The Charles Schwab Corporation (NYSE:SCHW) HOLD

Charles Schwab is a high-quality, re-accelerating asset-gatherer at a reasonable twenty times earnings — the medium-term signal is a STRONG BUY. But the stock has run eleven per cent into overbought territory at its 52-week high, with Q2 earnings inside two weeks, so the near-term entry is a hold: wait for a pullback.

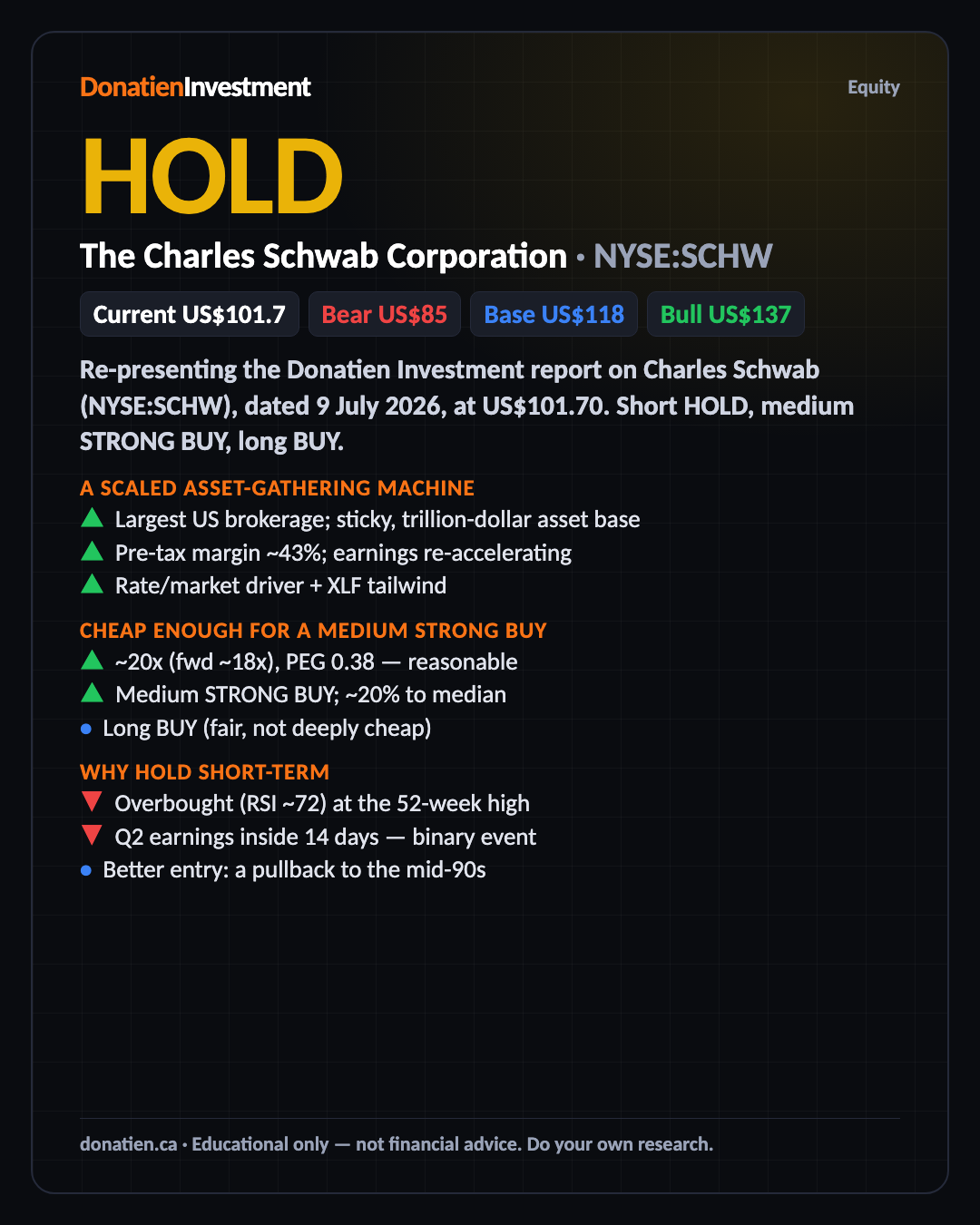

Re-presenting the Donatien Investment report on Charles Schwab (NYSE:SCHW), dated 9 July 2026, at US$101.70. Short HOLD, medium STRONG BUY, long BUY.

