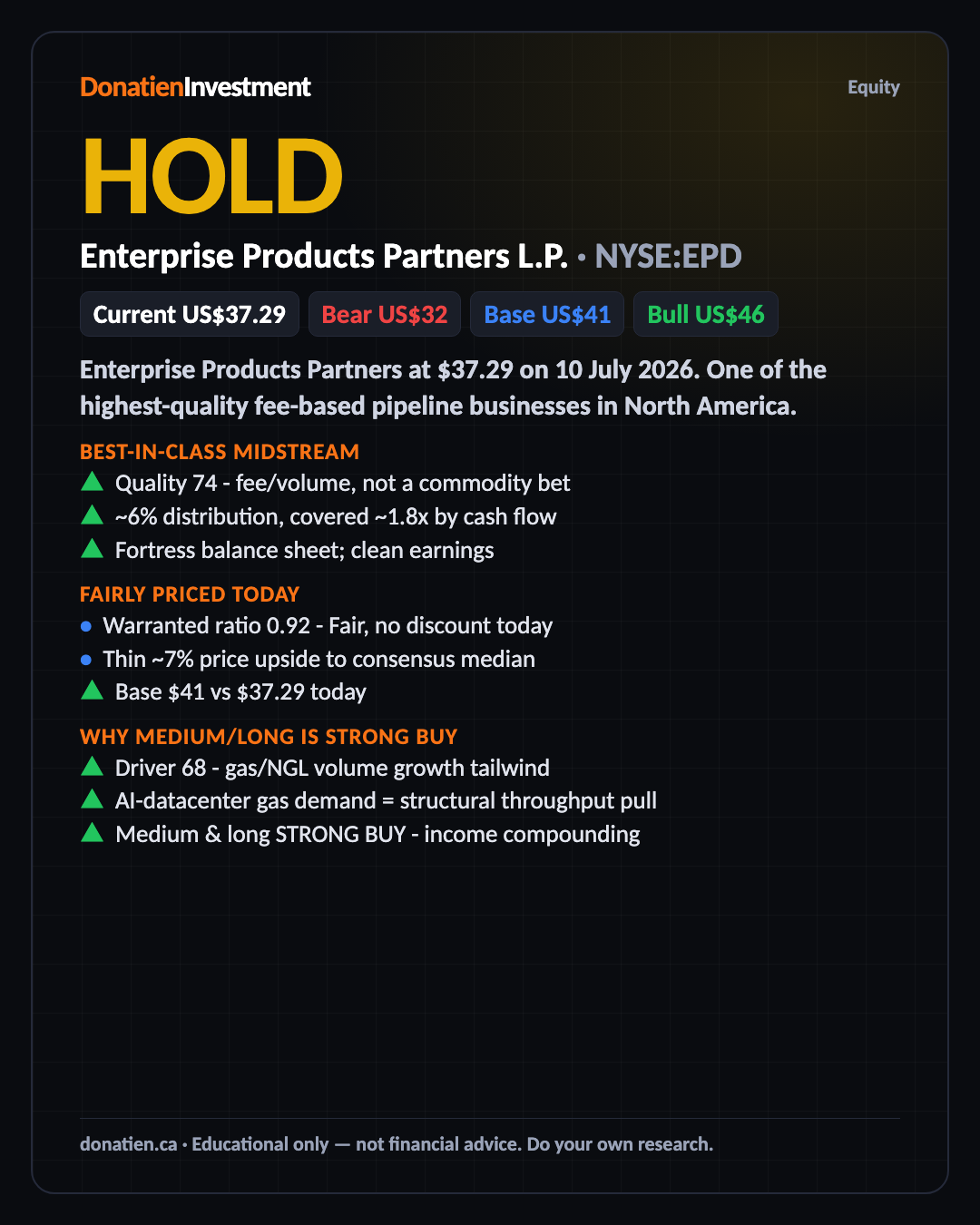

Enterprise Products Partners L.P. (NYSE:EPD) HOLD

A best-in-class midstream income compounder - fairly priced today, so a hold for now; the medium- and long-term call is STRONG BUY for the well-covered ~6% distribution and steady growth.

Enterprise Products Partners at $37.29 on 10 July 2026. One of the highest-quality fee-based pipeline businesses in North America. The short-term signal is HOLD - the units are fairly valued and the near-term tape is soft - but medium and long term the report reads STRONG BUY: this is an income compounder, not a price-appreciation story.

