The Stagflation Reaction Function Position for a Fed that bends to a loose Treasury — if stagflation holds

a steeper curve, a bid under gold and real assets, a structurally softer dollar, and equities that must earn their multiple

A Donatien Special Report — how Washington fights stagflation, and what it means for your portfolio.

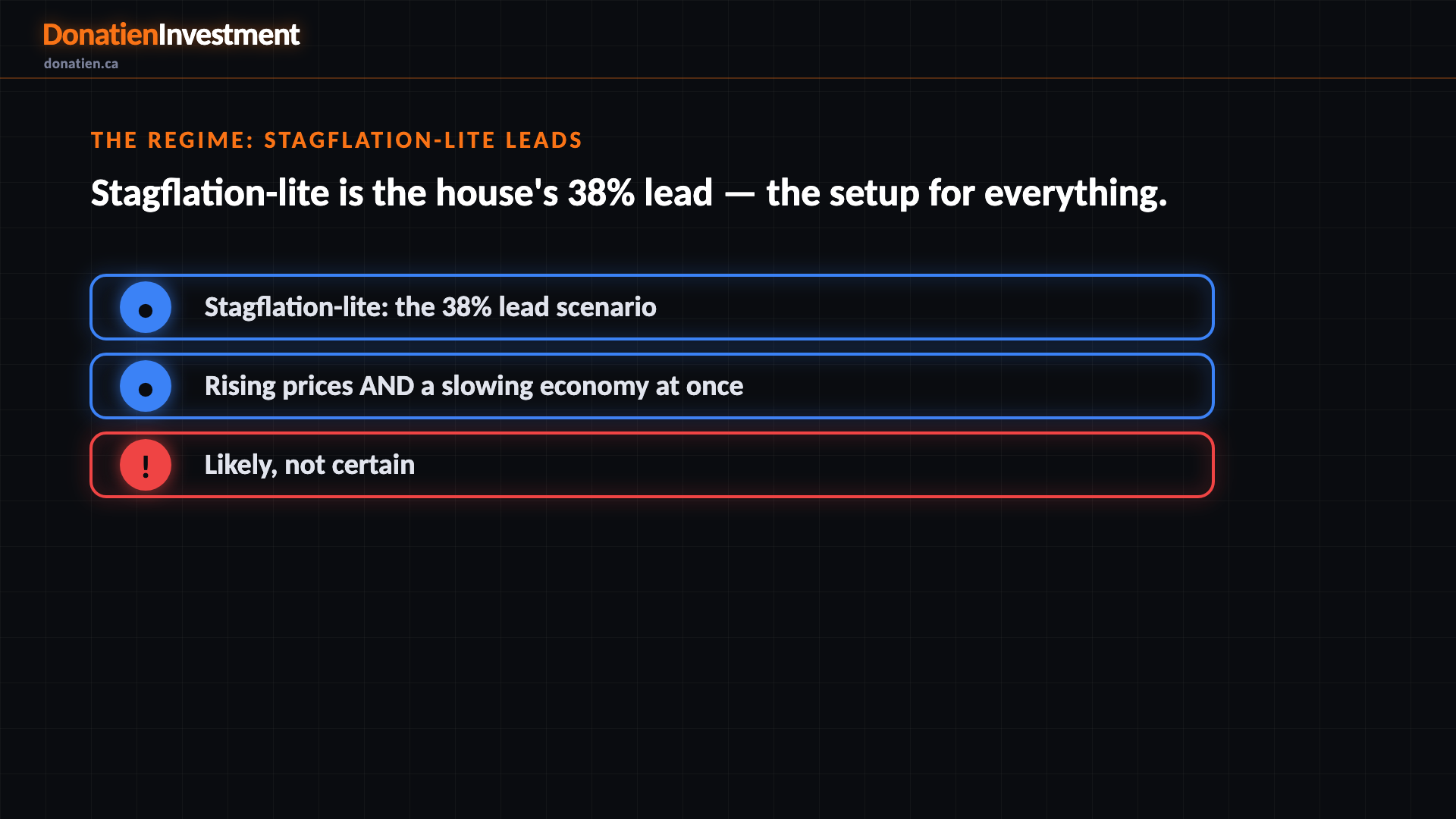

The regime: stagflation-lite leads

Let's start with the backdrop. Stagflation is a rare, nasty mix: prices keep rising too fast while the economy slows and unemployment climbs. It's the hardest spot for the Federal Reserve, because its two jobs clash — high prices say raise interest rates, rising unemployment says cut them. In stagflation both are true at once. Our house view makes this the single most likely path, at thirty-eight percent, though far from certain. It's the one regime that forces the people in charge to choose.

