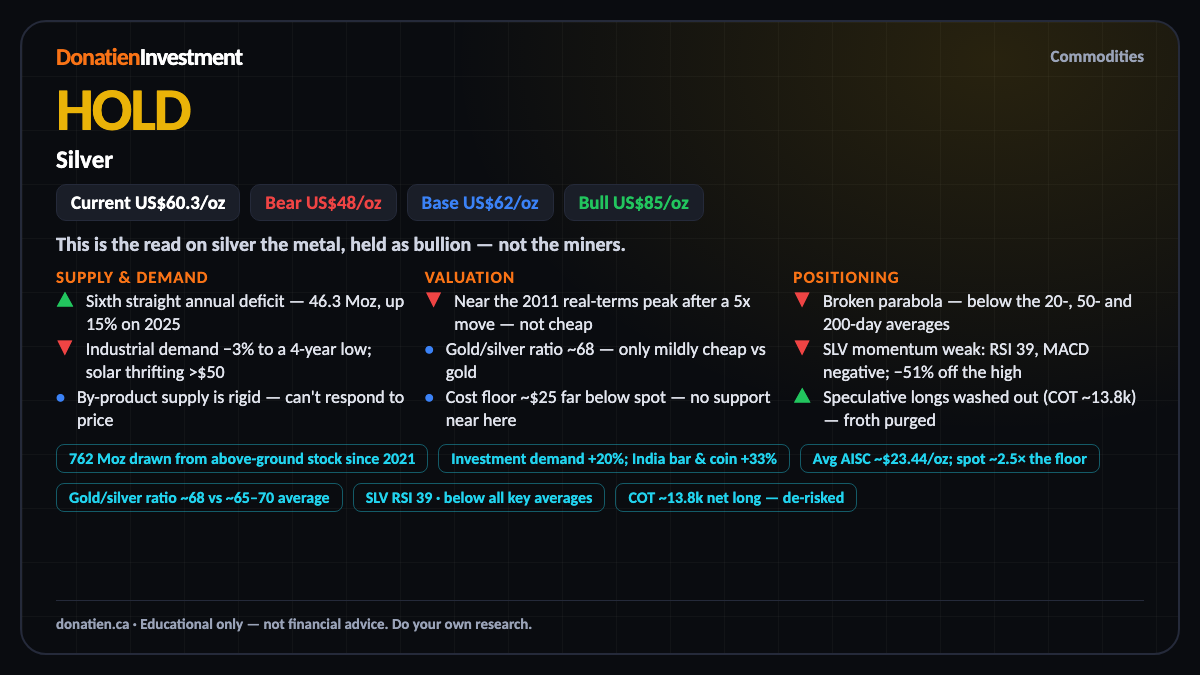

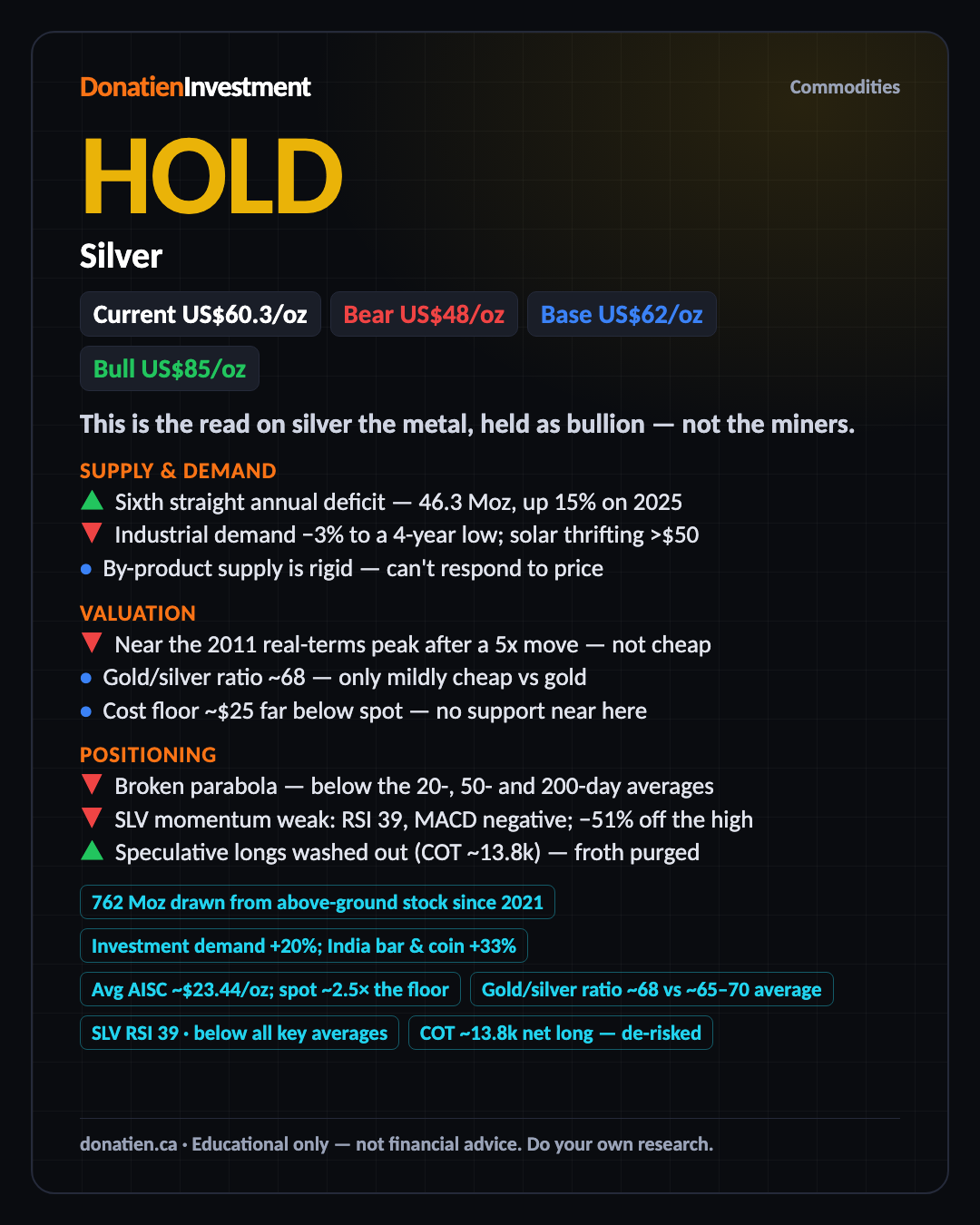

Silver HOLD

A long-term buy on a sixth straight annual deficit — but downgraded from strong buy: the squeeze has unwound, industrial demand is falling and the metal is rich after halving from its peak. Hold, and accumulate on weakness.

This is the read on silver the metal, held as bullion — not the miners. Silver is a hybrid: roughly half monetary, riding gold's coat-tails, and half industrial, driven by solar and electronics. The story of 2026 is a violent round-trip — a squeeze drove it to $121, then a hawkish Fed halved it. The squeeze left; the deficit did not.

