The Debt Machine Cornered governments inflate AND grow at once — and that quietly moves wealth to real assets and borrowers

away from cash, wages and bonds; the losers hold money, the winners hold real things — especially with cheap fixed-rate debt

A Donatien Special Report — the debt machine driving the US and Canadian economies, in plain English.

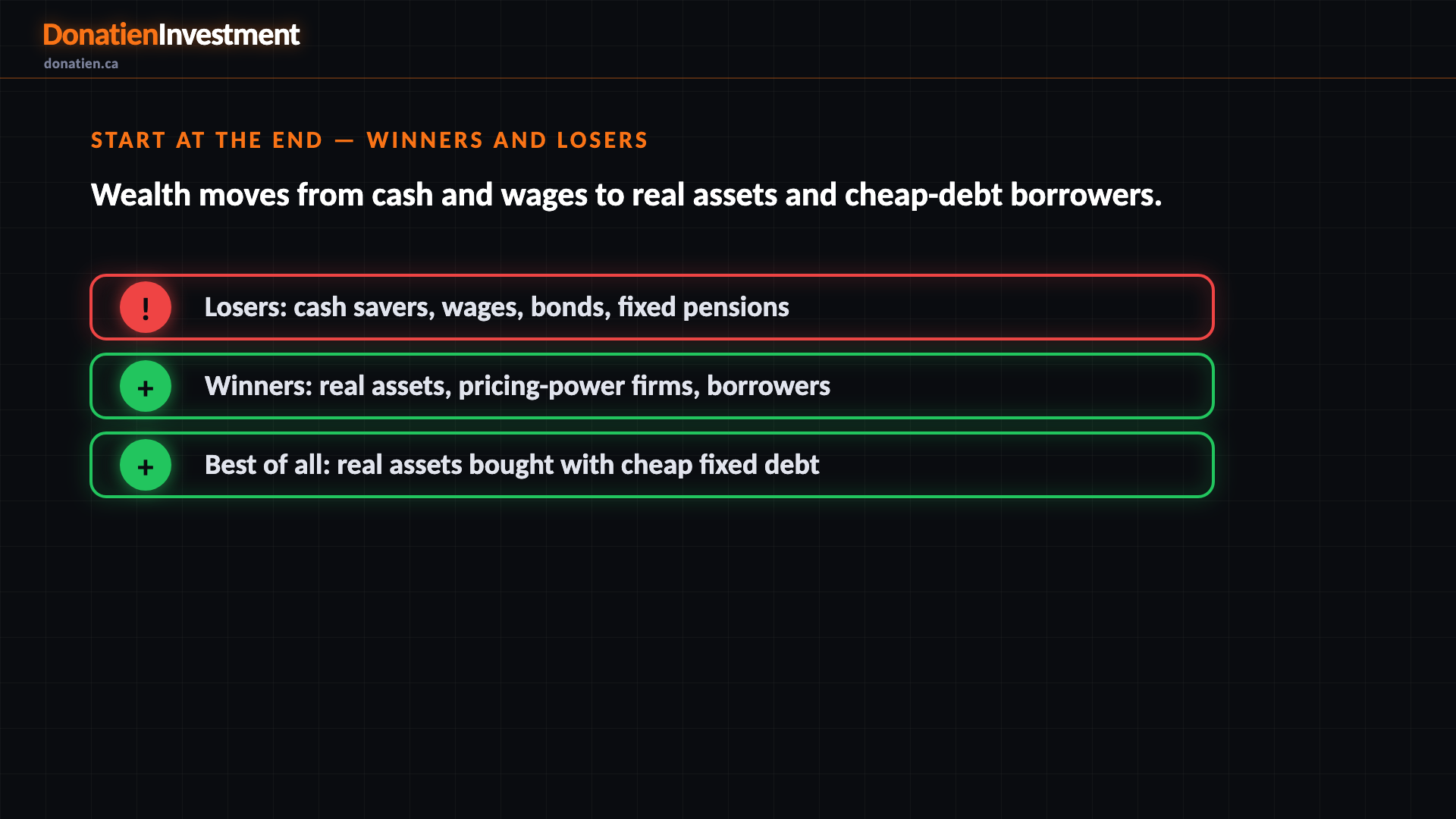

Start at the end — winners and losers

Let's start at the end, with who comes out ahead over the next five to ten years, and who falls behind. On one side, the losers: anyone holding their wealth in cash or a savings account, wage-earners whose pay lags prices, and people on fixed pensions or long-term bonds. On the other, the winners: owners of real assets and property, companies that can raise their prices, and borrowers — above all, people who own real things bought with cheap, fixed-rate debt. It looks arbitrary. It isn't. It falls straight out of a trap that every heavily indebted government is now caught in.