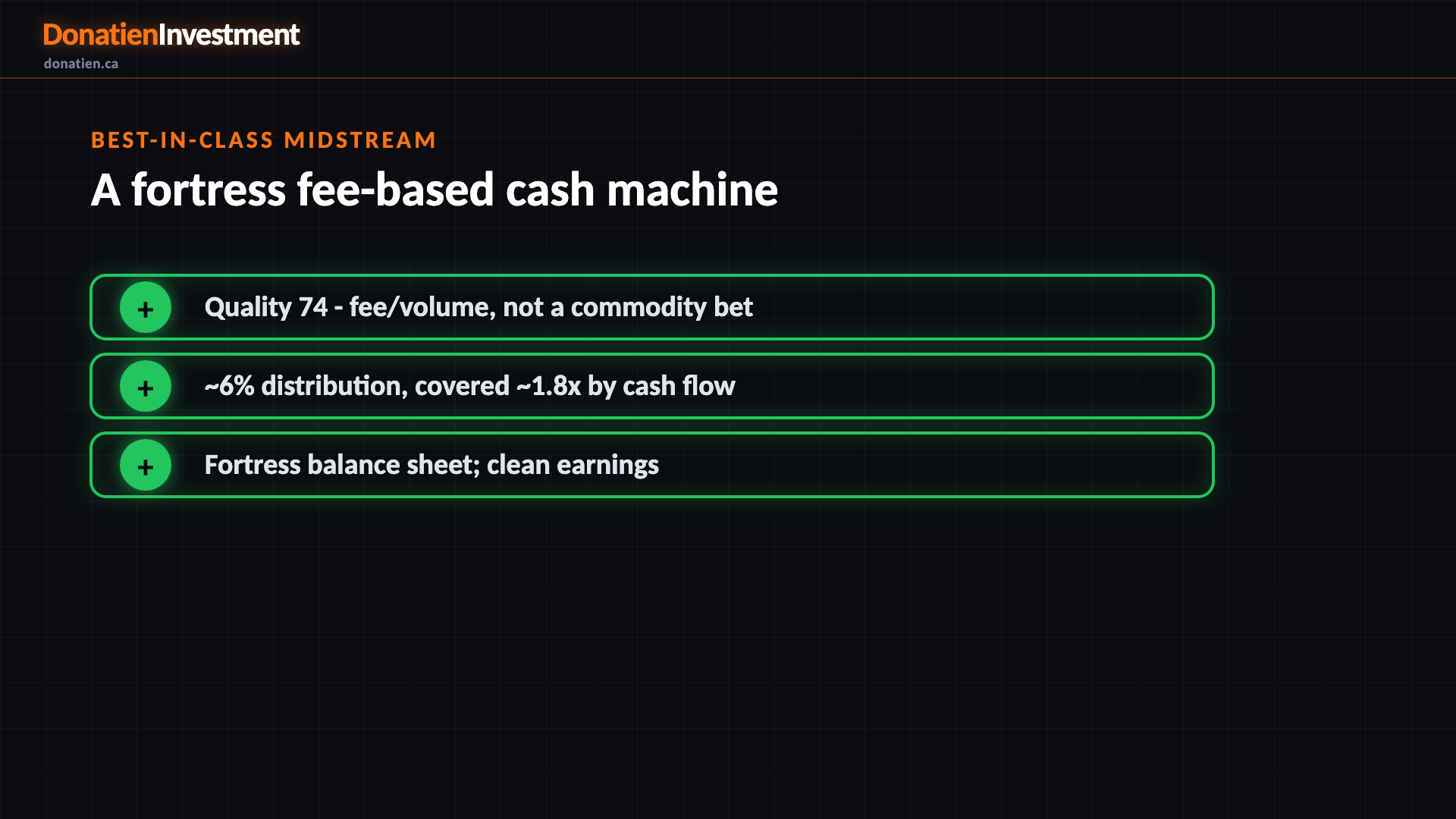

Best-in-class midstream

Quality scores 74. Enterprise is a fee-and-volume pipeline network, not a commodity bet - it gets paid to move hydrocarbons regardless of the price. The balance sheet is among the strongest in the sector, the distribution is covered about 1.8 times by cash flow, and it yields roughly six per cent. Earnings are clean, so the multiple is genuine. This is the kind of holding you own for the cheque it pays you, quarter after quarter.

