Clarivate Plc (NYSE:CLVT) HOLD

Statistically cheap, but a classic value trap - flat-to-declining growth, heavy debt that barely covers its interest, and AI eating into its core. Cheap is not the same as buy.

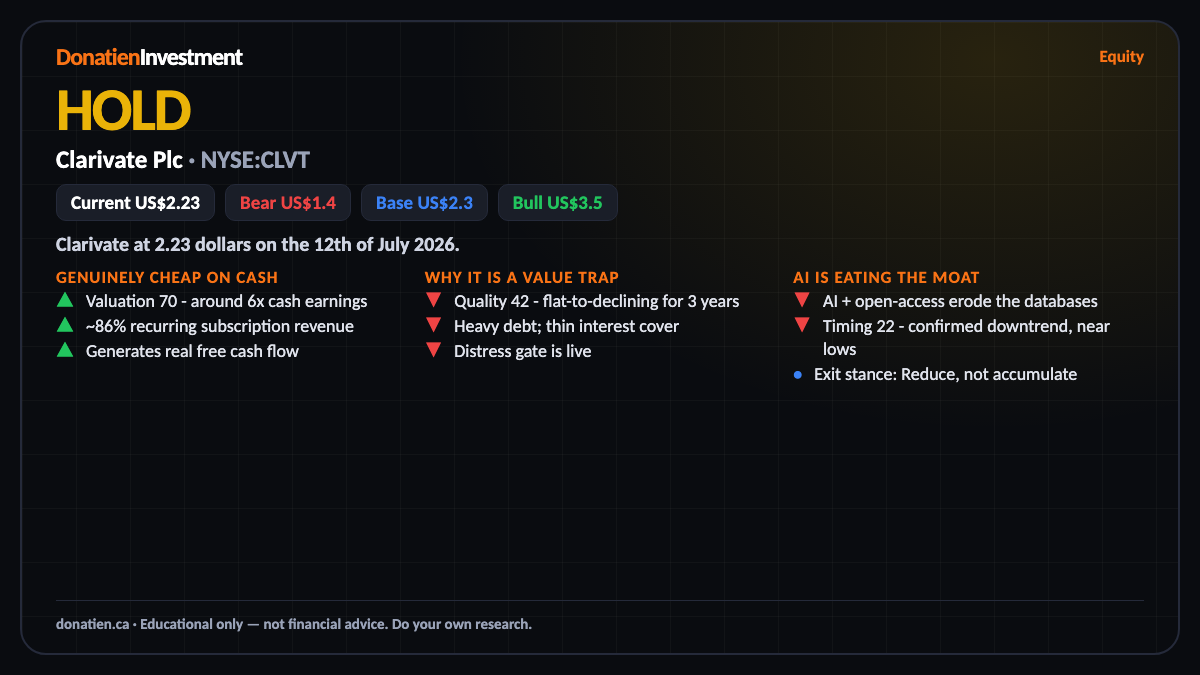

Clarivate at 2.23 dollars on the 12th of July 2026. Clarivate sells subscription data and analytics to researchers, universities and law firms - brands like the Web of Science. It throws off cash and screens statistically cheap. But the top line is flat-to-shrinking, the balance sheet carries heavy debt, and general-purpose AI and open-access are chipping away at the value of its gated databases.