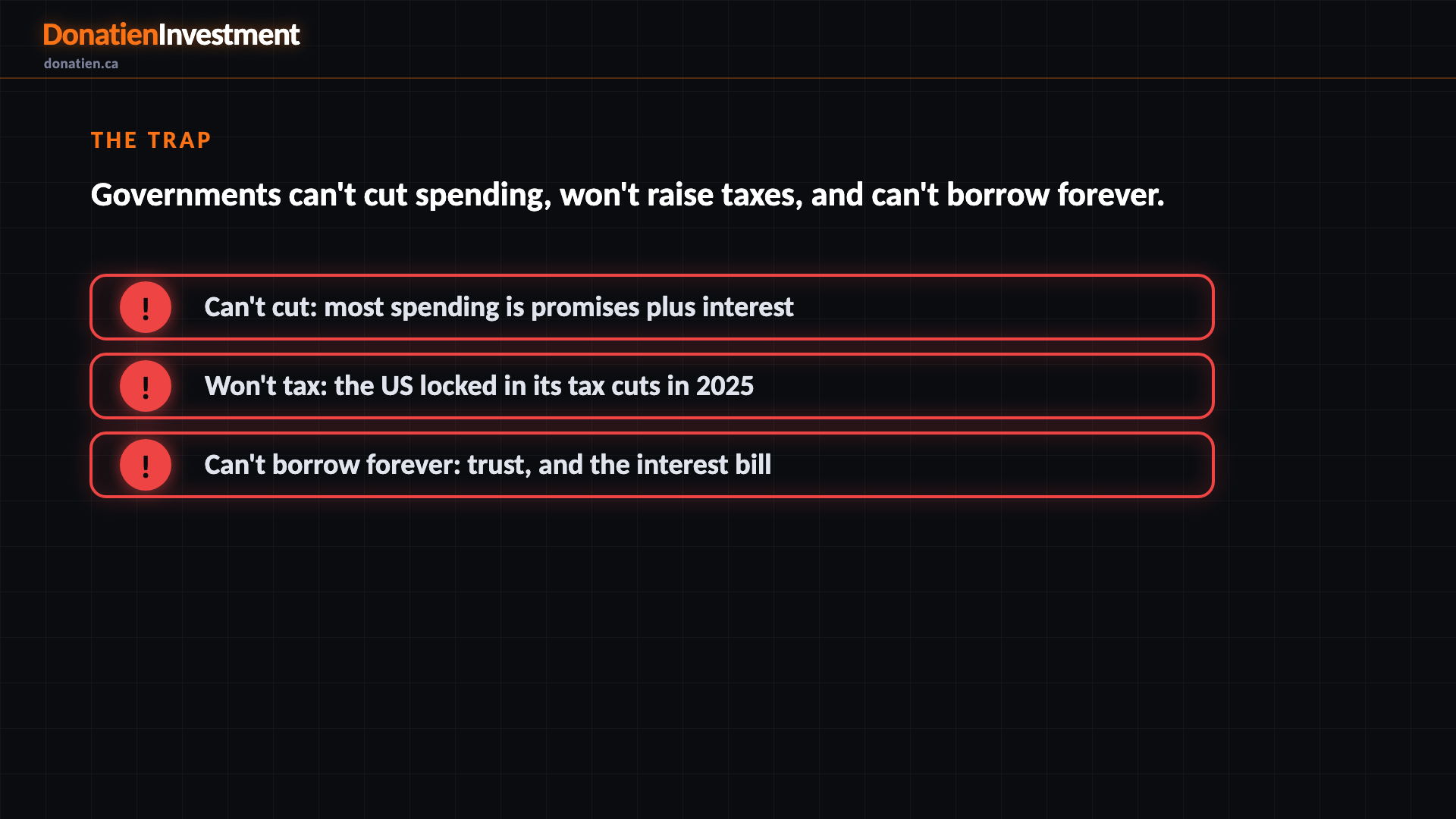

The trap

Here's the trap. A government has three obvious ways to deal with too much debt, and modern politics has closed all three. It can't easily cut spending, because most of the budget is promises already made — pensions, health care, and interest on old debt. It won't raise taxes; the United States actually made its tax cuts permanent in 2025, by law. And it can't borrow without limit, because lenders keep buying the bonds only while they trust they'll be repaid in money that still has value — and because the interest bill eventually eats the budget from the inside. Can't cut, won't tax, can't borrow forever. That's the corner.

