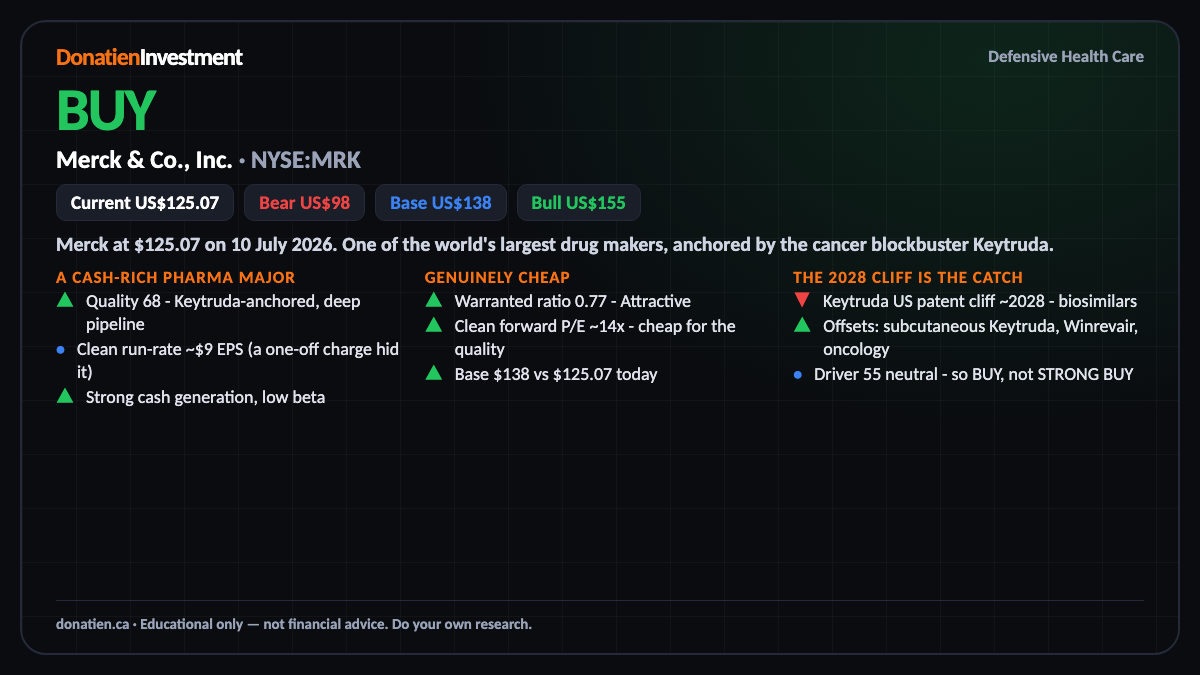

Merck & Co., Inc. (NYSE:MRK) BUY

A cheap, cash-rich pharma major on an attractive multiple - a BUY across all horizons, with the 2028 Keytruda patent cliff the risk to watch, not a reason to avoid.

