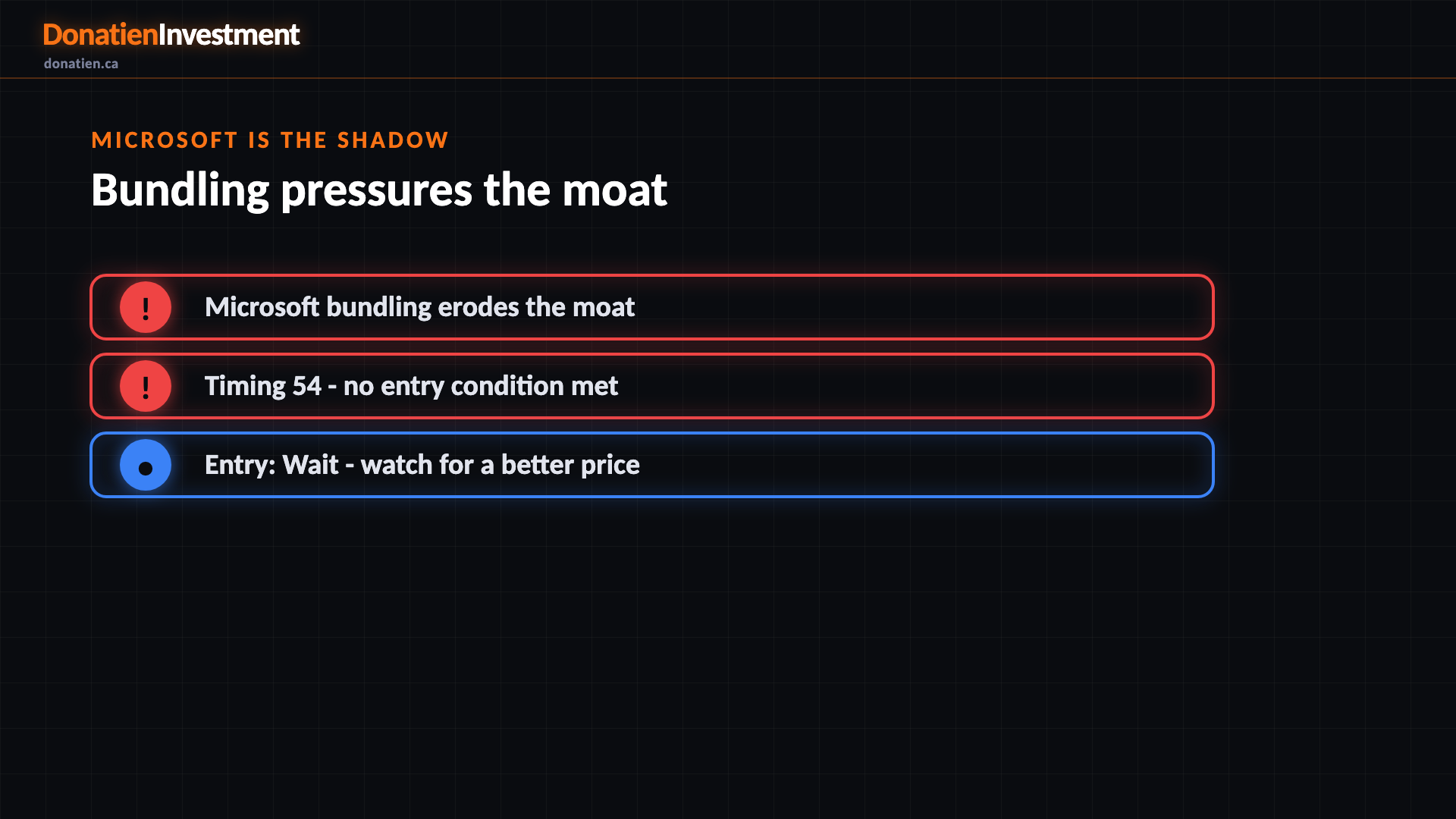

Microsoft is the shadow

The main competitive risk is Microsoft, which bundles its own identity product into deals customers are often already paying for. That pressures Okta's pricing and its switching-cost advantage over time, and it is why we see the moat as slowly eroding rather than widening. There is genuine upside optionality in newer, agent and machine-identity products. But with the tape stretched and no entry condition met, the balance is a hold - watch, and look for a better price.