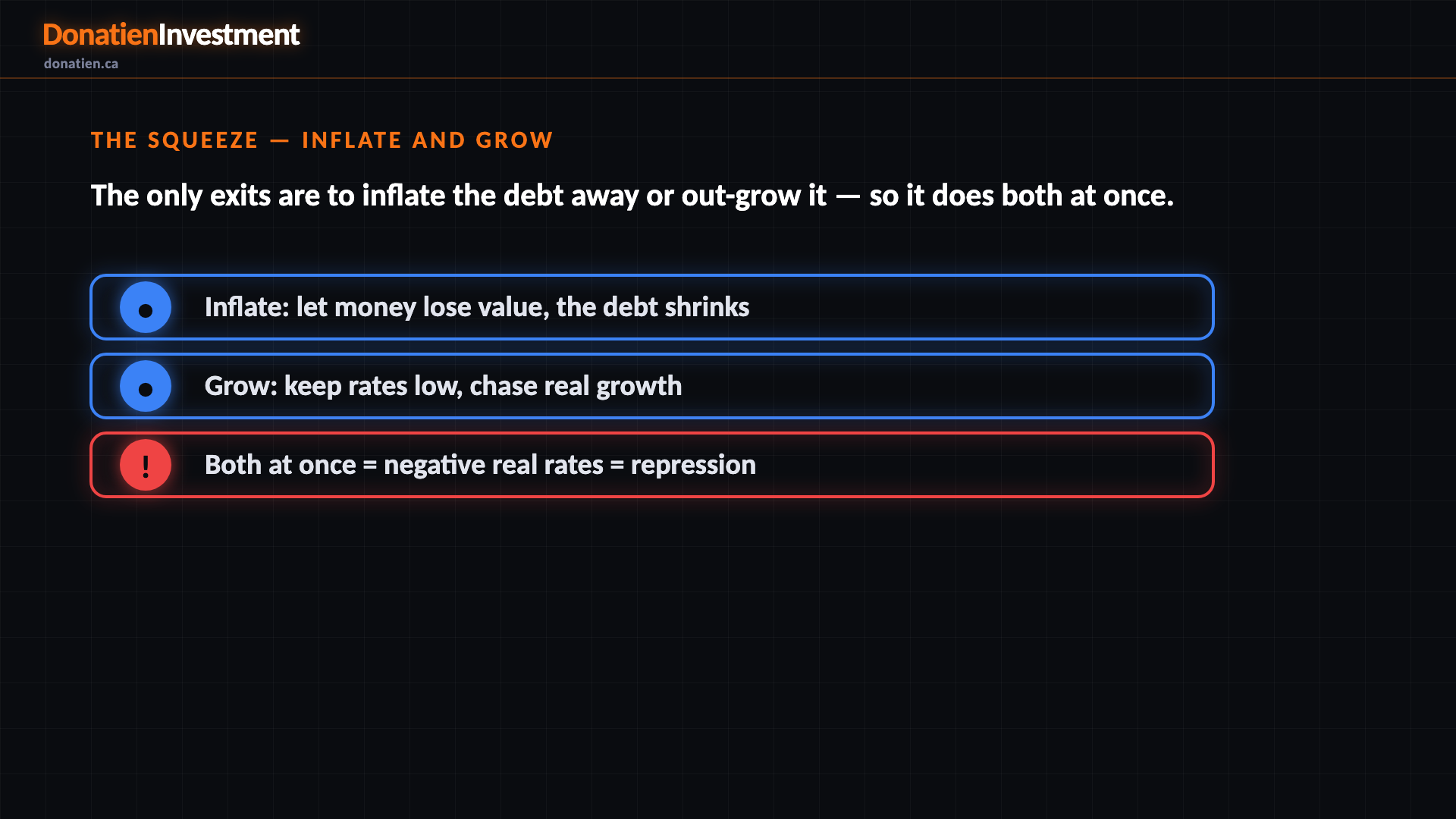

The squeeze — inflate AND grow

From that corner, a government has only two real exits, and here's the key point: it doesn't pick one, it runs both at the same time. Exit one, inflate it away: let the money supply grow and keep policy loose, so inflation quietly shrinks the debt — because the debt is a fixed number of dollars, and each dollar is worth a little less every year. Exit two, grow out of it: keep interest rates as low as possible and chase real growth, so the economy expands faster than the debt. Now watch what happens when you pull both levers together. Growth wants rates low; inflating wants prices high. Put them together and your cash earns less than prices are rising — a guaranteed slow loss. Economists have a name for that: financial repression. It's not a bug. It's the machine.

