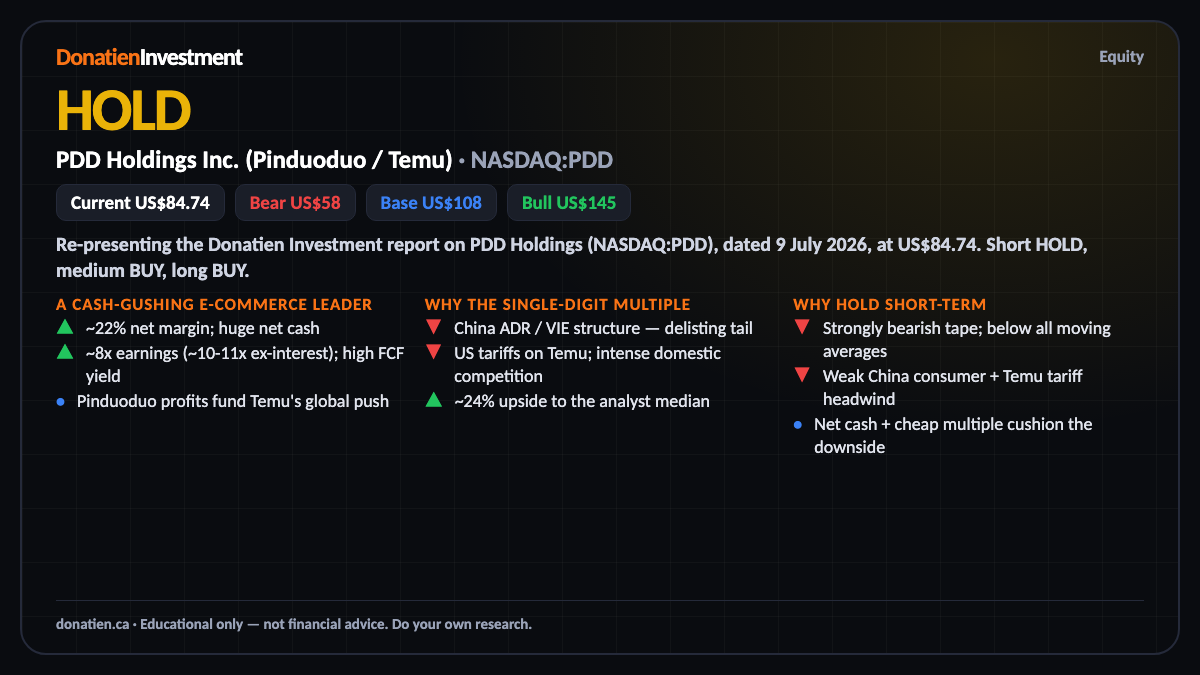

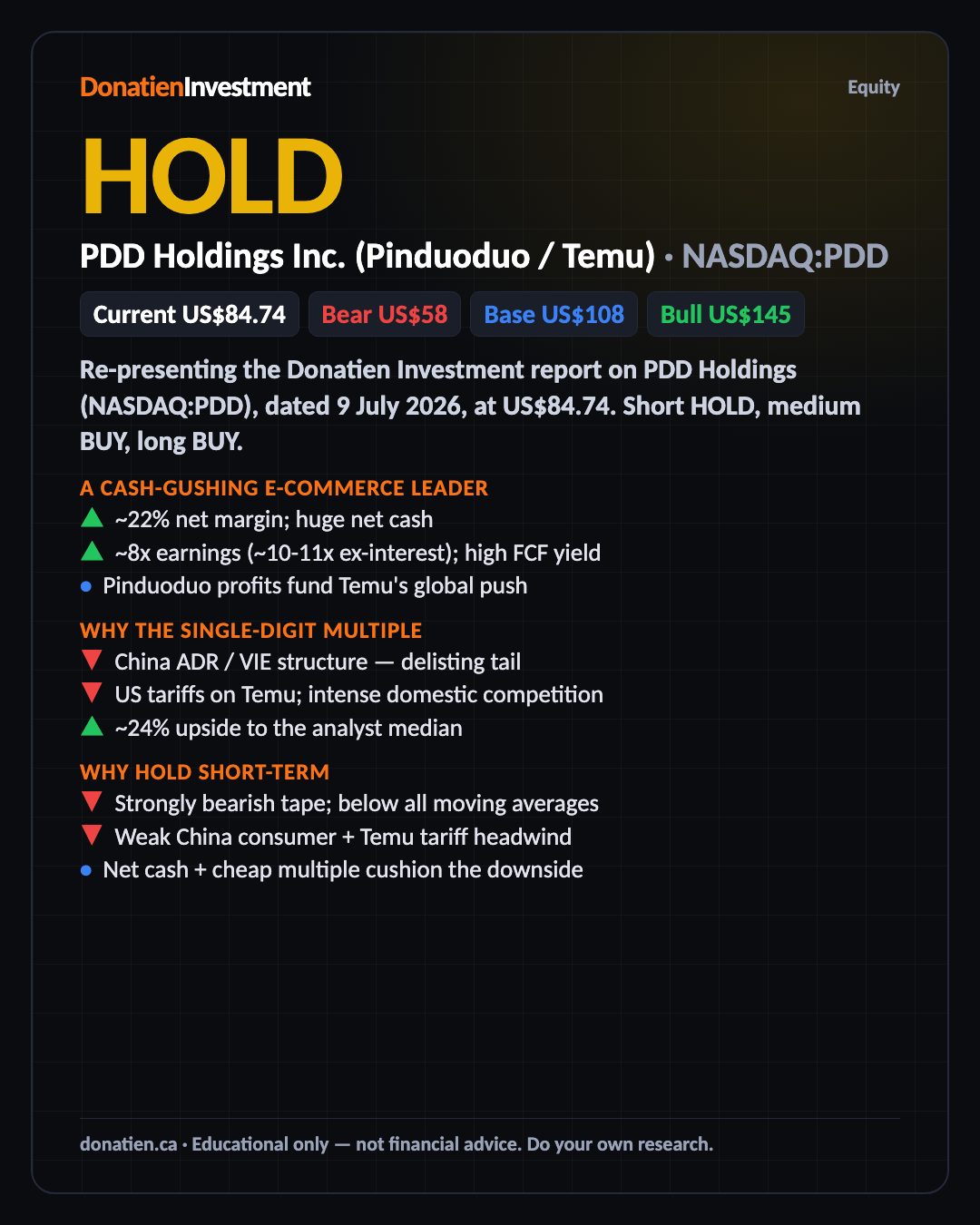

PDD Holdings Inc. (Pinduoduo / Temu) (NASDAQ:PDD) HOLD

PDD Holdings — Pinduoduo and Temu — is statistically very cheap at about eight times earnings with huge net cash and a twenty-per-cent-plus margin. But it's a Chinese ADR with a weak tape, tariff risk on Temu, and intense competition, so it's a short-term hold; the value case rates a medium and long BUY.

Re-presenting the Donatien Investment report on PDD Holdings (NASDAQ:PDD), dated 9 July 2026, at US$84.74. Short HOLD, medium BUY, long BUY.

A cash-gushing e-commerce leader

PDD runs Pinduoduo, a top-three Chinese e-commerce platform built on rock-bottom prices, and Temu, its fast-growing cross-border discount marketplace. The domestic marketplace is highly profitable — a twenty-two per cent net margin — and funds heavy investment in the loss-making but rapidly-scaling Temu. It holds enormous net cash. On any fundamental screen this is a very cheap, very profitable business.

Why the single-digit multiple

The eight-times multiple is not a bargain the market has overlooked — it's a risk discount. PDD is a Chinese ADR with a variable-interest-entity structure and a delisting tail; Temu faces US tariff and de-minimis changes that hit its economics; and there's an intense domestic price war with Alibaba, JD and Douyin. Those overhangs are real, which is why the value case is a medium and long buy, not a short-term one.

