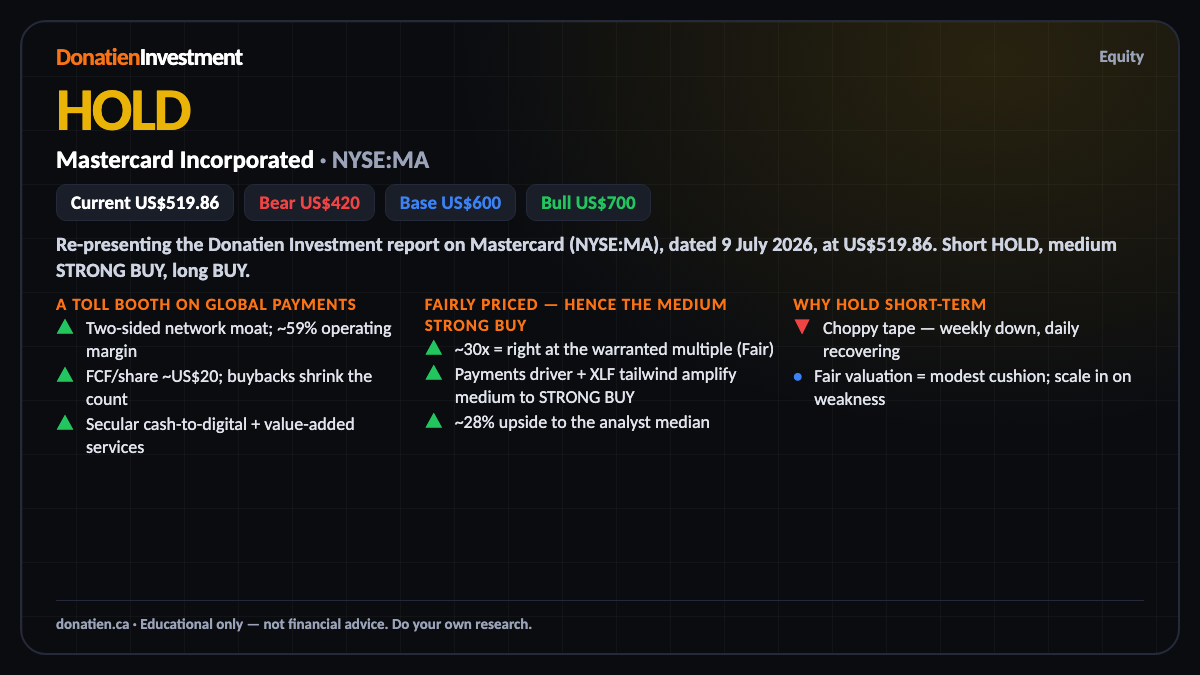

Mastercard Incorporated (NYSE:MA) HOLD

Mastercard is a near-unassailable, capital-light payments network — elite margins, a deep moat, ~28% upside to the analyst median. At about thirty times earnings it's fairly (not cheaply) priced, so it's a hold on a choppy tape short-term; the medium-term signal is STRONG BUY.