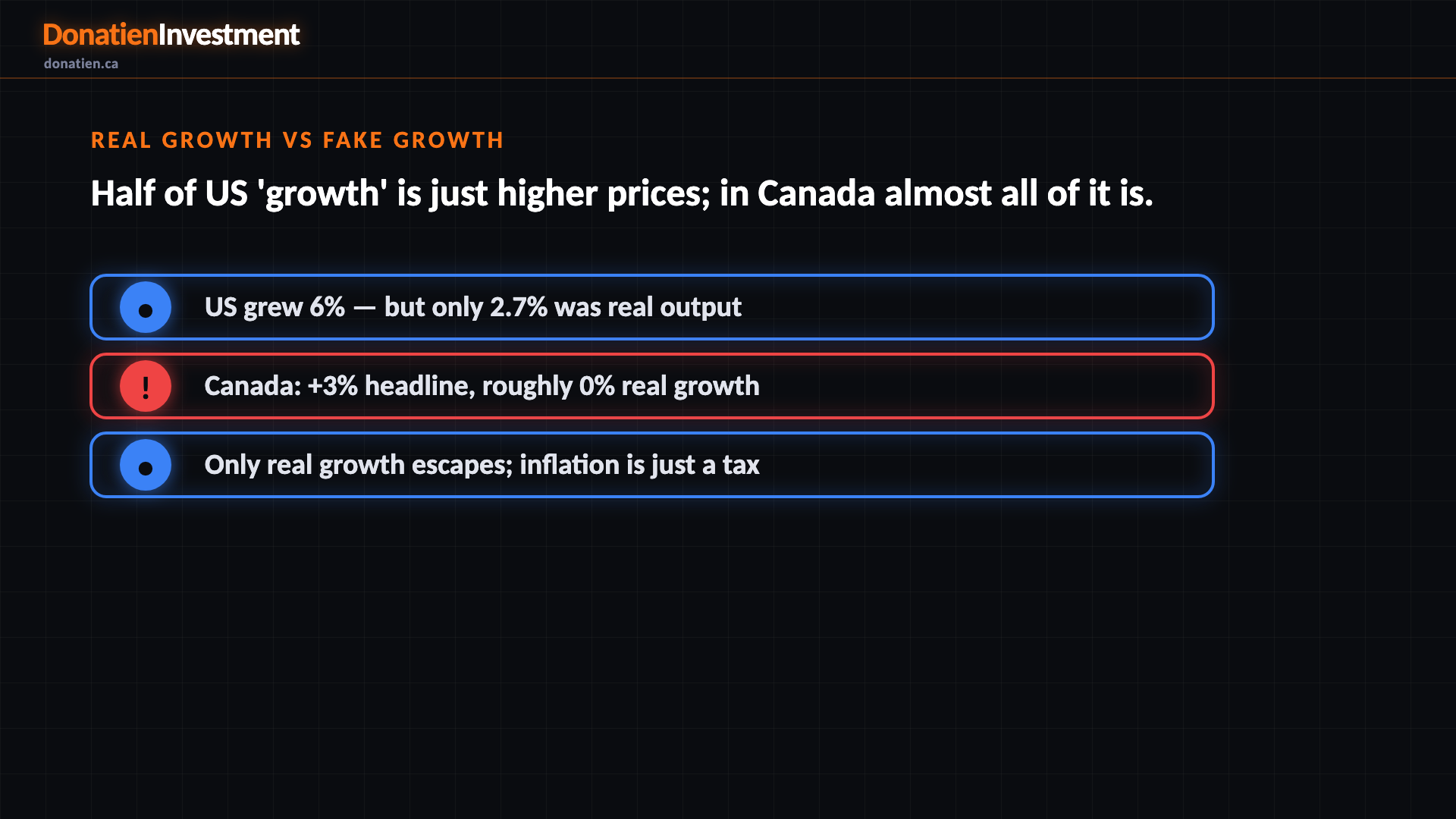

Real growth vs fake growth

This is where you have to watch the words closely, because there's real growth and there's fake growth. When you hear the economy grew six percent, that's measured in dollars that are losing value. Strip the inflation out and only about two-point-seven percent was real — actual extra stuff produced. The rest was just the price tag rising. Canada is the extreme version: its economy grew about three percent on paper, but once you remove inflation, real growth was essentially zero. The country's headline rose while Canadians, per person, went backwards. This matters because only real growth is a genuine escape from the debt. Inflated growth just shrinks the debt by taxing everyone through higher prices — the hidden tax, wearing a growth costume.

