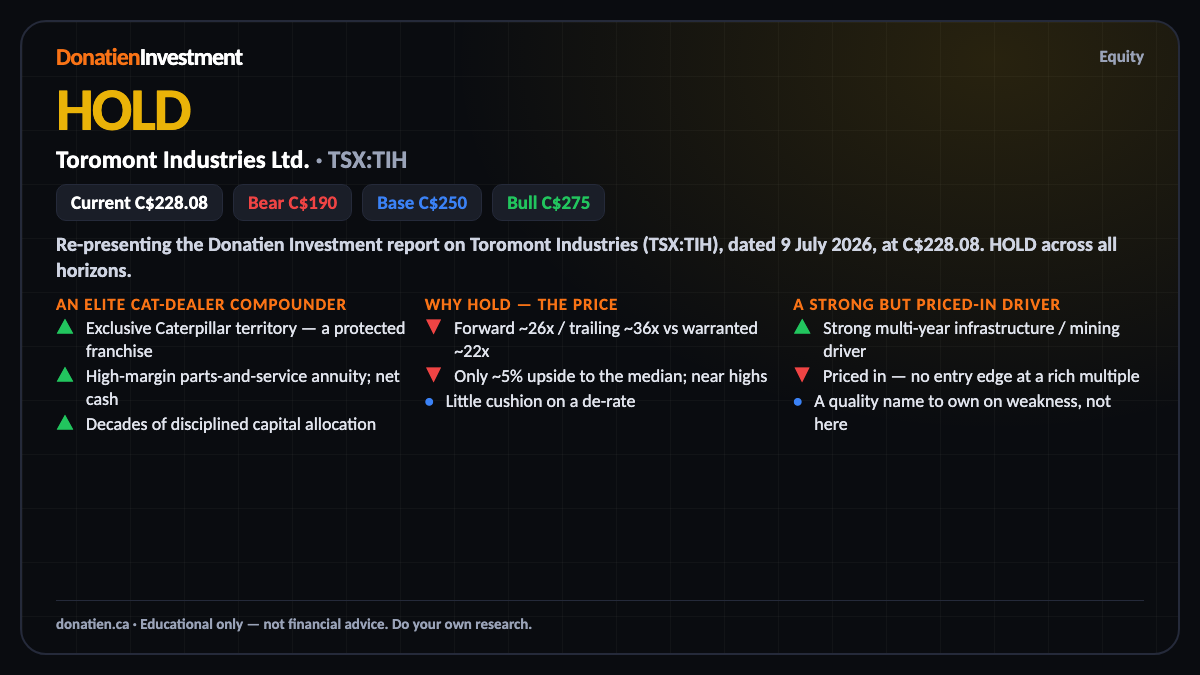

Toromont Industries Ltd. (TSX:TIH) HOLD

Toromont is an elite Canadian industrial compounder — the exclusive Caterpillar dealer across much of Canada — on a strong infrastructure and mining tailwind. But at a forward twenty-six times earnings, with only about five per cent upside to the median, the strong driver can't lift a valuation-capped signal. A great business at a rich price — HOLD.

