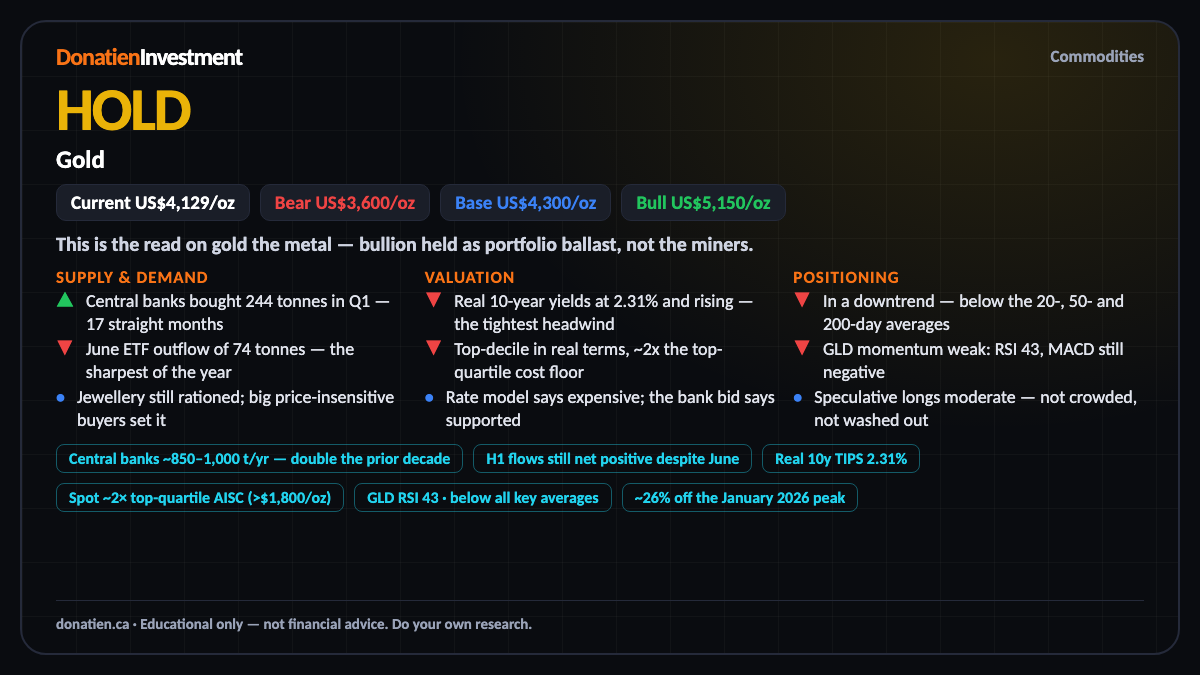

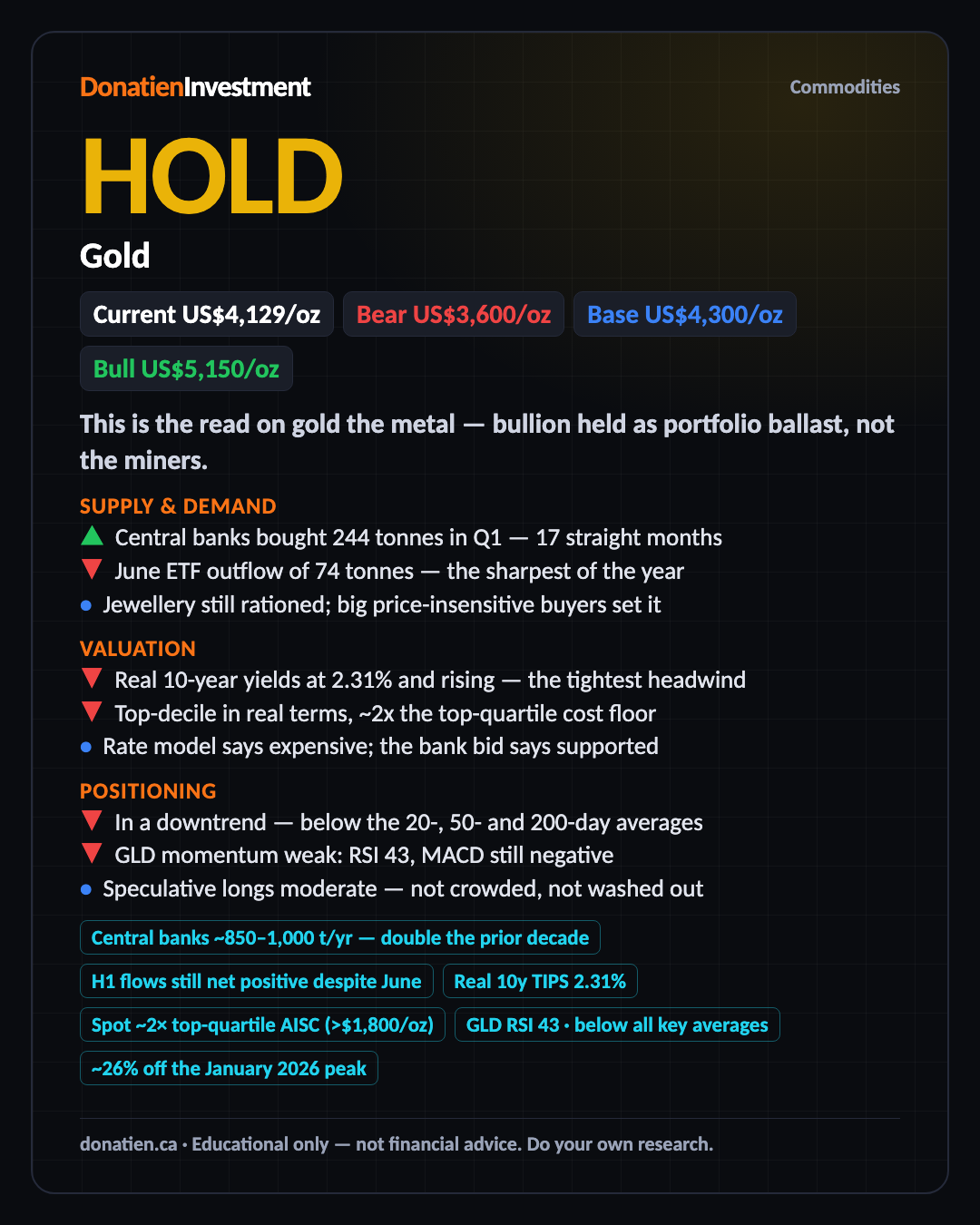

Gold HOLD

A long-term buy on the central-bank bid — but rich here, with real yields at a cycle high and the price still in a downtrend. Hold it, and add on weakness rather than chase it.

This is the read on gold the metal — bullion held as portfolio ballast, not the miners. What sets the price isn't jewellery; it's two large, price-insensitive buyers, central banks and investors. That bid is the spine of the case, and it's why a 26% fall from January's peak reads as a correction, not a top.