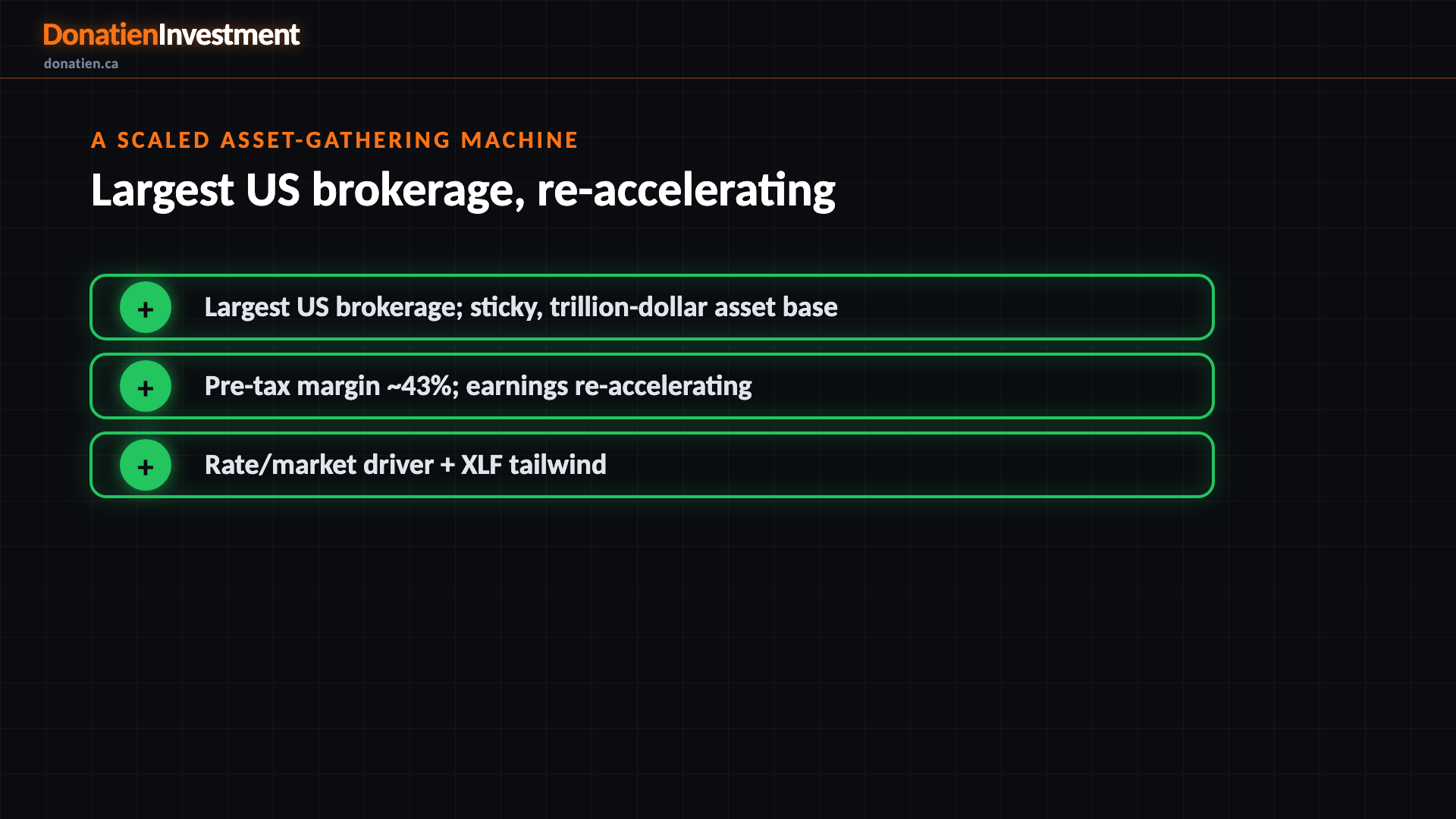

A scaled asset-gathering machine

Schwab is the largest US retail brokerage and a major custodian, holding trillions in client assets. It makes money mainly on net interest income from client cash, plus asset-management fees and trading. Its edge is scale, a sticky asset base, and strong operating leverage — earnings are re-accelerating as client cash re-prices higher and the rate and market environment turns favourable.