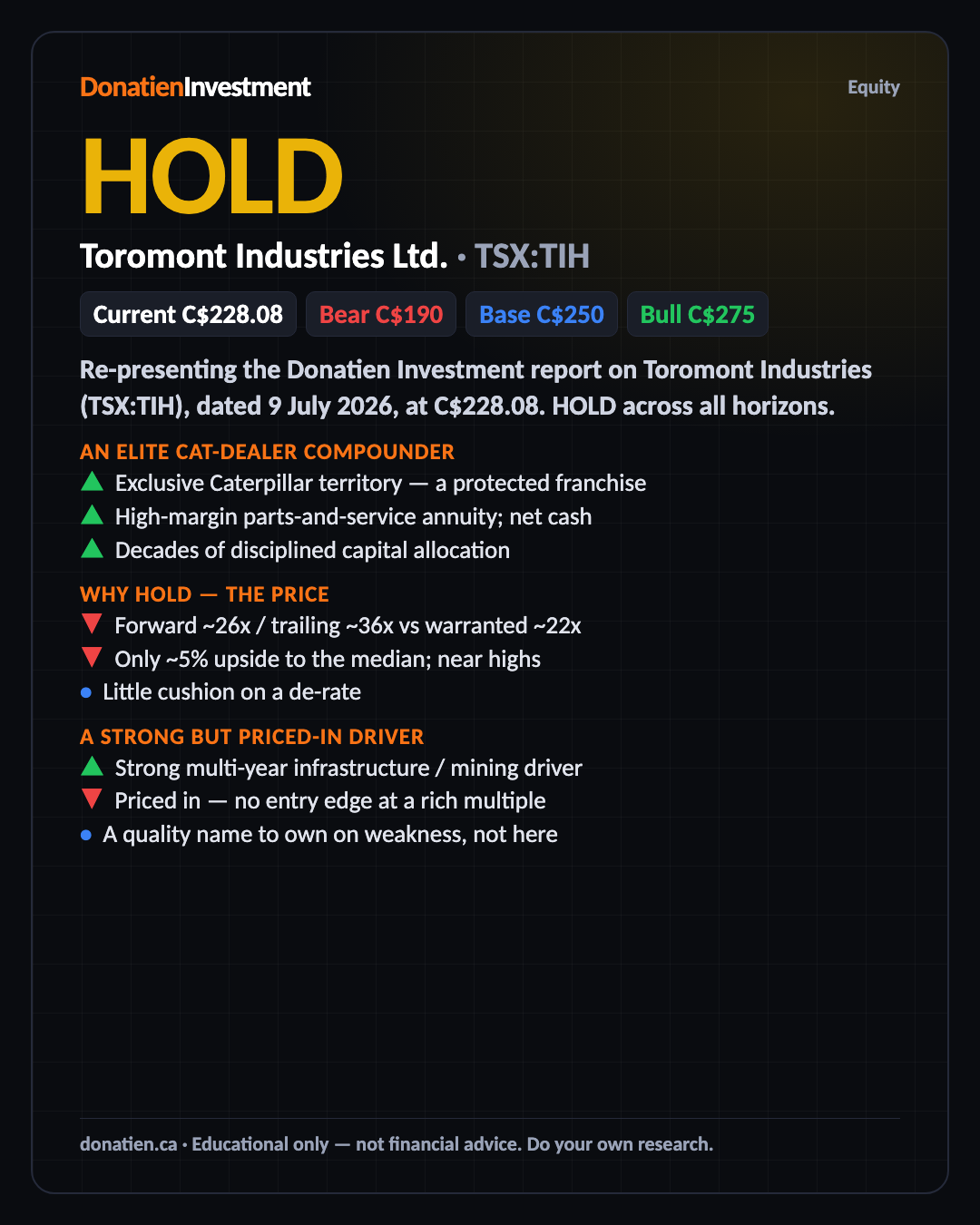

Re-presenting the Donatien Investment report on Toromont Industries (TSX:TIH), dated 9 July 2026, at C$228.08. HOLD across all horizons.

