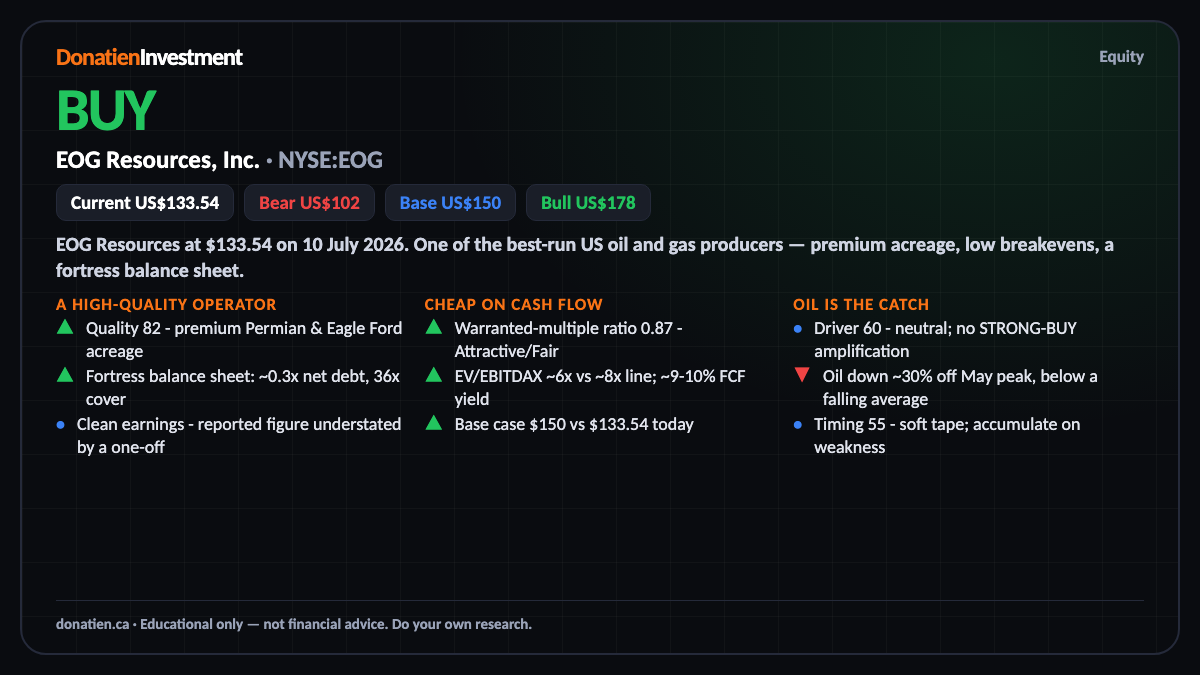

EOG Resources, Inc. (NYSE:EOG) BUY

A top-tier, low-cost shale operator on a cheap cash-flow multiple — but held at plain BUY, not STRONG BUY, while the oil tape is falling.

