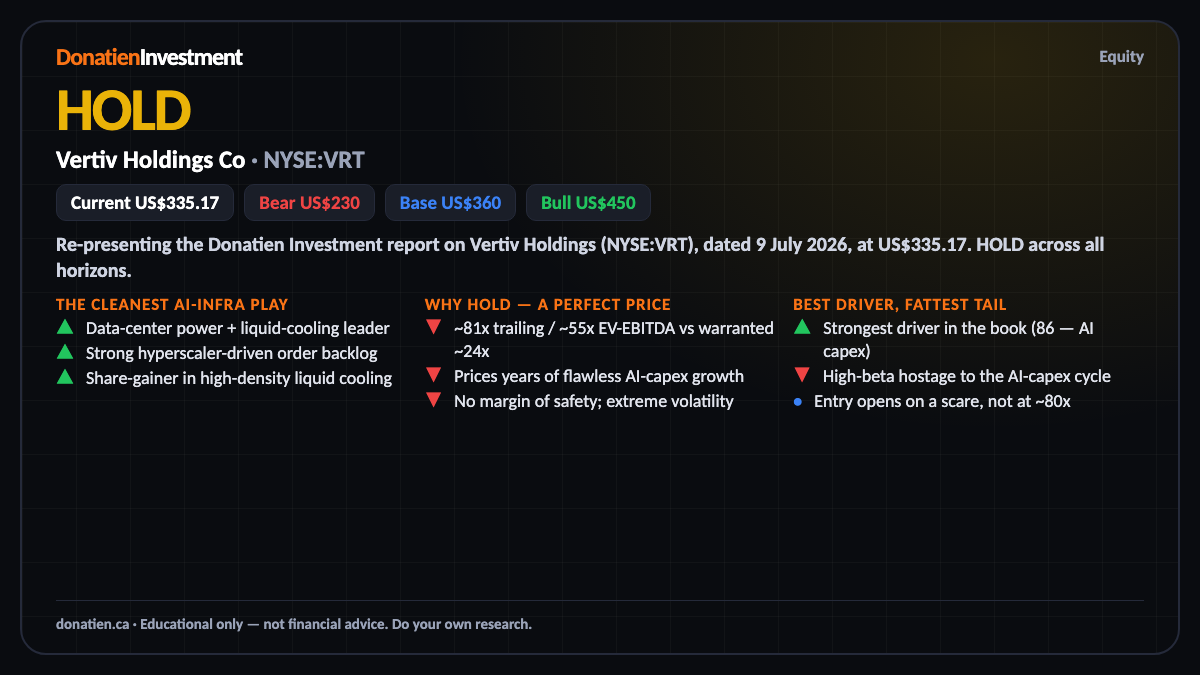

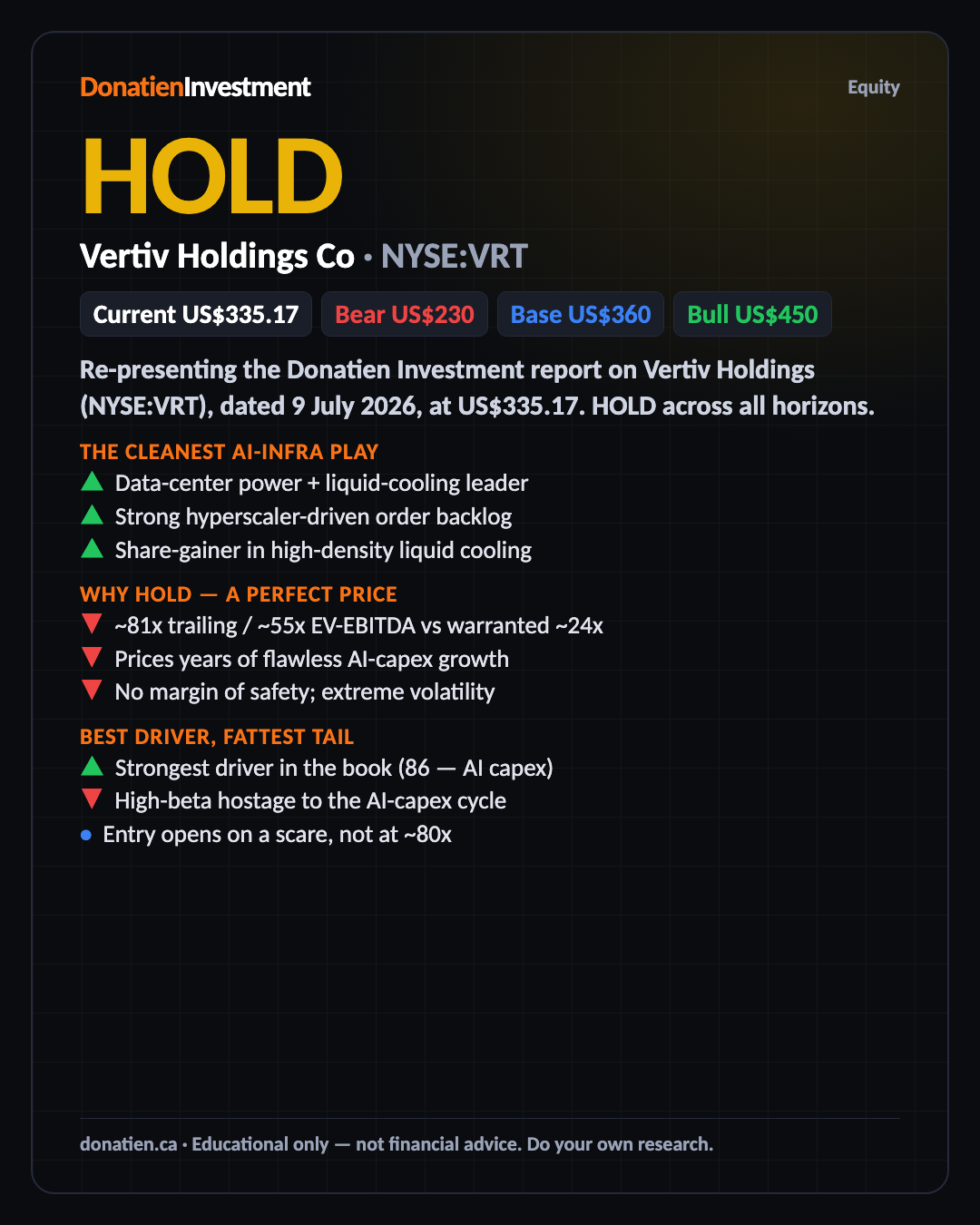

Vertiv Holdings Co (NYSE:VRT) HOLD

Vertiv is the cleanest pure-play on data-center power and cooling — the strongest driver in our entire book. But at about eighty times trailing earnings, fifty-five times EV-to-EBITDA, the price underwrites years of flawless AI-capex growth with no margin of safety. A superb business at a perfect price, and a high-beta hostage to the AI cycle — HOLD.

Re-presenting the Donatien Investment report on Vertiv Holdings (NYSE:VRT), dated 9 July 2026, at US$335.17. HOLD across all horizons.

The cleanest AI-infra play

Vertiv sells the physical infrastructure behind AI — power distribution, busway, switchgear, and increasingly liquid cooling for high-density GPU racks. As hyperscalers pour capital into compute, Vertiv sells the power and cooling around it, and it's a genuine share-gainer in liquid cooling with a strong order book. It's arguably the cleanest listed proxy for the AI build-out's physical layer.

Why hold — a perfect price

Here's the problem. At about eighty-one times trailing earnings and fifty-five times EV-to-EBITDA, against a warranted mid-twenties even on generous growth, Vertiv is very expensive — more than three times its warranted multiple. That price prices in years of uninterrupted AI-capex growth. The trailing PEG looks tame only if hyper-growth persists; any wobble compresses earnings and the multiple together.

Best driver, fattest tail

The AI-capex driver is the single strongest in our coverage. But that same concentration is the risk: at eighty times, an AI-capex pause — the systemic tail our macro work flags — would compress both growth and the multiple. That's why the bear case is a fat, correlated thirty-one per cent de-rate. Great company, hostage to a perfect price. The entry opens on an AI-capex scare, not here.

