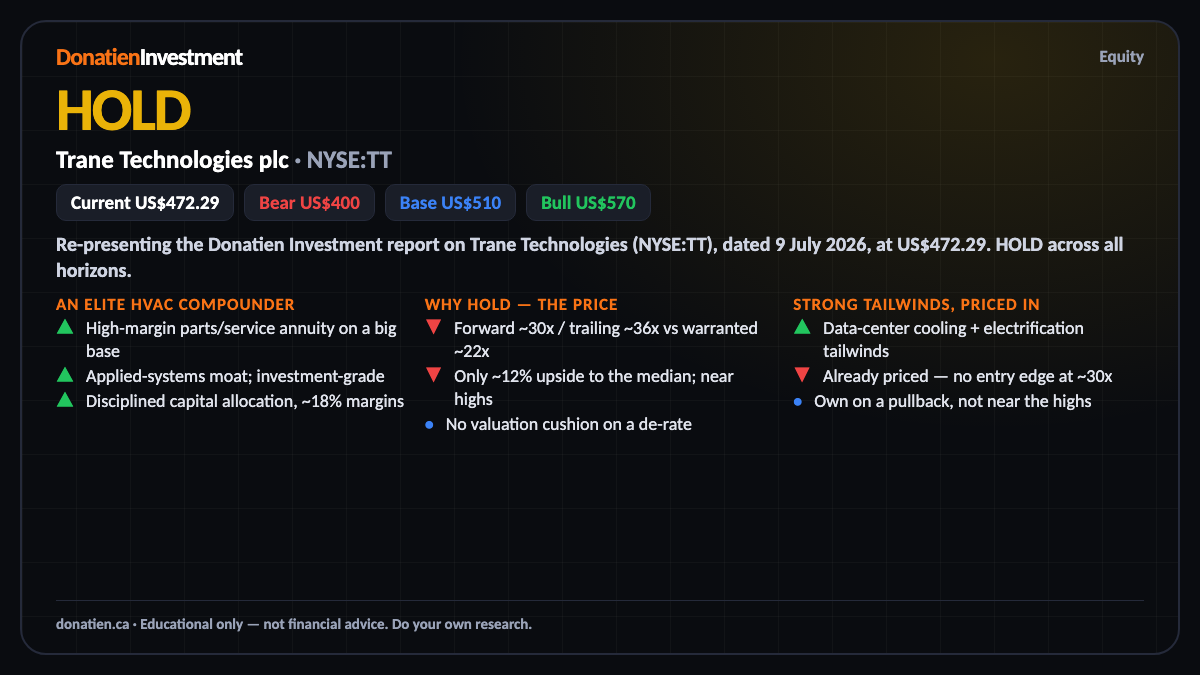

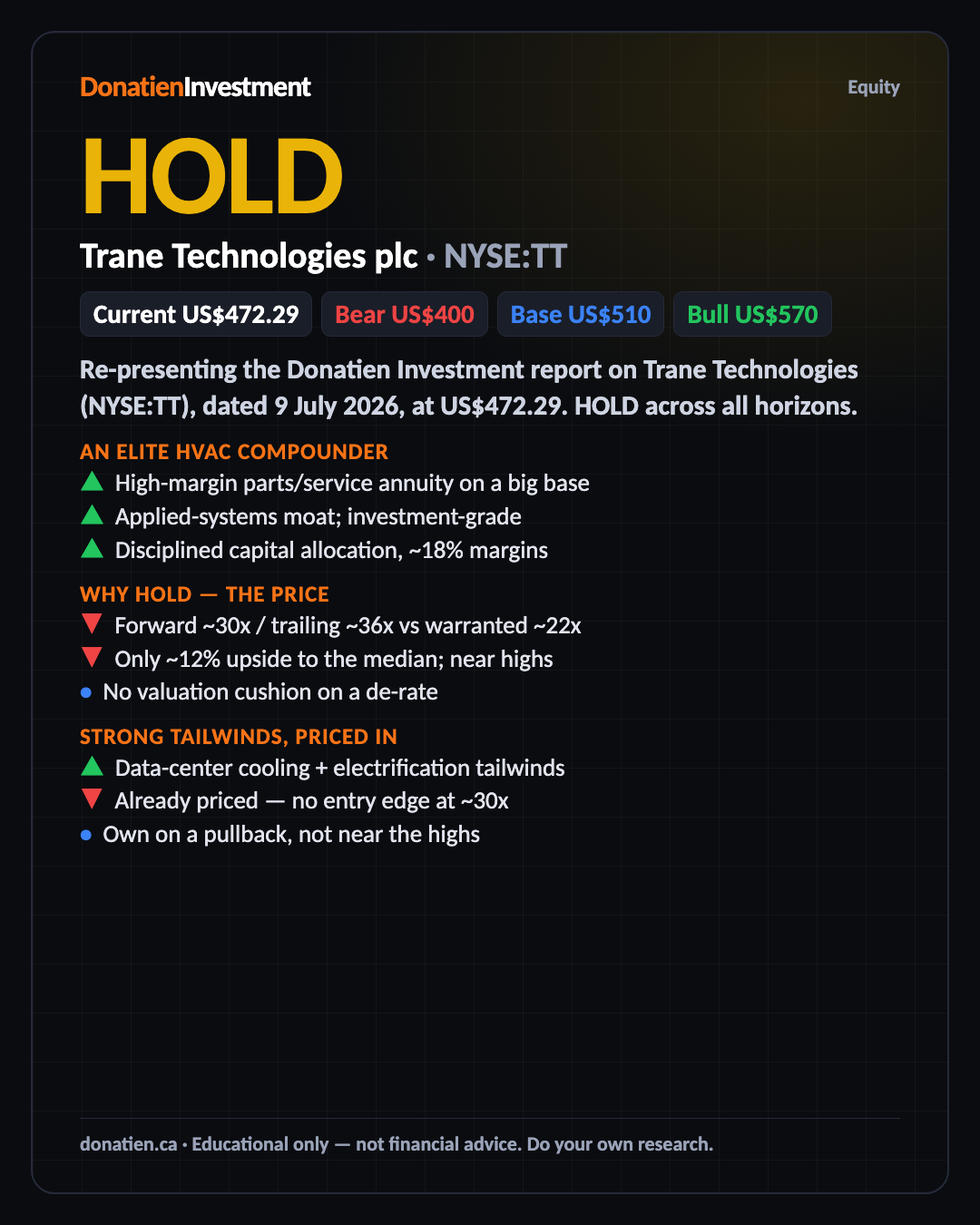

Trane Technologies plc (NYSE:TT) HOLD

Trane is an elite HVAC compounder on two strong tailwinds — data-center cooling and building electrification. But at a trailing thirty-six times earnings, forward thirty, against a warranted low-twenties, it's expensive, with only about twelve per cent upside to the median. A superb business at a rich price, so the strong driver can't lift it — HOLD.

Re-presenting the Donatien Investment report on Trane Technologies (NYSE:TT), dated 9 July 2026, at US$472.29. HOLD across all horizons.

