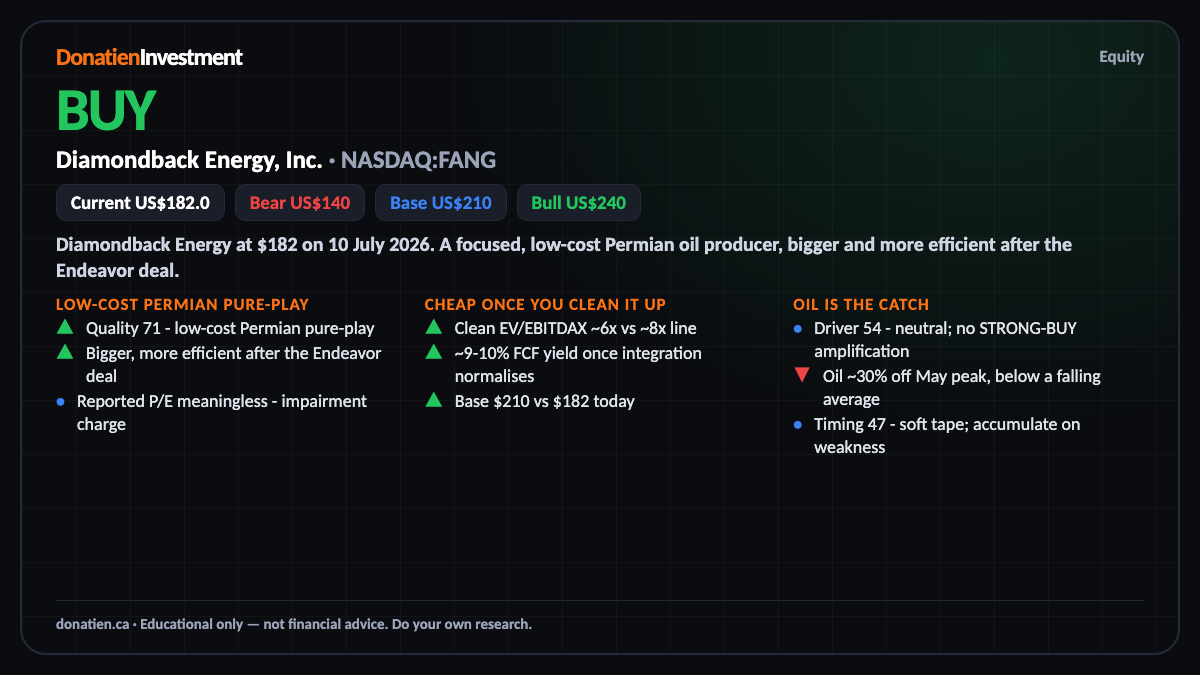

Diamondback Energy, Inc. (NASDAQ:FANG) BUY

A low-cost Permian pure-play that's genuinely cheap on cash flow once you strip out an impairment - held at BUY, not STRONG BUY, while the oil price trend is down.