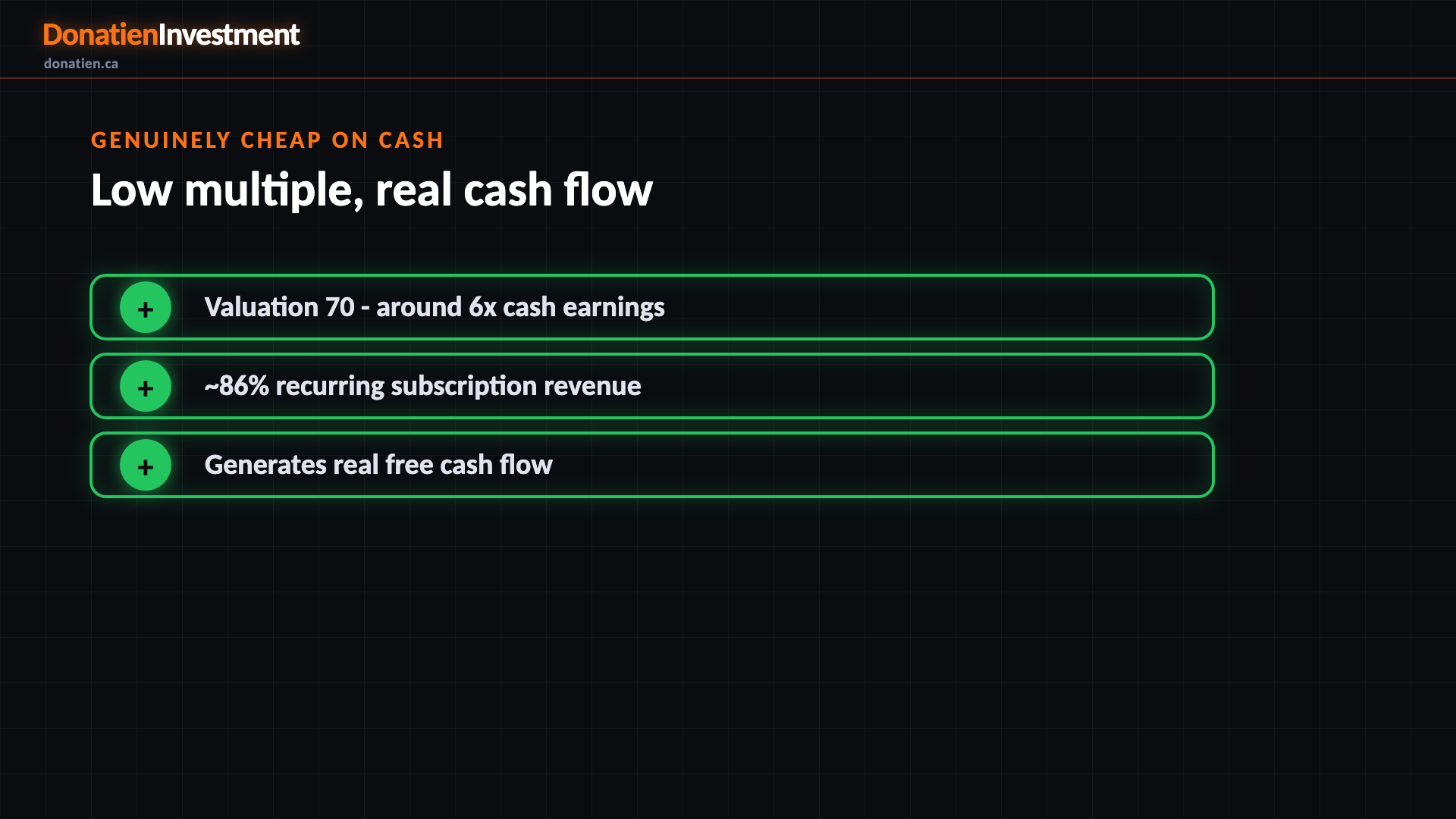

Genuinely cheap on cash

Valuation scores seventy - on the numbers this is a cheap stock. Clarivate trades around six times cash earnings, generates real free cash flow, and about eighty-six per cent of its revenue is recurring subscriptions. If you screen purely for cheapness, it stands out. The whole question with a name like this is whether cheap is an opportunity or a warning - and here the rest of the picture argues it is a warning.