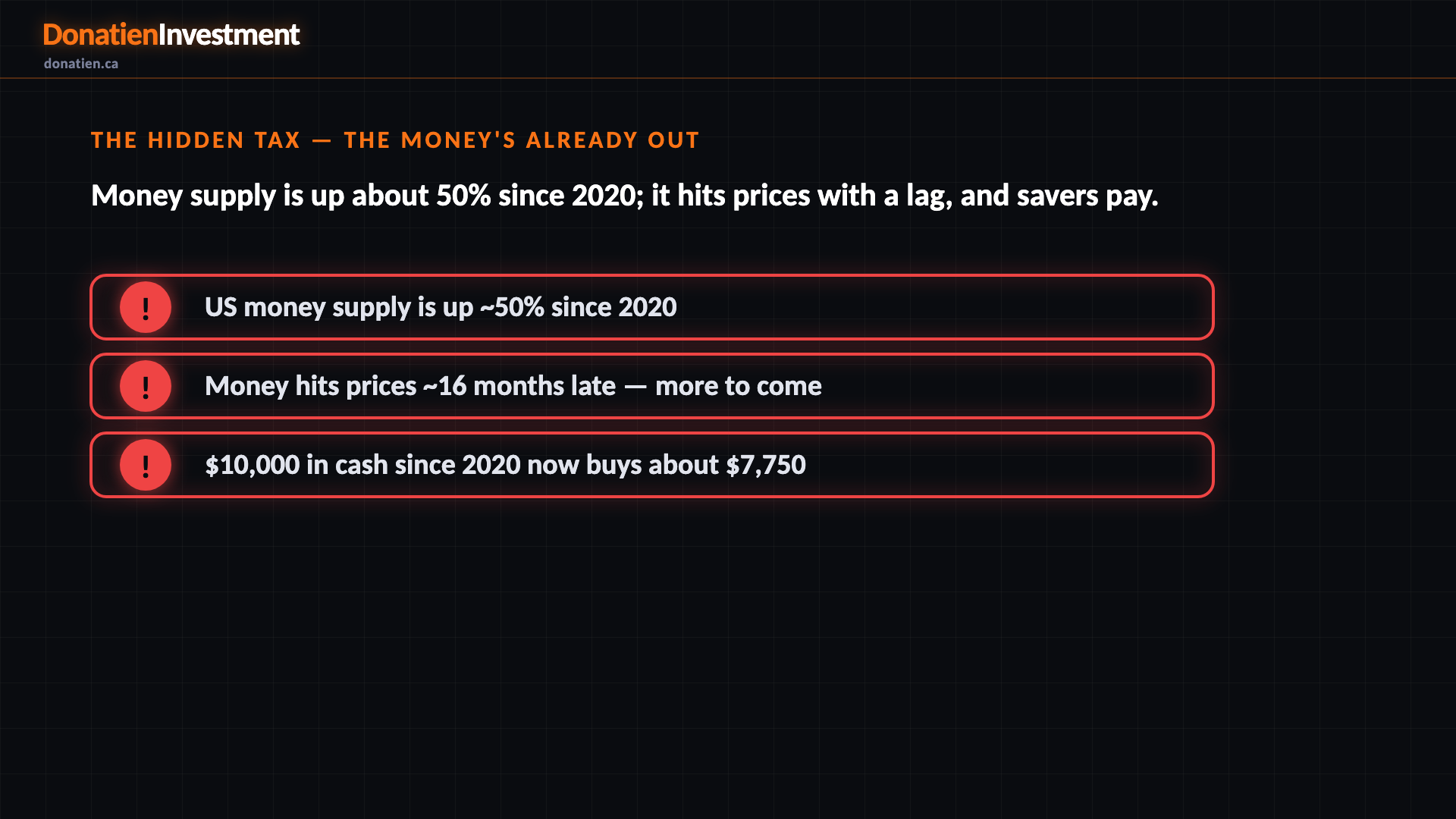

The hidden tax — the money's already out

So how does the inflating actually reach you? Quietly, and late. The amount of money in the US system has grown by roughly fifty percent since 2020 — most of it created in the pandemic — and that money never left. New money reaches prices with a long delay, usually a year or two: last cycle, money supply exploded in early 2021 but inflation didn't peak until the middle of 2022, about sixteen months later. So a burst of money-printing isn't finished when the printing stops; its effect on prices keeps arriving. And it doesn't hit everyone equally. It reaches asset owners first, wage-earners and savers last — after prices have already risen. The plain result: ten thousand dollars left in cash since 2020 now buys what about seven thousand seven hundred and fifty did then. Nothing was stolen. The number stayed the same; the money shrank.

