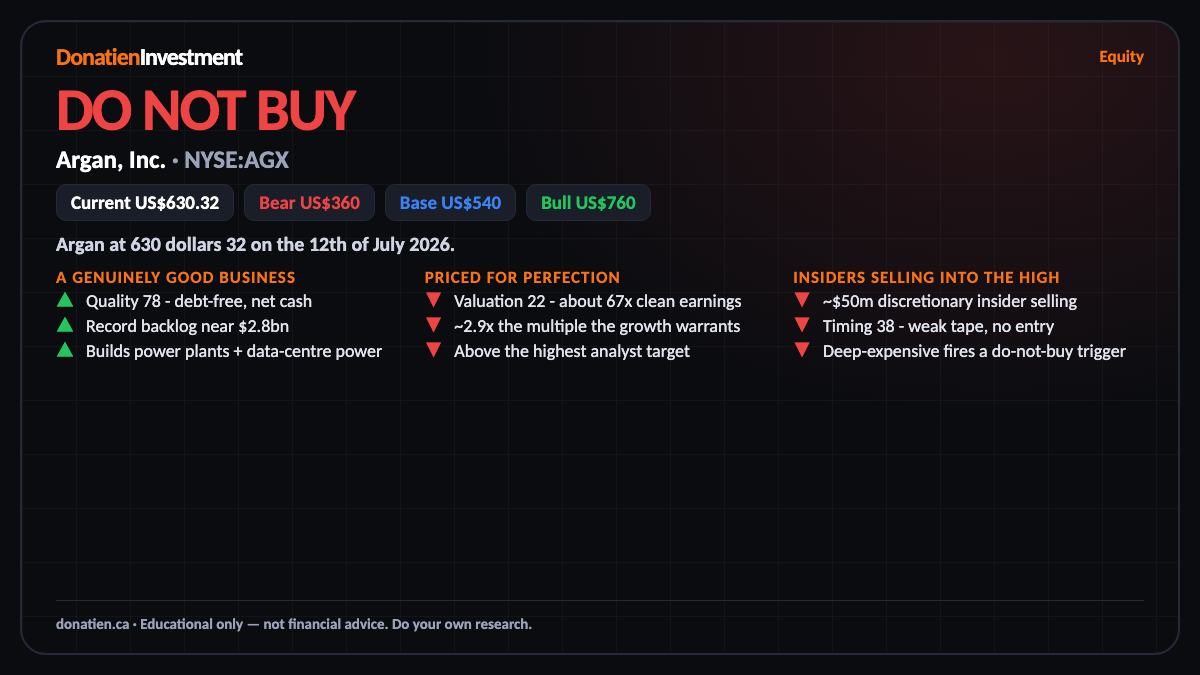

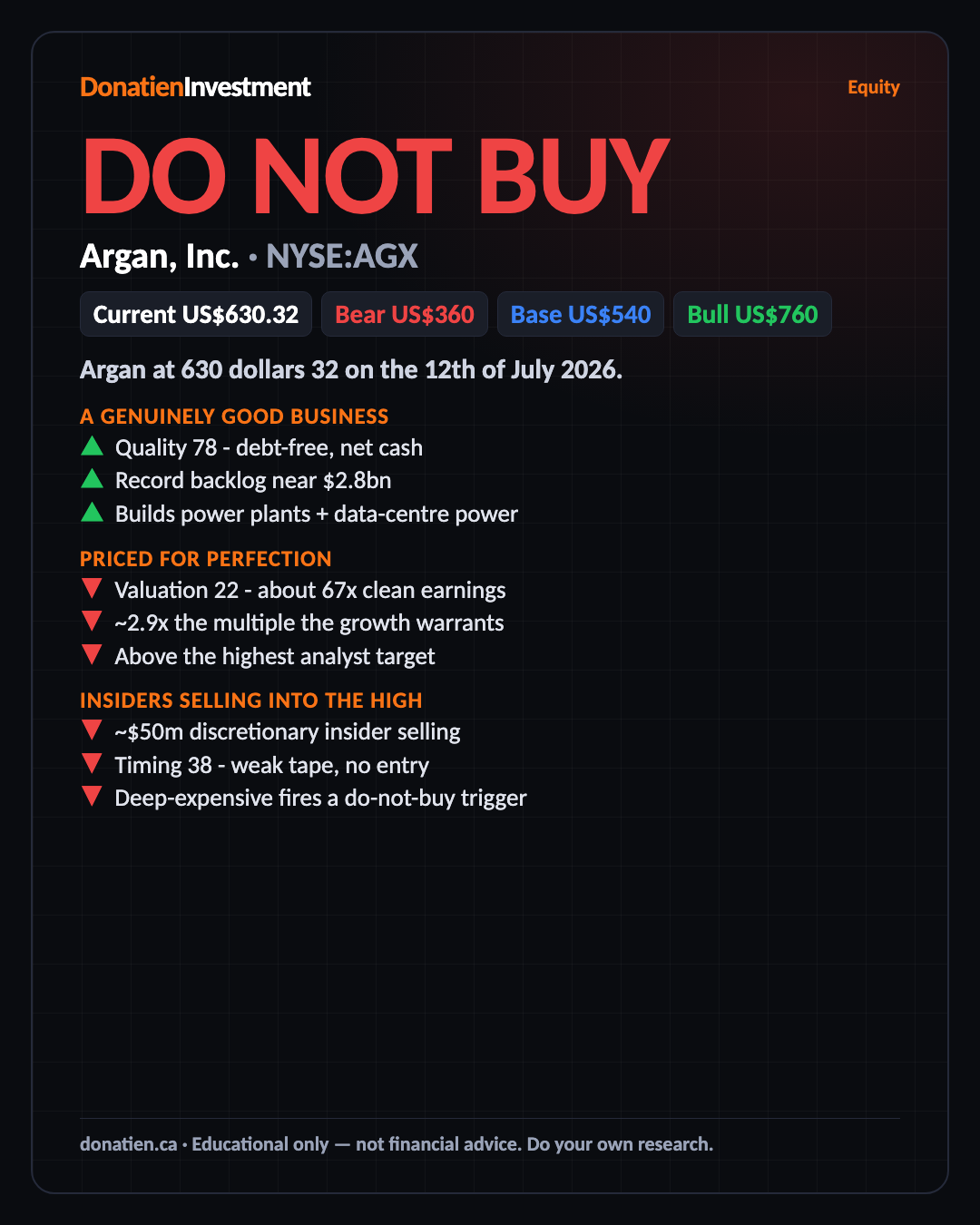

Argan, Inc. (NYSE:AGX) DO NOT BUY

A superb, debt-free builder of power plants and data-centre power - but priced near sixty-seven times clean earnings after a huge run, with insiders selling into the high. A great company at a wrong, risky price.

Argan at 630 dollars 32 on the 12th of July 2026. One of the best-run engineering-and-construction firms in America - it builds gas power plants and the power infrastructure behind data centres, carries no debt and a large cash pile, and sits on a record backlog near two-point-eight billion dollars. The business is genuinely good; the problem is entirely the price you are being asked to pay for it today.