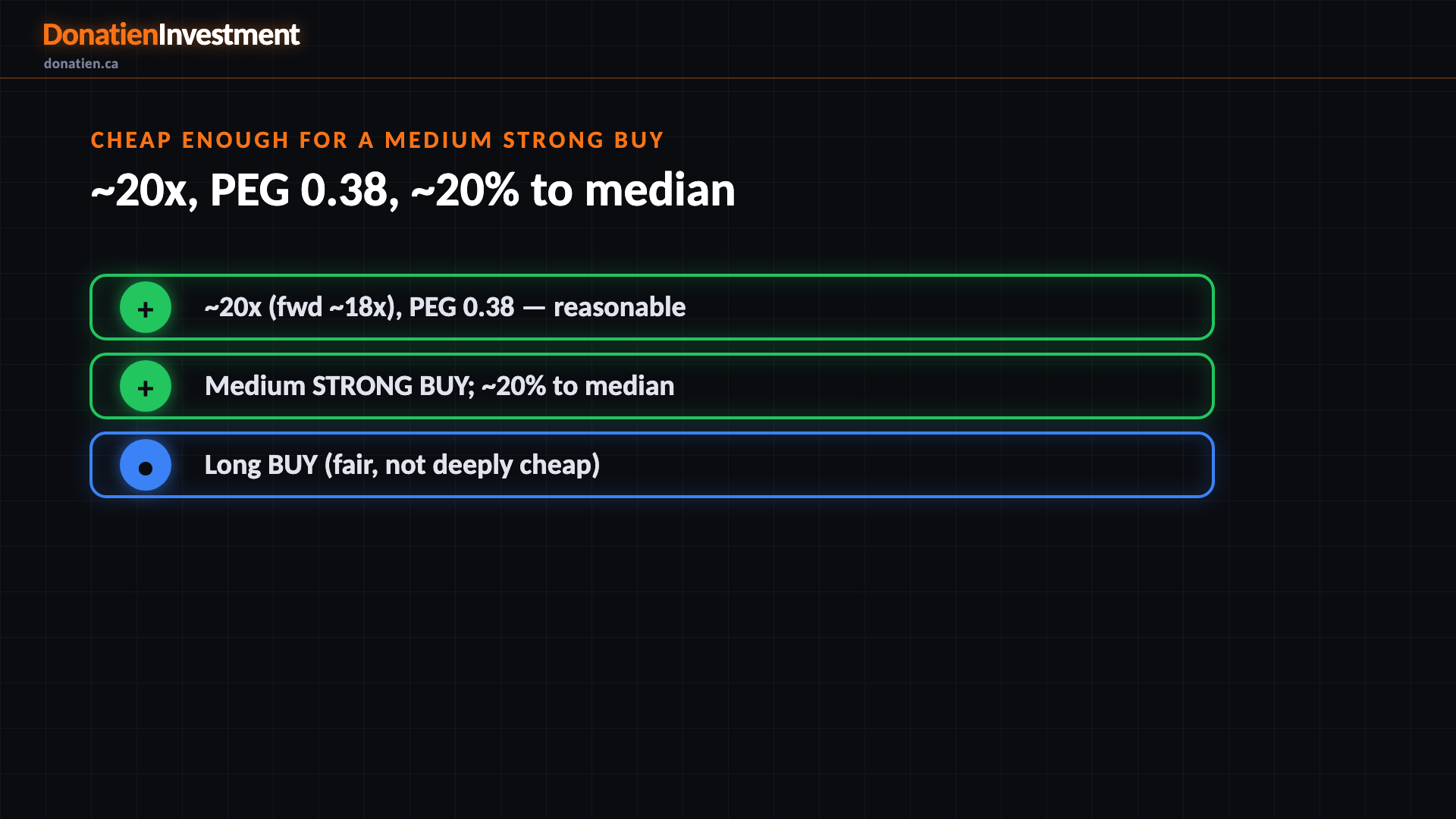

Cheap enough for a medium STRONG BUY

On valuation it's reasonable — about twenty times earnings, eighteen times forward, with a price-earnings-to-growth ratio under a half — for a business re-accelerating on the rate and market tailwind, roughly twenty per cent below the analyst median. That combination of a fair-to-attractive price, a strong driver, and a Financials tailwind amplifies the medium-horizon signal to a strong buy.