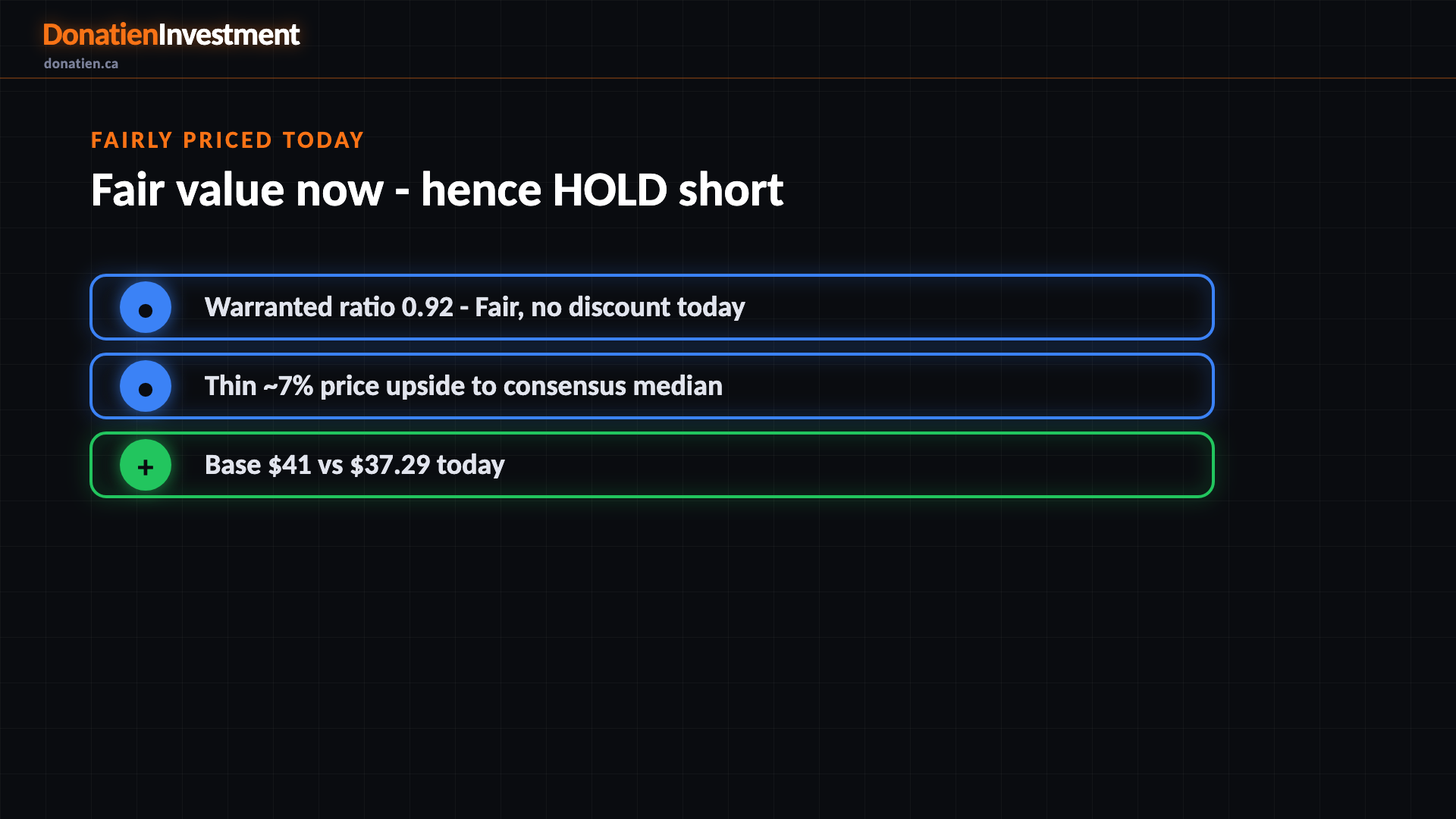

Fairly priced today

Valuation scores 63 - Fair. Against the rate-and-growth warranted multiple it trades at about 0.92, just inside fair value, and on its own five-year cash-flow range it sits in the upper third but nowhere near extreme. Consensus price upside is thin, around seven per cent to the median. That is exactly why the short-term call is HOLD: you are not getting a discount today. The return here is the growing distribution, not a quick re-rating.