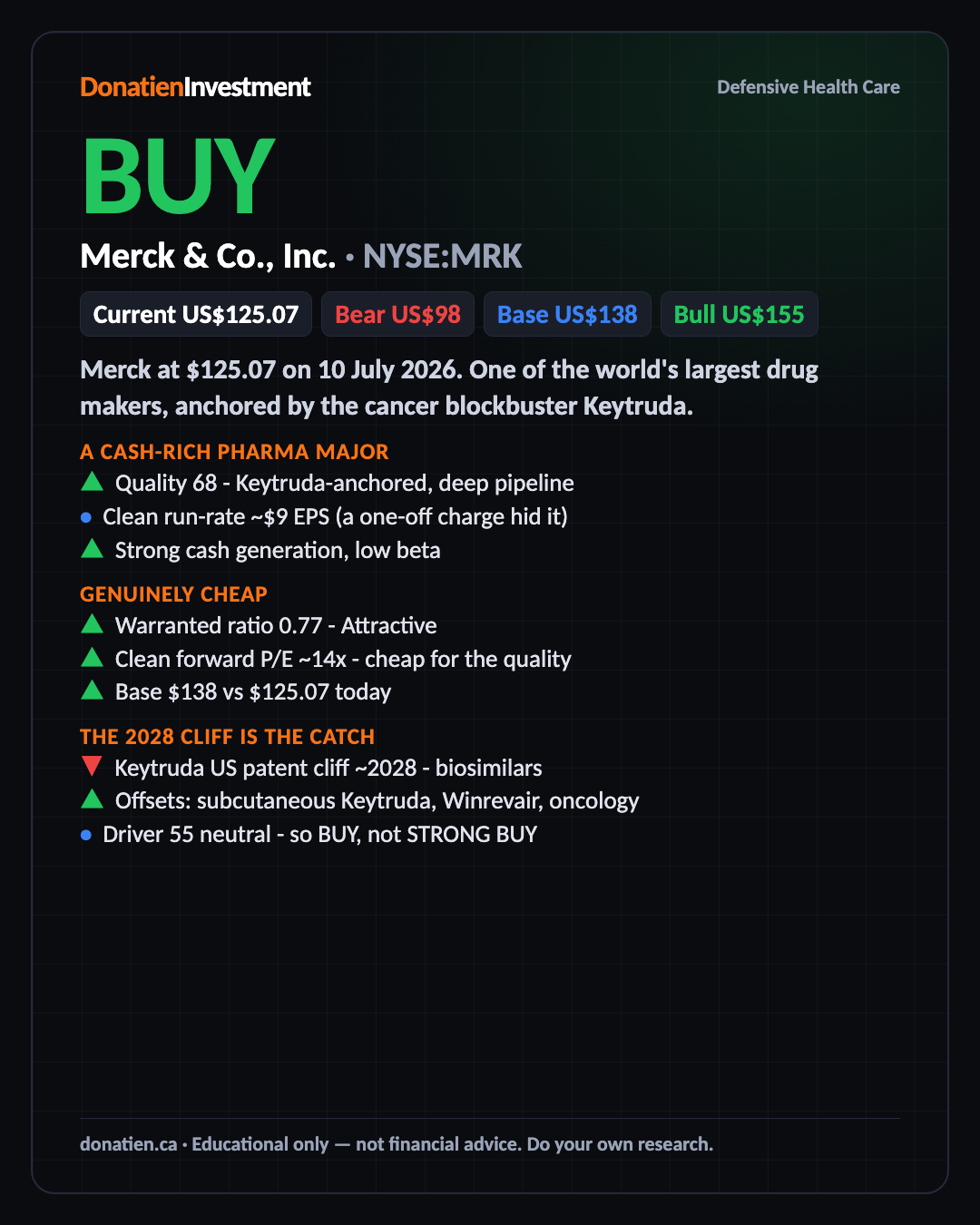

Merck at $125.07 on 10 July 2026. One of the world's largest drug makers, anchored by the cancer blockbuster Keytruda. The stock is cheap on the metrics that matter, the balance sheet is strong, and the report reads BUY at every horizon - the debate is whether the pipeline can offset Keytruda's US patent expiry in 2028.

