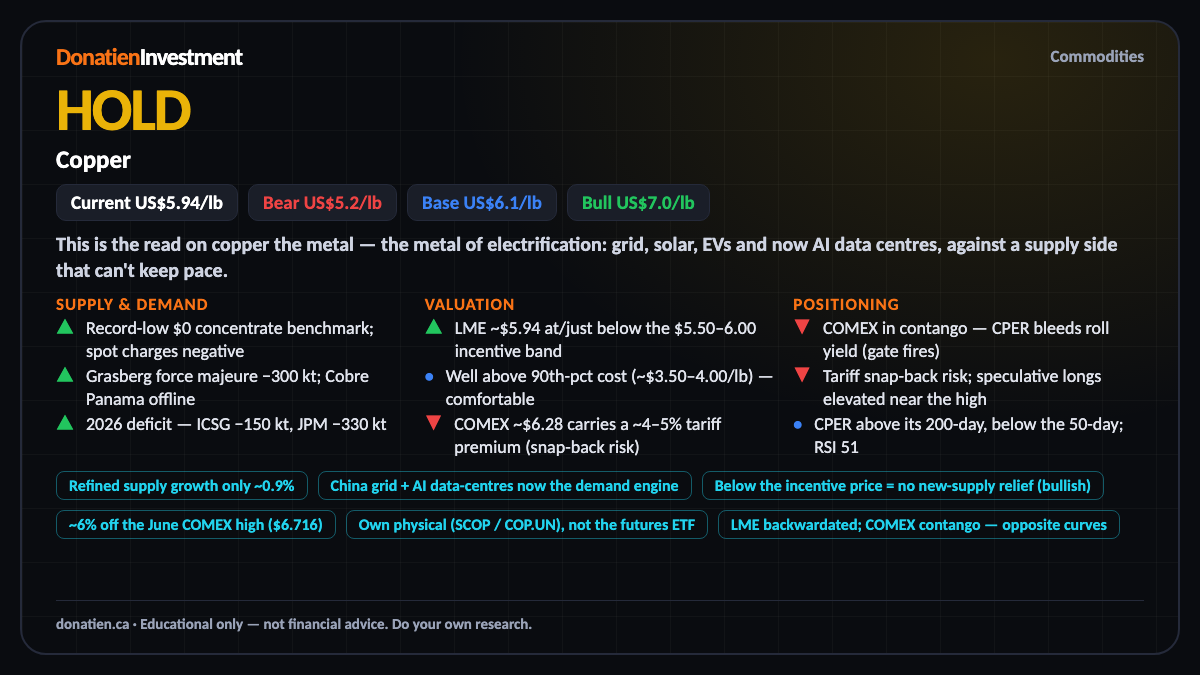

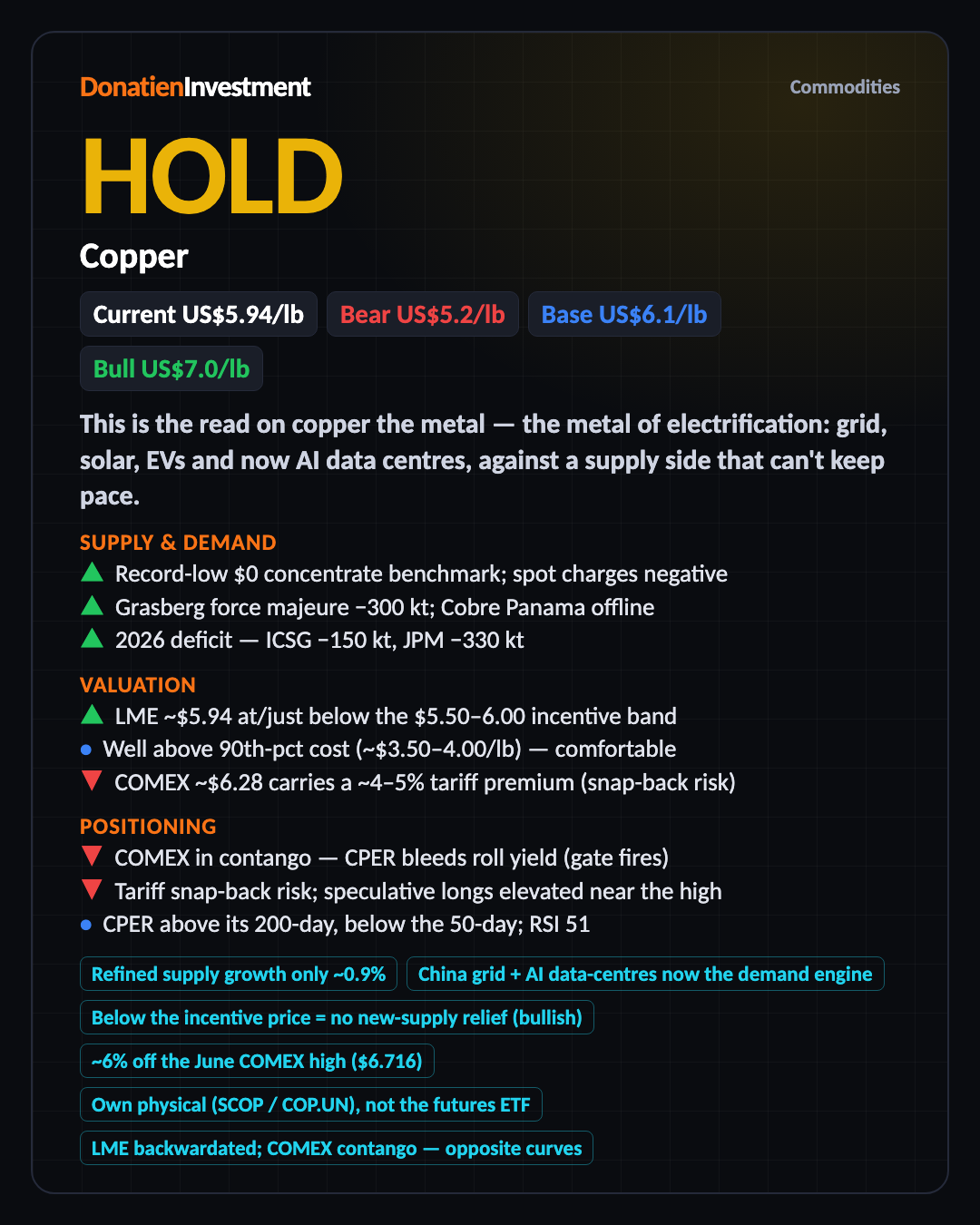

Copper HOLD

The right structural metal on a genuine deficit — but downgraded from strong buy: US futures flipped into contango, so the ETF now bleeds roll yield, the tariff-inflated price can snap back, and a pro-cyclical metal faces a growth headwind. Hold short; own the long case in physical, not CPER.

This is the read on copper the metal — the metal of electrification: grid, solar, EVs and now AI data centres, against a supply side that can't keep pace. It's pro-cyclical, so it wants a strong economy. The twist this update is a US tariff that has split the American price from the global one — and turned the popular ETF into a leaky vehicle.

