Macro Economics STAGFLATION-LITE

A hawkish Fed and re-accelerating inflation meet cooling growth and a live oil shock. Stagflation now leads at 38% — respect the higher-for-longer tape now, hold the inflation hedges for later.

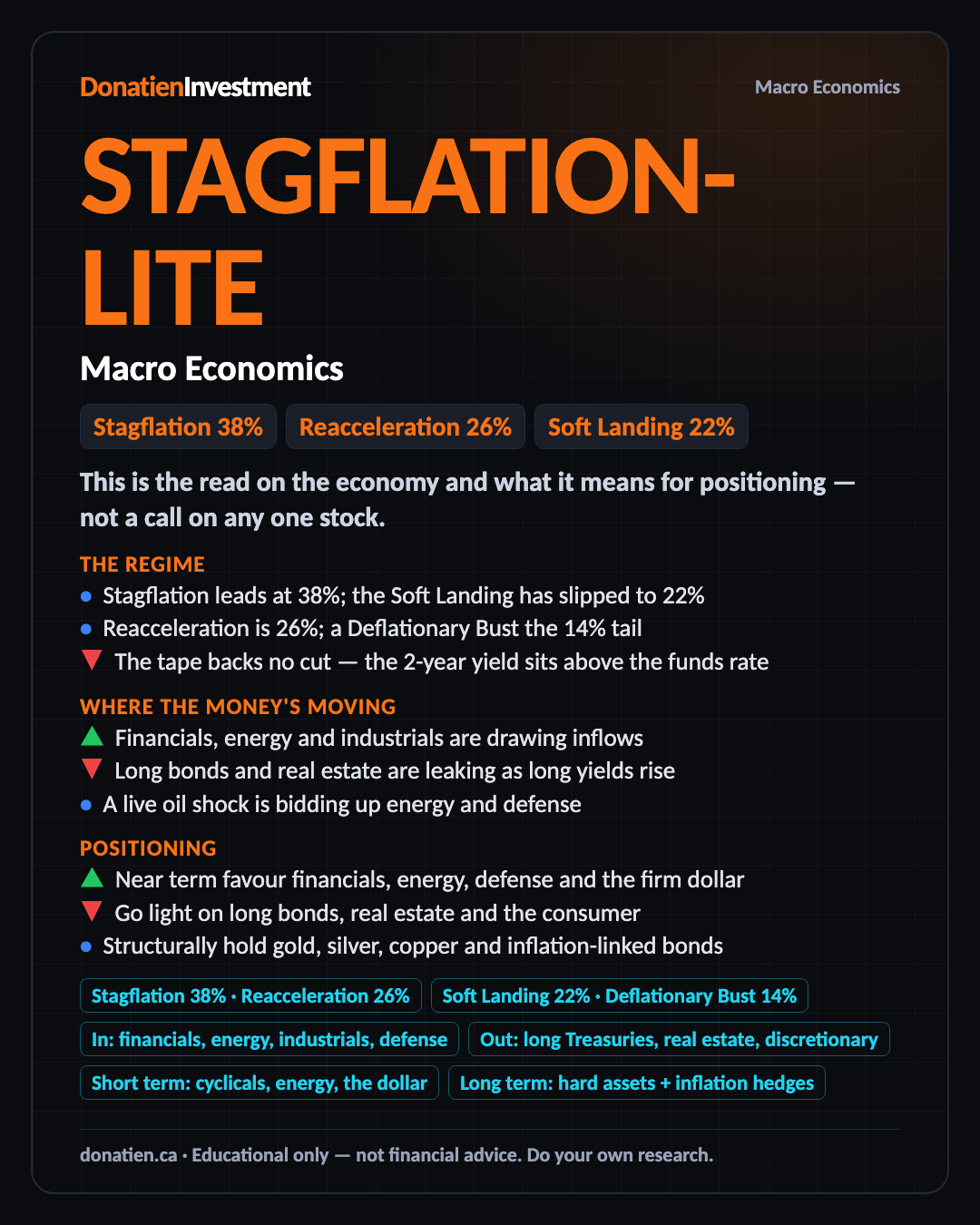

This is the read on the economy and what it means for positioning — not a call on any one stock. Four scenarios are always in play — Stagflation, a Reacceleration, a Soft Landing, and a Deflationary Bust — and this run the balance has tilted toward stagflation and higher-for-longer.