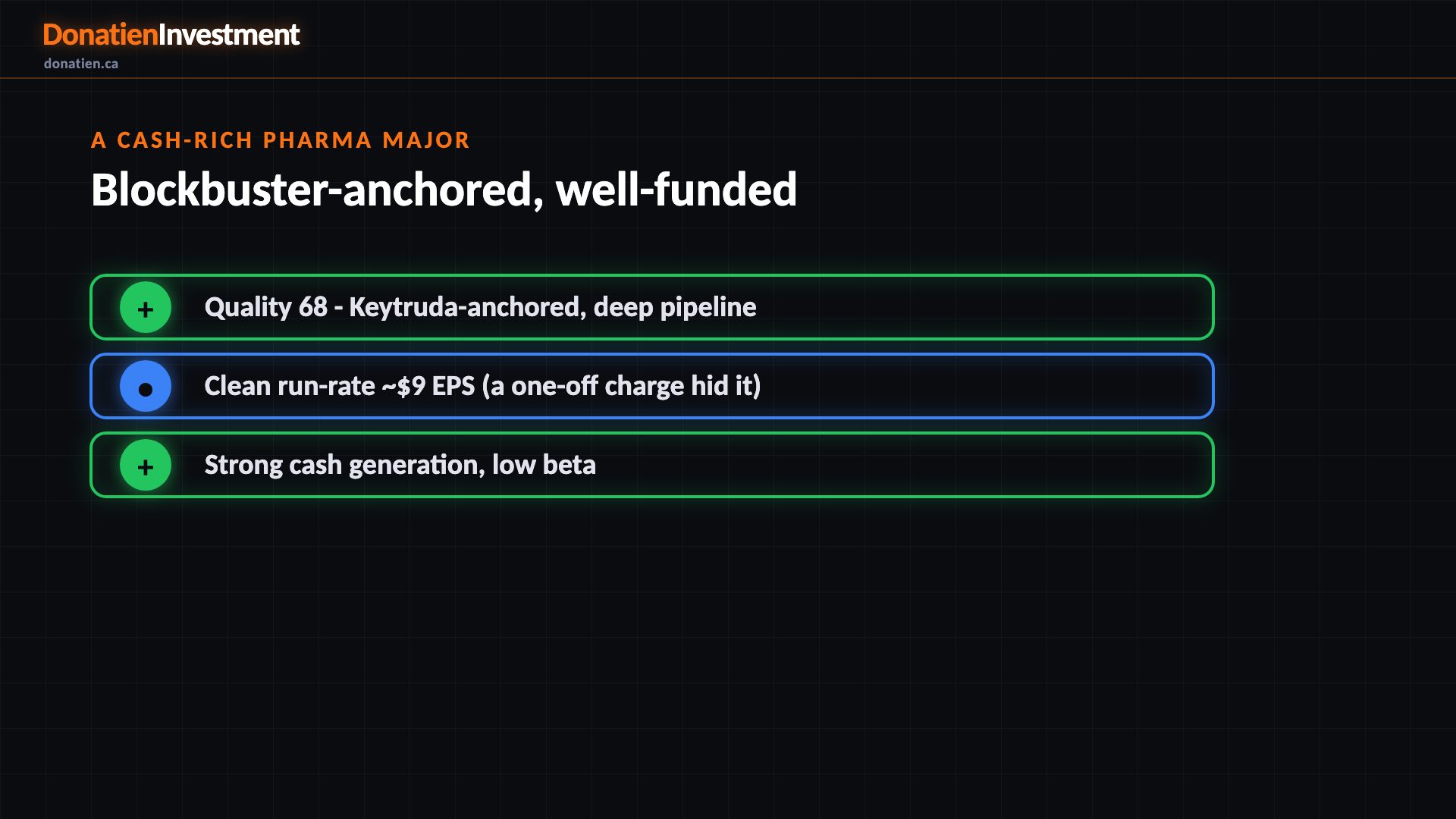

A cash-rich pharma major

Quality scores 68. Merck is built around Keytruda, the best-selling cancer immunotherapy, and backs it with a deep late-stage pipeline and strong cash generation. A recent quarter showed a headline loss, but that was entirely a one-off charge for buying in early-stage drug programmes - strip it out and the underlying earnings run at roughly nine dollars a share. This is a financially solid, research-driven business, not a distressed one.