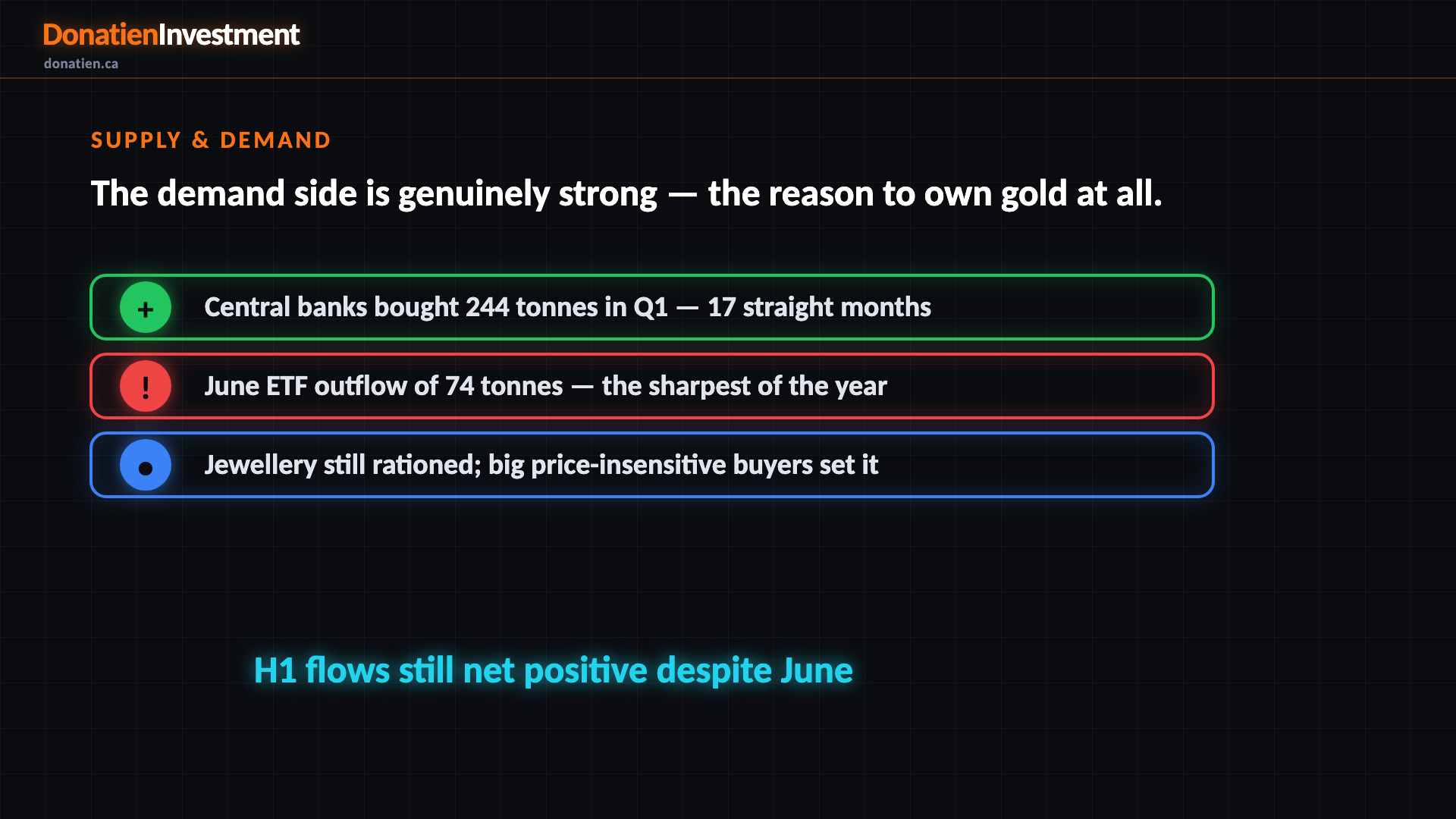

Supply & Demand

The demand side is the long-term case, and it is strong. Central banks bought 244 tonnes in the first quarter and have now added for seventeen straight months — a bid that runs on reserve policy, not price, and has roughly doubled to about a thousand tonnes a year. The soft spot is Western investors: exchange-traded funds shed 74 tonnes in June, the sharpest outflow of the year, as a hawkish Fed bit. But the half-year is still net positive, and the price-insensitive money dwarfs the wobble.

Central banks ~850–1,000 t/yr — double the prior decade · H1 flows still net positive despite June