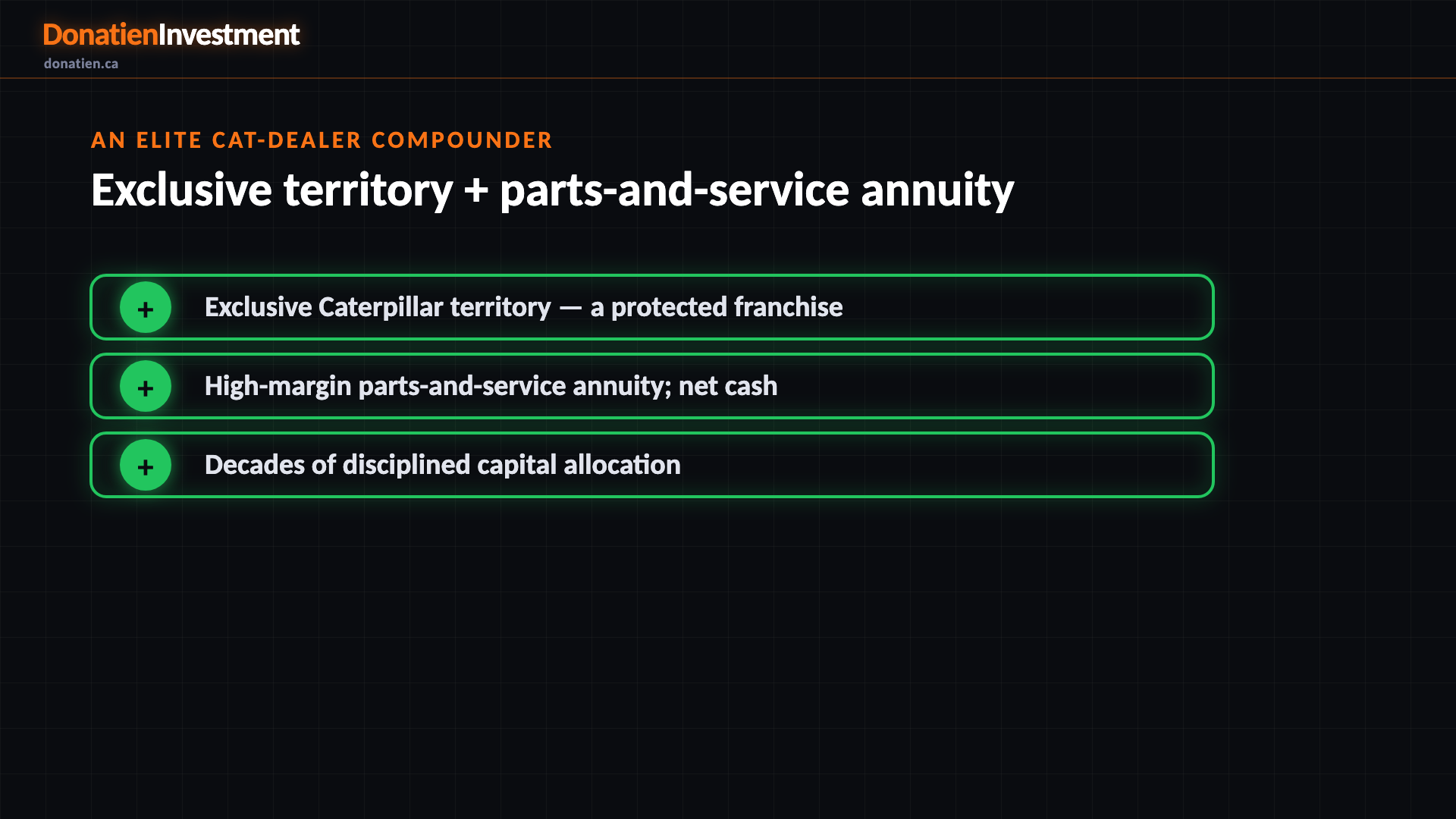

An elite Cat-dealer compounder

Toromont is built on two pillars: the exclusive Caterpillar dealership across much of Canada — selling, renting and servicing heavy equipment — and CIMCO refrigeration. Its core is razor-and-blade economics: sell the machine, then earn durable, high-margin revenue on parts and service for decades. Add a legendary record of disciplined capital allocation, steady dividend growth, and a net-cash balance sheet, and you have a genuine compounder.