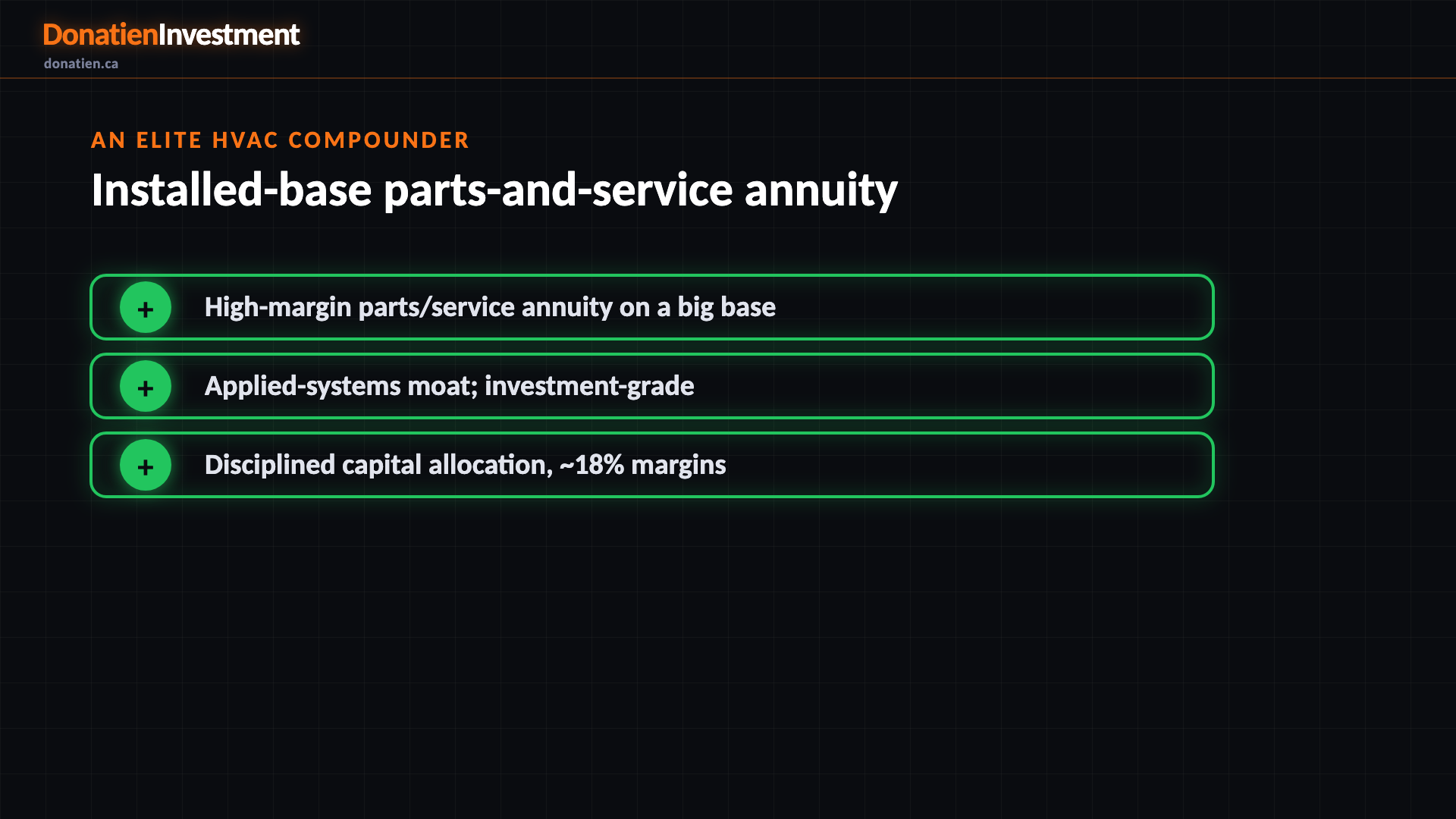

An elite HVAC compounder

Trane is a global leader in climate control — HVAC for commercial buildings, plus Thermo King transport refrigeration. Its quality rests on a huge installed base that throws off high-margin parts, service and controls revenue, applied-systems engineering that's hard to displace, and disciplined capital allocation. Operating margins near eighteen per cent, strong free cash flow, an investment-grade balance sheet. A genuine compounder.