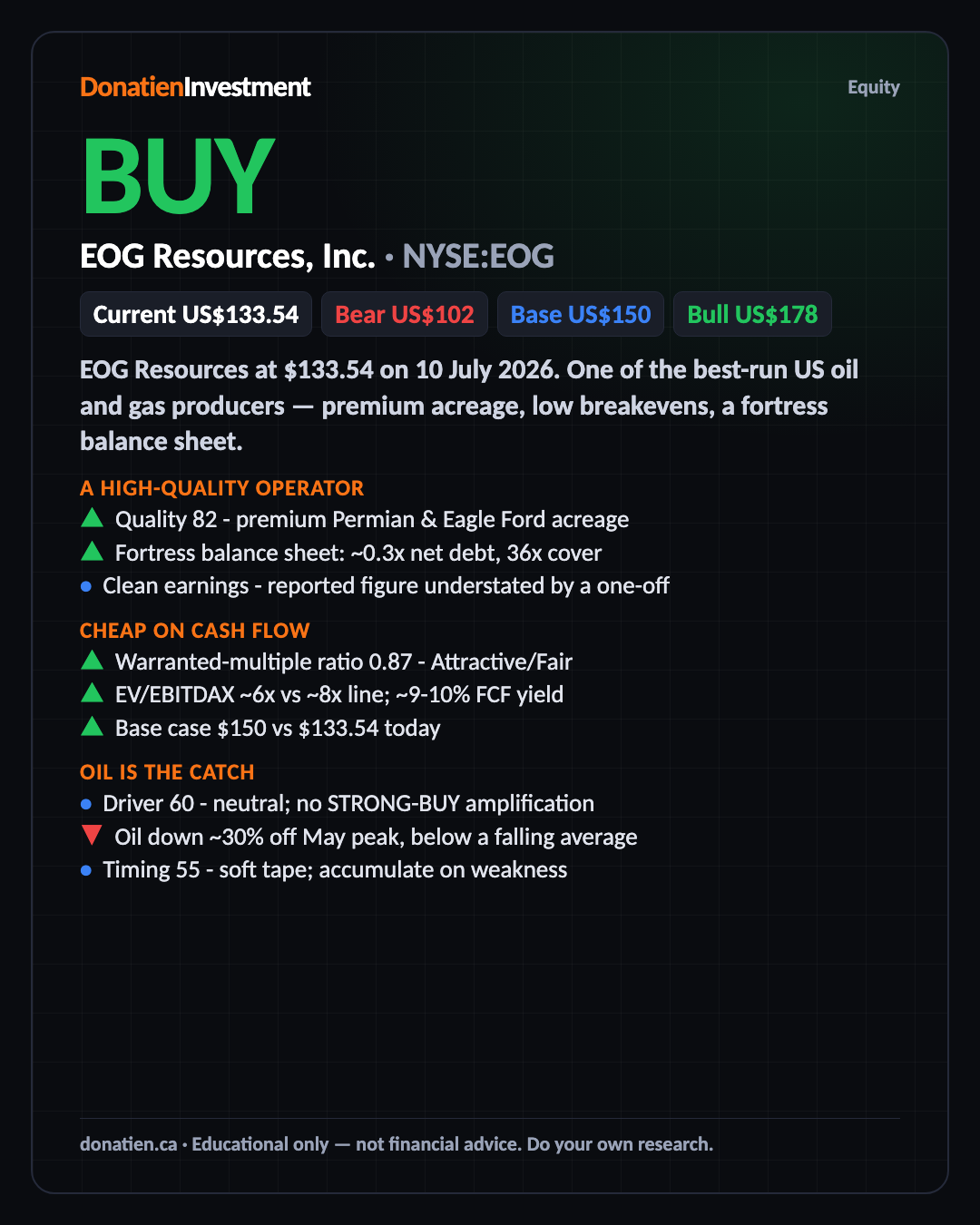

EOG Resources at $133.54 on 10 July 2026. One of the best-run US oil and gas producers — premium acreage, low breakevens, a fortress balance sheet. The report reads BUY across all three horizons, but deliberately stops short of STRONG BUY because the thing that drives EOG — the oil price — is in a downtrend right now.