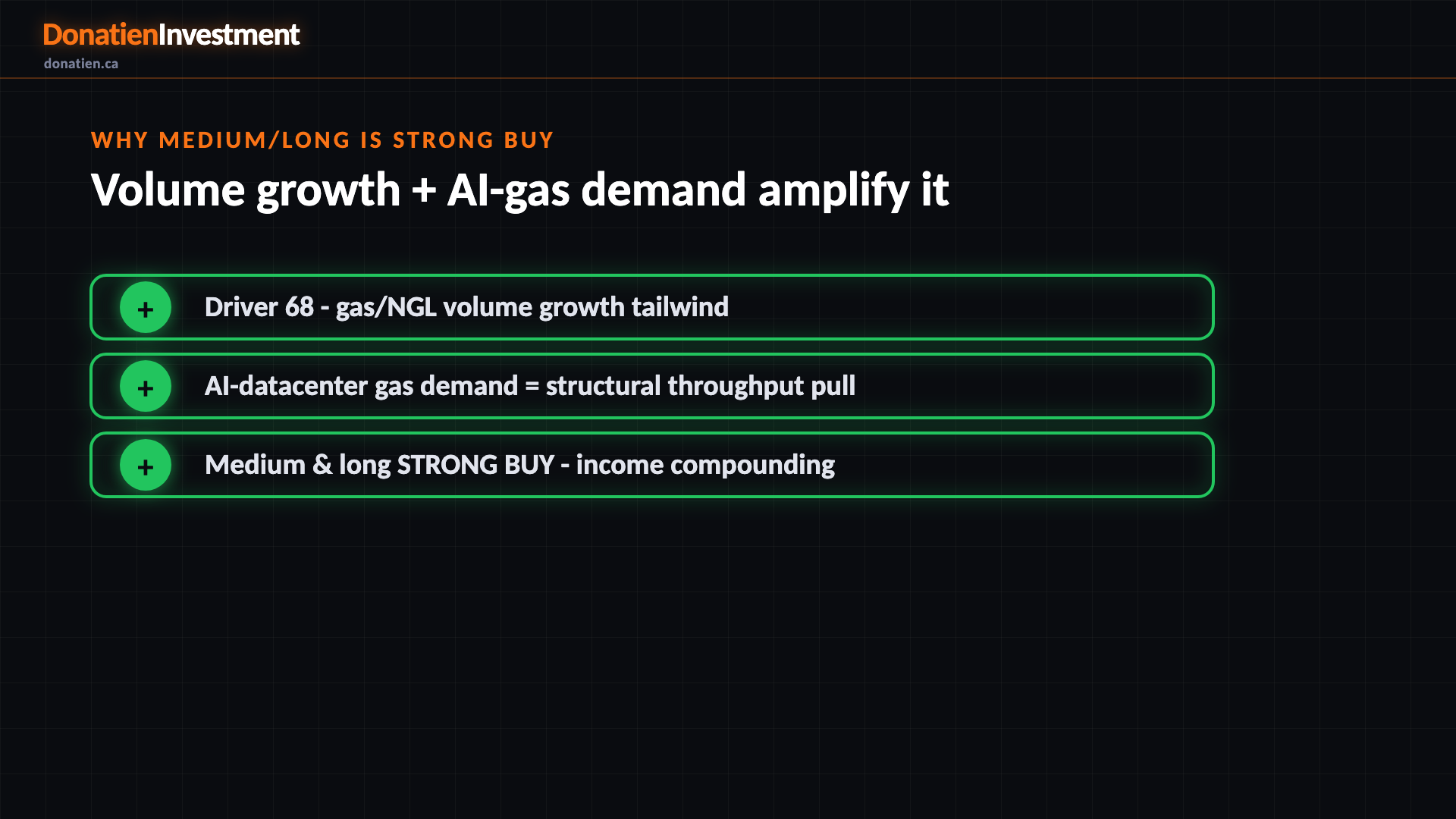

Why medium/long is STRONG BUY

Driver scores 68 - a genuine tailwind. Natural-gas and natural-gas-liquids volumes are growing, and the surge in AI-data-centre power demand is a structural pull on gas throughput that Enterprise is positioned to carry. With a supportive economy behind it and the valuation not in stretched territory, that tailwind is enough to amplify the medium- and long-term signal to STRONG BUY. Be clear about what that means: a compounding income return, not a promise of a soaring share price.