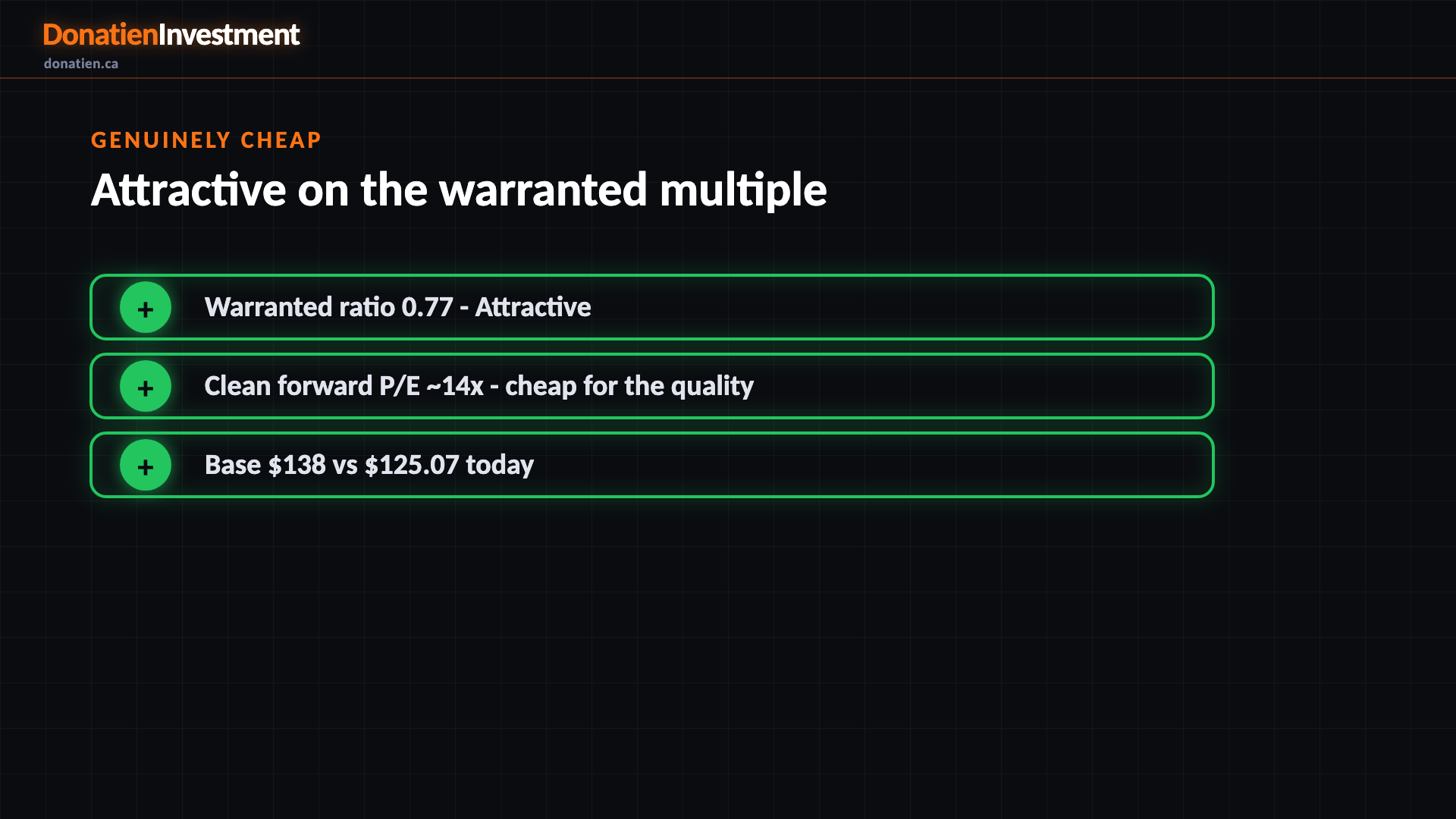

Genuinely cheap

Valuation scores 68 - Attractive. On the rate-and-growth warranted multiple it trades at about 0.77 of fair value, on a clean forward price-to-earnings near fourteen times - well below where a stable, cash-generative pharma of this quality should sit. Analysts see roughly eight per cent upside to consensus, and the base case is a hundred and thirty-eight against a hundred and twenty-five today. You're buying a quality franchise at a discount.

The 2028 cliff is the catch

Driver scores 55 - neutral, and that's why this is a plain BUY rather than a STRONG BUY. Keytruda loses US patent protection around 2028, and biosimilar competition plus drug-pricing pressure will bite. Merck is racing to offset it with a subcutaneous version of Keytruda, its pulmonary drug Winrevair, and new oncology - and there's a next-generation rival, ivonescimab, on the horizon. The health-care backdrop is supportive, but the cliff keeps us honest.