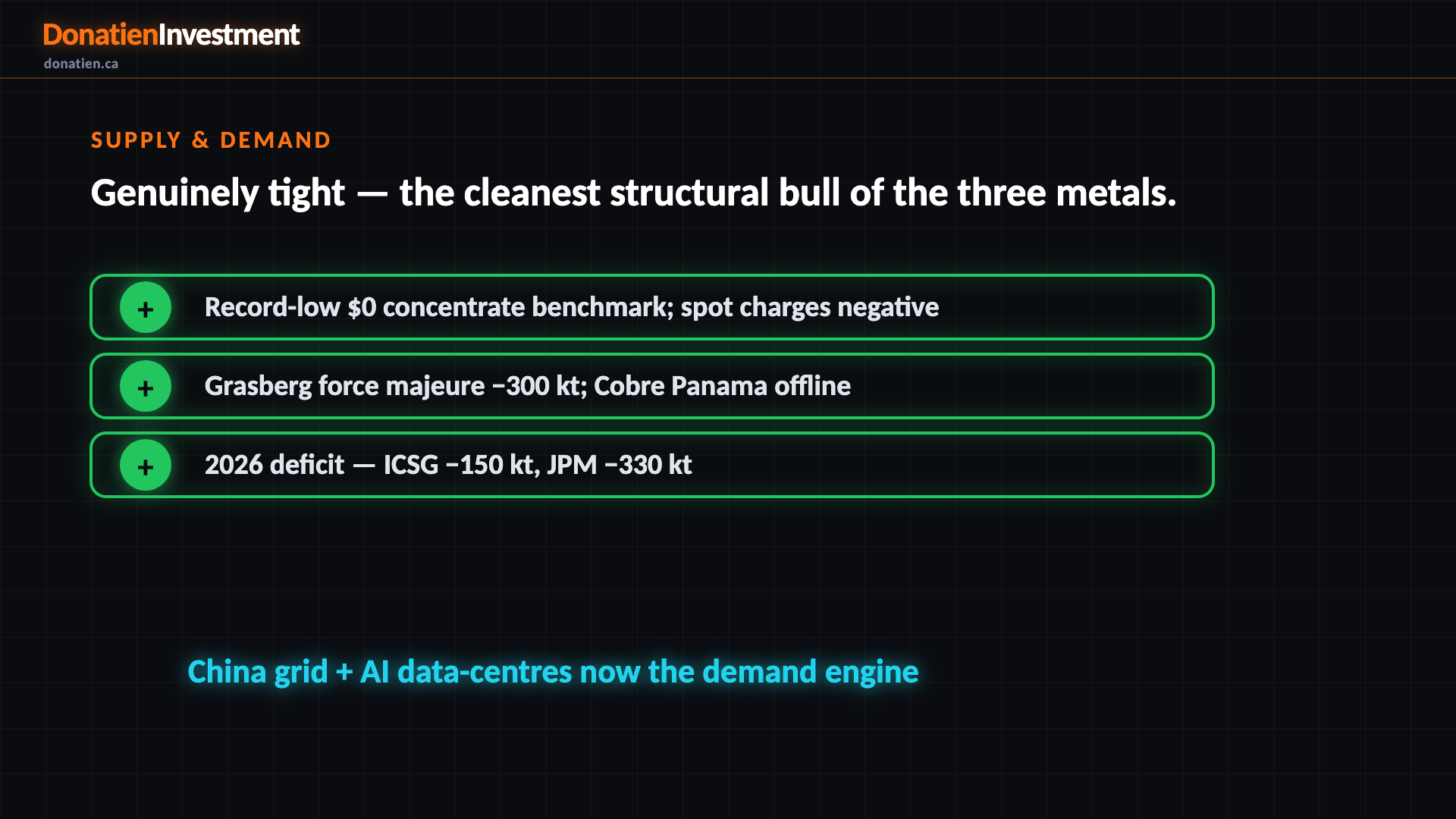

Supply & Demand

On the fundamentals copper is genuinely tight — the cleanest of the three. The annual charge to process concentrate settled at zero, a record low, and spot charges have gone negative, meaning smelters are paying miners for ore. Two big mines are impaired: Grasberg is under force majeure, down about three hundred thousand tonnes, and Cobre Panama is still offline. Refined supply is growing under one percent. Against that, China's grid build and AI data centres have taken over as the demand engine. The result is a real deficit.

Refined supply growth only ~0.9% · China grid + AI data-centres now the demand engine

Valuation

Valuation is judged on the global price, and there copper is fair. The London three-month price, about five ninety-four a pound, sits right at the low end of the five-fifty-to-six-dollar band new mines need to break ground — high enough to keep existing mines running, not yet high enough to unlock the new supply the deficit demands. That gap is the structural bull. It's comfortably above the ninetieth-percentile cost floor. The catch is the American price, around six twenty-eight, which carries a tariff premium that can unwind.

Below the incentive price = no new-supply relief (bullish) · ~6% off the June COMEX high ($6.716)