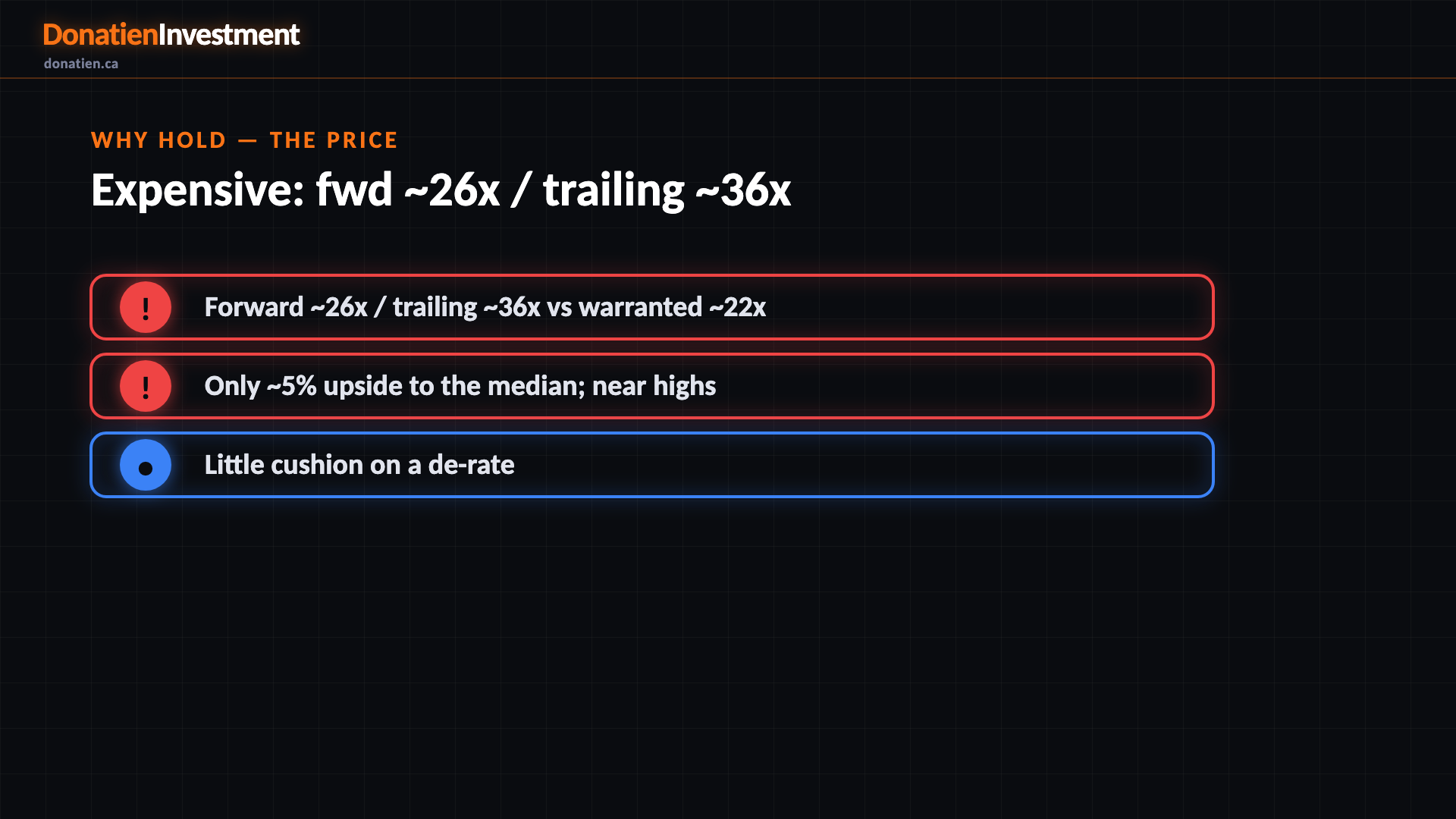

Why hold — the price

Here's the catch. At a forward twenty-six times earnings — trailing thirty-six — against a warranted low-twenties for an industrial, Toromont is expensive, with only about five per cent upside to the analyst median. The market knows how good it is, and the premium already discounts the quality and the infrastructure tailwind. There's little cushion if it de-rates.

A strong but priced-in driver

The infrastructure, construction and mining capex driver is one of the strongest in our coverage — a genuine multi-year tailwind for equipment and aftermarket service. But a strong driver can't lift a signal that's capped by an expensive valuation. It's the reason to keep watching Toromont for a better entry, not a reason to pay twenty-six times forward near the highs.