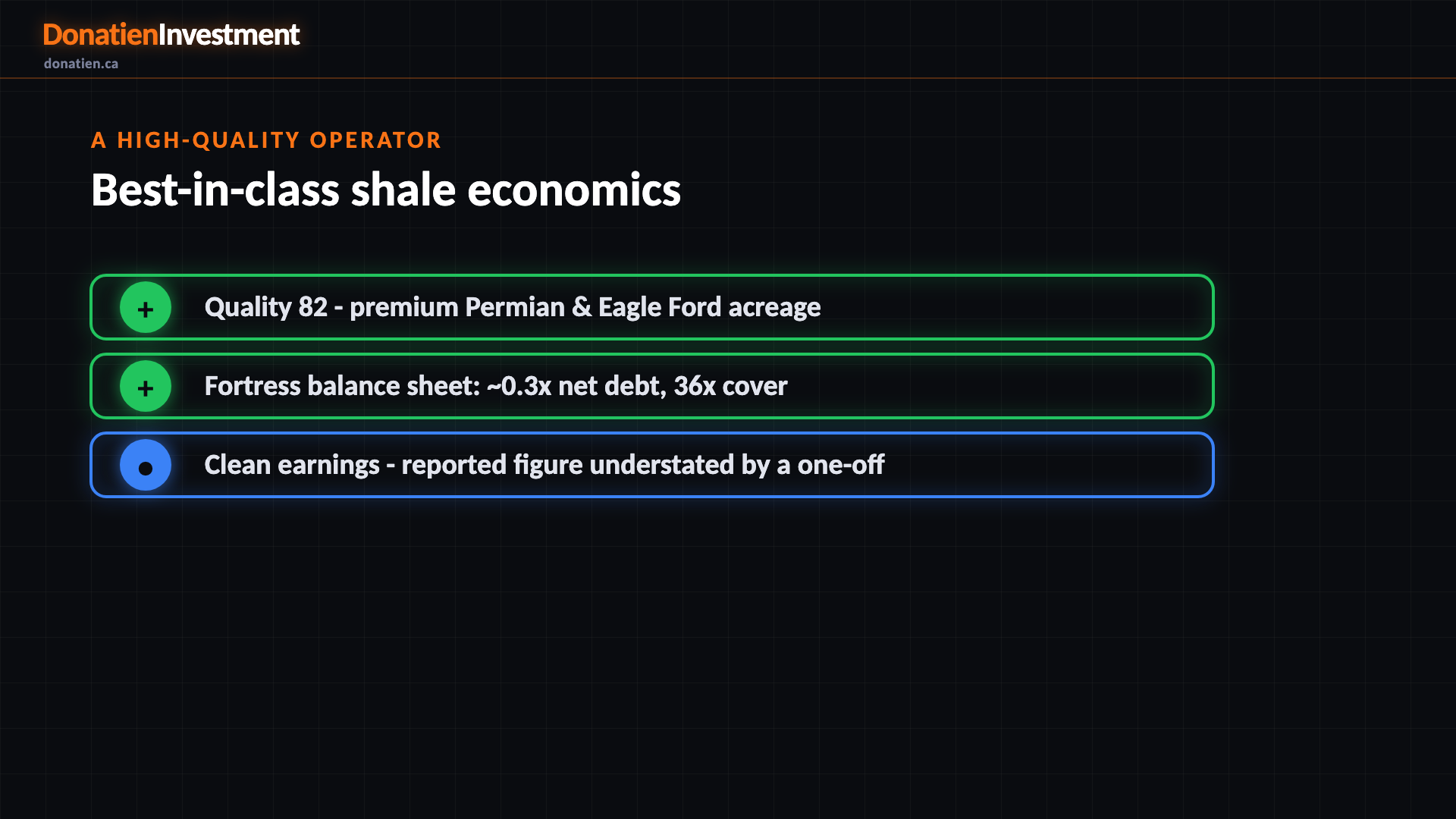

A high-quality operator

Quality scores 82 — near the top of the sector. EOG runs premium, low-cost acreage in the Permian and Eagle Ford, converts it into real free cash flow, and carries almost no net debt with interest cover above thirty times. Reported earnings were actually understated by a one-off charge, so the clean picture is better than the headline. This is the kind of balance sheet that survives a low-oil year without cutting the dividend — which is exactly what you want in a cyclical.