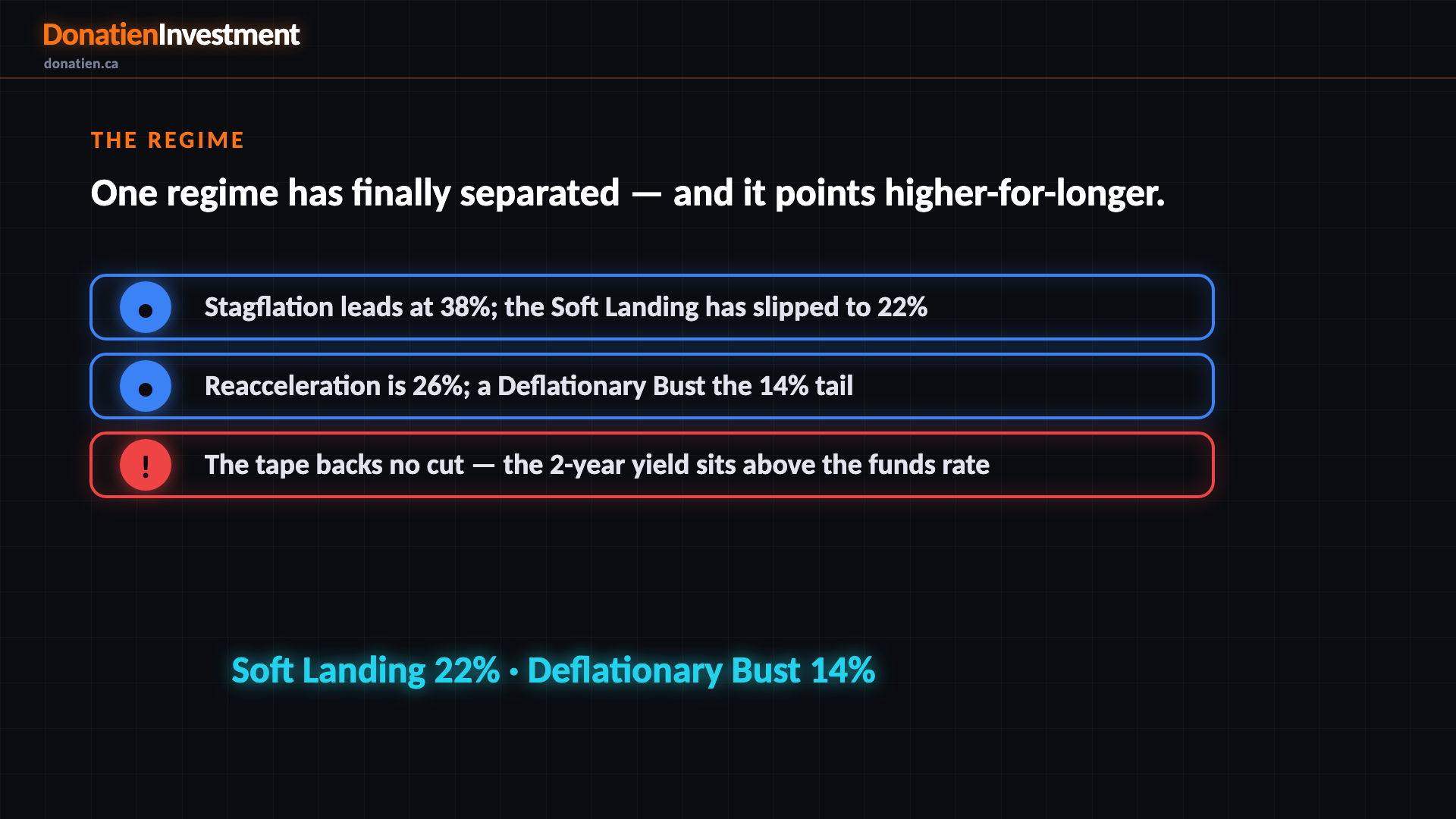

The regime

Four scenarios are always in play, and this run the balance tilted. Stagflation — growth slowing while inflation stays sticky — leads at 38%, as a hawkish Federal Reserve under its new chair meets re-accelerating prices. A reacceleration is 26%, a soft landing has slipped to 22%, and a deflationary bust is the 14% tail. Crucially, the tape confirms the hawkish read rather than fighting it: the two-year yield sits above the funds rate, the ten-year has risen to 4.56%, and the dollar is firm. Unlike the prior read, narrative and market now agree.