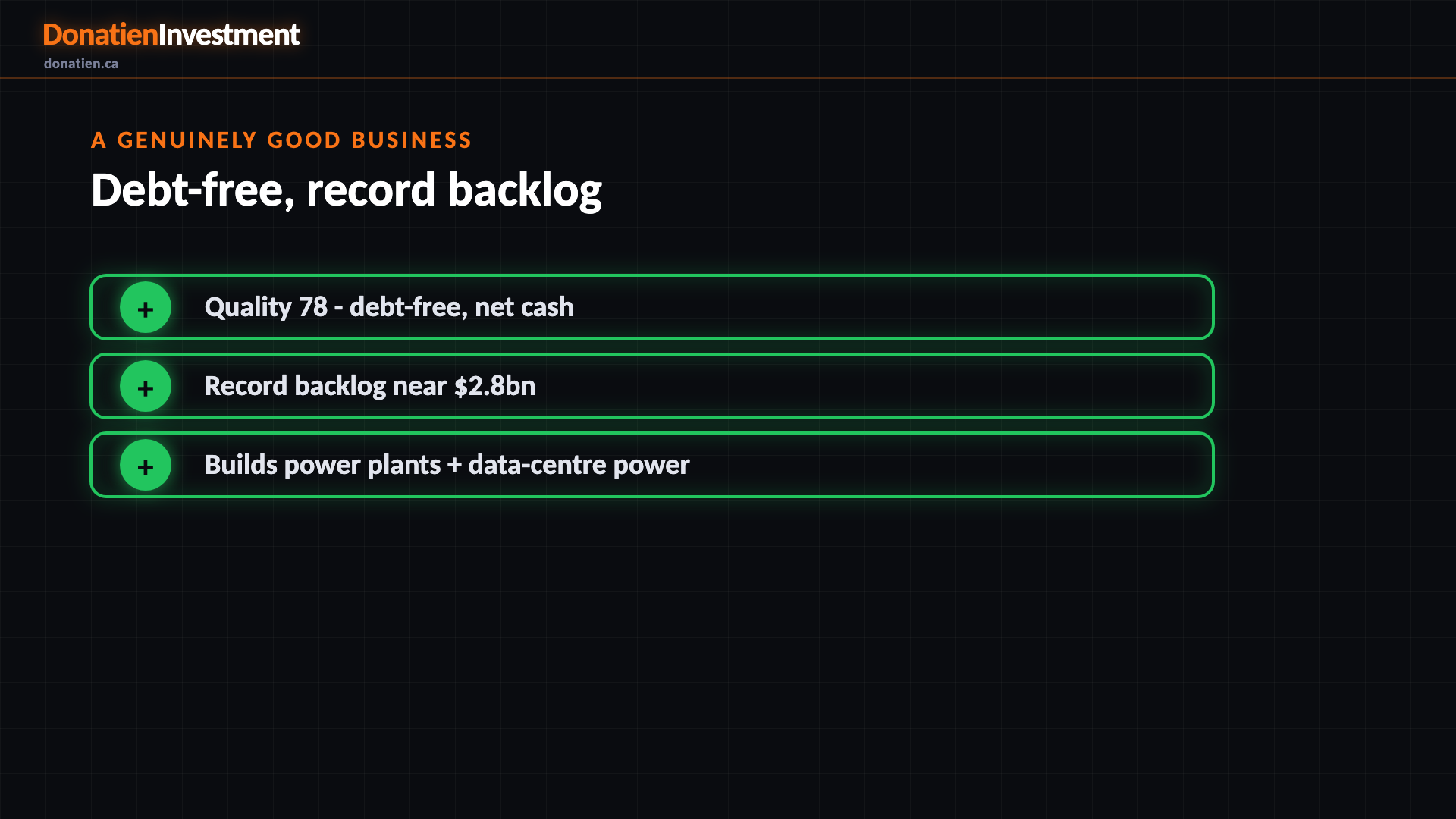

A genuinely good business

Let us be clear up front: this is a quality company. Quality scores seventy-eight. Argan builds gas-fired power plants and the power infrastructure behind data centres, carries net cash and no debt, and holds a record backlog near two-point-eight billion dollars as electricity demand from computing surges. Management has a strong record. Nothing here says the business is broken. Everything that follows is about valuation and risk, not about whether Argan is a good operator - it plainly is.