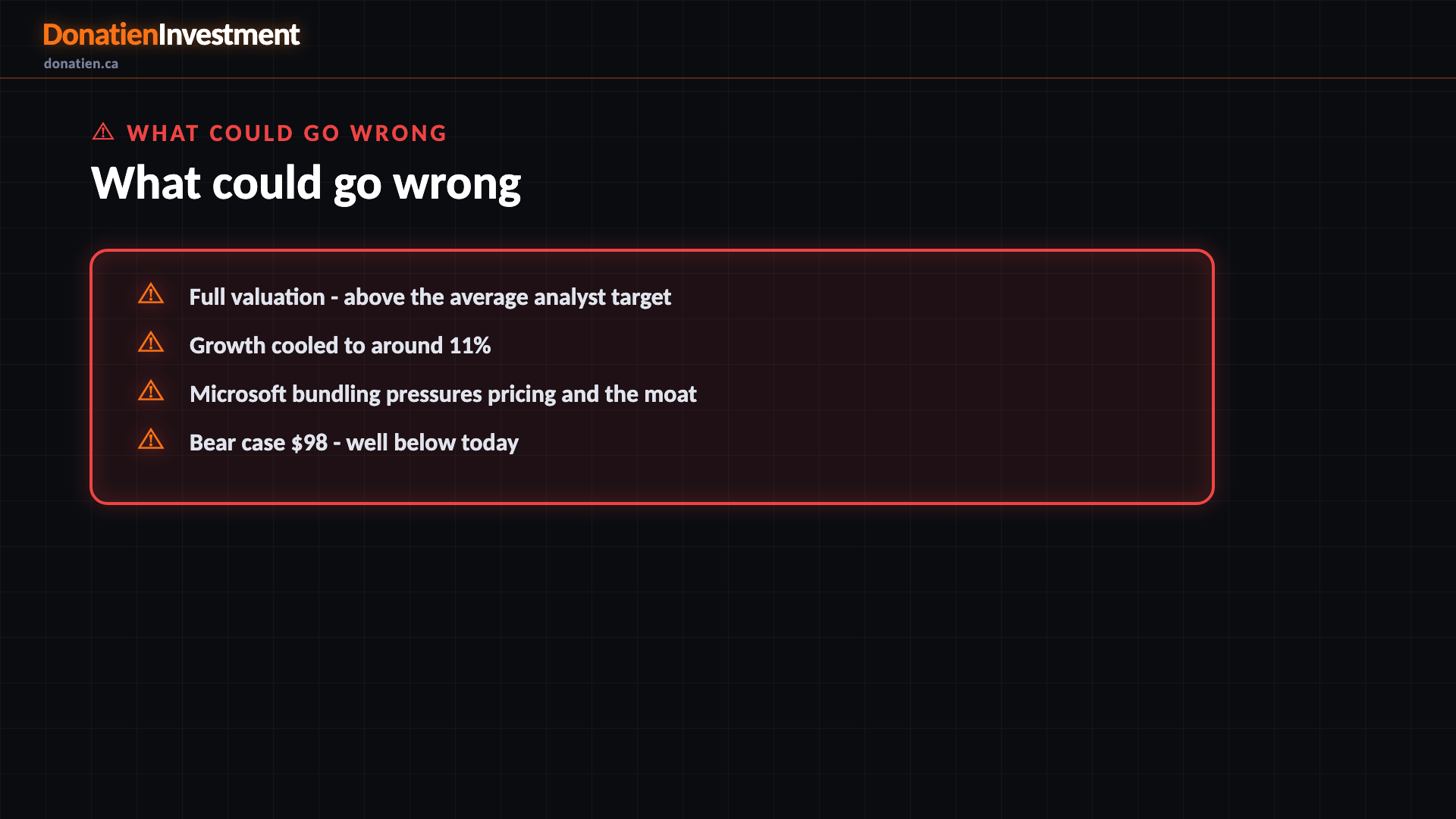

What could go wrong

Full valuation - above the average analyst target. Growth cooled to around 11%. Microsoft bundling pressures pricing and the moat. Bear case $98 - well below today. More than doubled off its low - stretched tape.

Risk vs Reward

Against the current US$138.63, the report frames a bull case at US$172 (+24%), a base case at US$127 (-8%) and a bear case at US$98 (-29%). See the full report for the probability weight behind each path.

The verdict

A profitable, cash-generative identity leader at a discount to its security peers - but fully valued after a big run, with Microsoft bundling chipping at its moat. A hold, not a chase.

Read the full report on donatien.ca →{kind=link}

{kind=link}