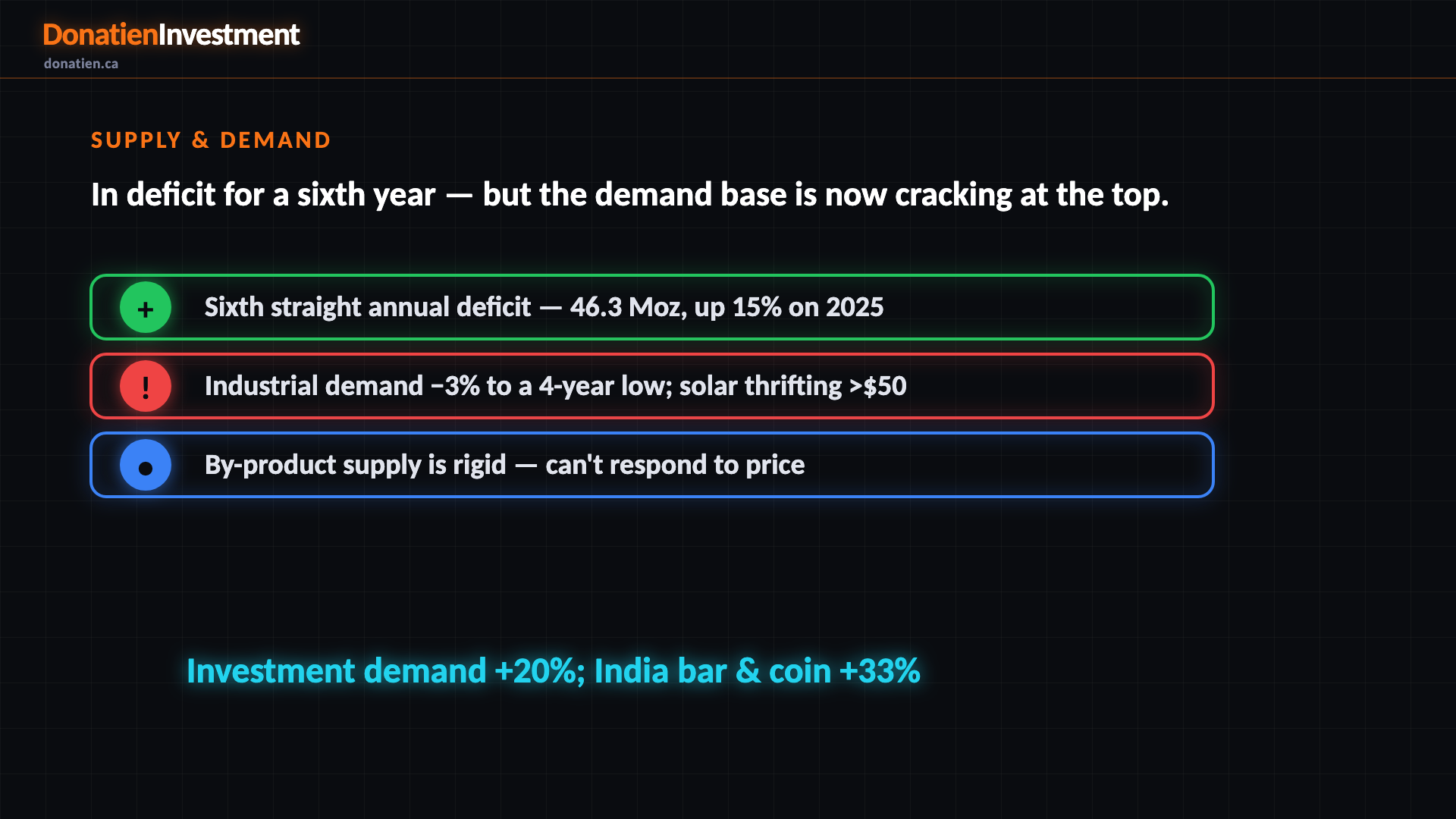

Supply & Demand

The structural case is a sixth straight annual deficit — 46.3 million ounces, widening from last year — with mine supply that can't respond, because seventy percent of silver is a by-product of other mining. That's genuinely bullish. But the demand base is cracking at the top: industrial demand fell three percent to a four-year low, and solar makers are actively engineering silver out above fifty dollars. Strong, in other words, but no longer strengthening — which is the heart of the downgrade.