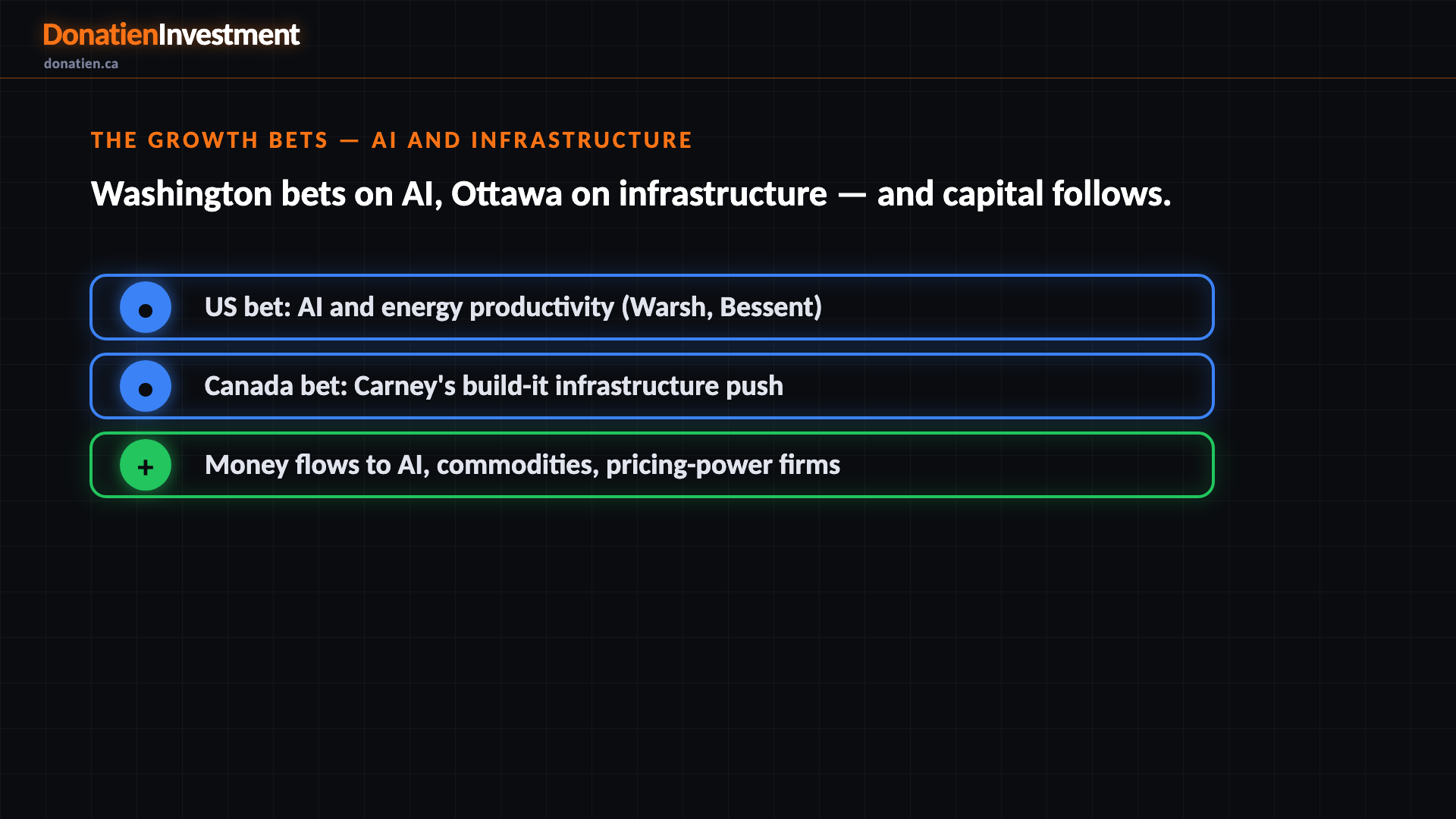

The growth bets — AI and infrastructure

If a government is going to try to grow out of its debt, it has to bet on something. Two bets are live right now. Washington is betting on artificial intelligence and energy: the Treasury argues AI can double productivity and deliver growth without inflation, and the Fed's new chair, Kevin Warsh, has argued the same — which he sees as grounds to eventually lower rates. You can see the money moving: US tech giants are pouring hundreds of billions into AI infrastructure. Canada is making a different bet — Mark Carney's government is borrowing deliberately to build: housing, energy, infrastructure. In plain terms, capital is flowing toward the growth each government is backing, and toward the real things a build-out needs — energy, metals, and companies that can hold their prices. This is a description of where money tends to flow, not a suggestion to buy any of it.