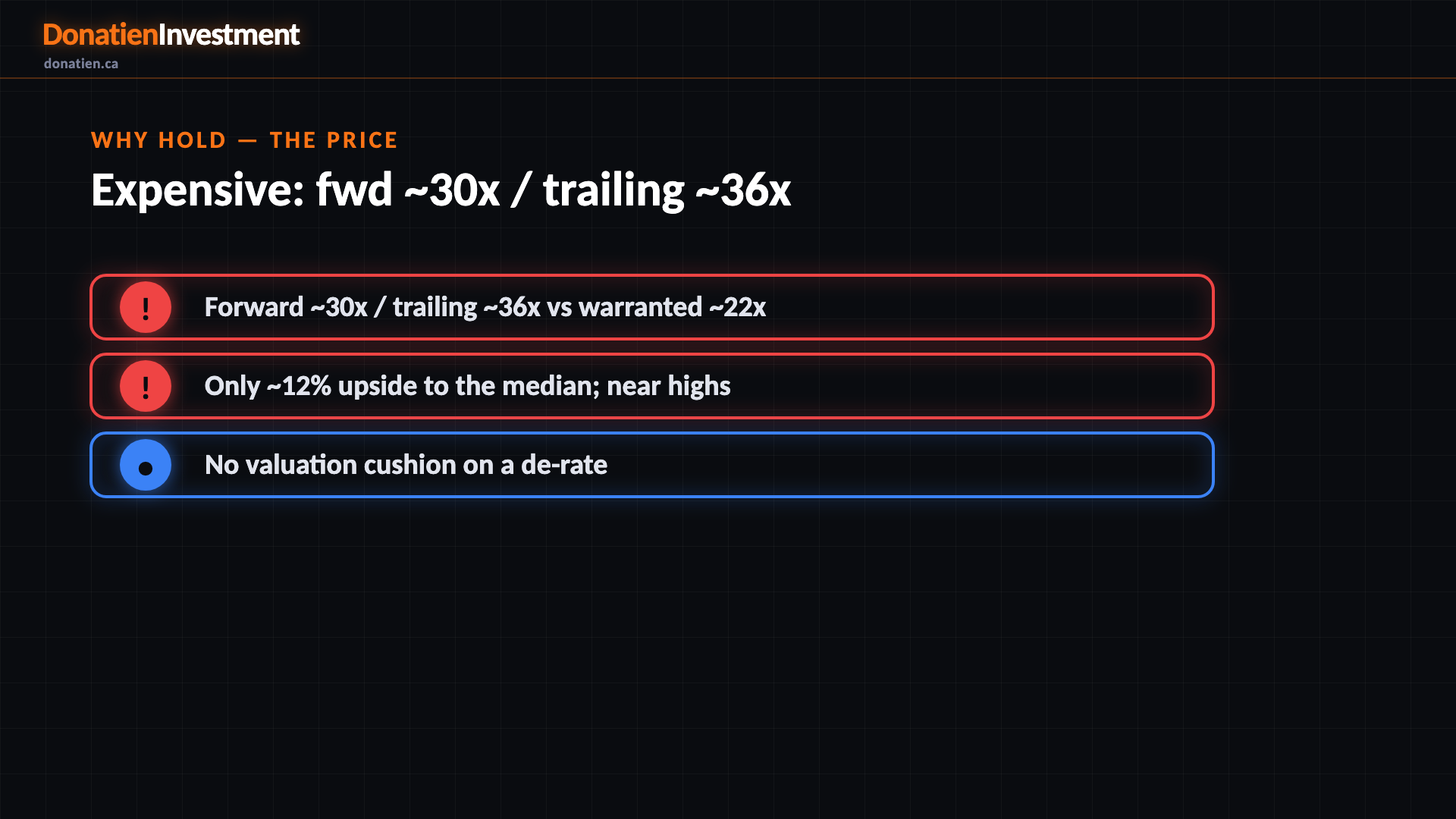

Why hold — the price

The catch is valuation. At forward thirty times earnings — trailing thirty-six, EV-to-EBITDA around twenty-five — against a warranted low-twenties for an industrial, Trane is expensive. That's roughly one-and-a-half times its warranted multiple, which trips our valuation gate and caps the signal at HOLD. Only about twelve per cent upside to the median, and no cushion if the premium de-rates.