Stagflation 38% · Reacceleration 26% · Soft Landing 22% · Deflationary Bust 14%

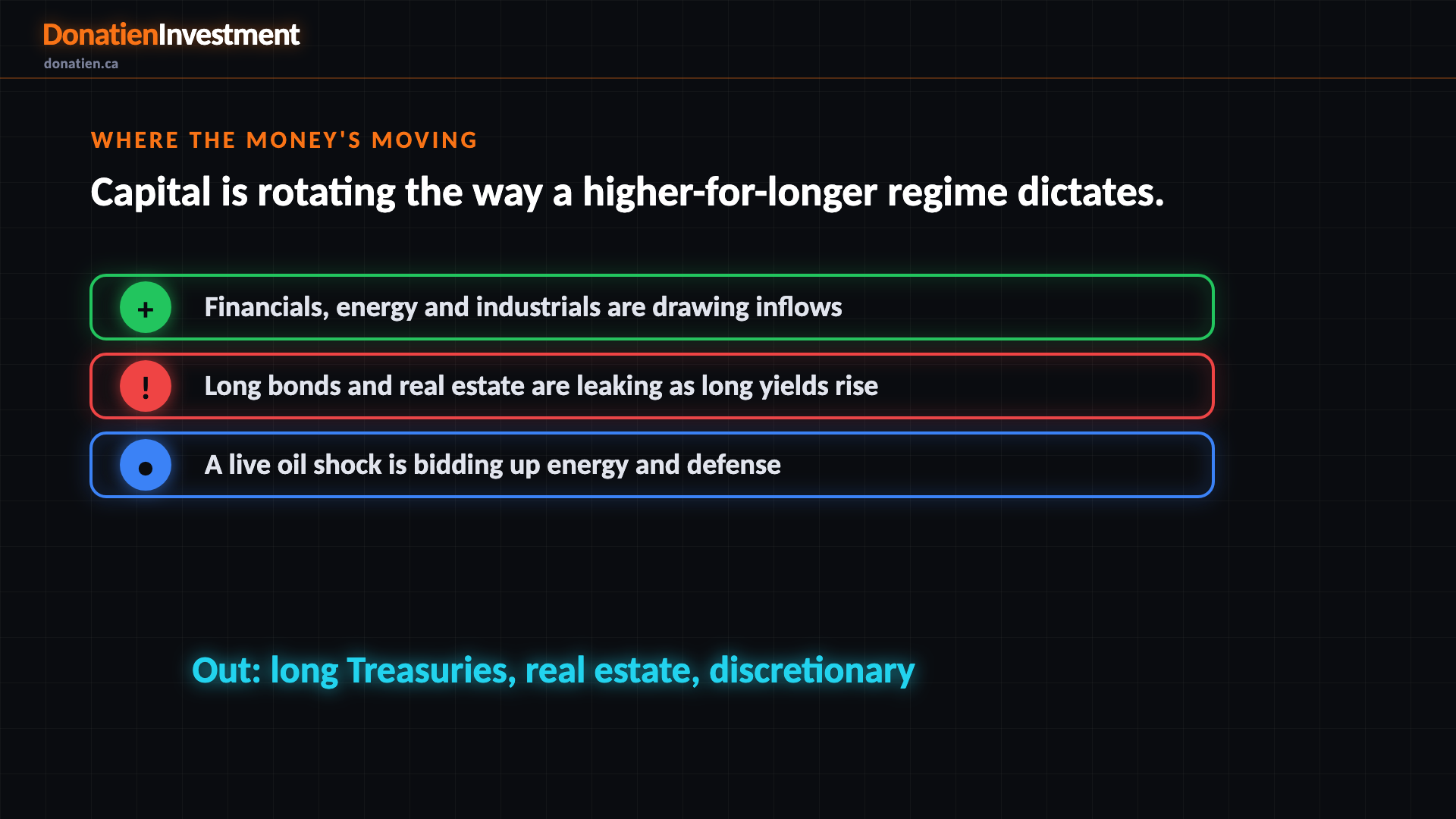

Where the money's moving

The money is moving the way a higher-for-longer regime dictates. Financials benefit from a steeper curve; energy is bid by the oil shock and scarcity; industrials ride reshoring and defense spending. On the other side, long-dated Treasuries and real estate are leaking as the thirty-year yield pushes to 5.06% and mortgages sit near 6.49%. The consumer softens as credit tightens. The fresh entrant is the Iran–Hormuz oil premium, which lifts energy and defense while dragging the global-trade-exposed corners of the market.

In: financials, energy, industrials, defense · Out: long Treasuries, real estate, discretionary

