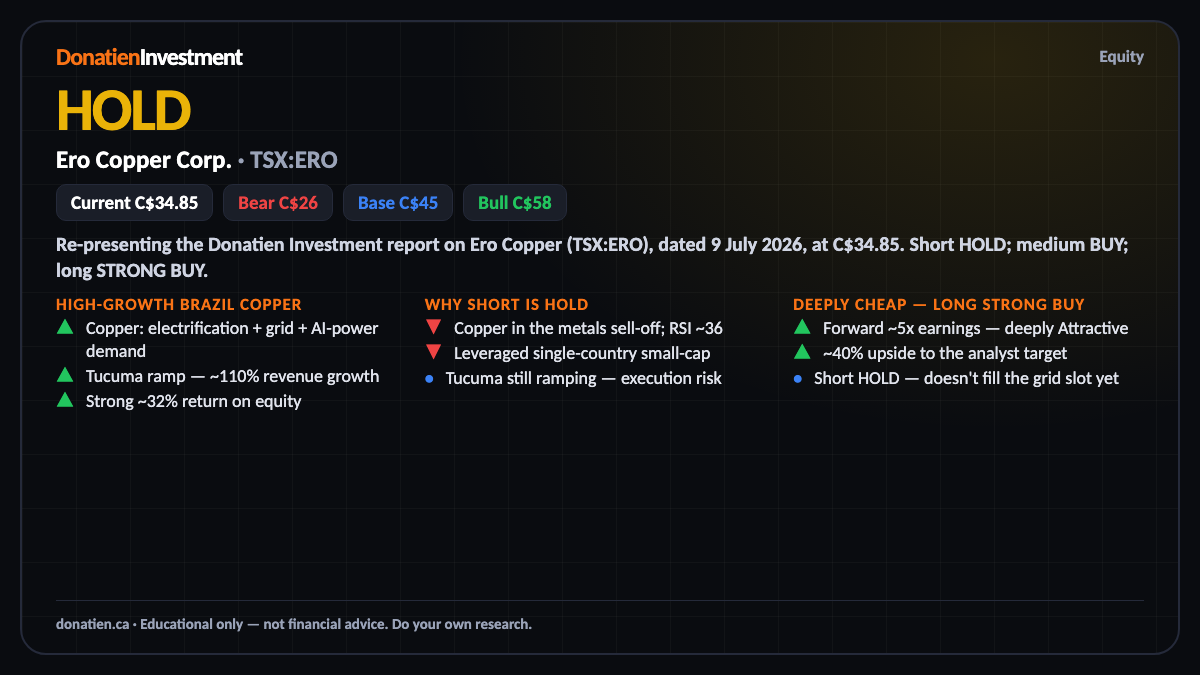

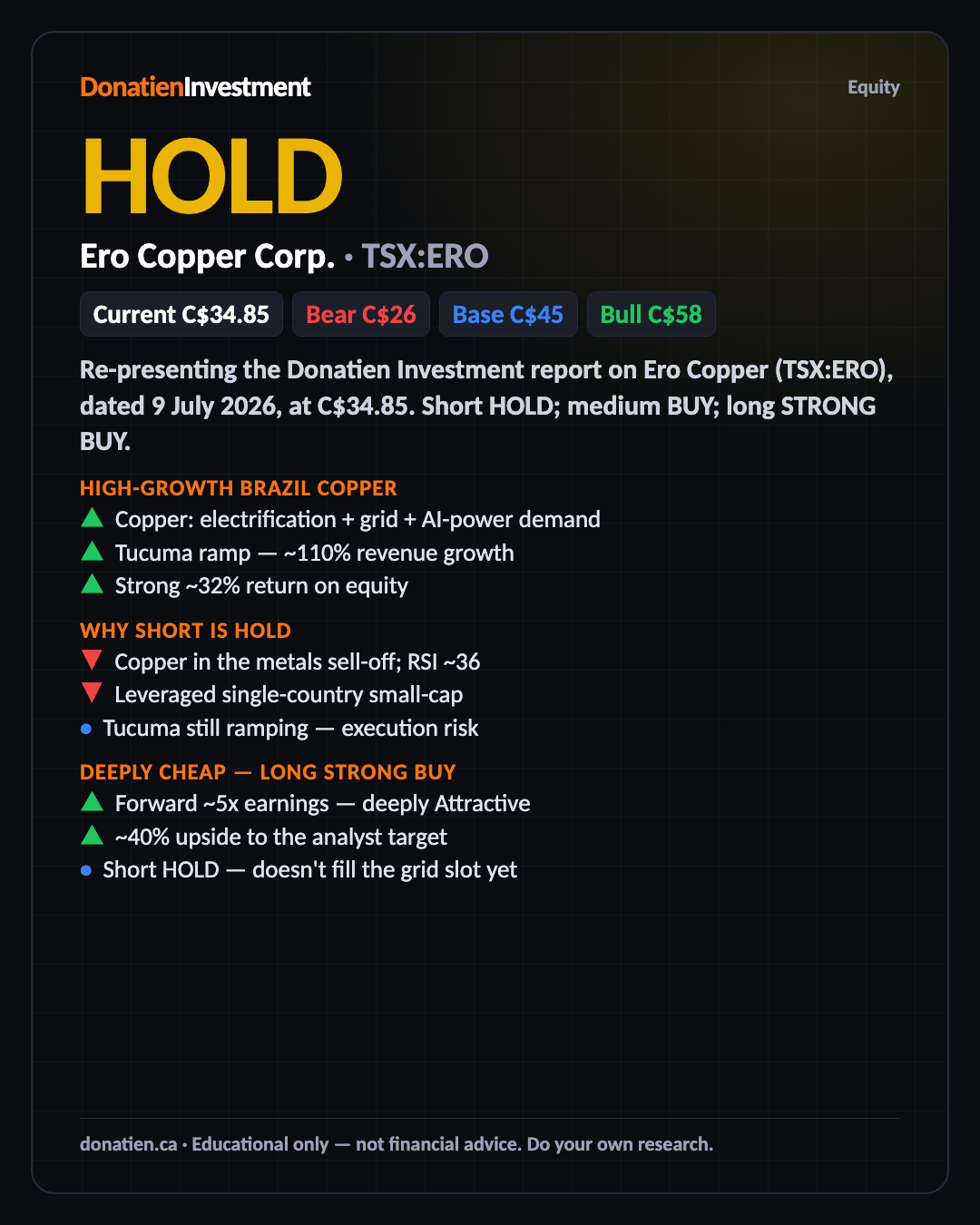

Ero Copper Corp. (TSX:ERO) HOLD

Ero Copper is a high-growth Brazilian copper producer, joining our watchlist as a Stock-Finder bench promotion. It's deeply cheap — a forward five times earnings, a thirty-two per cent return on equity, with the Tucuma mine ramping. But copper is caught in the metals sell-off, so the near-term call is HOLD; the long-horizon call is a STRONG BUY for risk-tolerant capital.