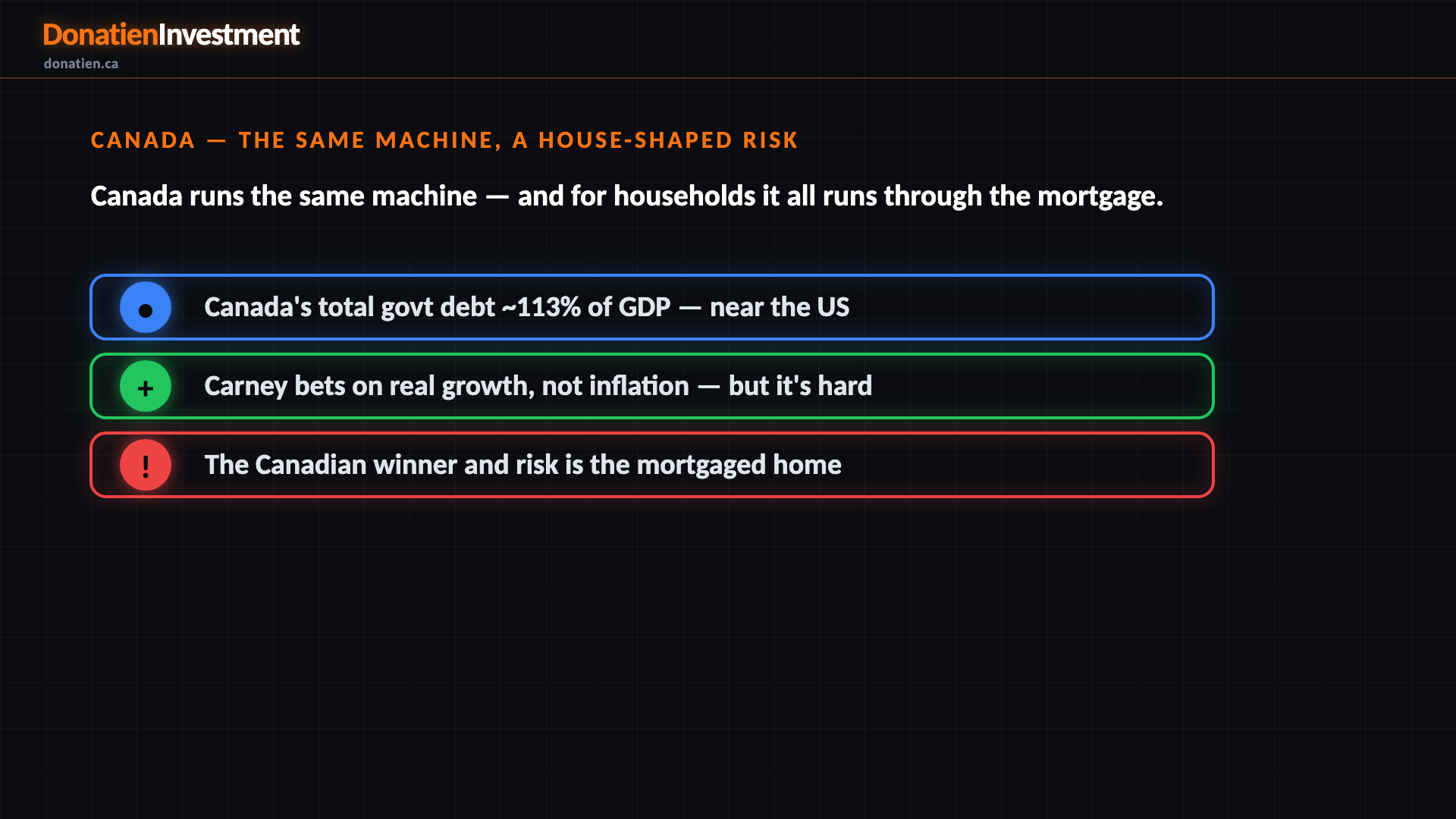

Canada — the same machine, a house-shaped risk

A quick word on Canada, because it runs the very same machine. It printed money in 2020 and 2021 too, and once you count the provinces, its total government debt is about a hundred and thirteen percent of the economy — right alongside America's. The difference is the bet: Mark Carney is trying to grow out of the debt rather than inflate out of it, which is the honest, hard path, and it may not pay off. And for Canadian households, this whole story runs through one asset — the house. Canadians hold most of their wealth in property, carry the highest household debt in the G7, and most of that is mortgages. So the report's biggest winner — a real asset bought with debt — is, very literally, the family home. That's also the risk: Canadian mortgages reset every few years, so the cheap rate doesn't last, and that leaves households far more exposed to rates than Americans.