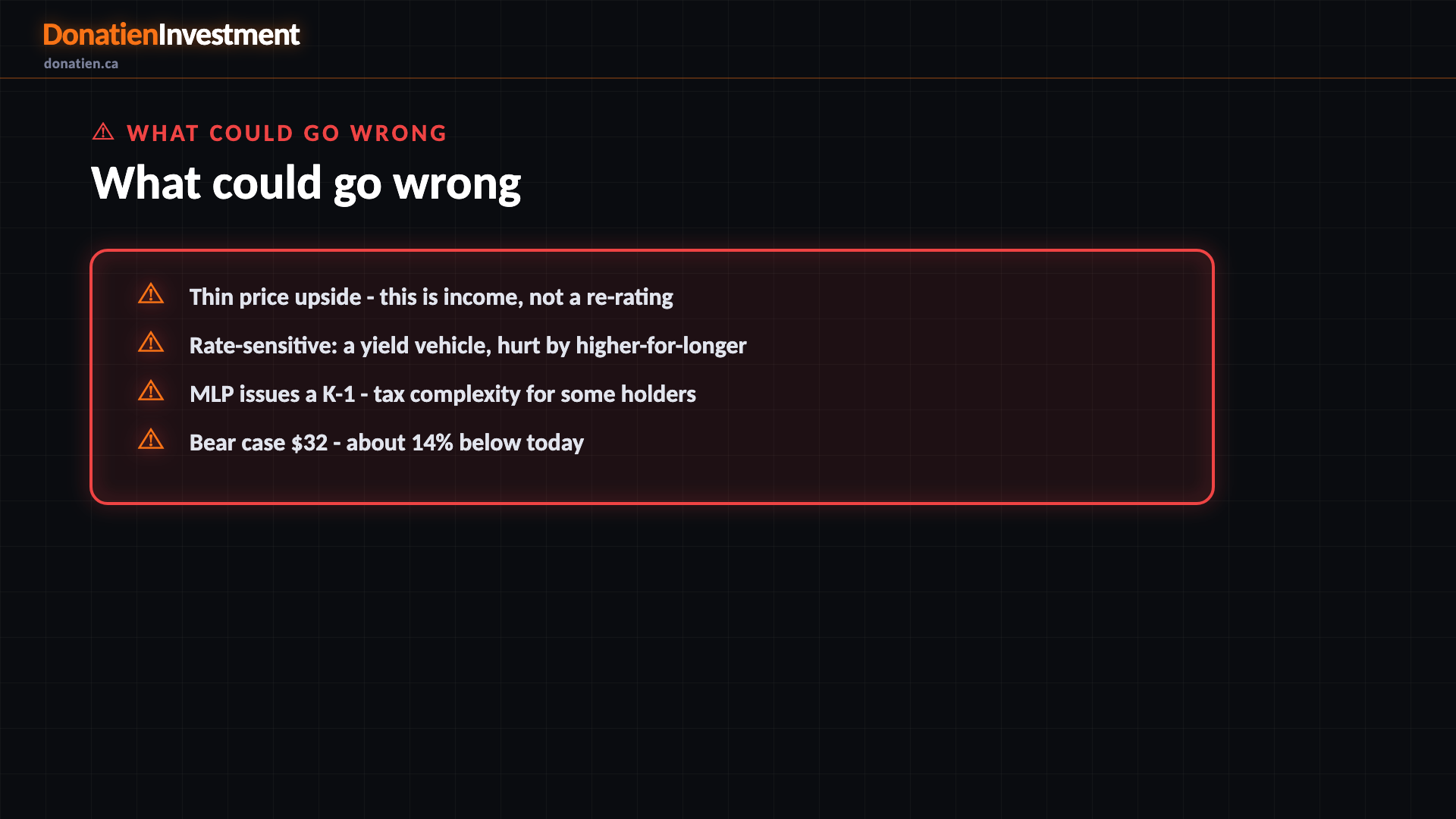

What could go wrong

Thin price upside - this is income, not a re-rating. Rate-sensitive: a yield vehicle, hurt by higher-for-longer. MLP issues a K-1 - tax complexity for some holders. Bear case $32 - about 14% below today.

Risk vs Reward

Against the current US$37.29, the report frames a bull case at US$46 (+23%), a base case at US$41 (+10%) and a bear case at US$32 (-14%). See the full report for the probability weight behind each path.

The verdict

A best-in-class midstream income compounder - fairly priced today, so a hold for now; the medium- and long-term call is STRONG BUY for the well-covered ~6% distribution and steady growth.

Read the full report on donatien.ca →{kind=link}

{kind=link}