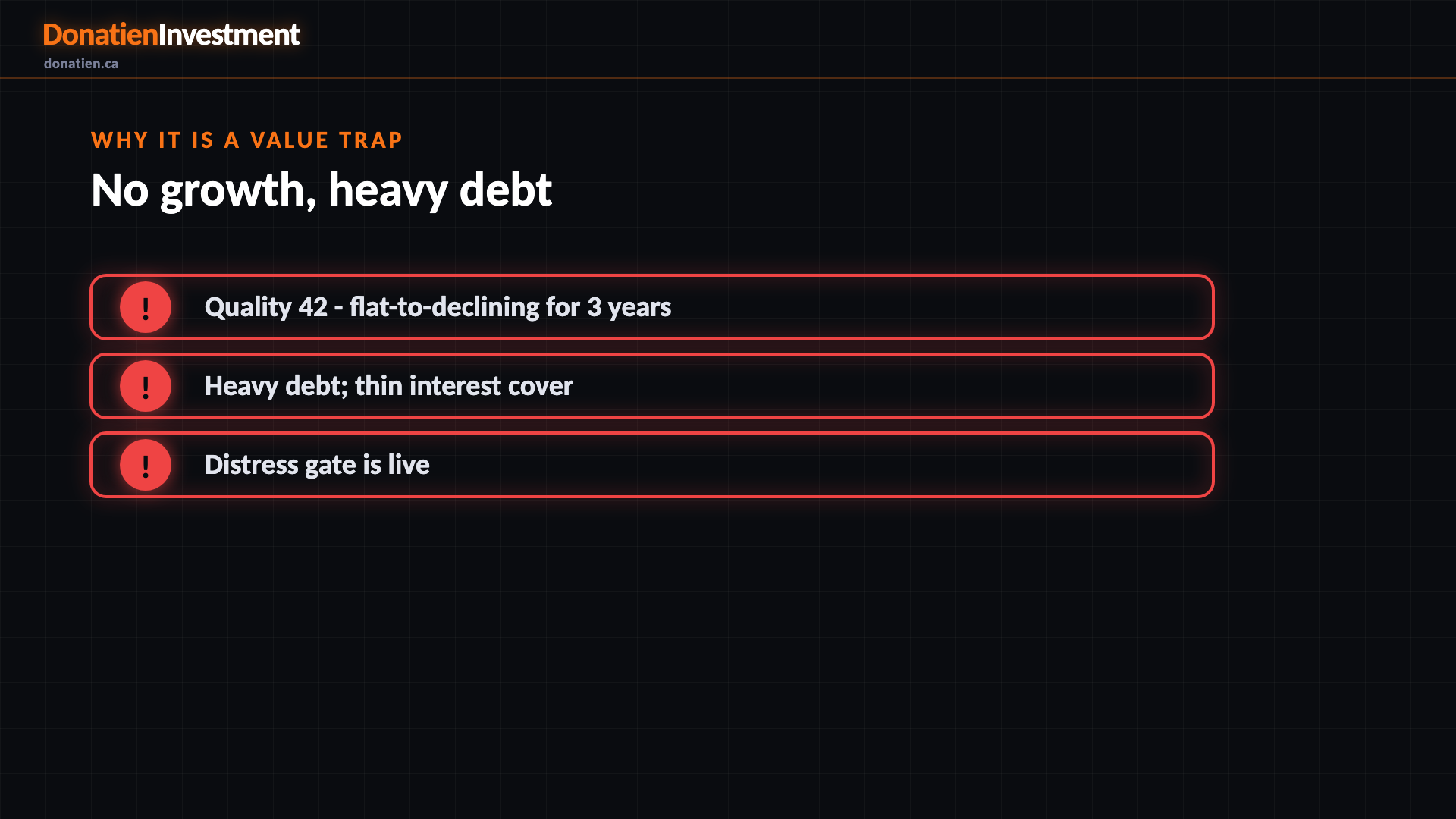

Why it is a value trap

Quality scores forty-two. The reason the stock is cheap is that the business is barely growing - revenue has been flat to declining for three years - while it carries heavy debt. Its operating profit only covers its interest bill about half over, once you count the full charge. A cheap multiple on a shrinking, indebted business is the textbook value trap: the price can stay low, or fall further, for a long time. That is why our financial-distress gate is flashing.