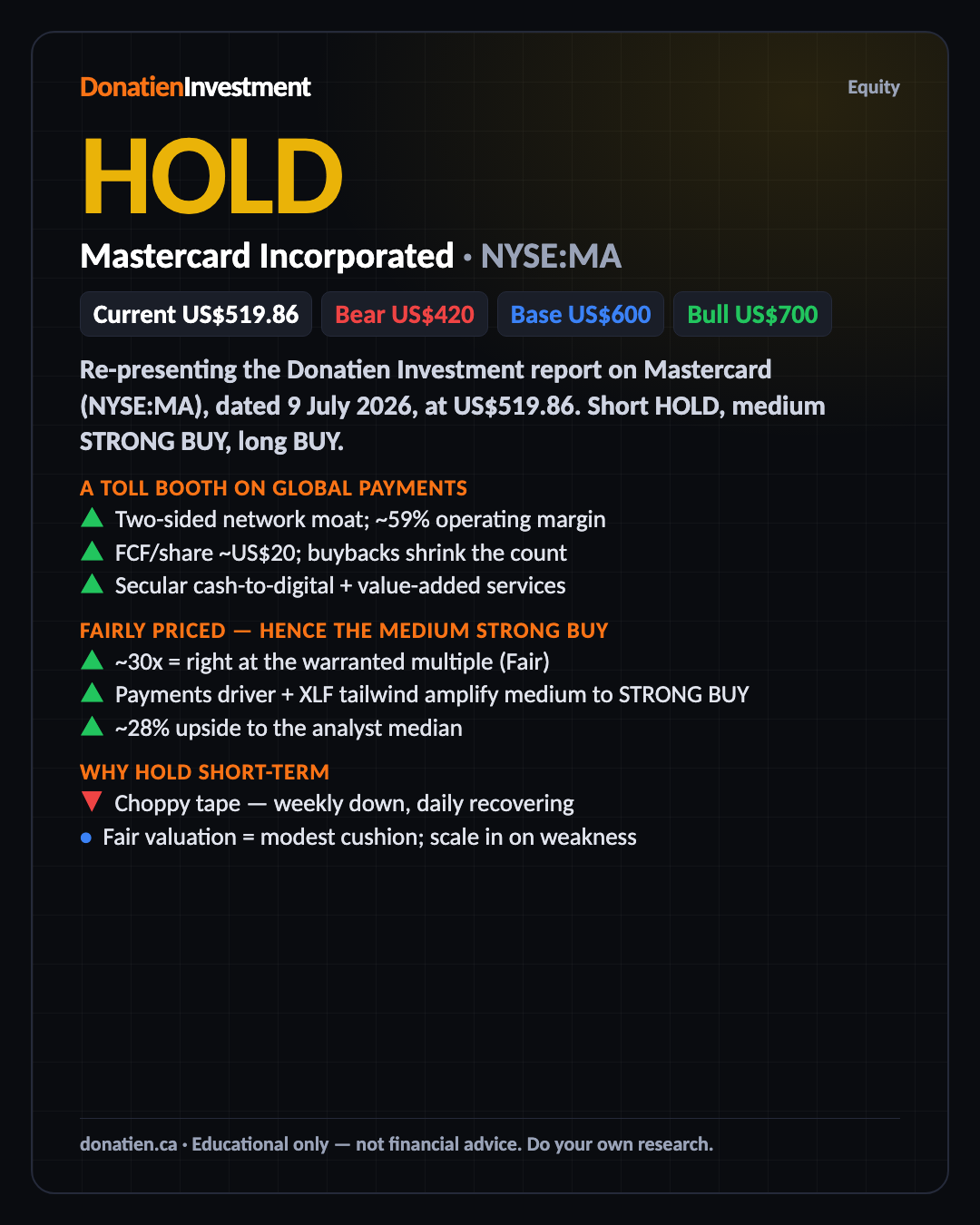

Re-presenting the Donatien Investment report on Mastercard (NYSE:MA), dated 9 July 2026, at US$519.86. Short HOLD, medium STRONG BUY, long BUY.