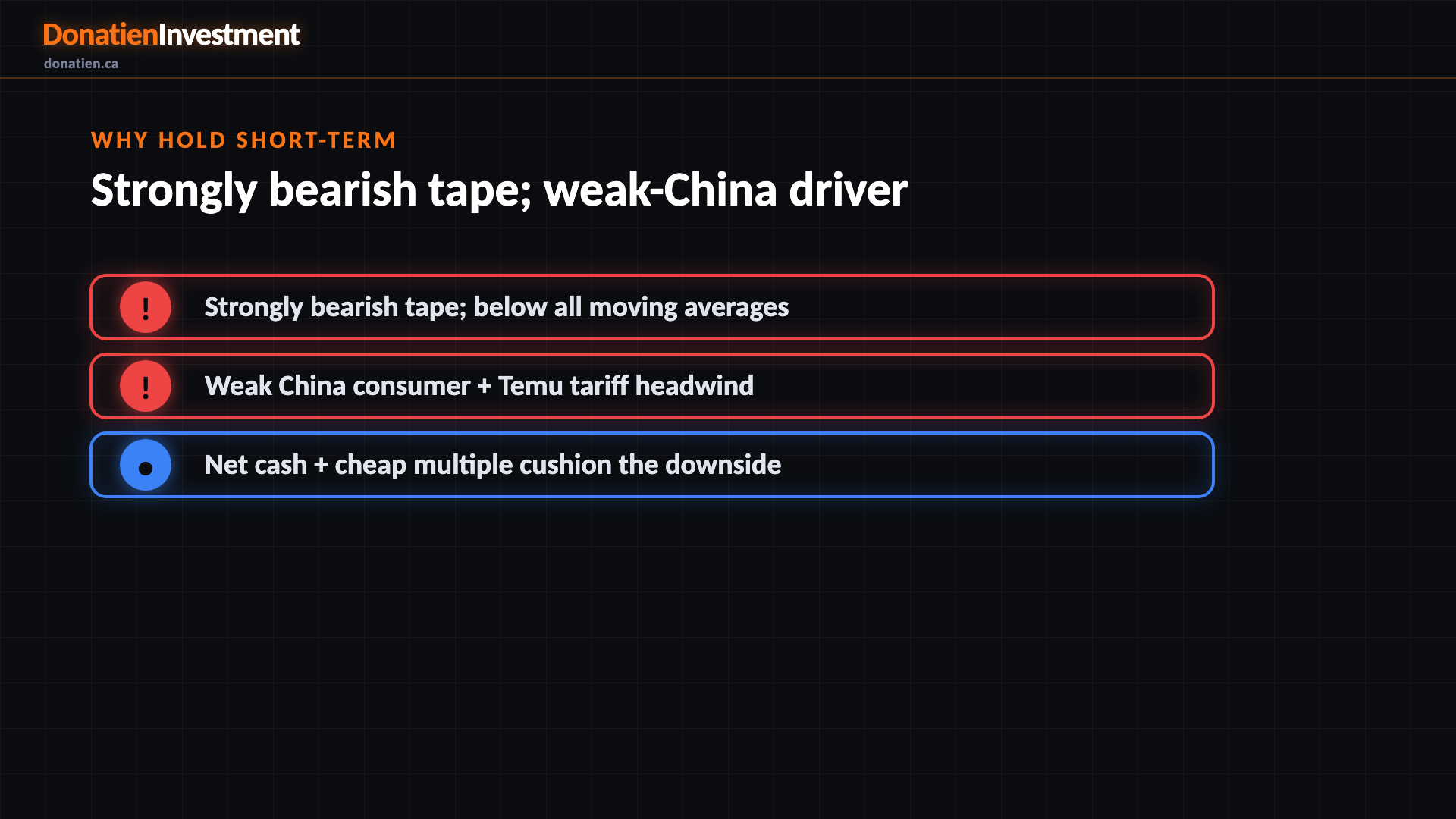

Why hold short-term

Short-term it's a hold because the tape is strongly bearish — a downtrend that's more than halved the stock, now trying to base — and the driver is a headwind, with a weak Chinese consumer and the tariff overhang on Temu. The cheap valuation and net cash cushion the downside, but there's no entry edge until the tape or the driver turns. This is deep value for the patient, not a short-term trade.