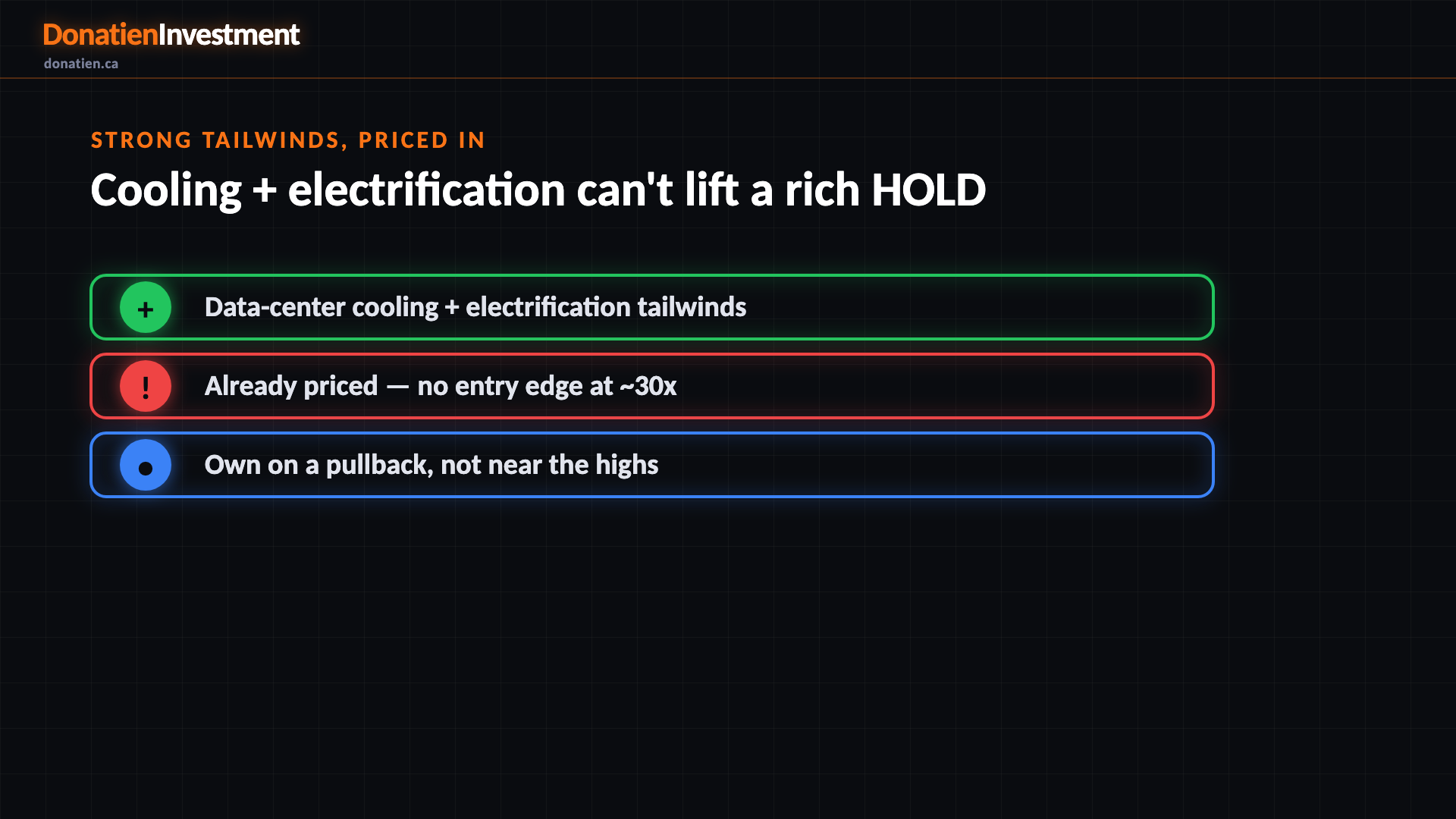

Strong tailwinds, priced in

Two structural engines drive Trane: data-center thermal management, as AI capacity needs enormous cooling, and building decarbonisation — heat pumps, efficiency retrofits. Both are multi-year and both play to Trane's strengths. But the market already pays for them. A strong driver can't lift a valuation-capped HOLD; it's the reason to own Trane on weakness, not to pay thirty times forward near the highs.