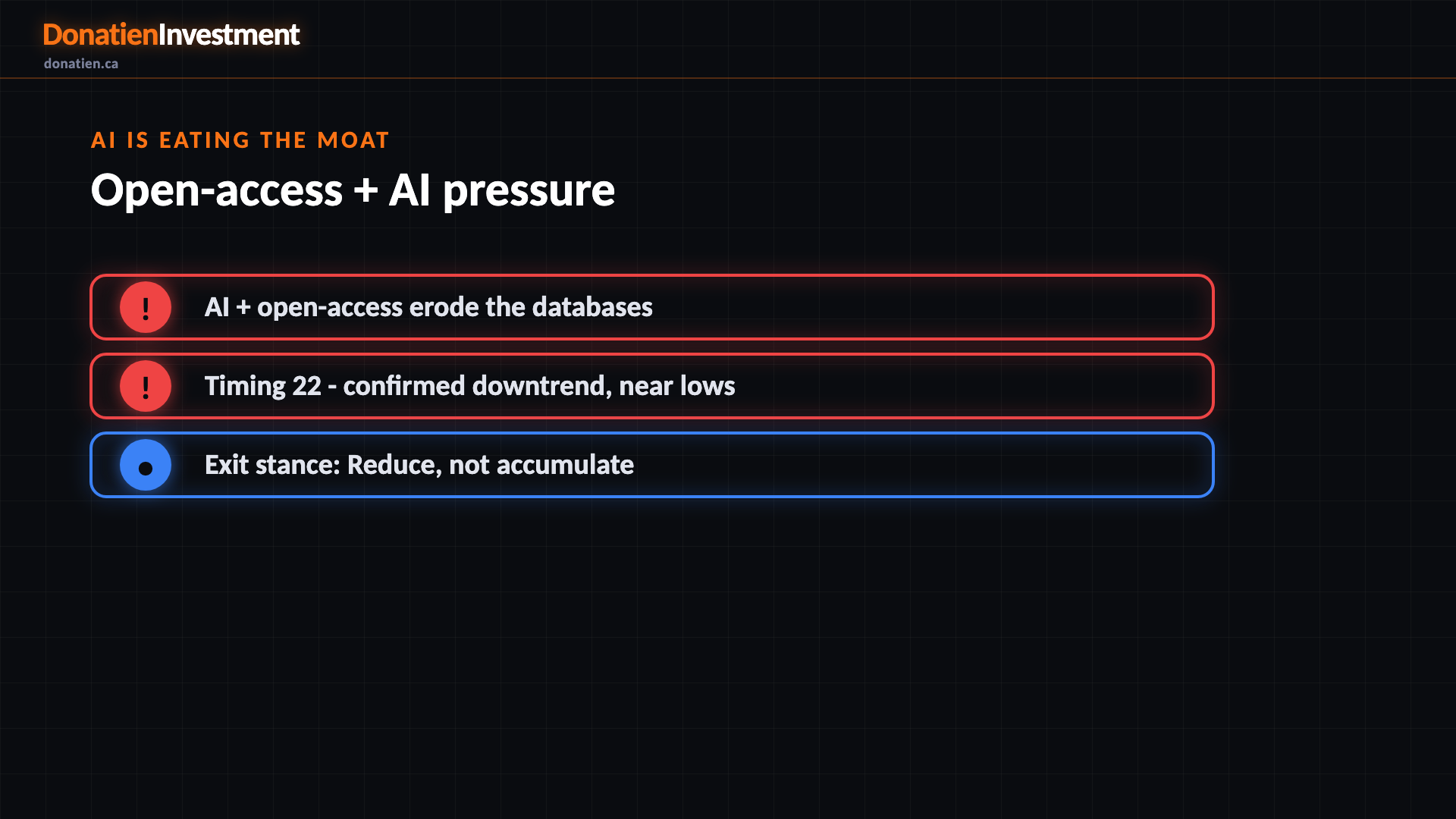

AI is eating the moat

On top of the debt, the long-run threat is structural: free open-access research and general-purpose AI search are chipping away at the value of paying for gated databases. There are real self-help levers - a recent divestiture should cut debt, and the company is repositioning around AI - so this is not a sell into the hole. But it is not a buy either. A hold: too cheap and too self-helping to short, too troubled to own until the turnaround actually shows up in the numbers.