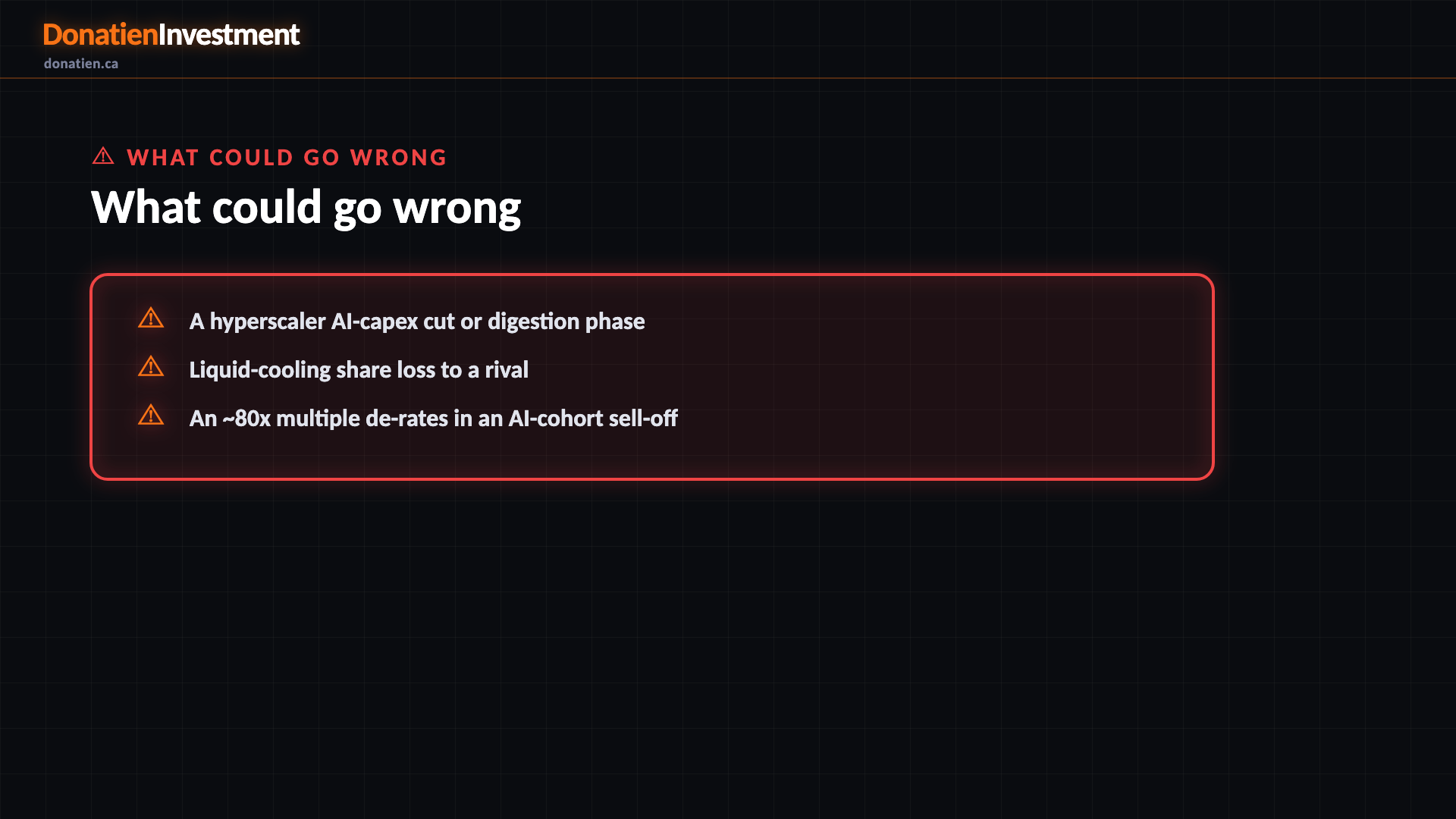

What could go wrong

A hyperscaler AI-capex cut or digestion phase. Liquid-cooling share loss to a rival. An ~80x multiple de-rates in an AI-cohort sell-off.

Risk vs Reward

The report weights three twelve-month paths. The base case, most likely at fifty per cent, sees Vertiv around US$360 — strong growth continues but the eighty-times multiple digests sideways. The bull at twenty-five per cent reaches US$450 if AI capex stays vertical. The bear at twenty-five per cent falls to US$230 — a thirty-one per cent drop — if an AI-capex pause compresses both growth and the multiple. Probability-weighted, about US$350, with a fat, correlated bear.

The verdict

The cleanest AI-infrastructure pure-play on the strongest driver in our book — but at about eighty times earnings it underwrites perfection and is a high-beta hostage to the AI-capex cycle. A HOLD until the price offers a cushion. This is not financial advice.

Read the full report on donatien.ca →{kind=link}

{kind=link}