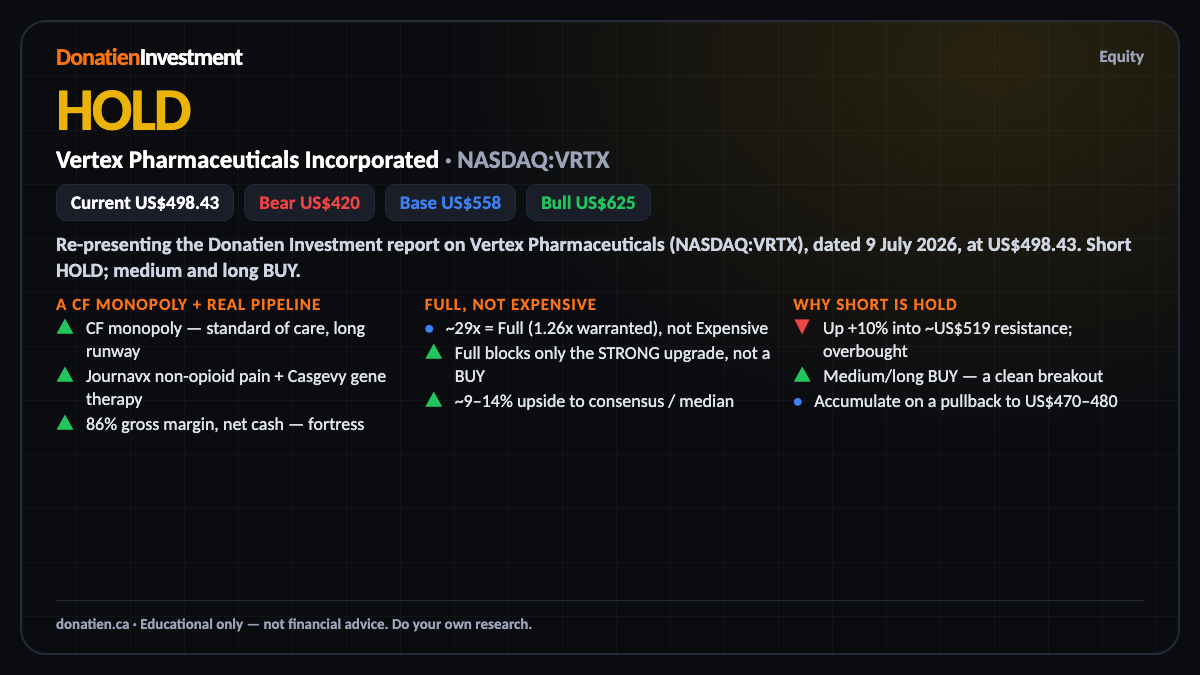

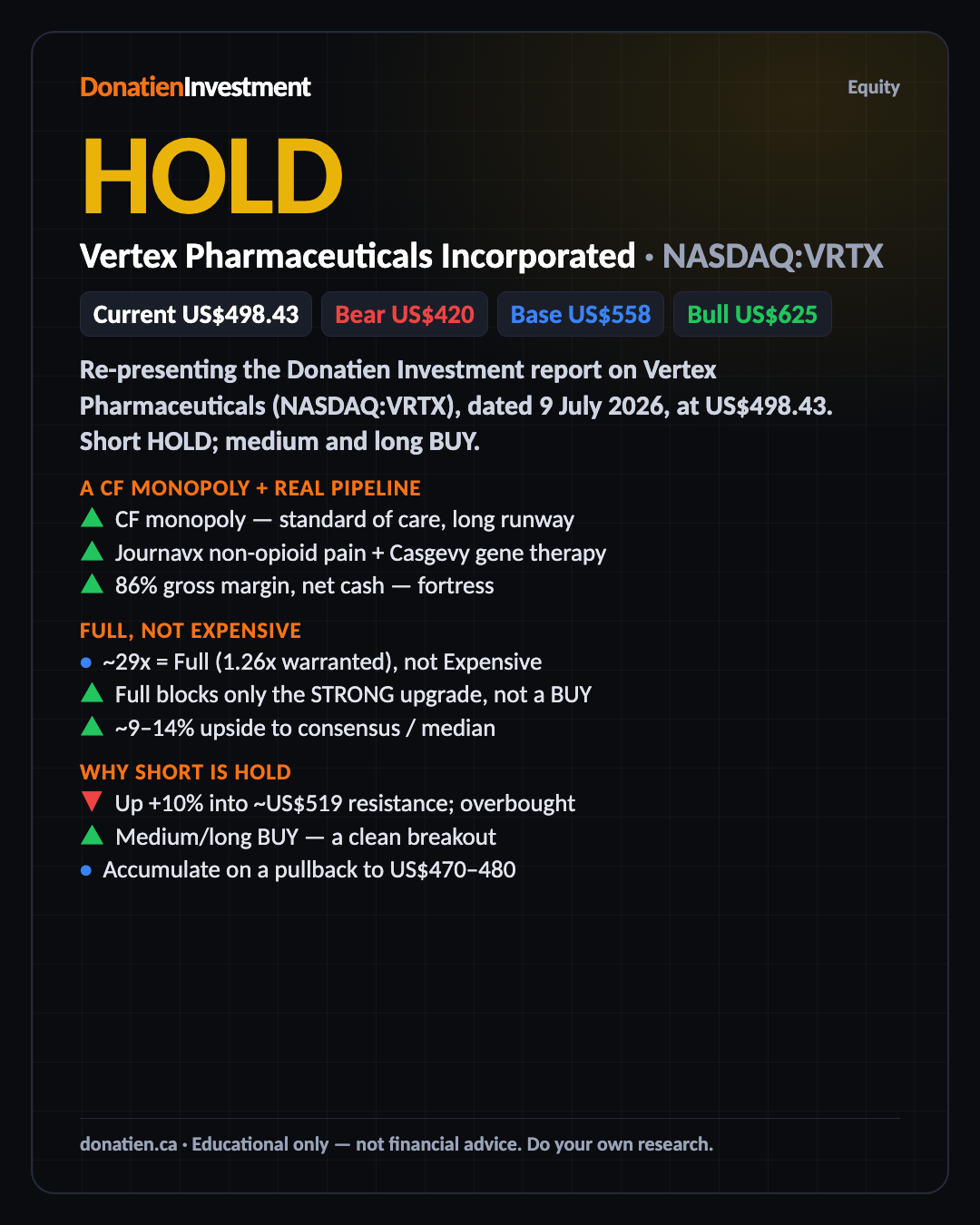

Vertex Pharmaceuticals Incorporated (NASDAQ:VRTX) HOLD

Vertex is an elite biotech — a cystic-fibrosis monopoly funding a genuinely differentiated pipeline. At about twenty-nine times earnings the valuation is Full, not Expensive, so it blocks only the strong-buy upgrade, not a base buy: medium and long are a BUY. But the stock is up ten per cent into resistance and overbought, so the near-term call is HOLD — accumulate on a pullback.

Re-presenting the Donatien Investment report on Vertex Pharmaceuticals (NASDAQ:VRTX), dated 9 July 2026, at US$498.43. Short HOLD; medium and long BUY.

A CF monopoly + real pipeline

Vertex owns cystic fibrosis — Trikafta and Alyftrek are the standard of care, with no meaningful rival and a long patent runway, throwing off eighty-six per cent gross margins and a fortress net-cash balance sheet. That cash funds a diversifying pipeline: Journavx, a first-in-class non-opioid pain drug attacking a huge market; Casgevy, the CRISPR gene therapy; and a cell therapy aiming to functionally cure type-one diabetes. Elite quality with genuine optionality.

Full, not Expensive

Valuation is the key nuance. At about twenty-nine times earnings — roughly one-and-a-quarter times our warranted multiple — Vertex is Full, but it's below the line that would force a HOLD. Full blocks only the strong-buy upgrade; it leaves a base BUY intact for medium and long owners. Ignore the trailing PEG near zero — that's a launch distortion; the forward PEG around two-and-a-half is the honest read.