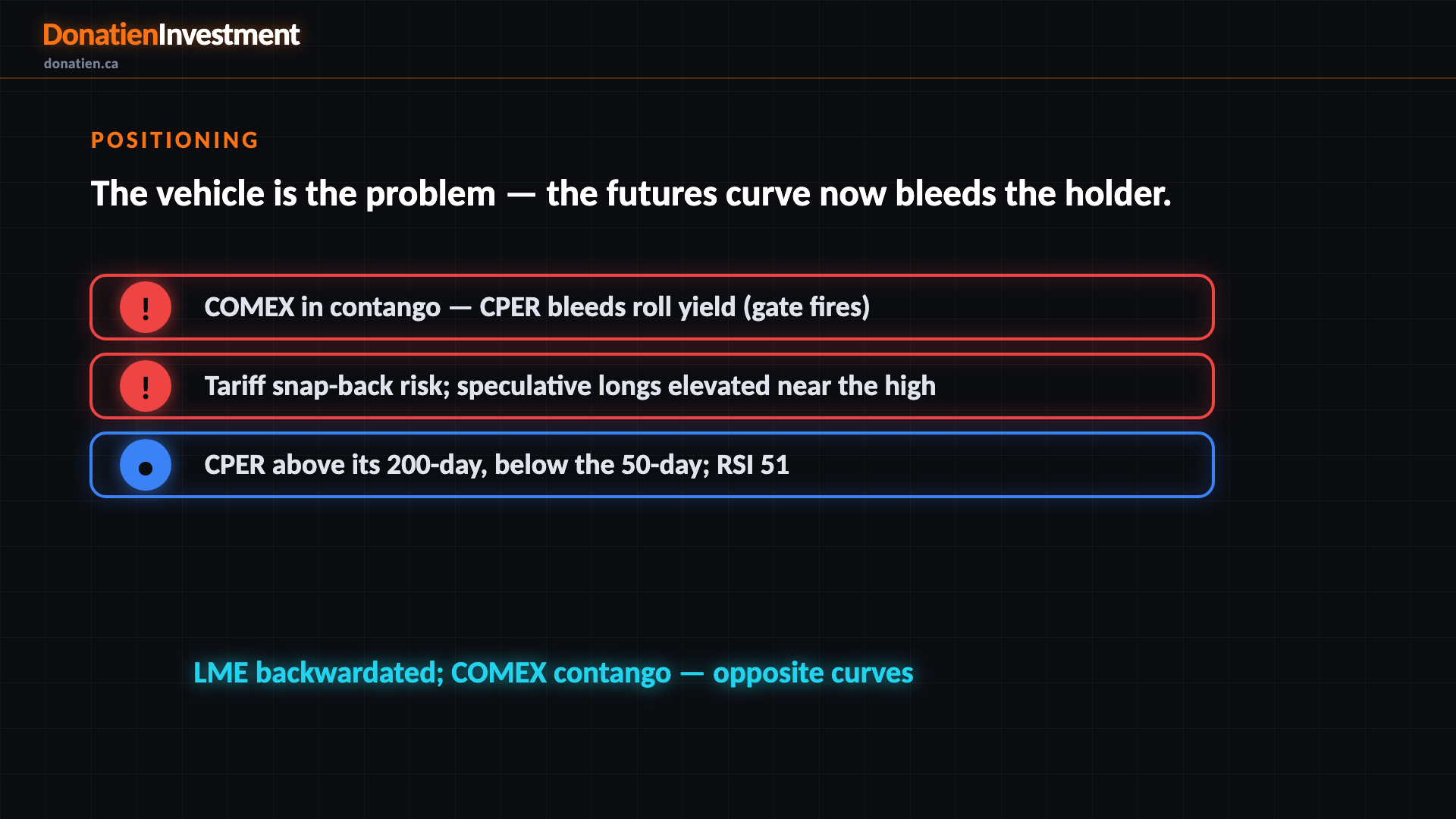

Positioning

Here's the catch that drove the downgrade. American copper futures have flipped into contango — each further-out contract costs more — because the market is pricing a proposed tariff into forward months. The popular copper ETF holds those futures, so it now bleeds roll yield: you lose money rolling the position even if the metal goes nowhere. Speculative longs are elevated after the rally, and the price is a few percent off its high. The metal's trend is fine; the vehicle is the problem — which is why you own physical.

Own physical (SCOP / COP.UN), not the futures ETF · LME backwardated; COMEX contango — opposite curves