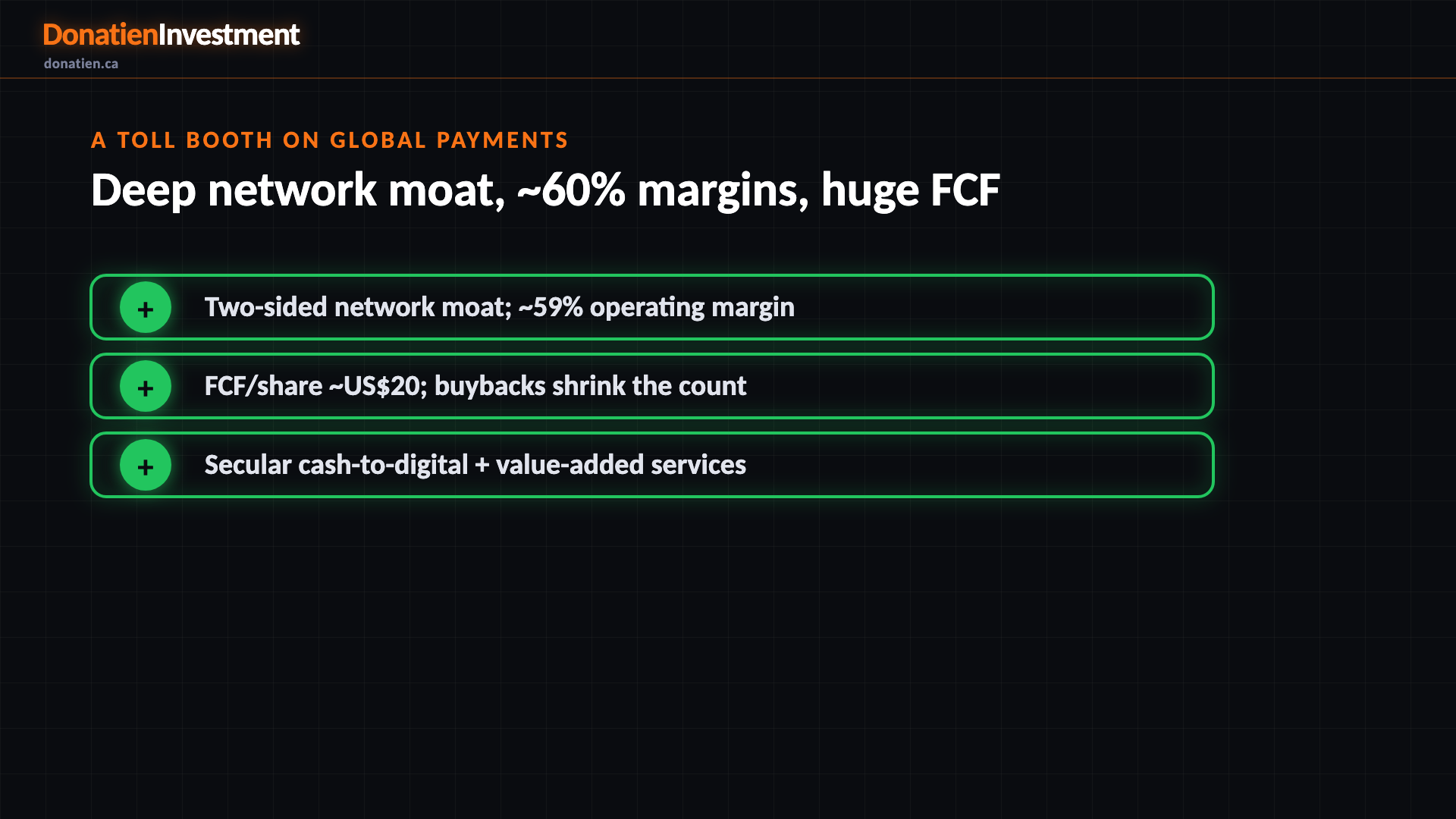

A toll booth on global payments

Mastercard runs one of the world's two dominant payment networks, taking a small fee on an enormous volume of transactions. It's capital-light with roughly sixty per cent operating margins, prodigious free cash flow, and a near-unassailable two-sided network moat with real pricing power. It grows with the secular shift from cash to electronic payments, plus fast-growing value-added services. This is one of the highest-quality businesses in the market.

Fairly priced — hence the medium STRONG BUY

On our anchor, thirty times earnings is right at the multiple a capital-light compounder of this quality warrants — Fair, not expensive. Combine a fair price with a strong payments driver, a Financials sector tailwind, and elite quality, and the medium-horizon signal amplifies to a strong buy, with roughly twenty-eight per cent upside to the analyst median. Long term it's a plain buy because the price is fair rather than a bargain.