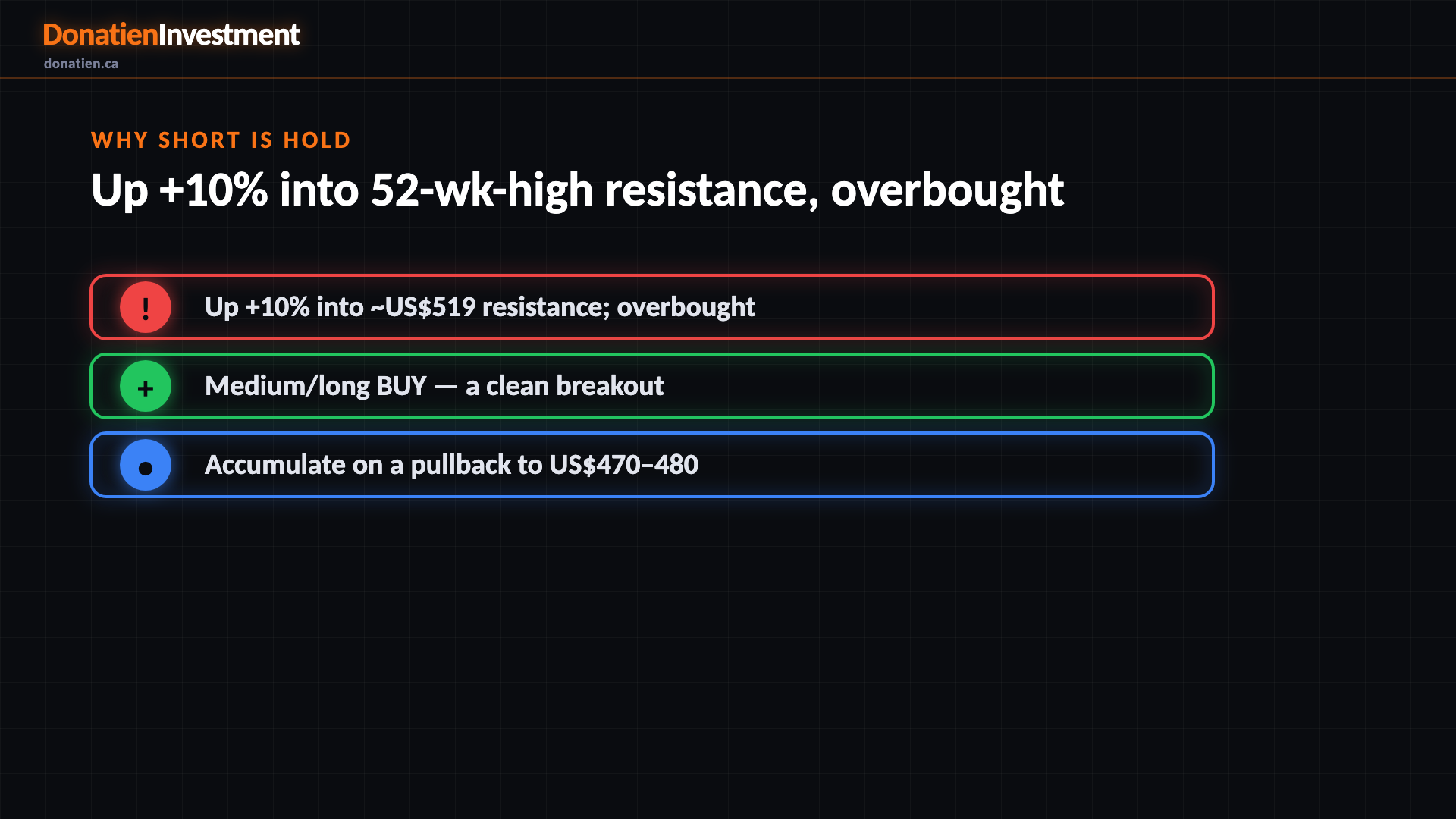

Why short is HOLD

So why is the near-term call still HOLD? The stock broke out to a fresh fifty-two-week-high zone, up ten per cent in three weeks, and it's now overbought on the hourly, bumping resistance around five-nineteen. The medium and long trends are constructive — this is a BUY to accumulate — but chasing an extended breakout is a poor short-term entry. Wait for a pullback toward four-seventy to four-eighty.