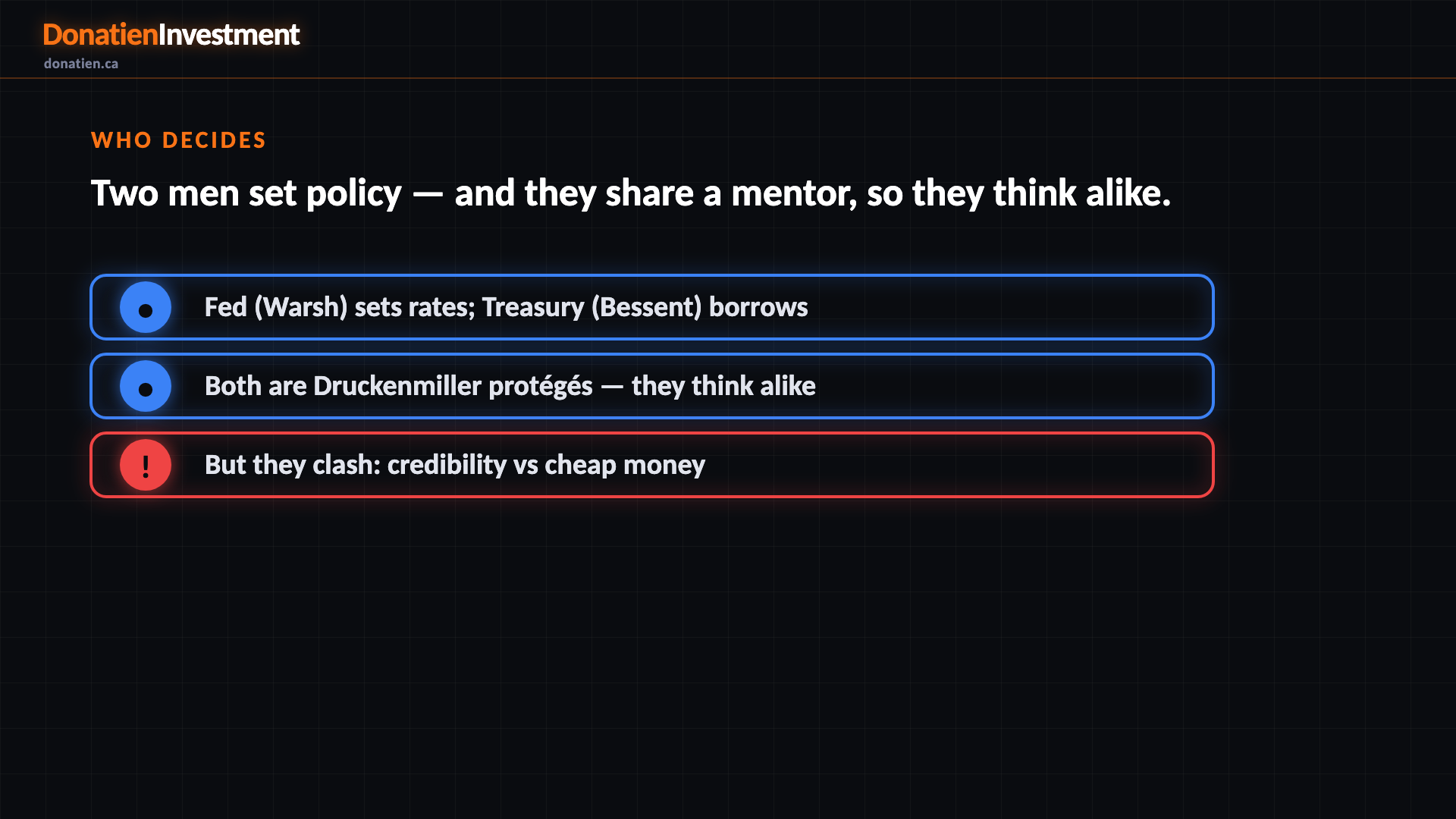

Who decides

So who decides? Two people. Kevin Warsh runs the Federal Reserve, which sets interest rates. Scott Bessent runs the Treasury, which manages the government's huge borrowing. Here's the thread most coverage misses: both are protégés of the same man, Stanley Druckenmiller, one of the most famous hedge-fund investors alive. Bessent made his fortune working under him; Warsh has been his business partner for fifteen years. So they think alike — but in stagflation they want different things. Warsh wants to hold rates high to defend the Fed's credibility on inflation; Bessent wants cheap borrowing, so he leans toward looser, easier money.