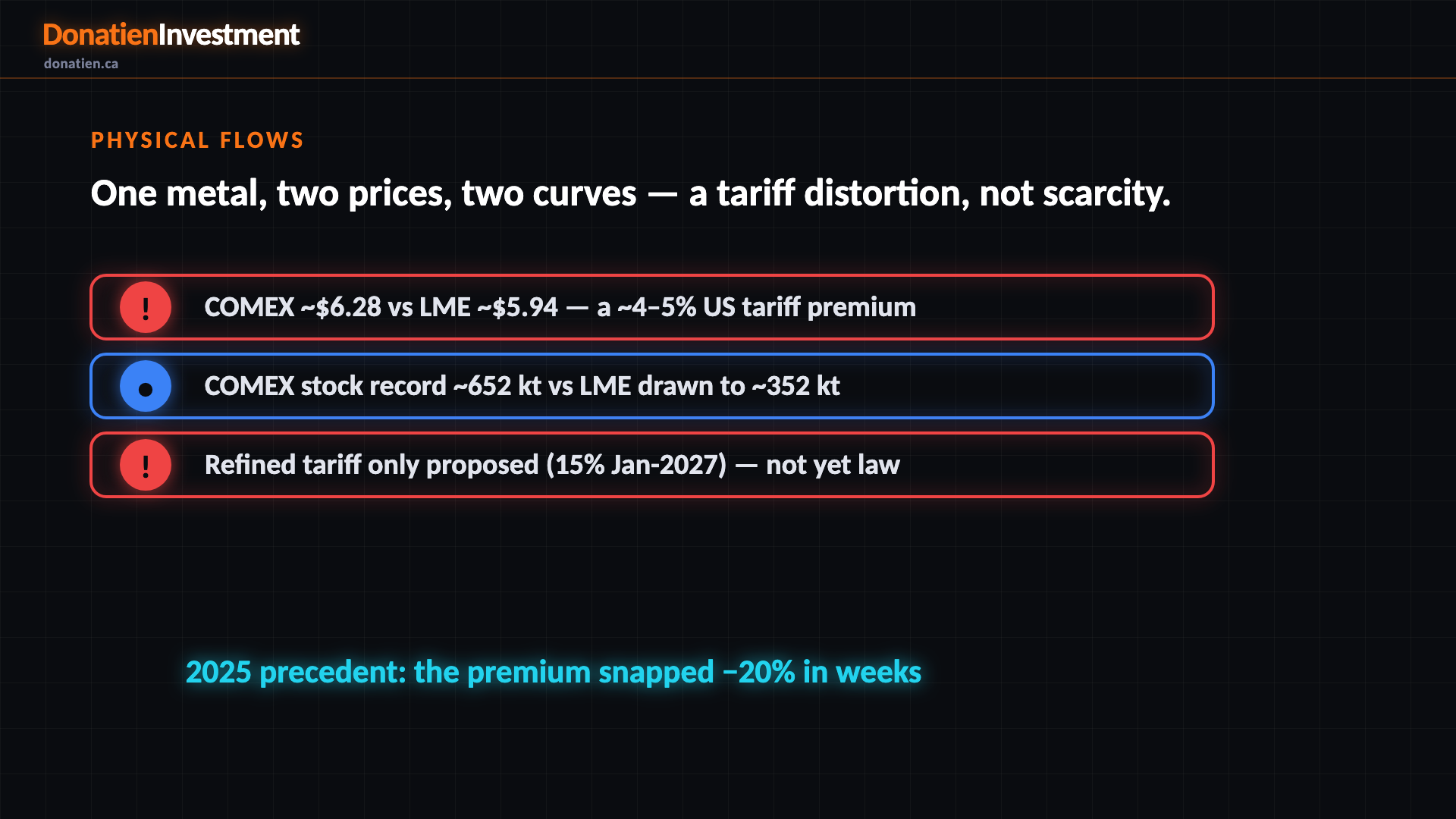

Physical flows

The plumbing is a tale of two prices. American COMEX trades about four to five percent over the global London price, and that premium widens further out the curve, because it prices a refined-copper tariff that is only proposed — fifteen percent from January twenty-twenty-seven — and not yet law. Metal has piled into American warehouses, a record six hundred fifty thousand tonnes, while London stock was drawn down. Strip the tariff and the tightness is real but not panicked — and if the tariff is rejected, that premium can snap back hard, as it did in twenty twenty-five.

COMEX contango: Jul $6.23 → Dec-2027 $6.70 · 2025 precedent: the premium snapped −20% in weeks