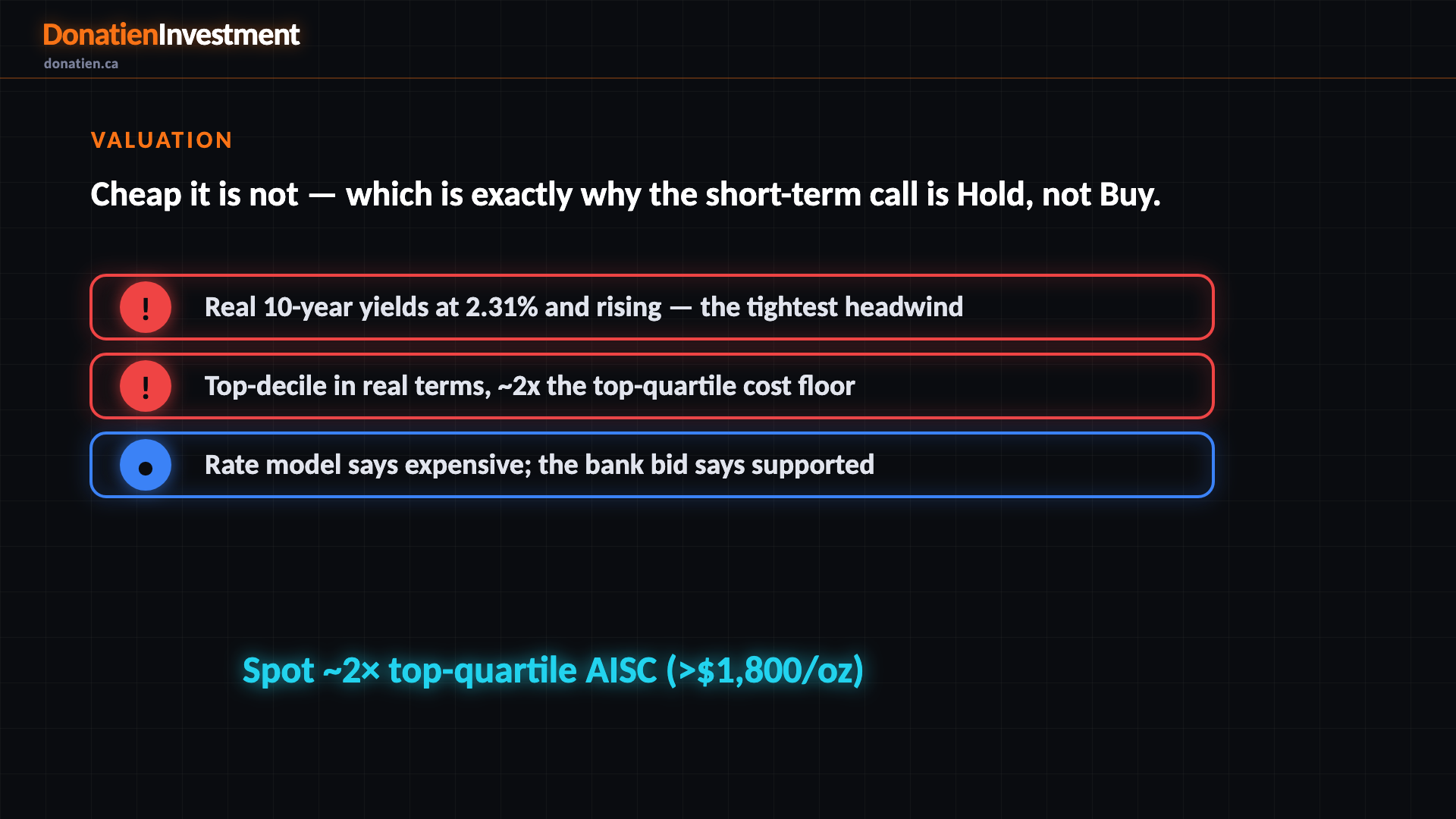

Valuation

Gold is not cheap, and that is what caps the short term. Real ten-year yields sit at 2.31% and are still rising — the single tightest inverse driver of the price. Even after a 26% correction gold is in the top decile of its history in real terms, about twice its top-quartile cash-cost floor. The rate model says expensive; the central-bank floor says supported. Both are true, which is why the honest call is hold, not buy — you wait for a better entry.

Real 10y TIPS 2.31% · Spot ~2× top-quartile AISC (>$1,800/oz)