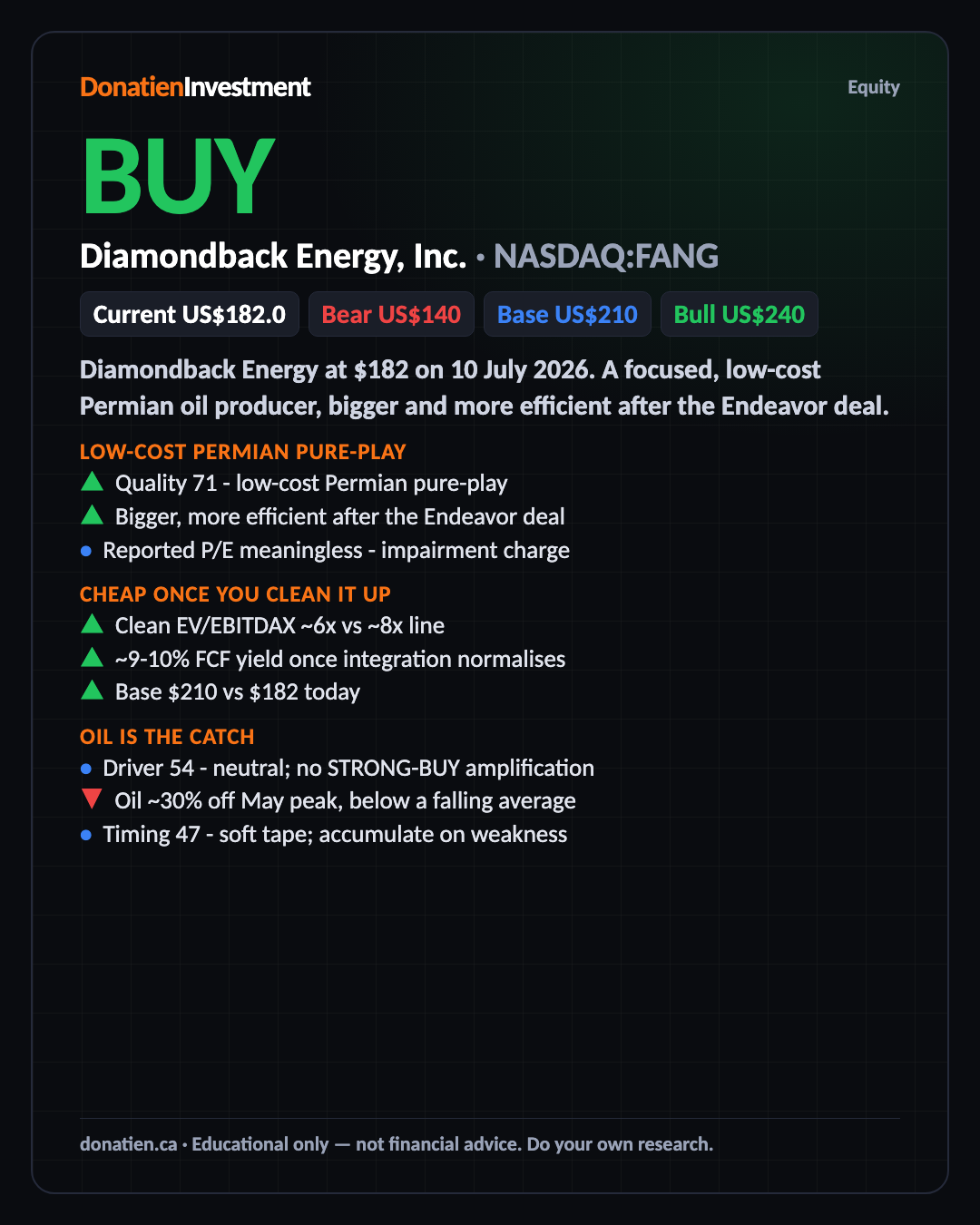

Diamondback Energy at $182 on 10 July 2026. A focused, low-cost Permian oil producer, bigger and more efficient after the Endeavor deal. The report reads BUY across all three horizons but stops short of STRONG BUY - because oil, the thing that drives it, is falling.