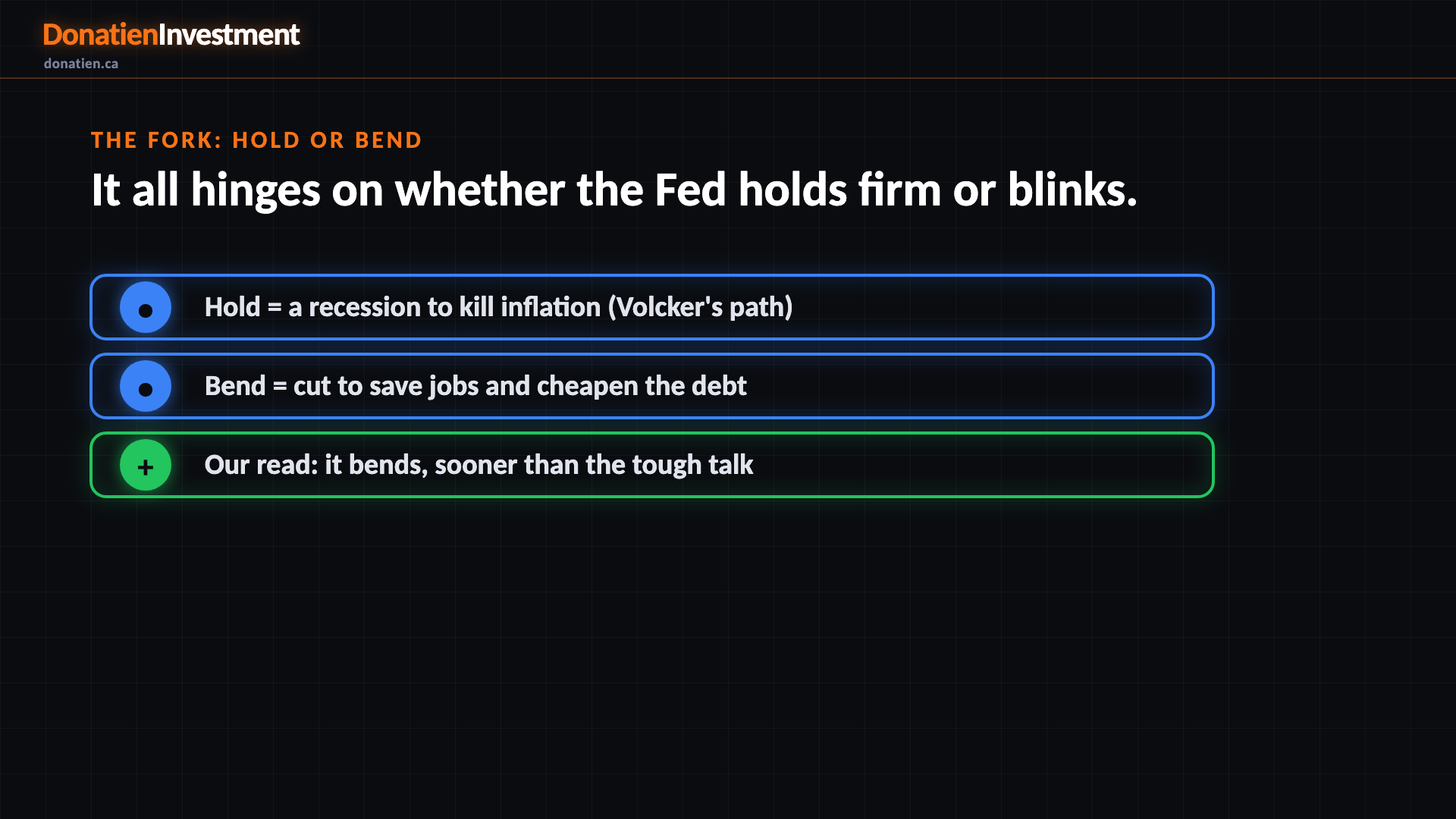

The fork: hold or bend

It comes down to one decision. When growth weakens, does the Fed hold firm — accept a recession to crush inflation, as Paul Volcker did in the eighties — or blink, and cut rates to protect jobs and cheapen the government's debt? Our read is that it blinks, sooner than Warsh's tough talk suggests: he wanted cuts before inflation spiked, the debt bill is huge, and he's built a way to justify easing using his own softer inflation measures. That's a judgement, not a fact — and if he holds the line, much of this is wrong.