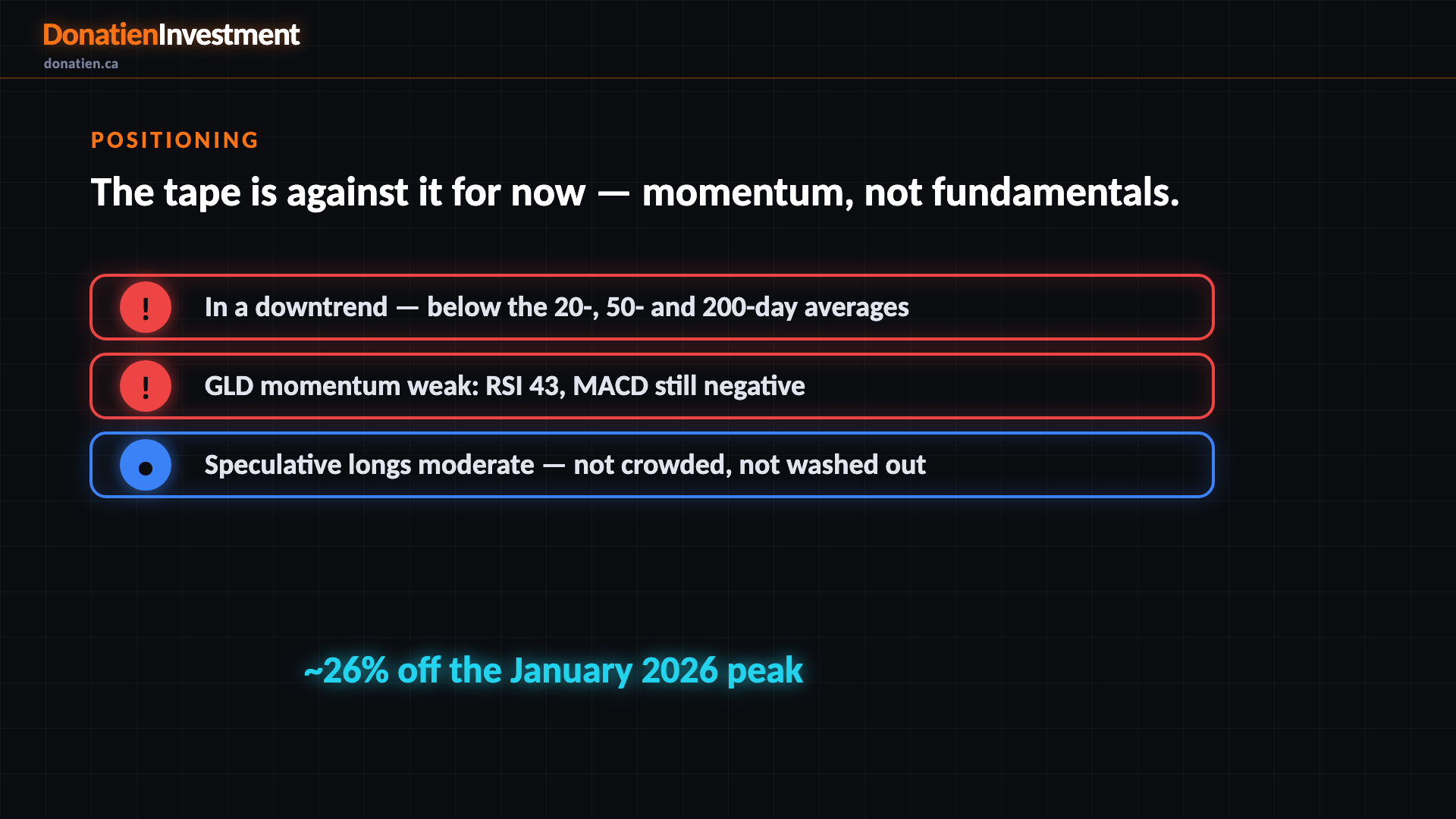

Positioning

Right now the tape is against gold. The price is below its 20-, 50- and 200-day averages, momentum is weak with the relative-strength index in the low forties and the MACD still negative, and it sits 26% below January's peak. Speculative positioning is only moderate — neither crowded nor washed out, so there's no contrarian spark either. The long-term trend is still up, just extended. None of this changes the multi-year case; it is why you wait rather than chase.