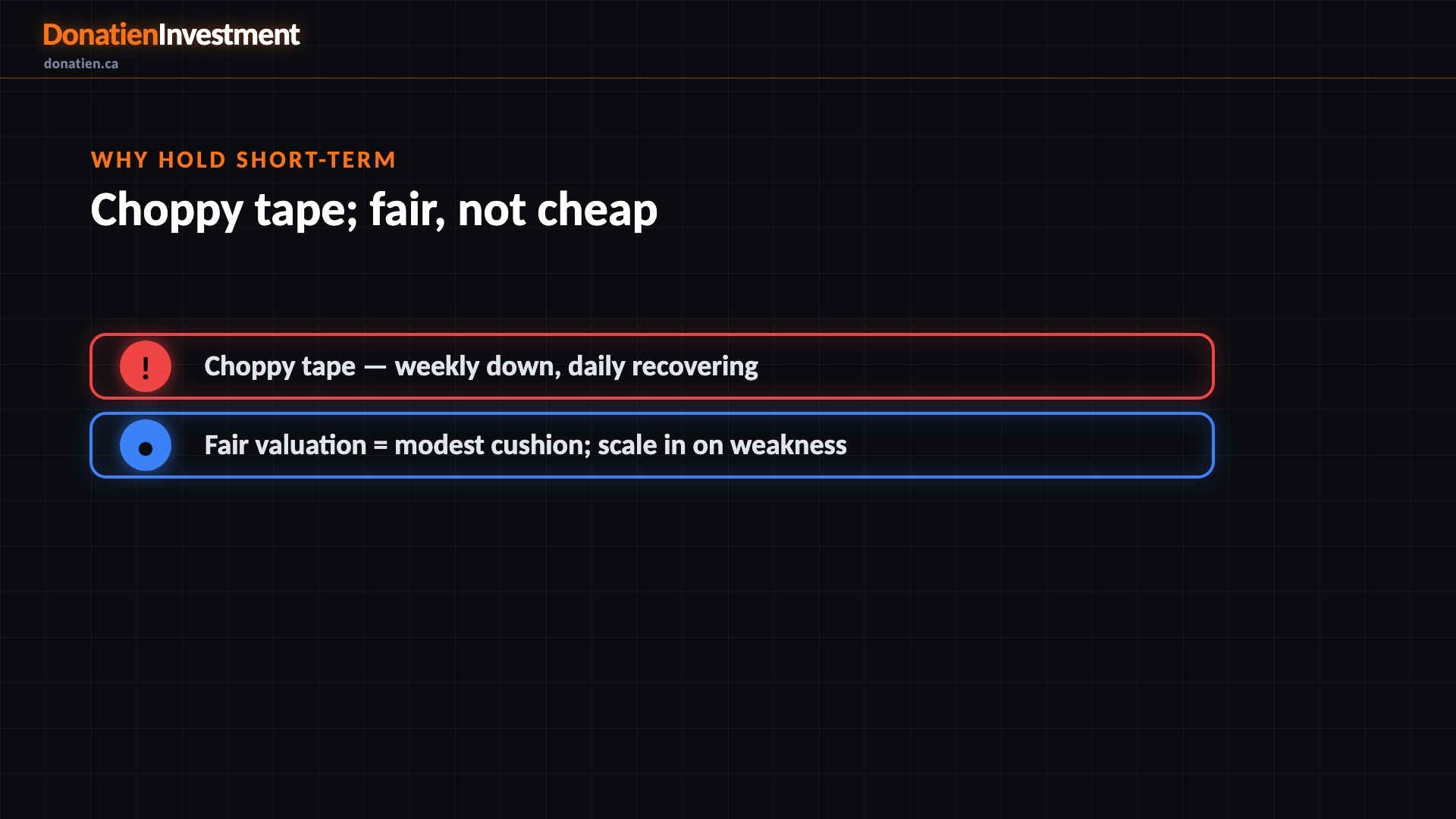

Why hold short-term

The reason short-term is a hold: the tape is choppy — a longer uptrend but a weekly downtrend and an intraday pullback — and at a fair valuation there's limited cushion for a fresh entry here. The medium-term thesis is a strong buy, so the read is to scale in on weakness rather than chase, with a reclaim of the mid-five-thirties the technical confirmation.