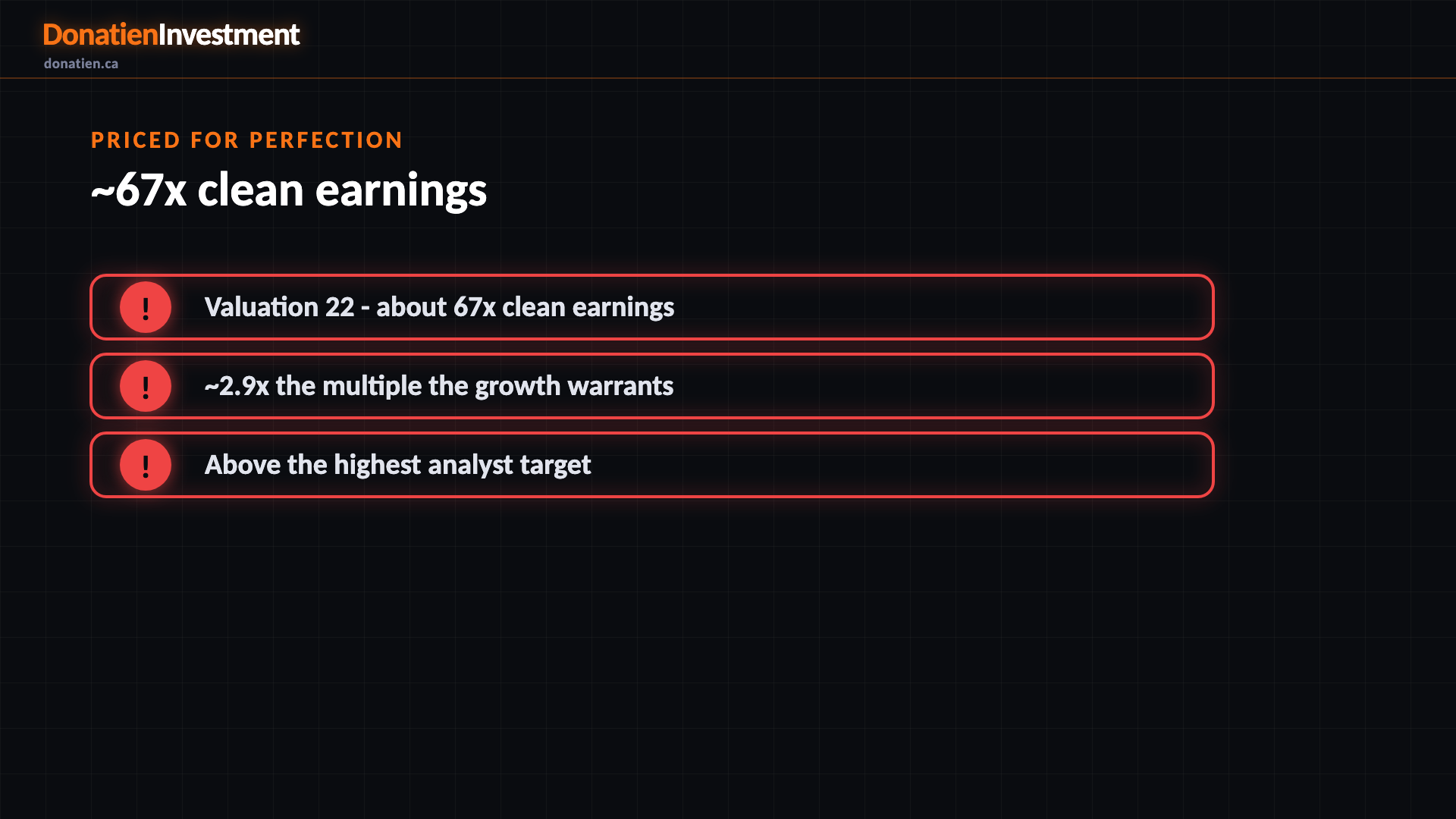

Priced for perfection

Valuation scores twenty-two. After a run from under two hundred to over eight hundred dollars, the shares trade near sixty-seven times clean earnings - almost three times the multiple the growth actually warrants, and above the highest analyst target. That is deep enough into expensive territory to fire our do-not-buy trigger, not just cap the signal. Part of the reported profit is simply interest on the cash pile, which flatters the headline number. If the multiple merely drifts back toward what the growth warrants, that is a forty-per-cent move on its own.