GLD RSI 43 · below all key averages · ~26% off the January 2026 peak

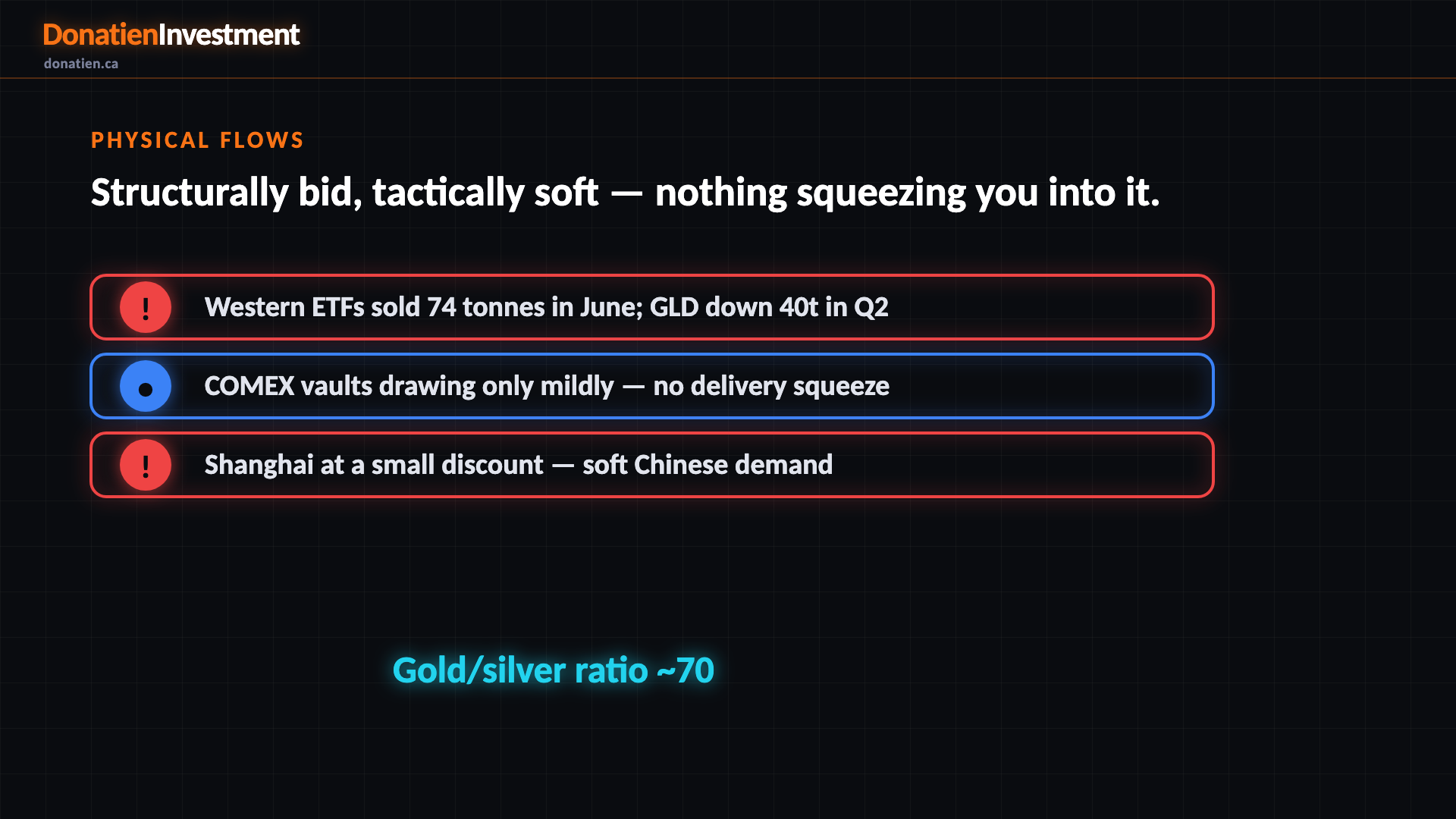

Physical flows

The plumbing tells the same story: strong structurally, soft tactically. The long bid is real — the dollar's share of reserves has slipped below 57% and gold is now the number-two reserve asset at about 27%. But the acute-tightness gauges aren't flashing. Western funds sold 74 tonnes in June, Shanghai trades at a small discount rather than a premium, and COMEX vaults are drawing only mildly. Nothing here is squeezing you into the trade — which, again, is the case for patience.