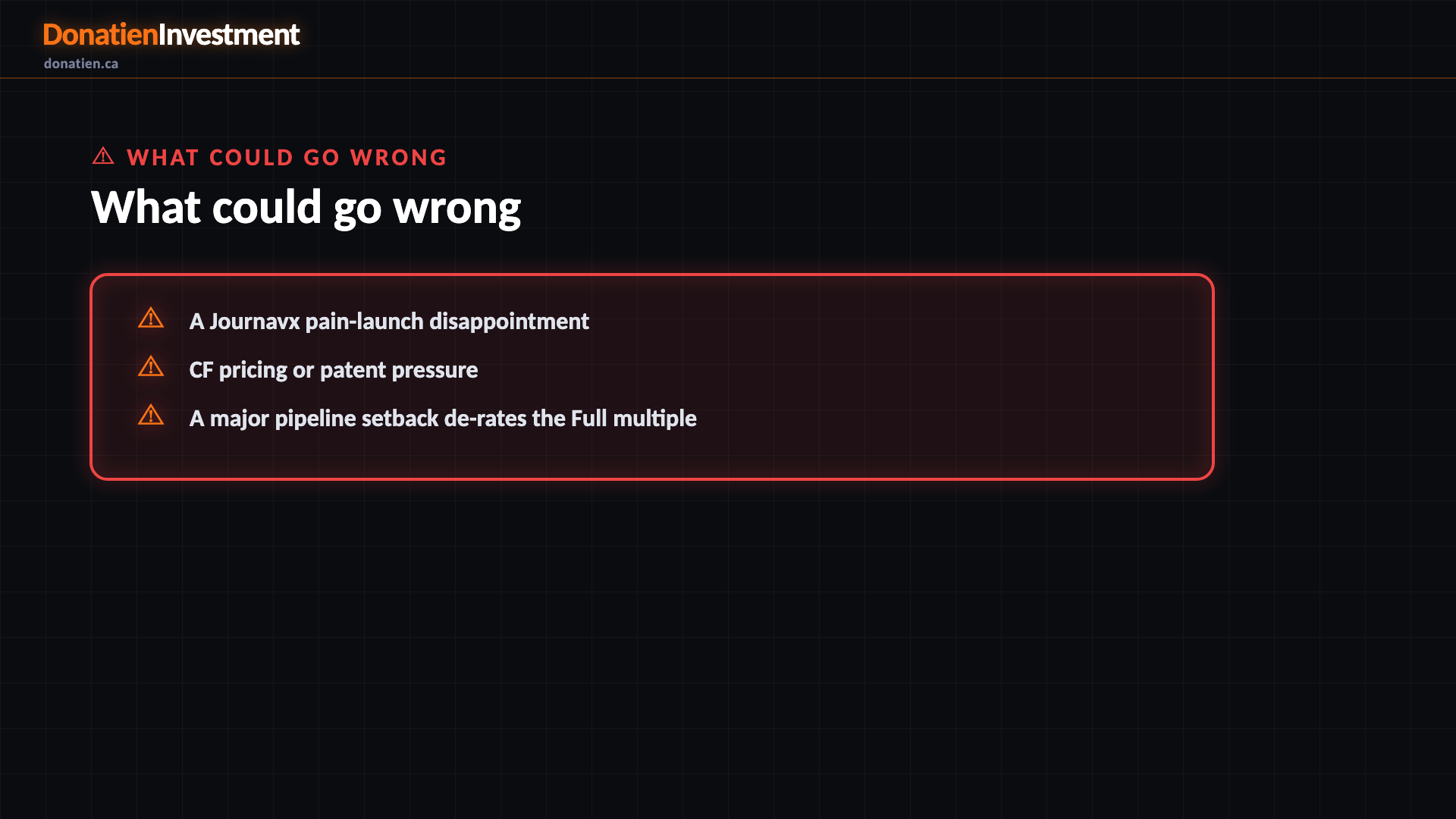

What could go wrong

A Journavx pain-launch disappointment. CF pricing or patent pressure. A major pipeline setback de-rates the Full multiple.

Risk vs Reward

The report weights three twelve-month paths. The base case, most likely at fifty per cent, sees Vertex around US$558 — cystic-fibrosis cash compounds and the pipeline delivers steadily. The bull at twenty-five per cent reaches US$625 if Journavx adoption beats and the pipeline re-rates. The bear at twenty-five per cent falls to US$420 on a launch miss or a patent scare. Probability-weighted, about US$540 — a positive skew that supports the medium and long BUY.

The verdict

An elite cystic-fibrosis monopoly funding a differentiated pipeline, at a Full but not Expensive multiple — a medium and long BUY. The near-term call is HOLD only because it's overbought into resistance after a ten per cent run; accumulate on weakness. This is not financial advice.

Read the full report on donatien.ca →{kind=link}

{kind=link}