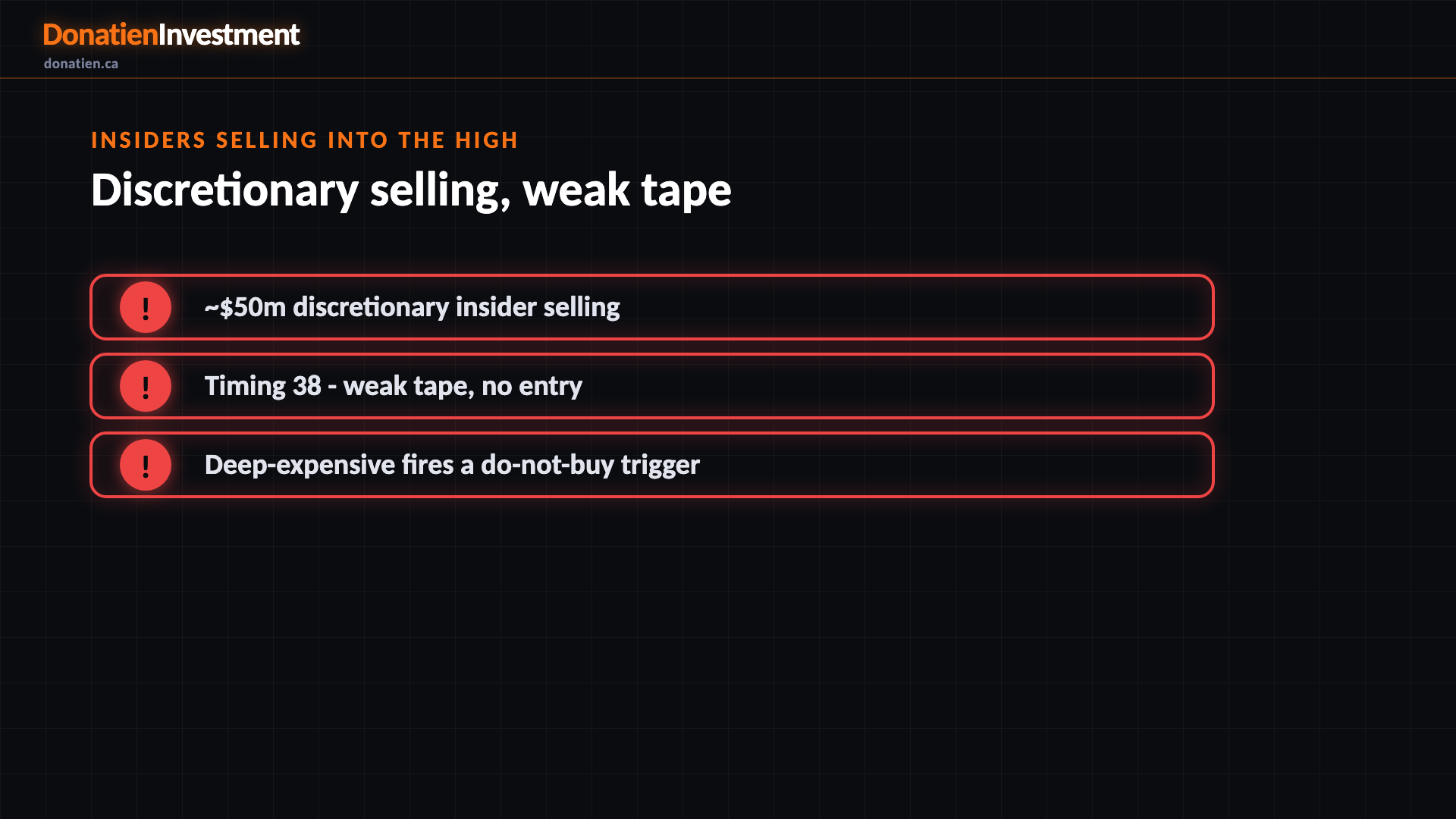

Insiders selling into the high

On top of the valuation, company insiders sold roughly fifty million dollars of stock into the fifty-two-week high, and these were discretionary sales, not pre-arranged plans. That is a corroborating flag, not the main case, but it points the same way as the valuation. Timing is weak at thirty-eight, and none of our entry conditions is met. Add it up and the expected value of buying here is poor: a wonderful business, but the price and the setup both say wait - or look elsewhere.