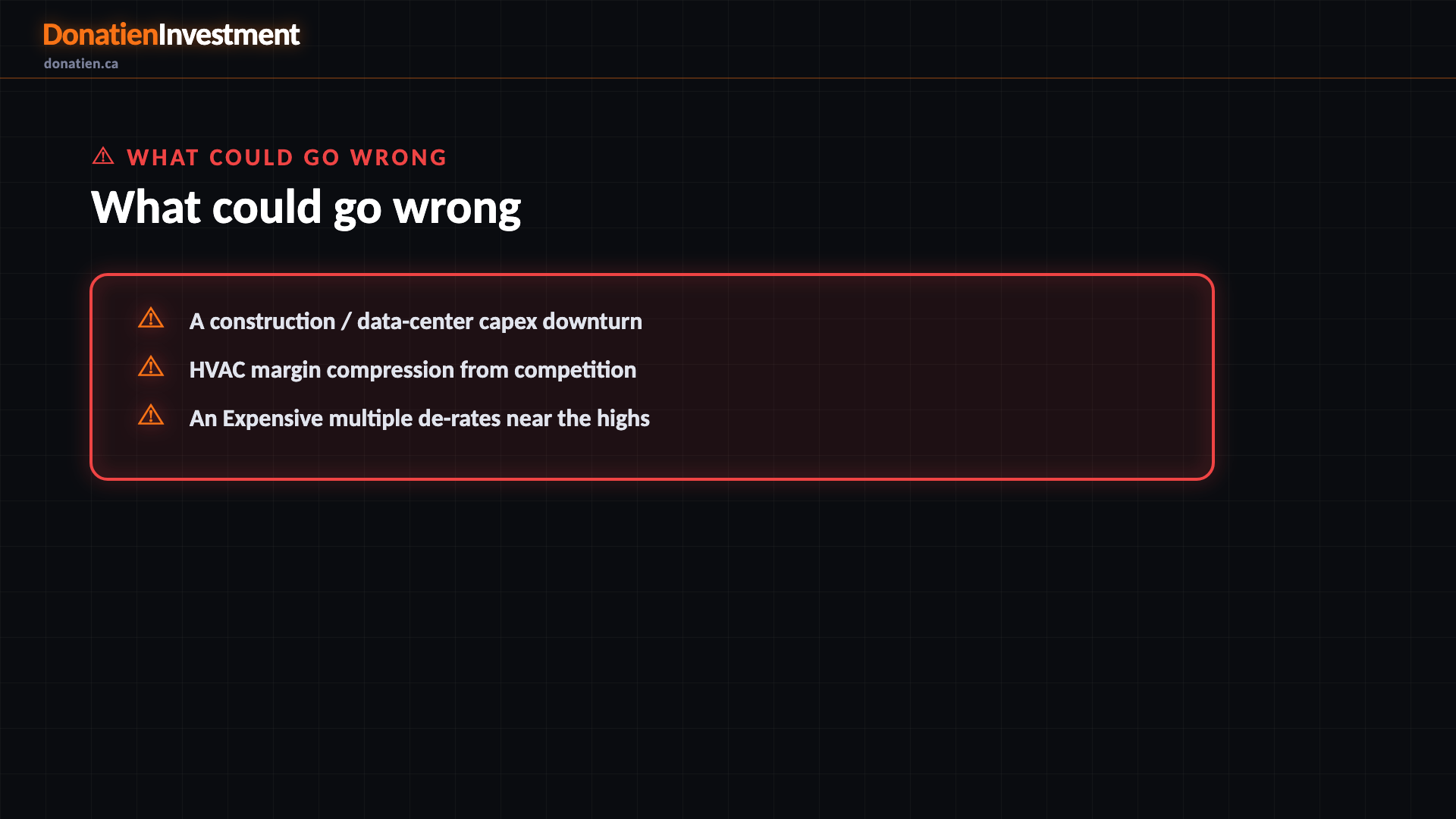

What could go wrong

A construction / data-center capex downturn. HVAC margin compression from competition. An Expensive multiple de-rates near the highs.

Risk vs Reward

The report weights three twelve-month paths. The base case, most likely at fifty per cent, sees Trane around US$510 — steady mid-teens compounding, but a rich multiple caps the re-rate. The bull at twenty-five per cent reaches US$570 if cooling and electrification orders accelerate. The bear at twenty-five per cent falls to US$400 on a capex slowdown or a de-rate. Probability-weighted, about US$497 — a modest skew that can't justify chasing at thirty times forward.

The verdict

An elite HVAC compounder on strong data-center-cooling and electrification tailwinds — but at thirty times forward it's expensive, with little upside to the median and no cushion. A great business to own on weakness, not at these levels — HOLD. This is not financial advice.

Read the full report on donatien.ca →{kind=link}

{kind=link}