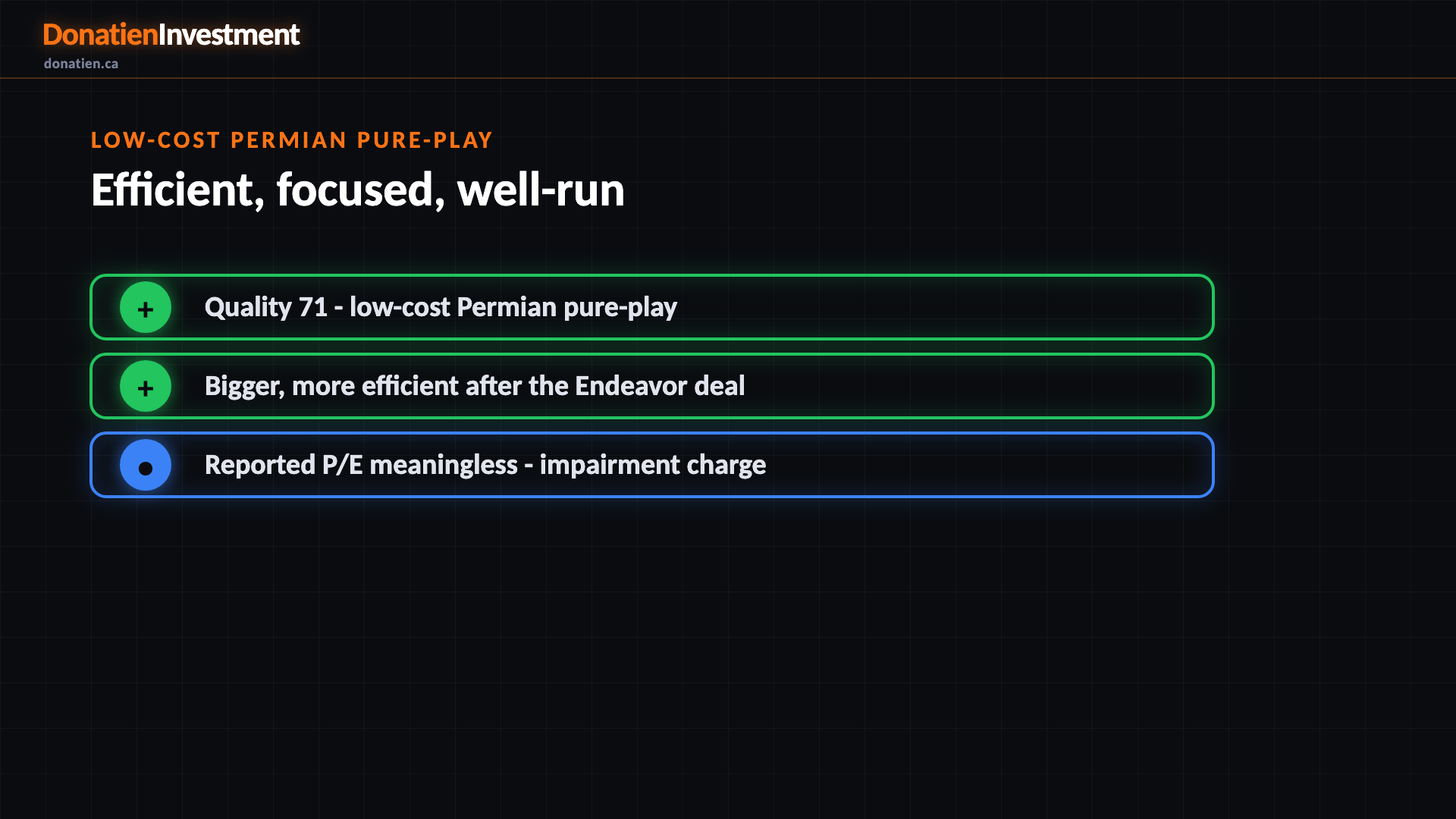

Low-cost Permian pure-play

Quality scores 71. Diamondback is one of the lowest-cost operators in the Permian basin, and the Endeavor acquisition made it bigger and more efficient. There's a wrinkle worth knowing: the reported profit is crushed by a large one-off impairment charge, so the headline price-to-earnings of over two hundred times is meaningless. Look through it and the underlying business is healthy and cash-generative.