762 Moz drawn from above-ground stock since 2021 · Investment demand +20%; India bar & coin +33%

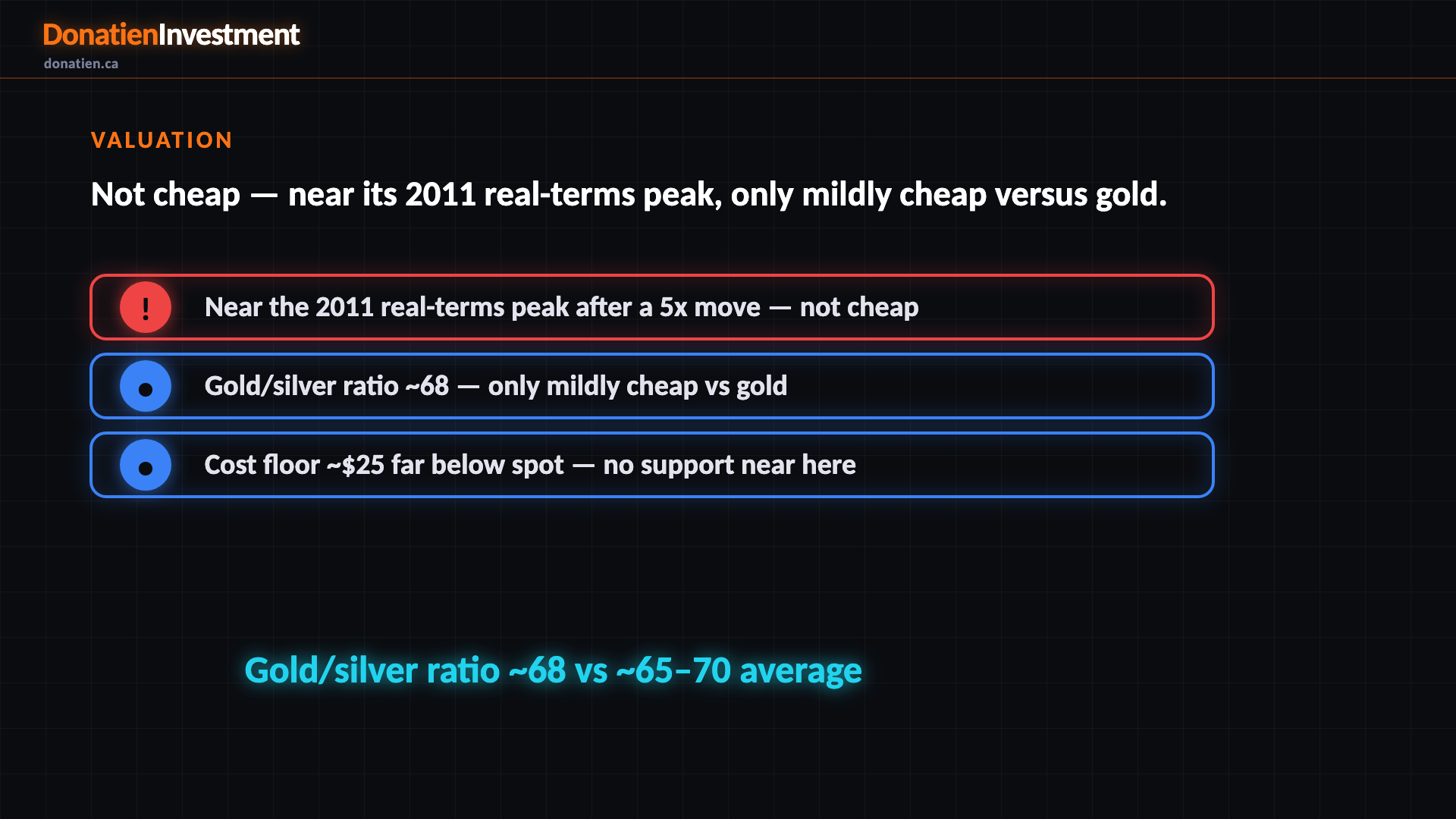

Valuation

Silver is not cheap. Even after halving it sits near its 2011 peak in real terms, having done a five-fold move off the base earlier this decade. The gold-to-silver ratio is about sixty-eight — only mildly cheap versus gold, and the easy catch-up trade is largely spent. The cost floor, around twenty-five dollars, is far below spot, so it offers no support anywhere near here. On valuation, then, the metal is fair-to-rich, not a bargain.

Avg AISC ~$23.44/oz; spot ~2.5× the floor · Gold/silver ratio ~68 vs ~65–70 average