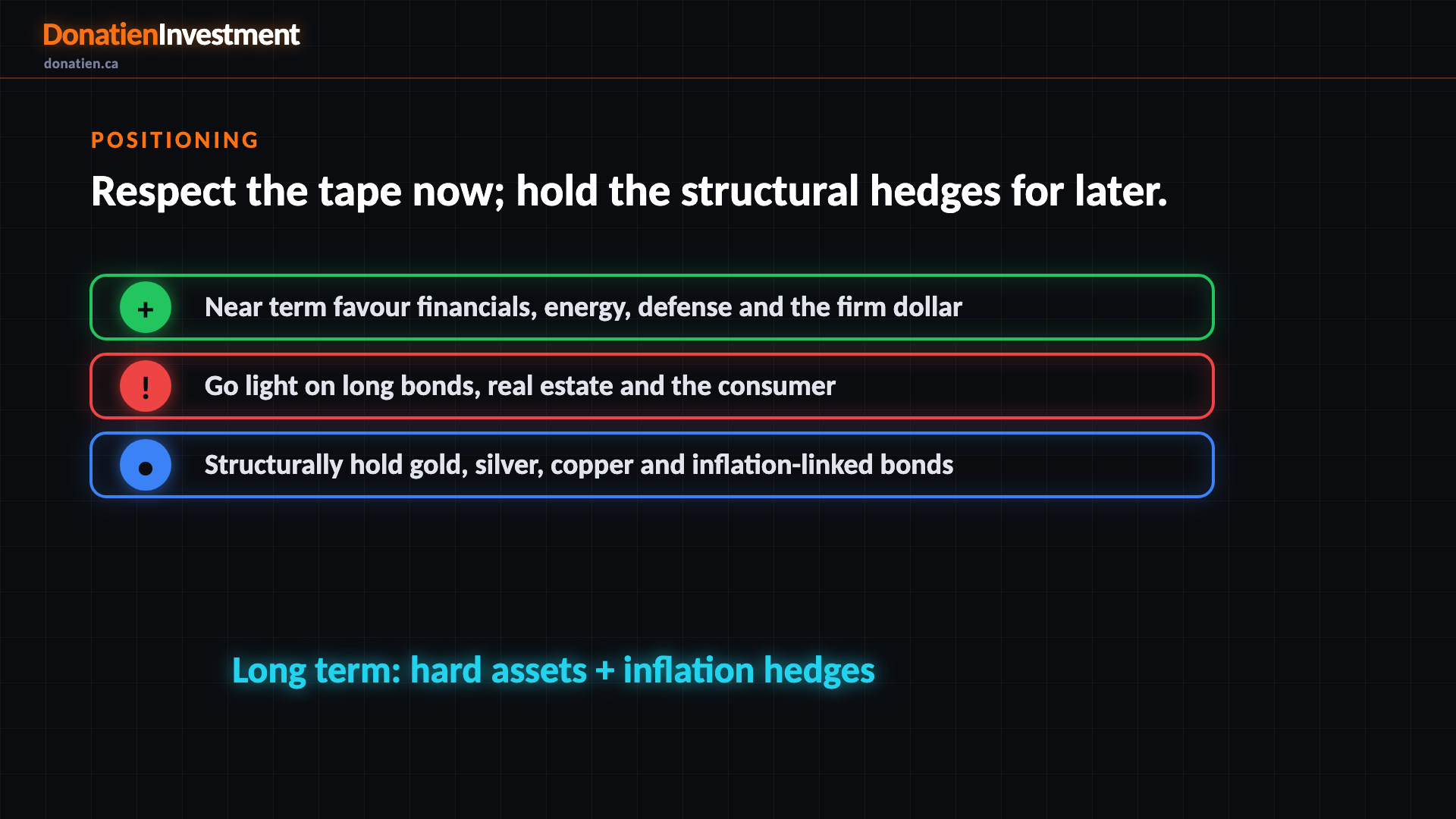

Positioning

Positioning splits by horizon. Near term, respect the tape: favour financials and energy, lean on the firm dollar, and go light on long-duration bonds, real estate and the consumer. Gold is capped short term by high real rates, though the Hormuz safe-haven bid offsets some of that. Longer term, hold the structural book — gold, silver and copper on debasement and electrification, inflation-protected bonds while prices stay sticky, and technology for the productivity trend, sized carefully for its concentration risk.

Short term: cyclicals, energy, the dollar · Long term: hard assets + inflation hedges