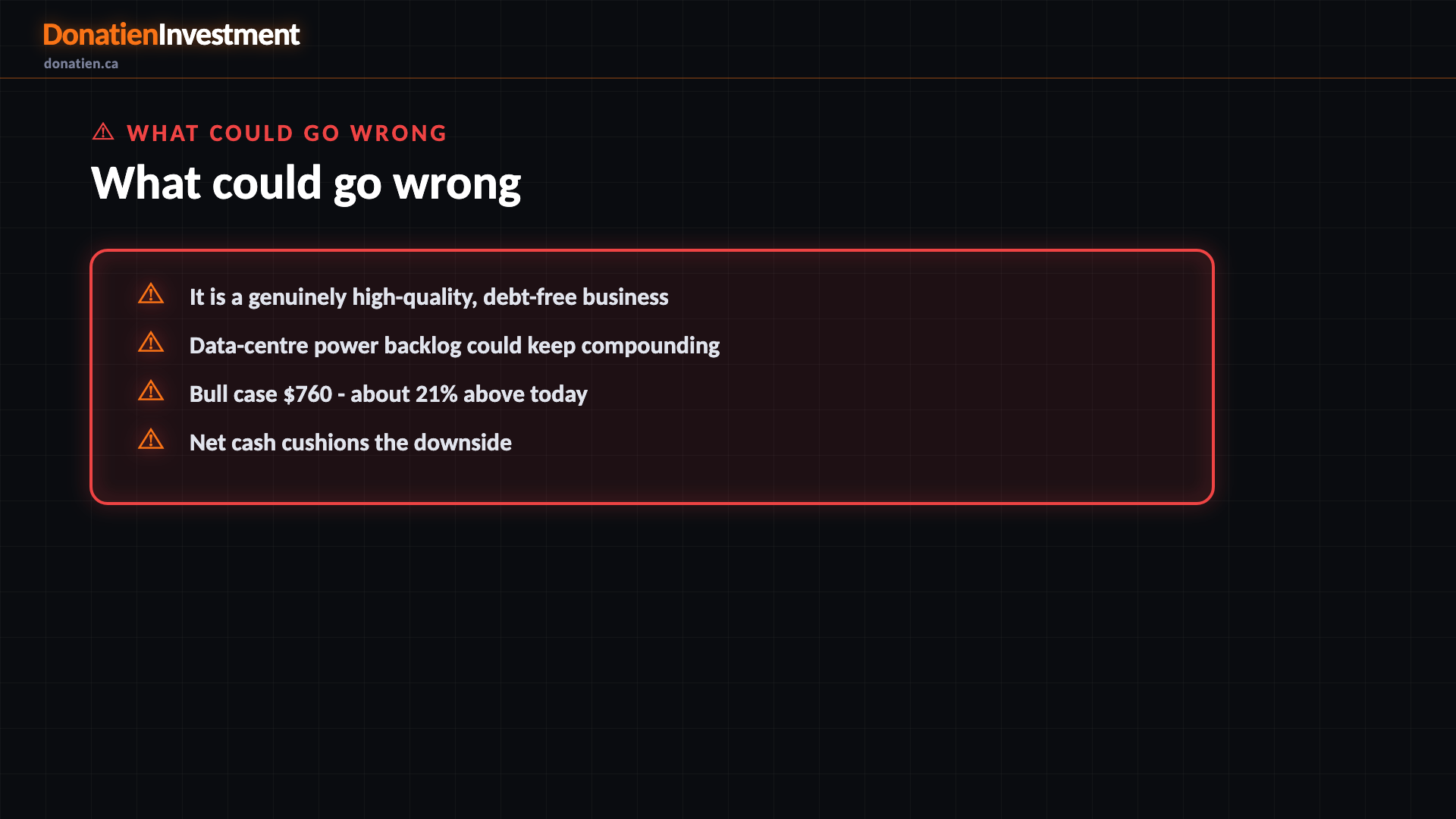

What could go wrong

It is a genuinely high-quality, debt-free business. Data-centre power backlog could keep compounding. Bull case $760 - about 21% above today. Net cash cushions the downside. So this is 'wrong price', not 'bad company'.

Risk vs Reward

Against the current US$630.32, the report frames a bull case at US$760 (+21%), a base case at US$540 (-14%) and a bear case at US$360 (-43%). See the full report for the probability weight behind each path.

The verdict

A superb, debt-free builder of power plants and data-centre power - but priced near sixty-seven times clean earnings after a huge run, with insiders selling into the high. A great company at a wrong, risky price.

Read the full report on donatien.ca →{kind=link}

{kind=link}