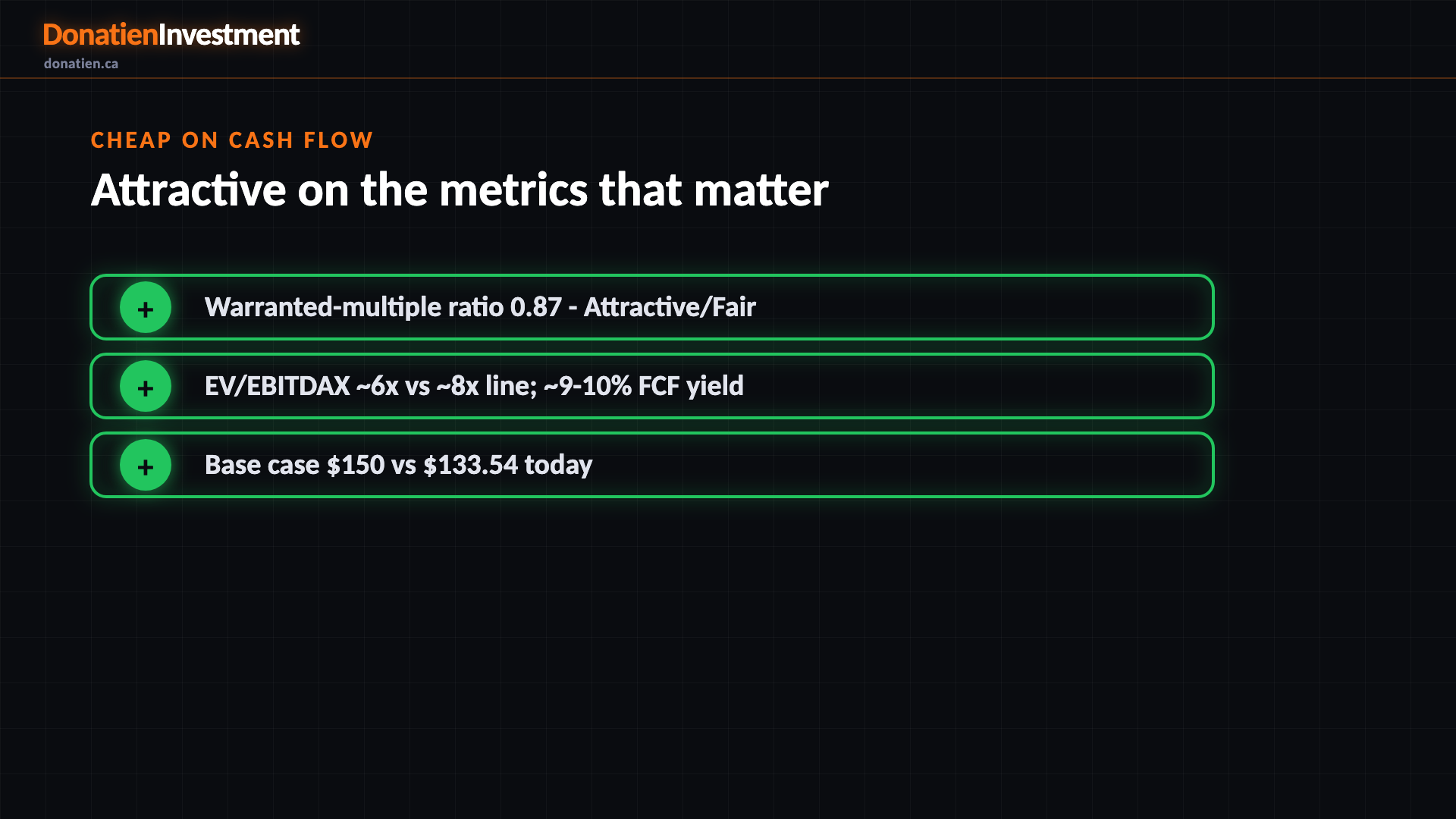

Cheap on cash flow

Valuation scores 74. On the earnings multiple the framework anchors to — the rate-and-growth warranted multiple — EOG trades at about 0.87 of fair, in the Attractive-to-Fair band. On enterprise value to cash flow it is around six times against an eight-times sector line, and the free-cash-flow yield sits near nine to ten percent. Analysts see mid-teens upside to consensus. So you are not overpaying; the debate is about the commodity, not the price of the equity.

Oil is the catch

Driver scores 60 — neutral, not a tailwind — and that is the whole reason this is a plain BUY. Oil sits at a decent level versus EOG's mid-forties breakeven, but the price trend is down: crude is off nearly thirty percent from its May peak and below a falling average, with the macro oil signal soft in the near term. A four-day bounce on Middle-East headlines is a risk premium, not a trend change. So the short-term amplification is switched off, and the oil bear is a live risk today, not a distant tail.