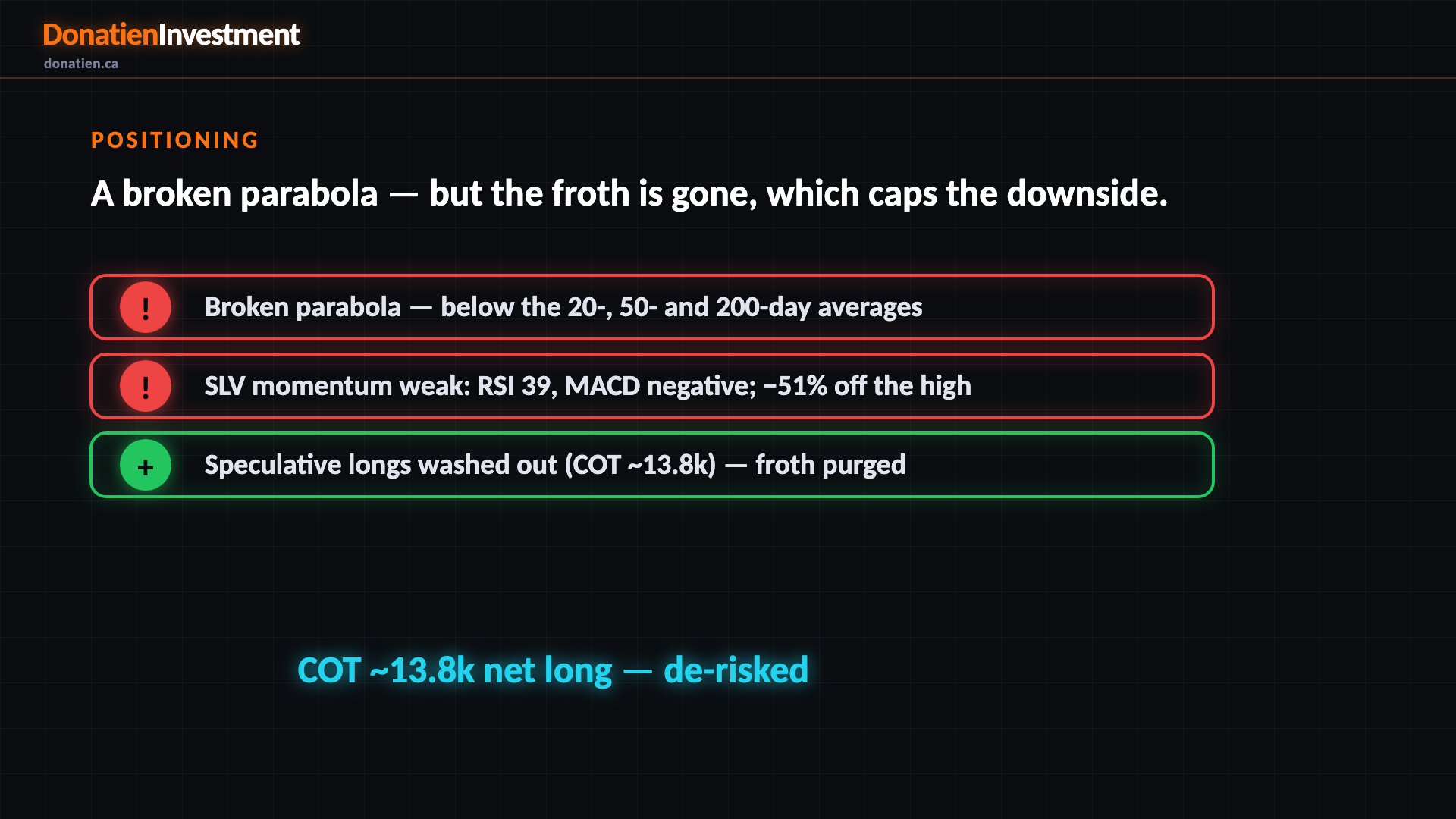

Positioning

The tape is a broken parabola. Silver is below its twenty, fifty and two-hundred-day averages, momentum is weak, and it's fifty-one percent off January's high. But there is a silver lining in the positioning: speculative longs have washed out to about fourteen thousand contracts — the froth is gone, which means less forced-selling fuel and room to rebuild. So the downside from here is a purge, not a rout — and that's why the call is hold, not sell.