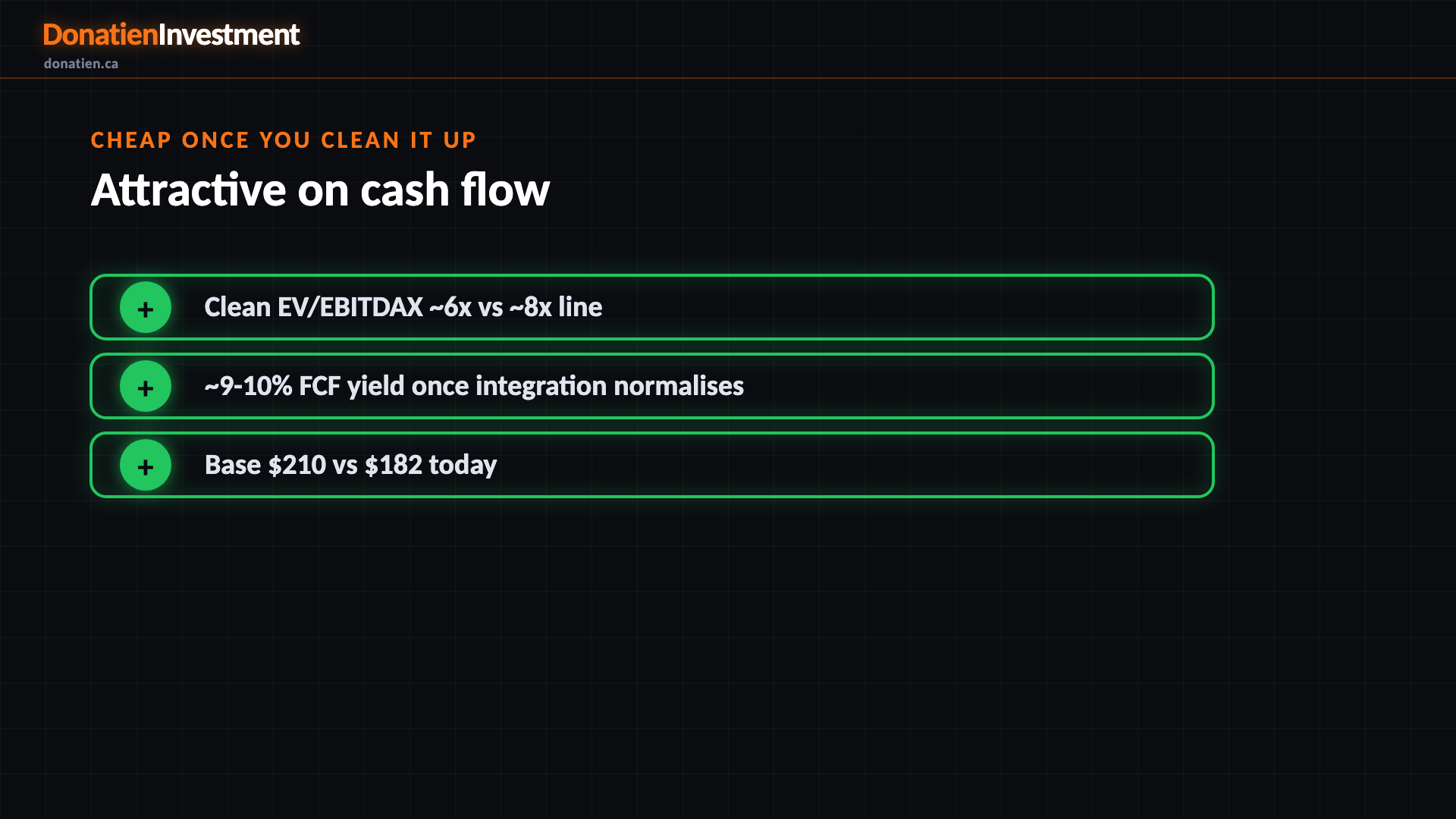

Cheap once you clean it up

Valuation scores 68. Ignore the distorted earnings multiple and look at cash: enterprise value to cash flow is around six times against an eight-times sector line, and the free-cash-flow yield is roughly nine to ten per cent once the integration spending normalises. The base case is two hundred and ten against a hundred and eighty-two today. So the equity is genuinely cheap - the argument is entirely about where oil goes next.

Oil is the catch

Driver scores 54 - neutral, not a tailwind. Oil sits at a workable level versus Diamondback's low breakeven, but the price trend is clearly down: crude is off around thirty per cent from its May peak and below a falling average. Our overlay treats that live downtrend as a real near-term risk and switches off the short-term amplification, which is why this is a plain BUY. Timing is soft too, at forty-seven - so accumulate on weakness rather than chase.