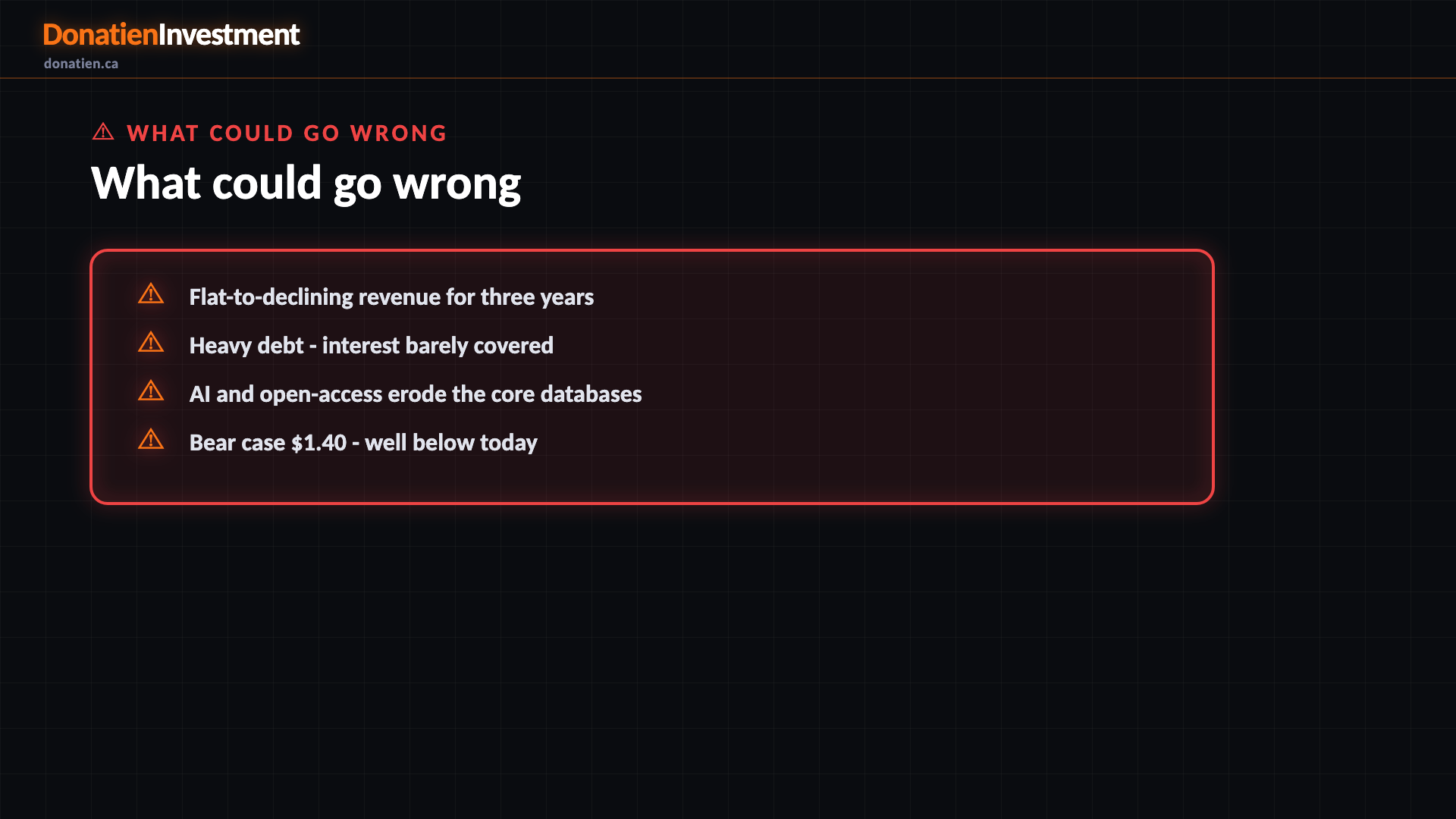

What could go wrong

Flat-to-declining revenue for three years. Heavy debt - interest barely covered. AI and open-access erode the core databases. Bear case $1.40 - well below today. Cheap can stay cheap - the value-trap risk.

Risk vs Reward

Against the current US$2.23, the report frames a bull case at US$3.5 (+57%), a base case at US$2.3 (+3%) and a bear case at US$1.4 (-37%). See the full report for the probability weight behind each path.

The verdict

Statistically cheap, but a classic value trap - flat-to-declining growth, heavy debt that barely covers its interest, and AI eating into its core. Cheap is not the same as buy.

Read the full report on donatien.ca →{kind=link}

{kind=link}