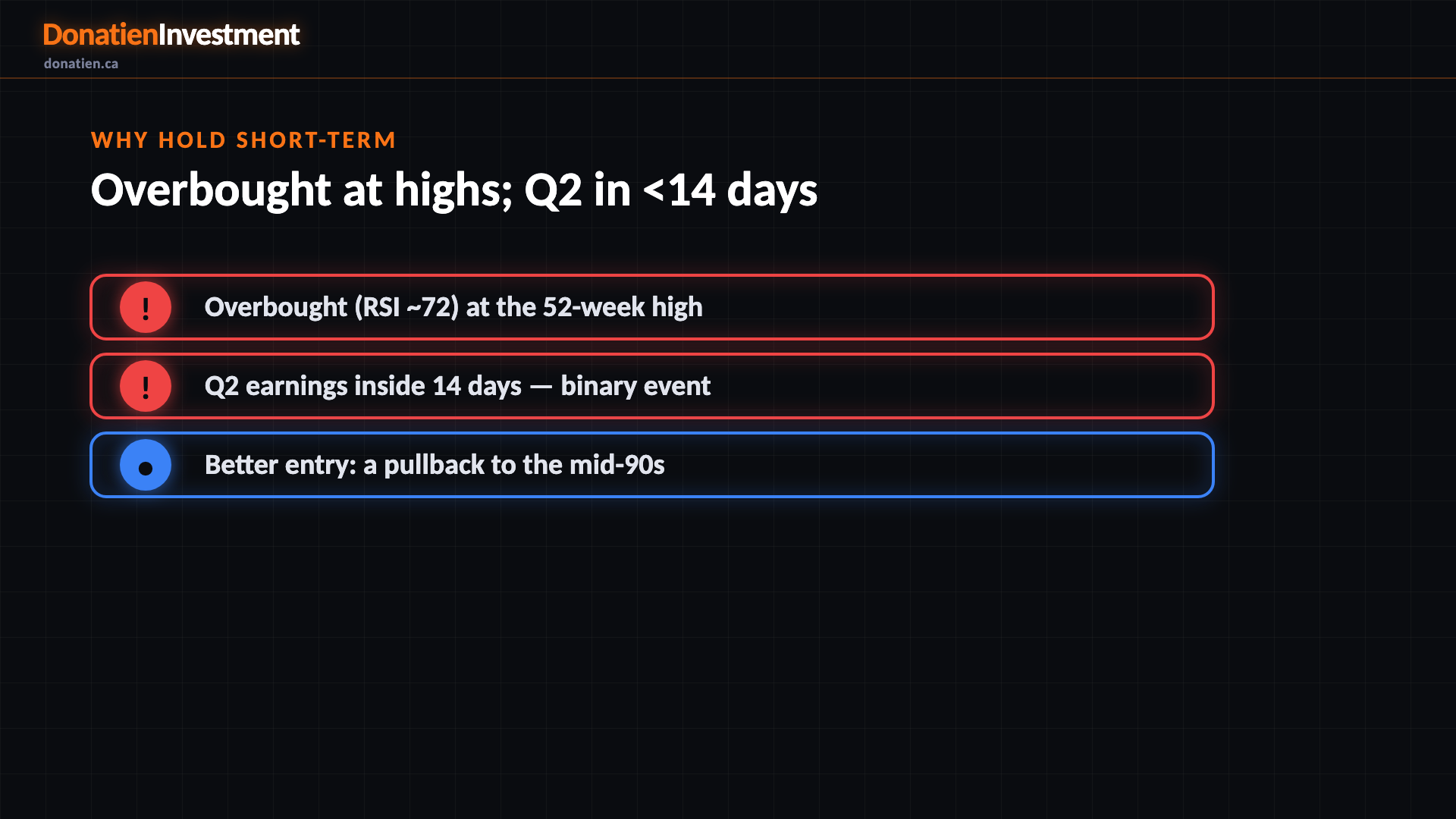

Why hold short-term

Here's the near-term caveat. The stock has run eleven per cent in a fortnight into overbought territory — a daily relative-strength reading around seventy-two — right at its fifty-two-week high, and Q2 earnings land in under two weeks. Chasing an overbought name at its highs ahead of a binary print is exactly what the framework counsels against short-term, so it's a hold: wait for a pullback toward the ninety-fours or a clean post-earnings hold.