SLV RSI 39 · below all key averages · COT ~13.8k net long — de-risked

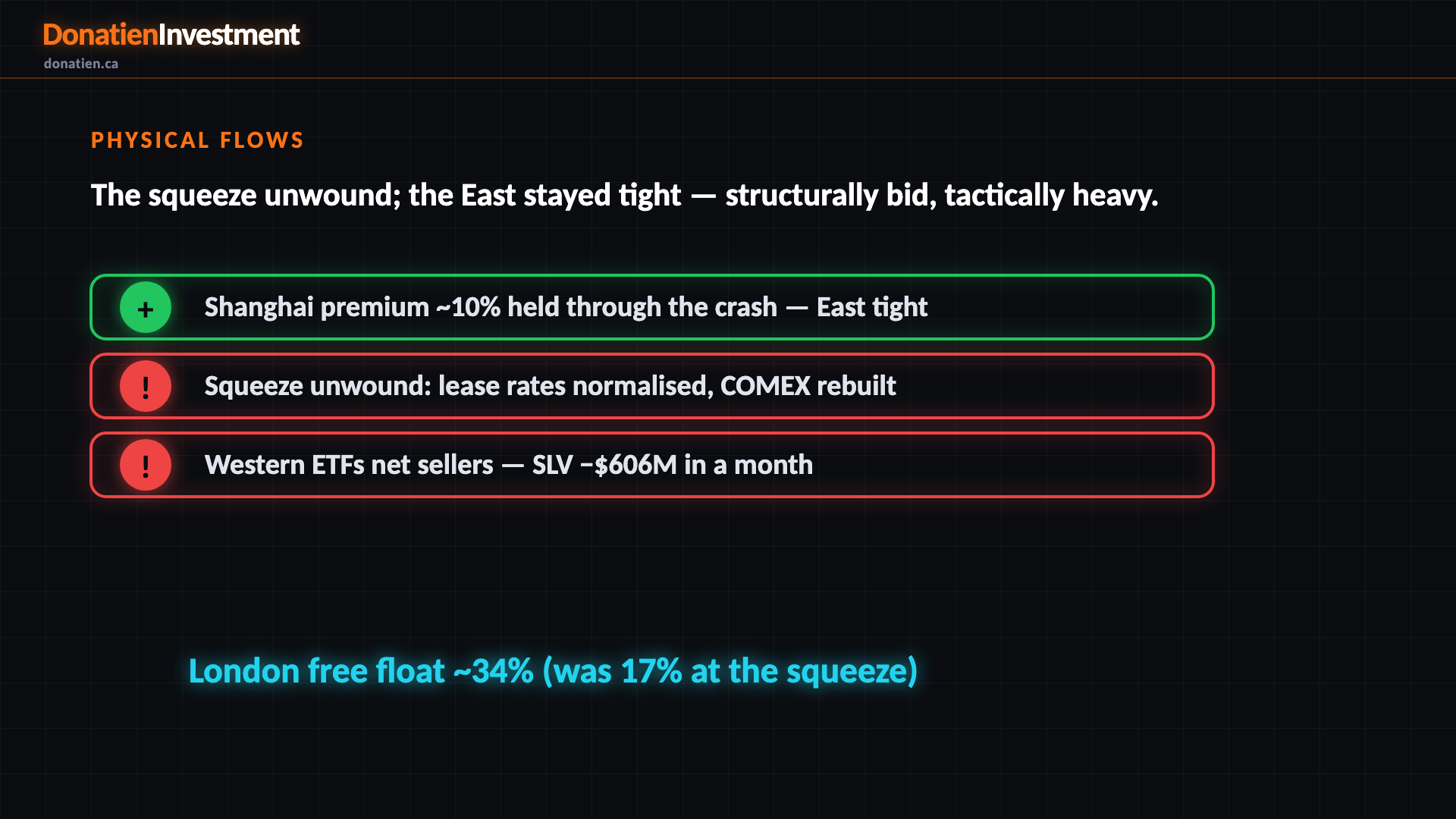

Physical flows

The plumbing tells the tension precisely. The mechanics of the spike released — lease rates normalised, COMEX stocks rebuilt, London's free float recovered from a record-low seventeen percent to thirty-four — and Western funds have been net sellers, with the big silver trust shedding six hundred million dollars in a month. Yet the Shanghai premium, around ten percent, held right through the crash. The East is still tight. West distributing, East accumulating: structurally bid, tactically heavy.

COMEX paper/physical back to 6.3:1 (was ~28:1) · London free float ~34% (was 17% at the squeeze)