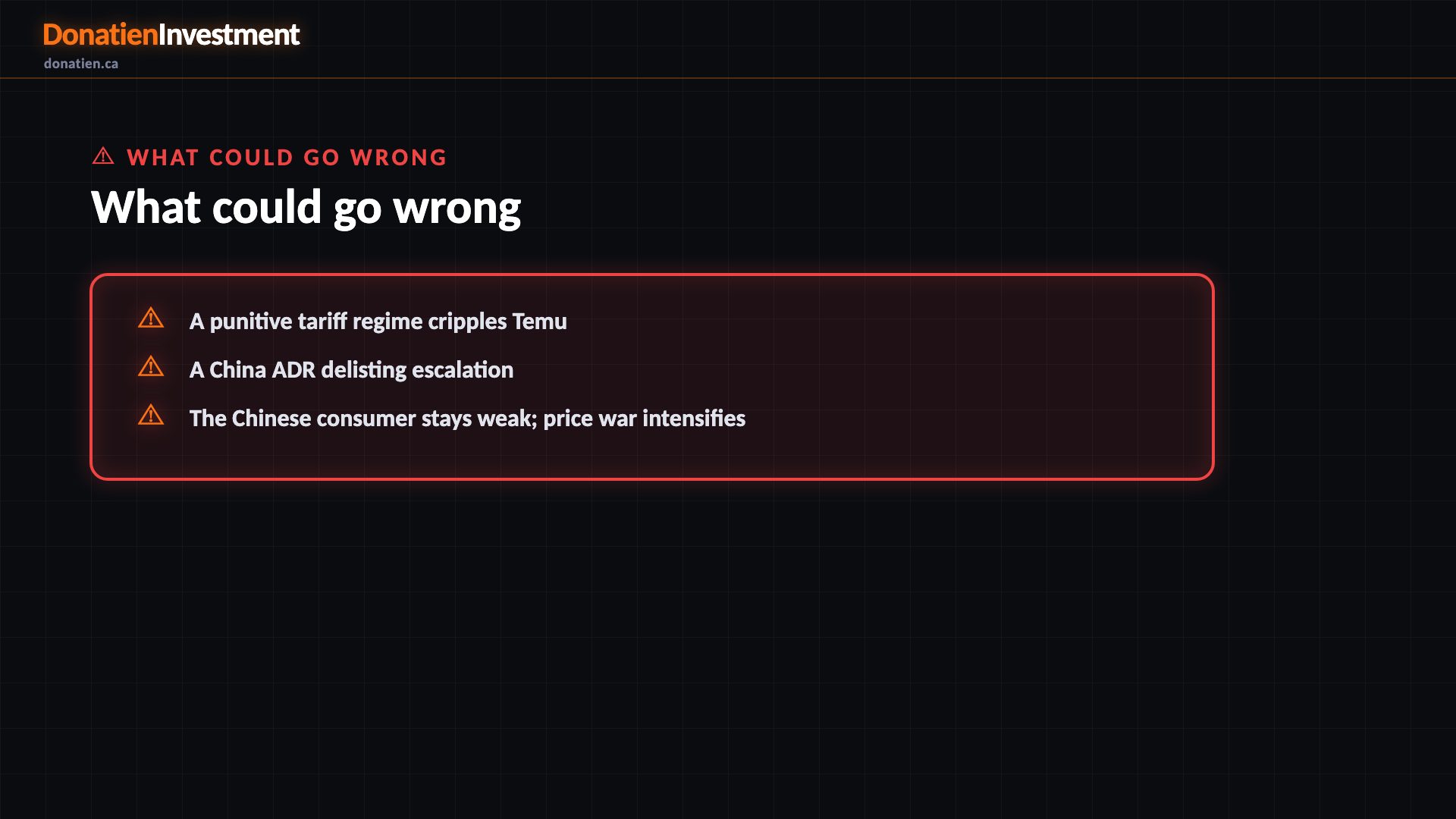

What could go wrong

A punitive tariff regime cripples Temu. A China ADR delisting escalation. The Chinese consumer stays weak; price war intensifies.

Risk vs Reward

The report weights three twelve-month paths — a wide, high-variance distribution. The base case — most likely at 50% — sees PDD around US$108 as domestic profits hold, Temu stabilises, and the multiple normalises modestly, about 27% above today. The bull at 25% reaches US$145 if China stimulus lifts the consumer and tariff fears ease. The bear at 25% takes it to US$58 if a punitive tariff regime cripples Temu or ADR/delisting risk escalates.

The verdict

The bottom line: statistically PDD is very cheap — eight times earnings, huge net cash, twenty-four per cent upside to the median — so the value case rates a medium and long buy for the patient. But it's a Chinese ADR with a weak tape, tariff risk on Temu, and a delisting tail, so short-term it's a hold with no entry edge until the driver or tape turns. Deep value, but size it small and eyes-open on the China risk.

Read the full report on donatien.ca →{kind=link}

{kind=link}