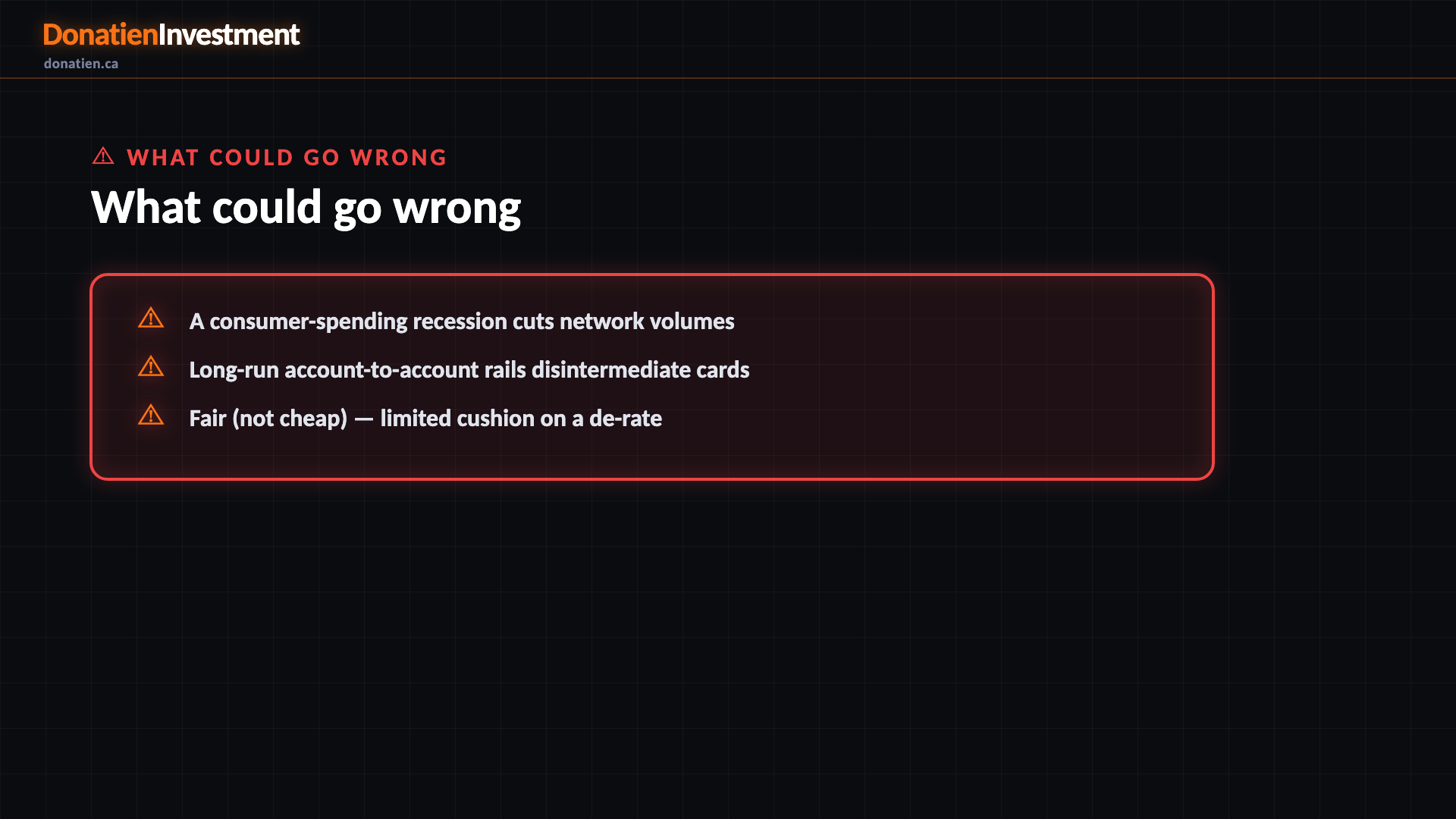

What could go wrong

A consumer-spending recession cuts network volumes. Long-run account-to-account rails disintermediate cards. Fair (not cheap) — limited cushion on a de-rate.

Risk vs Reward

The report weights three twelve-month paths with a positive skew. The base case — most likely at 55% — sees Mastercard around US$600 on double-digit compounding at a fair multiple, about 15% above today. The bull at 25% reaches US$700 if spending stays firm and value-added services accelerate. The bear at 20% takes it to US$420 on a consumer-spending recession that cuts volumes and de-rates the multiple.

The verdict

The bottom line: an elite, capital-light payments network at a fair price with a secular tailwind. The medium-term signal is a strong buy — fair valuation plus a payments driver plus a Financials tailwind. Short-term it's a hold on a choppy tape with limited cushion, so scale in on weakness rather than chase; a reclaim of the mid-five-thirties would confirm the entry.

Read the full report on donatien.ca →{kind=link}

{kind=link}