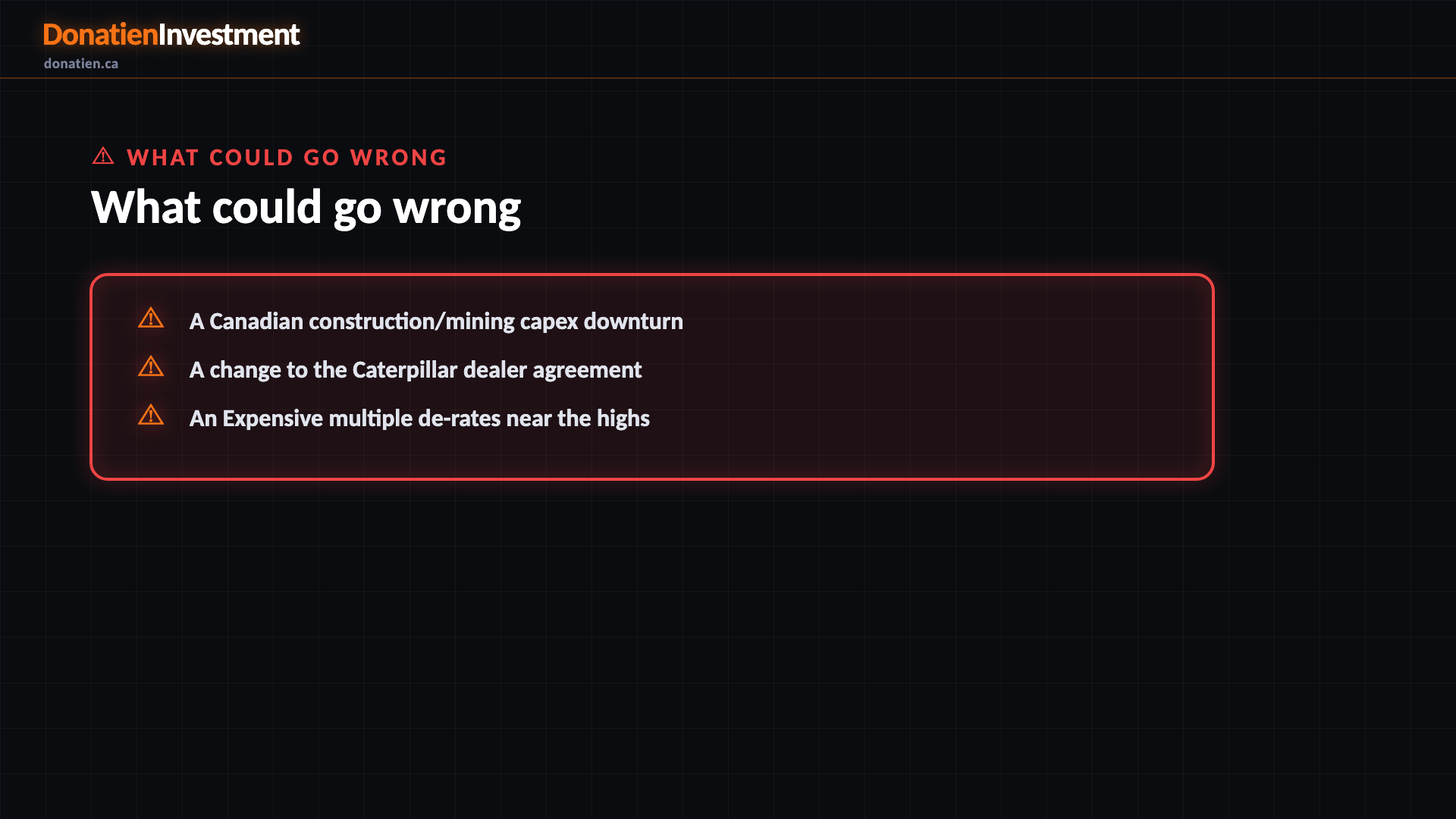

What could go wrong

A Canadian construction/mining capex downturn. A change to the Caterpillar dealer agreement. An Expensive multiple de-rates near the highs.

Risk vs Reward

The report weights three twelve-month paths. The base case — most likely at 50% — sees Toromont around C$250 on steady compounding on the infrastructure tailwind, but a rich multiple caps the re-rate, about 10% above today. The bull at 25% reaches C$275 if capex accelerates and the multiple holds. The bear at 25% takes it to C$190 on a construction or mining slowdown, or a de-rating of the expensive multiple toward the low-twenties.

The verdict

The bottom line: an elite Caterpillar-dealer compounder on a strong infrastructure and mining tailwind — but at a forward twenty-six times earnings near its highs, with only five per cent upside to the median, the quality isn't the question, the price is. It's a hold. Wait for a pullback or a de-rate toward the low-twenties multiple before paying up for the tailwind — a quality name to own on weakness, not here.

Read the full report on donatien.ca →{kind=link}

{kind=link}