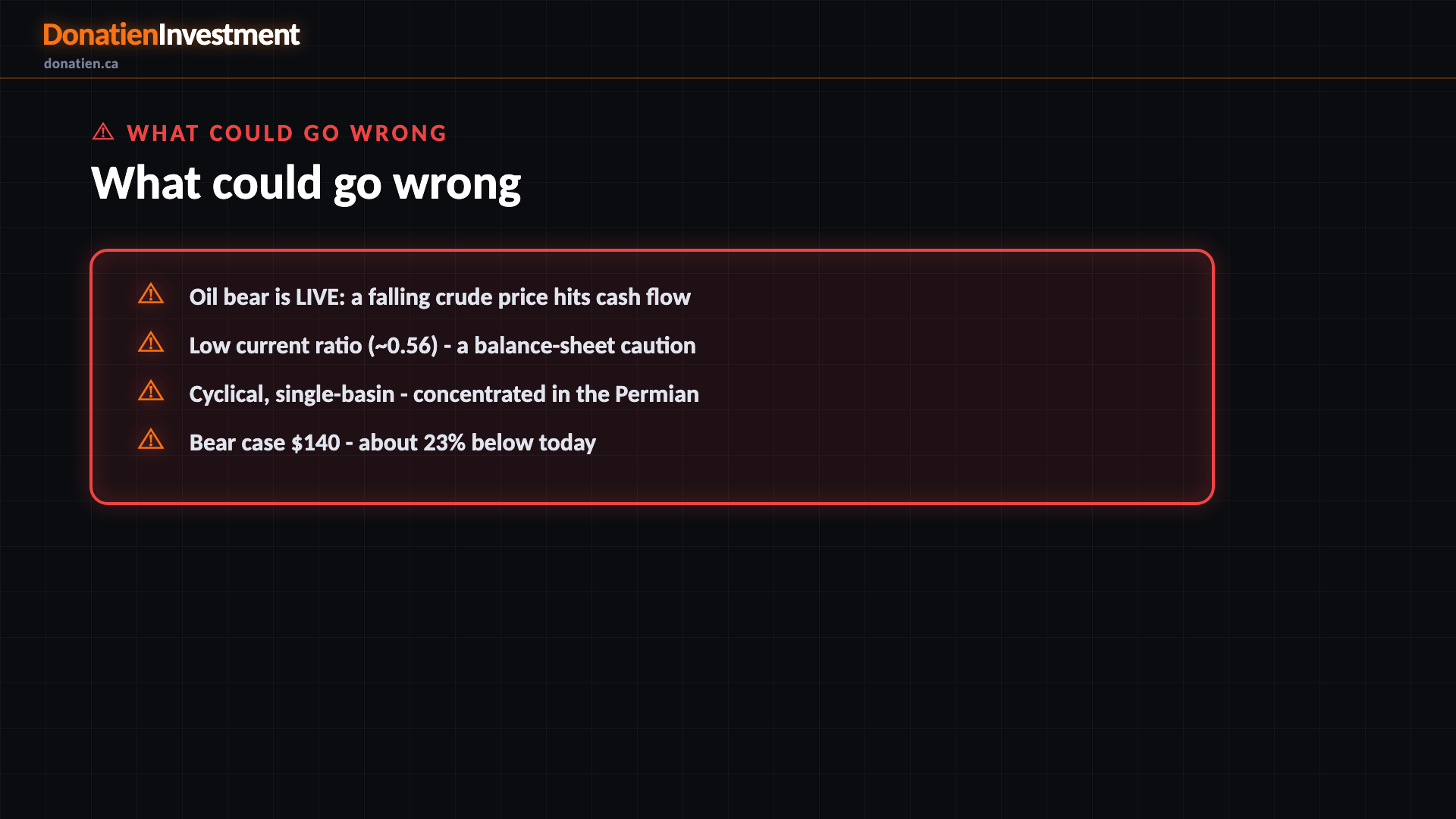

What could go wrong

Oil bear is LIVE: a falling crude price hits cash flow. Low current ratio (~0.56) - a balance-sheet caution. Cyclical, single-basin - concentrated in the Permian. Bear case $140 - about 23% below today.

Risk vs Reward

Against the current US$182.0, the report frames a bull case at US$240 (+32%), a base case at US$210 (+15%) and a bear case at US$140 (-23%). See the full report for the probability weight behind each path.

The verdict

A low-cost Permian pure-play that's genuinely cheap on cash flow once you strip out an impairment - held at BUY, not STRONG BUY, while the oil price trend is down.

Read the full report on donatien.ca →{kind=link}

{kind=link}