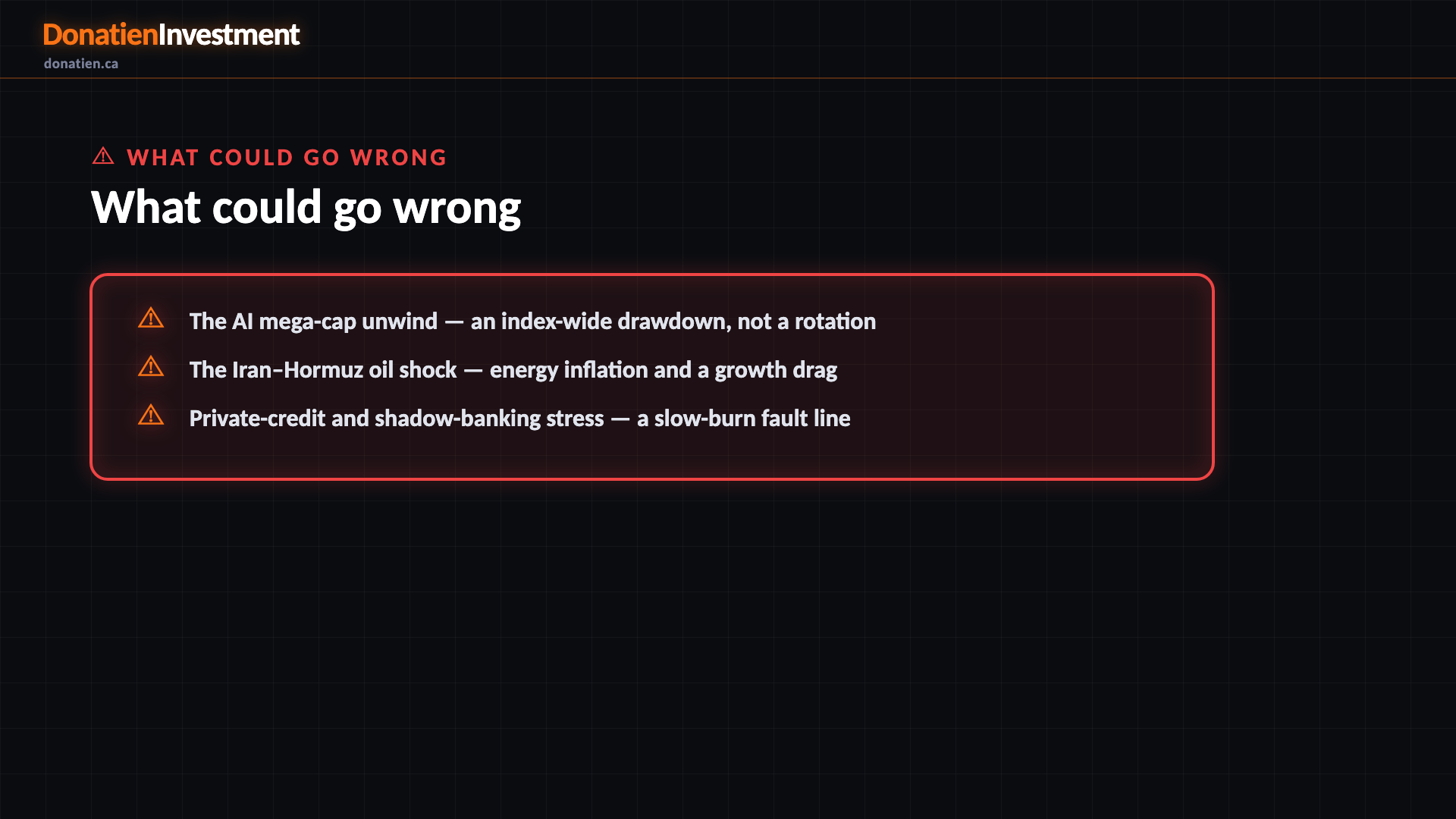

What could go wrong

The risks are loud and they cut both ways. The biggest tail is the one that's armed but not triggering: the S&P 500 is led by a handful of AI mega-caps making up roughly 41% of the index, on partly non-operating earnings — so a reversal there is an index-wide drawdown, not a tidy rotation, and breadth narrowed again this week. The Iran–Hormuz shock is a genuine two-way risk: it lifts energy but drags growth, and a closure of the strait would be a sharp escalation. And private credit remains the cycle's untested fault line as higher-for-longer squeezes refinancing.

Risk vs Reward

The four scenarios have spread out from the prior dead heat. Stagflation now leads at 38%, a reacceleration is 26%, a soft landing has slipped to 22% as the disinflation case weakened, and a deflationary bust is the 14% tail. The lead is modest, not decisive — but for the first time in weeks one regime has separated, and it points toward higher-for-longer.

The verdict

The honest read is a mildly stagflationary, higher-for-longer economy: sticky-to-rising inflation, a hawkish Fed that may still hike, cooling growth, and a live oil shock on top. Near term, respect the tape — favour financials and energy, lean on the firm dollar, go light on long bonds and rate-sensitive real estate. Longer term, hold the structural inflation hedges: gold, silver, copper and inflation-protected bonds. The next tells are the inflation print on the 14th and the Iran–Hormuz situation, which could force an earlier update.

Read the full report on donatien.ca →{kind=link}

{kind=link}