USD reserve share below 57% — gold now ~27% · Gold/silver ratio ~70

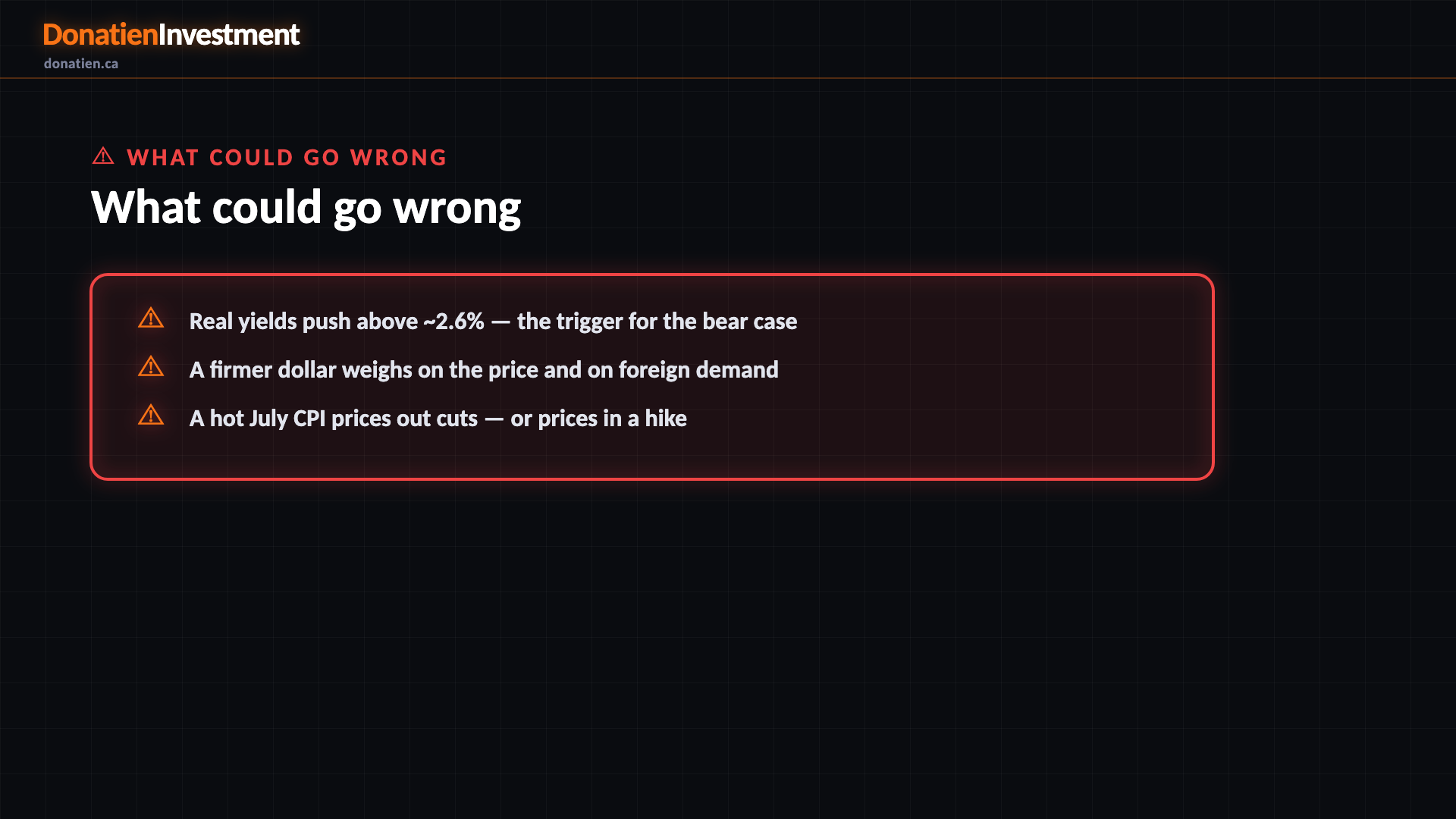

What could go wrong

The risks all run through rates and the dollar. If real ten-year yields push above about 2.6%, that triggers the bear case. A firmer dollar weighs on the price mechanically and erodes foreign demand. And the near-term swing is the July inflation print: a hot core reading keeps the Fed hawkish — pricing out cuts, or even pricing in a hike — and the downtrend has further to run. These are why the call is hold, not buy.

Risk vs Reward

The base case, and the likeliest over six to twelve months, has gold around $4,300 an ounce — digesting the correction in a range with the central-bank bid as the floor. The bull case is about $5,150 if real yields fall, the Fed pivots, or a shock hits. The bear case is around $3,600 if a hot inflation print keeps rates higher for longer and the last Western longs capitulate.

The verdict

Short term, hold — right asset, wrong moment to chase. Medium term, hold and add on weakness. Long term it's a buy: the central-bank and de-dollarisation bid dominates over years, and that is what makes gold worth holding as ballast. The bear case owns the next few months; the bull case owns the next few years. Drivers and regime only amplify that — rich valuation and a broken tape set the near-term call.

Read the full report on donatien.ca →{kind=link}

{kind=link}