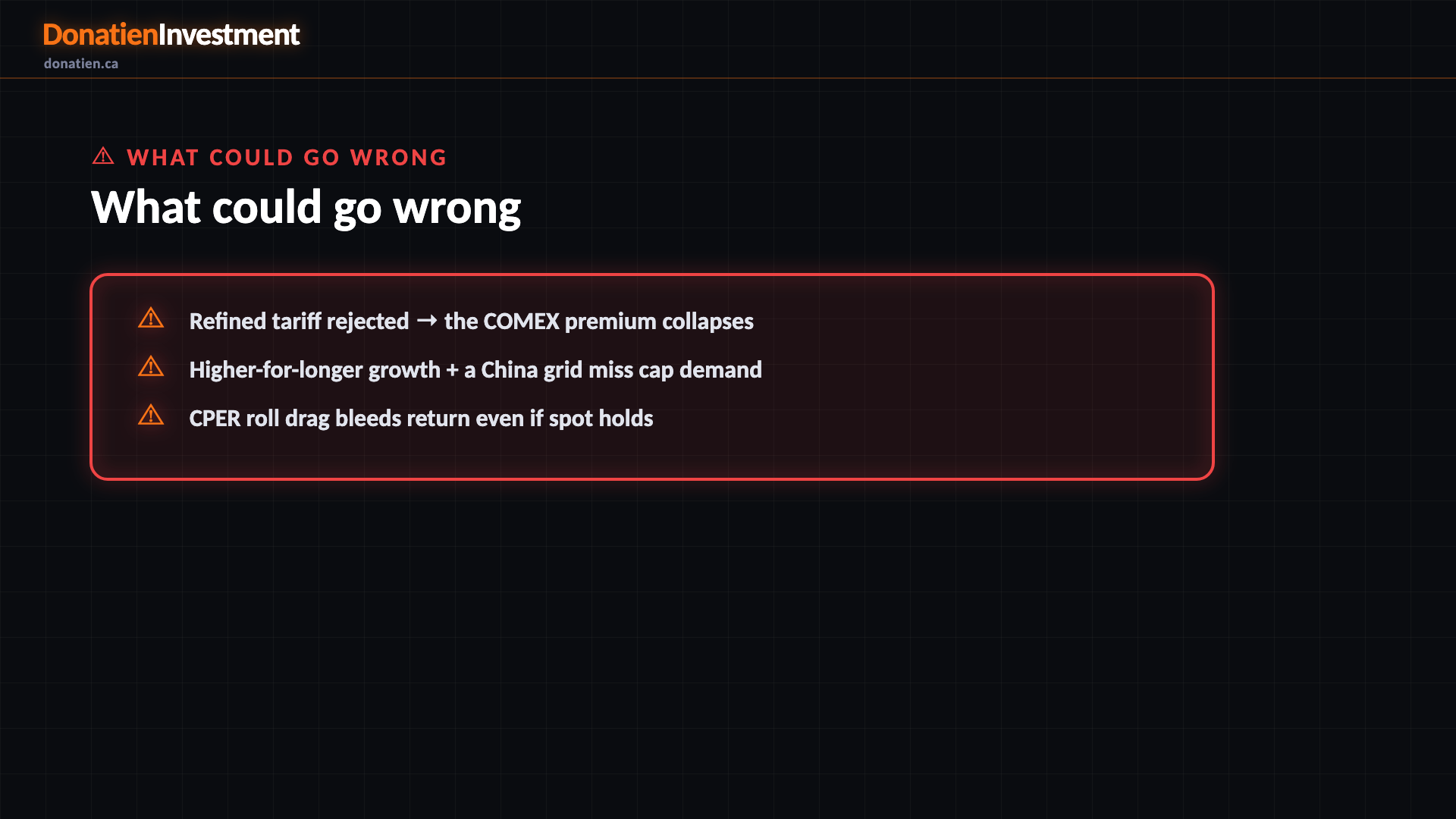

What could go wrong

The risks are as much about the vehicle and the tariff as the metal. If the President rejects or delays the refined tariff, the American premium collapses and the warehouse overhang floods back — the 2025 precedent was a twenty-percent drop in under a month. A pro-cyclical metal into a higher-for-longer economy, plus any disappointment in China's grid spend, caps the demand side. And even if the metal holds, the futures ETF keeps bleeding roll yield in this contango. These are why the short-term call is hold.

Risk vs Reward

The base case, and the likeliest over six to twelve months, has copper around six dollars ten a pound on the global price — the deficit flooring it near the incentive level while a slowing economy caps the top. The bull case is about seven dollars if the deficit bites harder or the tariff is enacted. The bear case is around five twenty if the tariff is rejected and growth softens.

The verdict

Short term, hold — the futures ETF is bleeding roll yield, the American price can snap back, and a pro-cyclical metal faces a growth headwind. Medium and long term it's a buy, down from strong buy, on a genuine deficit that supply can't answer below the incentive price. But own the long case in physical — the Sprott copper trust holds real cathode with no roll — not the futures ETF. Drivers and regime only amplify; the tight market and the leaky vehicle set the call.

Read the full report on donatien.ca →{kind=link}

{kind=link}