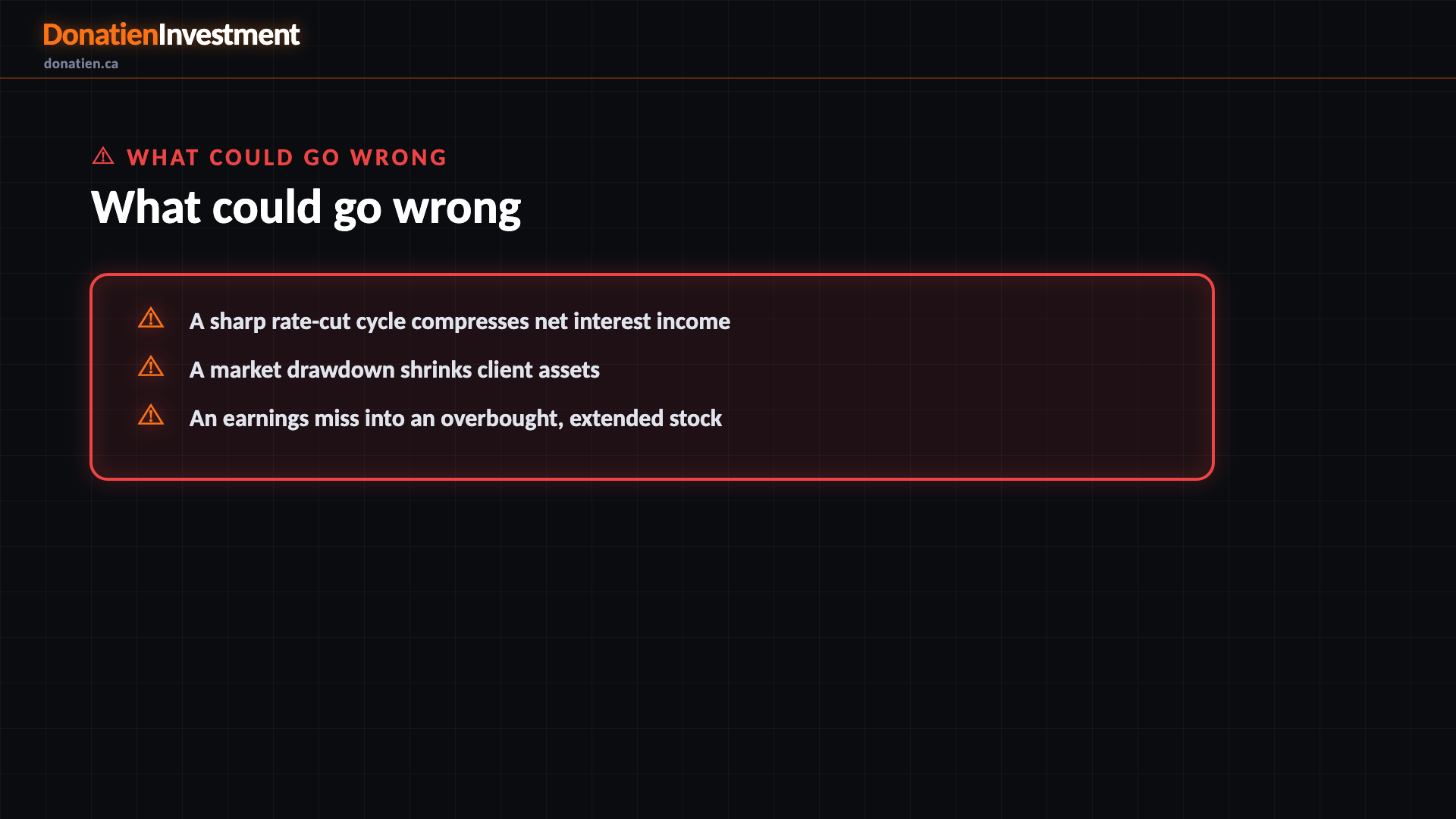

What could go wrong

A sharp rate-cut cycle compresses net interest income. A market drawdown shrinks client assets. An earnings miss into an overbought, extended stock.

Risk vs Reward

The report weights three twelve-month paths with a positive skew. The base case — most likely at 55% — sees Schwab around US$118 on steady earnings re-acceleration, about 16% above today. The bull at 25% reaches US$137 if net interest income and asset inflows beat and the multiple re-rates. The bear at 20% takes it to US$85 on a sharp rate-cut cycle or a market drawdown that de-rates the extended stock.

The verdict

The bottom line: a high-quality, reasonably-valued asset-gatherer re-accelerating on the rate and market tailwind — the medium-term signal is a strong buy. But it's run eleven per cent into overbought territory at its highs, days before a binary Q2 print, so the near-term entry is poor. Hold, and wait for a pullback toward the mid-nineties or a clean post-earnings hold rather than chasing here.

Read the full report on donatien.ca →{kind=link}

{kind=link}