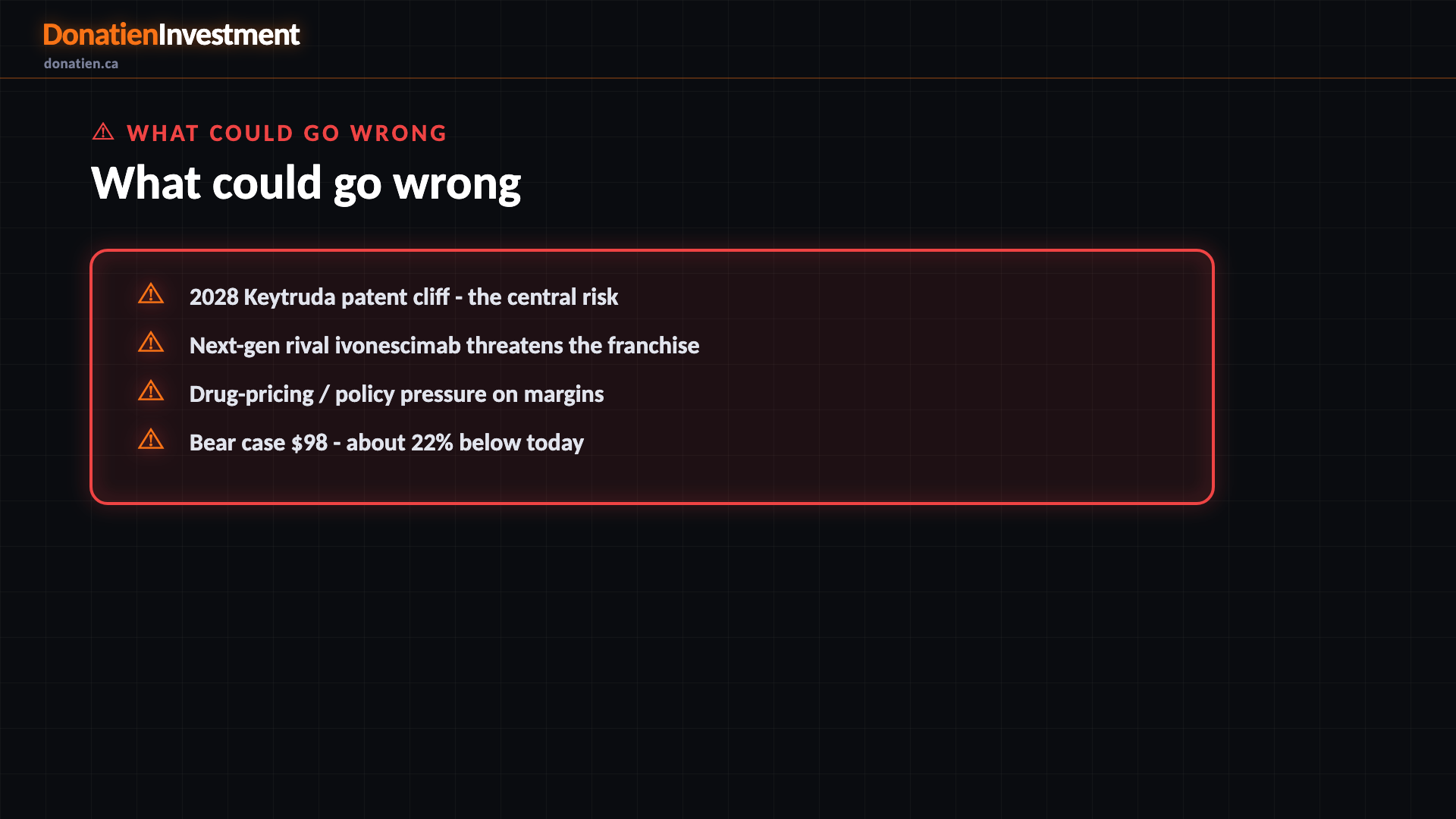

What could go wrong

2028 Keytruda patent cliff - the central risk. Next-gen rival ivonescimab threatens the franchise. Drug-pricing / policy pressure on margins. Bear case $98 - about 22% below today.

Risk vs Reward

Against the current US$125.07, the report frames a bull case at US$155 (+24%), a base case at US$138 (+10%) and a bear case at US$98 (-22%). See the full report for the probability weight behind each path.

The verdict

A cheap, cash-rich pharma major on an attractive multiple - a BUY across all horizons, with the 2028 Keytruda patent cliff the risk to watch, not a reason to avoid.

Read the full report on donatien.ca →{kind=link}

{kind=link}