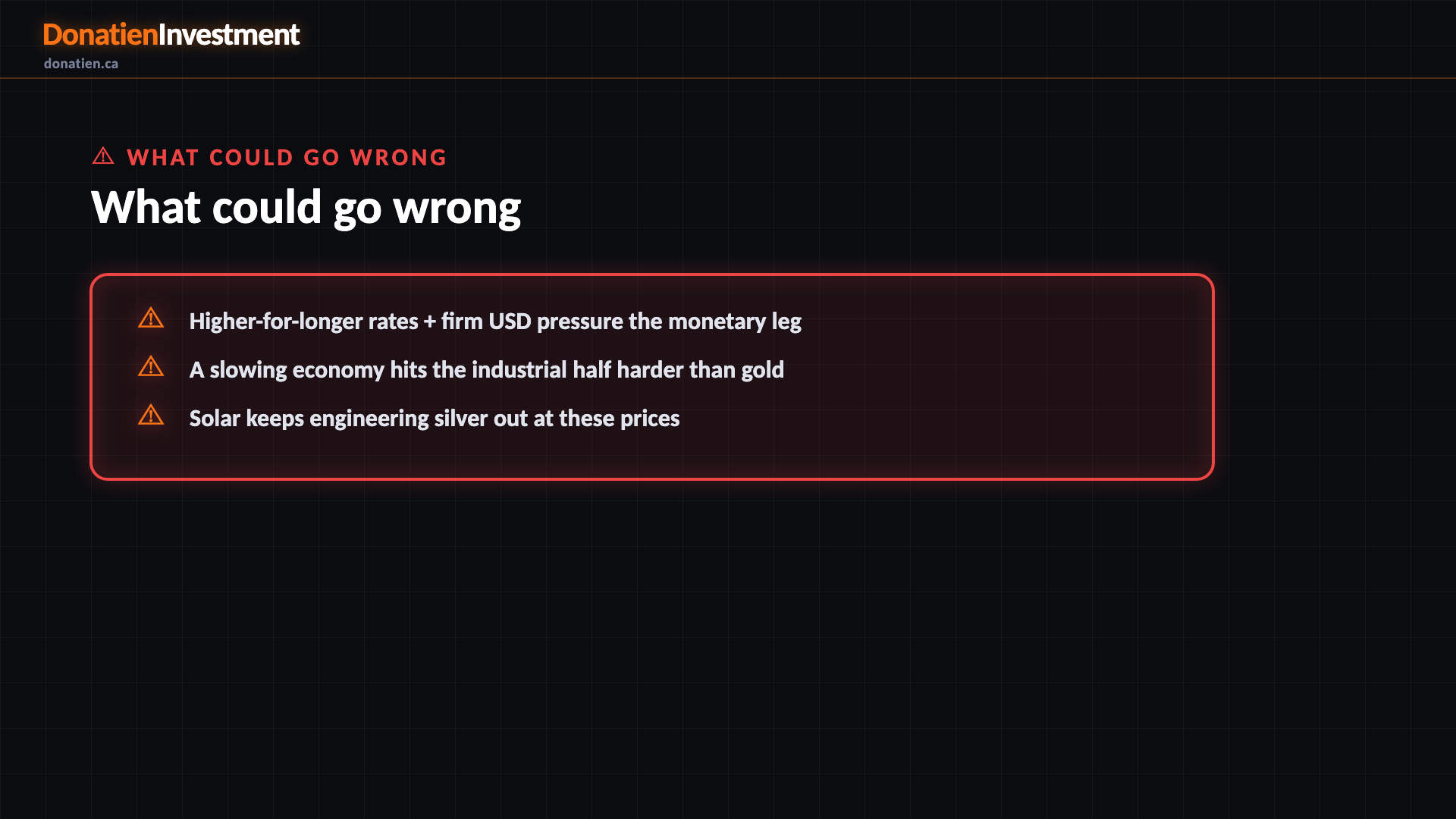

What could go wrong

The risks are the mirror of the case. Silver is the higher-beta cousin of gold and half its demand is industrial, so it's doubly exposed. Higher-for-longer rates and a firm dollar keep the monetary leg pressured — that's what halved it. A slowing economy would hit the industrial half harder than gold. And the bull's own engine is self-limiting: high prices keep pushing solar makers to thrift and substitute silver away. These are why the medium-term call came down to hold.

Risk vs Reward

The base case, and the likeliest over six to twelve months, has silver around sixty-two dollars an ounce — ranging around sixty as the deficit floors it and washed-out positioning slowly rebuilds. The bull case is about eighty-five if the Fed is forced back toward cuts and the monetary leg re-rates. The bear case is around forty-eight if higher-for-longer persists and the industrial slowdown deepens.

The verdict

Short term, hold. Medium term, hold — down from buy, because the demand base is eroding and the monetary tailwind has reversed. Long term it's still a buy on the sixth-year deficit and rigid supply, just no longer a strong buy. The squeeze that justified a hundred-dollar price has expired; accumulate the deficit thesis into weakness rather than chase the bounce. Drivers and regime only amplify — the eroding demand, the rich valuation and the broken tape set the call.

Read the full report on donatien.ca →{kind=link}

{kind=link}