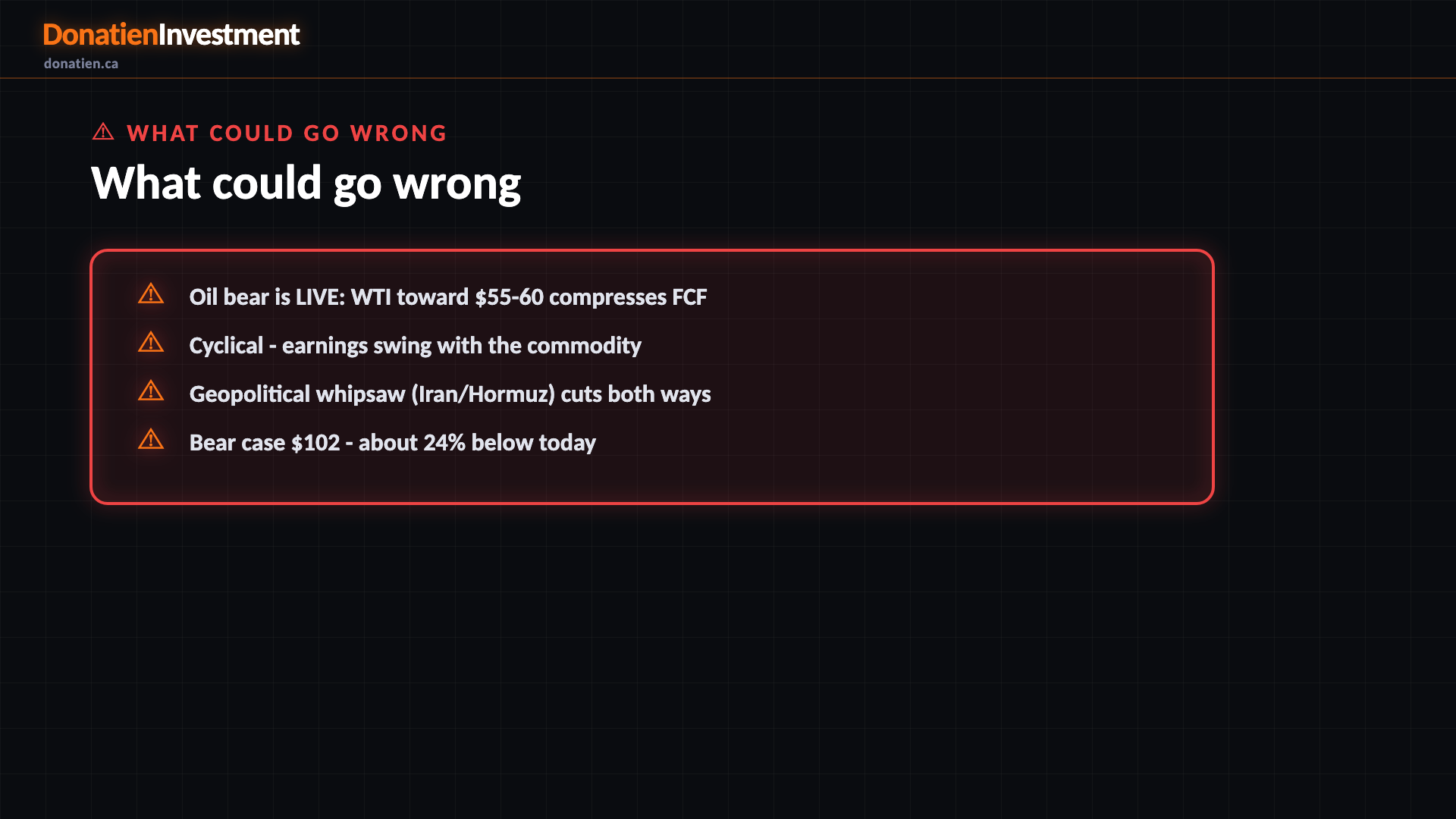

What could go wrong

Oil bear is LIVE: WTI toward $55-60 compresses FCF. Cyclical - earnings swing with the commodity. Geopolitical whipsaw (Iran/Hormuz) cuts both ways. Bear case $102 - about 24% below today.

Risk vs Reward

Against the current US$133.54, the report frames a bull case at US$178 (+33%), a base case at US$150 (+12%) and a bear case at US$102 (-24%). See the full report for the probability weight behind each path.

The verdict

A top-tier, low-cost shale operator on a cheap cash-flow multiple — but held at plain BUY, not STRONG BUY, while the oil tape is falling.

Read the full report on donatien.ca →{kind=link}

{kind=link}