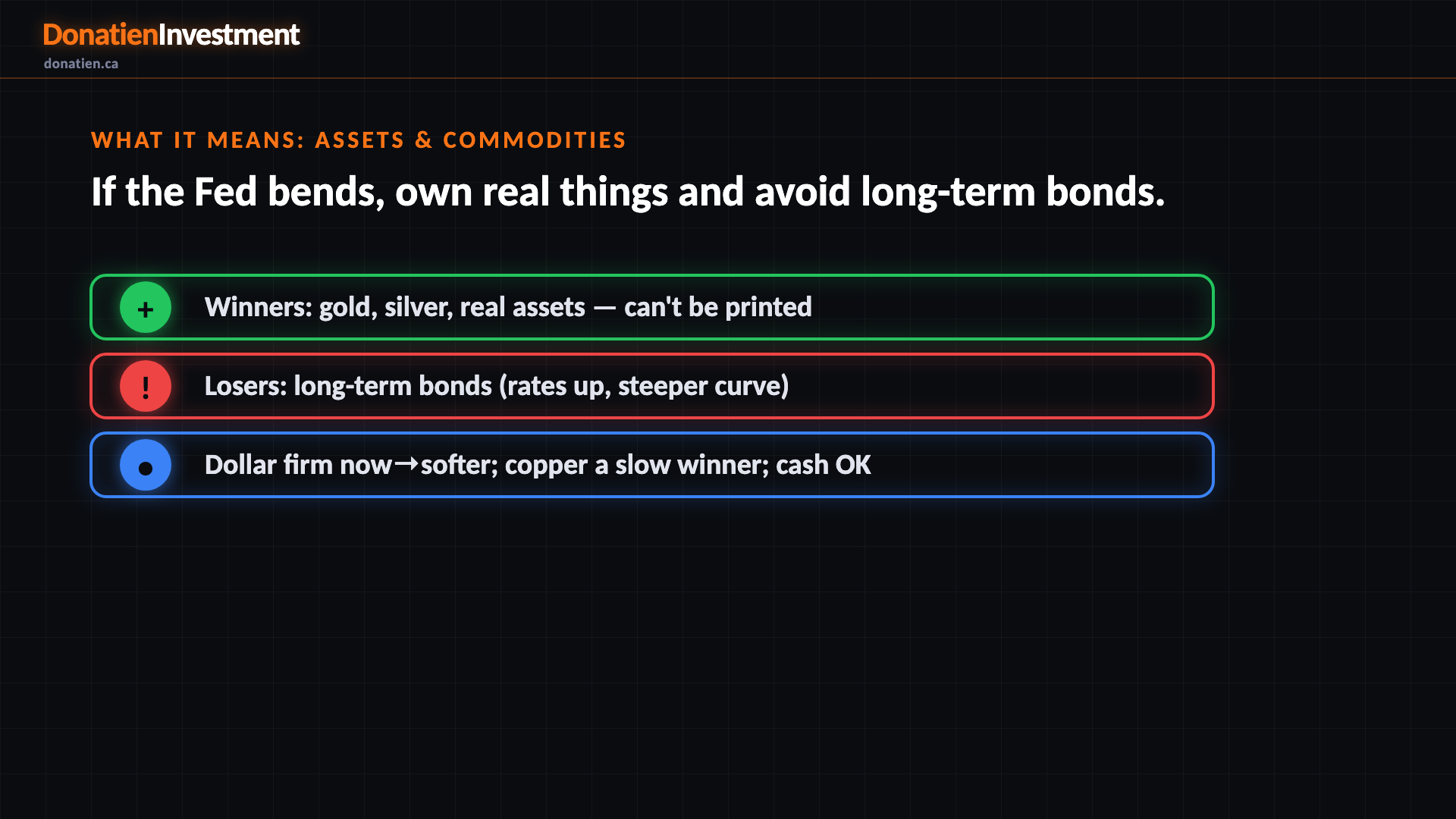

What it means: assets & commodities

So if the Fed bends, what happens to your money? Start with the broad asset classes. Long-term government bonds are the clear loser: heavy borrowing plus sticky inflation pushes long rates up, what traders call a steeper curve. Cash pays you to wait. The dollar holds up for now, then weakens over time. Gold and real assets, things you can't print, are the core winners, because they hold value as money is made cheaper. In commodities, gold and silver lead, copper is a slower-burn winner as industry re-tools, and oil stays firm near-term but is capped later.

What it means: stock sectors

Now the stock market, sector by sector. The winners are the real-economy and defensive names: energy and materials, which inflation and hard assets favour; consumer staples and health care, which people buy whatever happens; and banks, which gain from that steeper curve and lighter regulation. The losers are the rate-sensitive and expensive names: pricey technology, marked down when long rates rise; consumer discretionary, as squeezed households cut back; and property trusts and utilities, which trade like bonds. In one line: own steady, cash-generative businesses with pricing power, over expensive growth.

What could break this

Now the other side, loudly, because none of this is certain. Stagflation-lite is our best single guess at thirty-eight percent, which leaves a sixty-two percent chance it's something else. If the economy simply reaccelerates, about a one-in-four chance, the Fed stays tough and gold and bonds get hurt instead. If growth collapses into a bust, the map flips toward owning those same long-term bonds. And if Warsh proves a true inflation hawk who won't blink, the easing never comes. This is a map of what's likely if one scenario holds — not a prediction, and not financial advice.

Risk vs Reward

The house puts stagflation-lite at thirty-eight percent, a reacceleration at twenty-six, a soft landing at twenty-two, and a deflationary bust at fourteen. The base case assumes the lead scenario holds, and it shifts as those odds shift.

The verdict

If stagflation holds and this team runs true to form, the trade looks like their mentor's own book: a steeper curve, gold and real assets bid, a softer dollar over time, and steady, cash-generative shares over expensive growth. The risk is that the Fed holds firm instead; the base case is that it bends.

Read the full report on donatien.ca →{kind=link}

{kind=link}