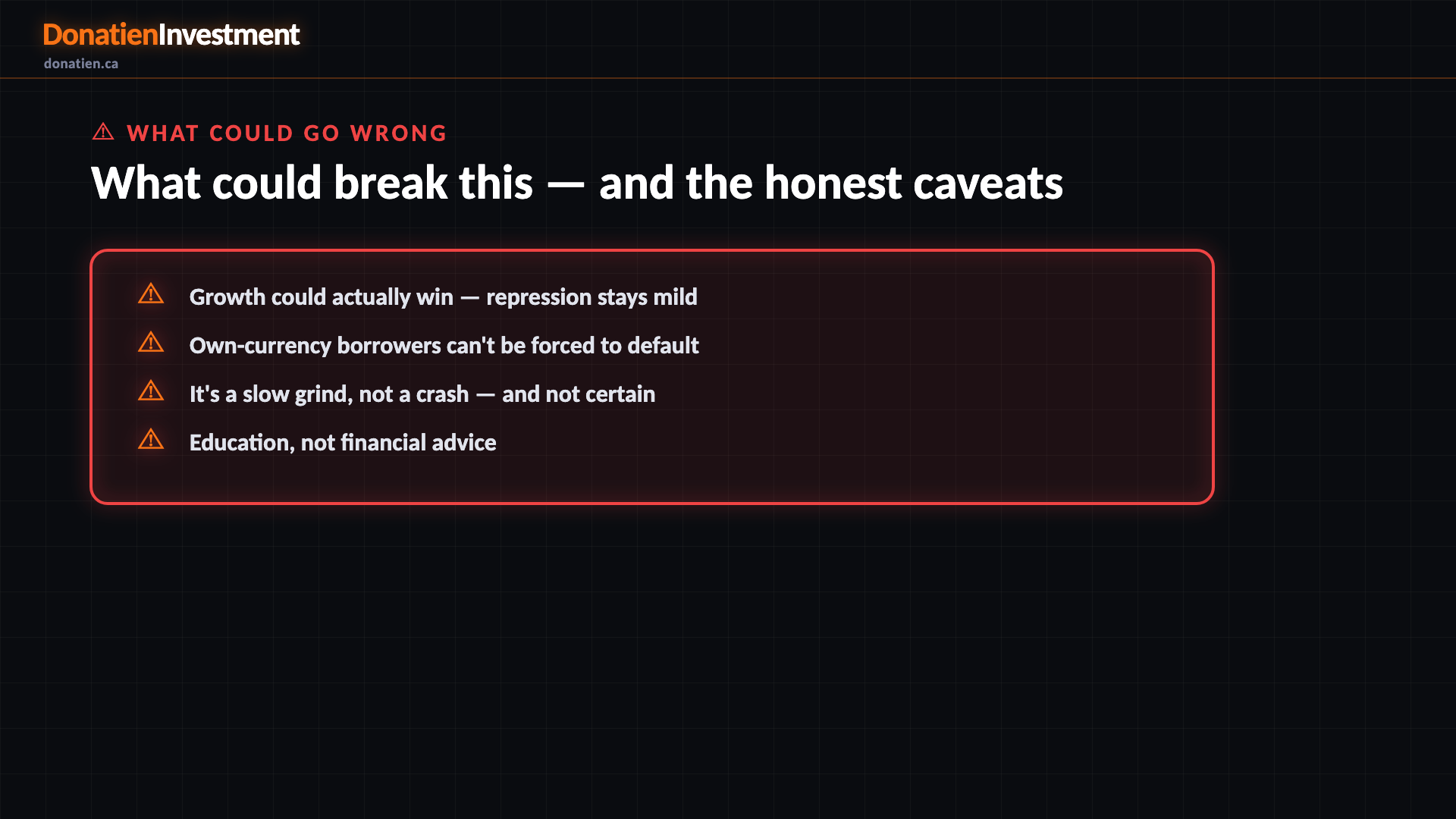

What could break this — and the honest caveats

Now the other side, loudly, because none of this is certain and it is not a forecast of doom. There's a real chance the growth bet actually works — that AI and investment lift the real economy fast enough that the debt shrinks without much pain. That's roughly a one-in-four chance, and it's exactly what Canada is attempting. Governments that borrow in their own currency also can't be forced to go bankrupt; the risk is slow erosion, not a sudden crash. Two more honest points. The printer is not running at full tilt today — the real return on savings is still slightly positive, though the US central bank did quietly start expanding again in late 2025. And this describes where wealth tends to flow; it names no investments, and it is not financial advice.

Risk vs Reward

Putting numbers on the uncertainty: the base case, a slow managed erosion — the squeeze closing gradually — is about fifty-five percent. Growth genuinely winning the race is about twenty-five. And a funding scare, where lenders balk and a central bank is forced to print openly, is about twenty. Most likely a slow grind, a real chance of a clean escape, a smaller chance of a scare.

The verdict

So, the machine in one breath. Cornered governments inflate and grow at the same time, and the collision — cheap money running alongside hotter inflation — quietly moves wealth in one direction: toward real assets, pricing power and cheap-fixed-rate borrowers, and away from cash, wages and bonds. There is one clean way out that isn't a tax on savers — real growth, fast enough to outrun the debt. It's the hardest path, and it's the one Canada is now openly attempting. Whether those growth bets pay off is the single most important question in the whole story.

Read the full report on donatien.ca →{kind=link}

{kind=link}