Re-presenting the Donatien Investment report on Ero Copper (TSX:ERO), dated 9 July 2026, at C$34.85. Short HOLD; medium BUY; long STRONG BUY. First report — a new watchlist add.

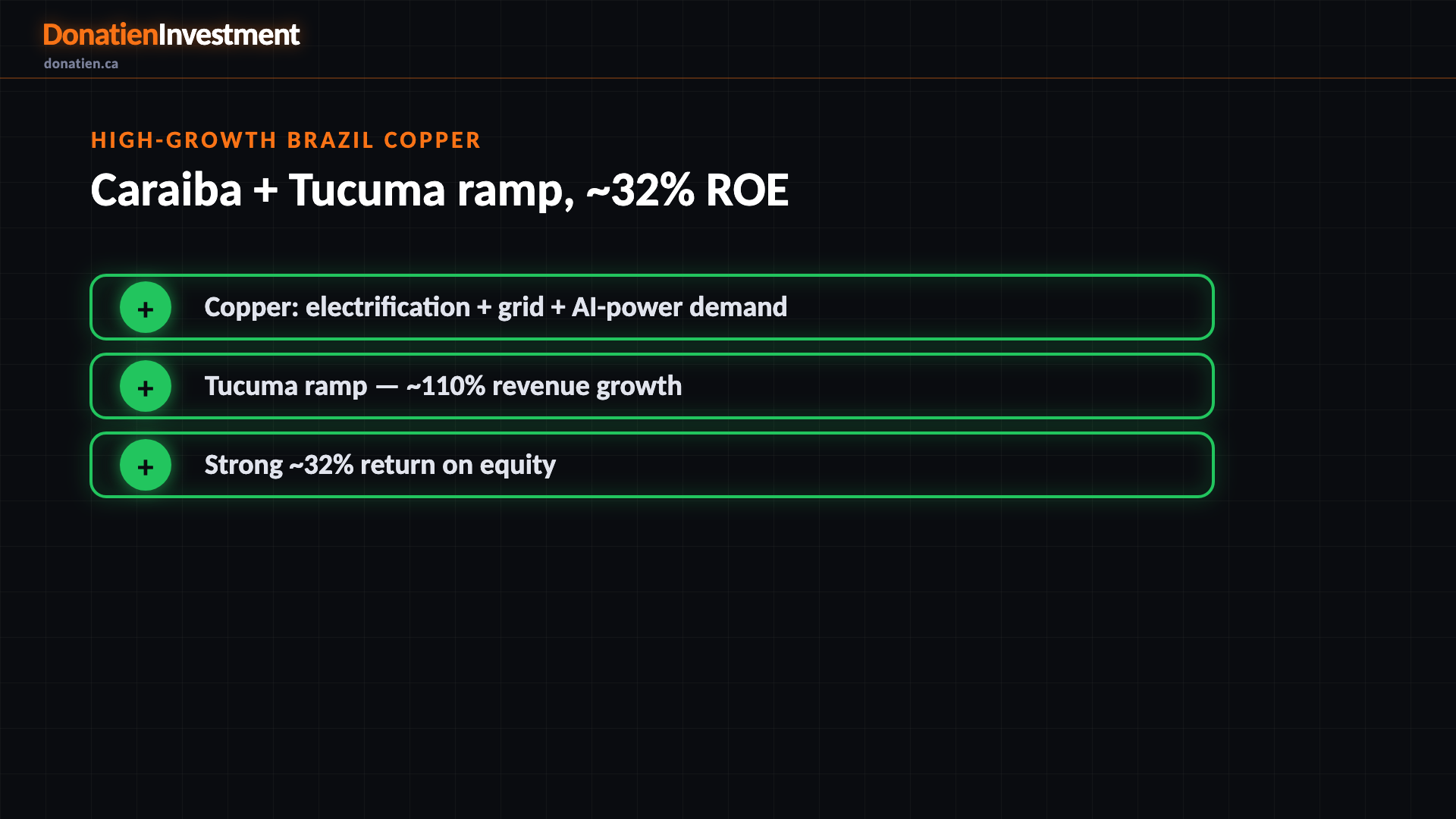

High-growth Brazil copper

Ero Copper offers leveraged exposure to copper — the metal at the centre of electrification, grid build-out and data-center power. Its established Caraiba operations plus the newly-ramping Tucuma mine are driving triple-digit revenue growth, at a strong thirty-two per cent return on equity. It joins our watchlist here as a Stock-Finder bench promotion, to test the empty Materials-Canada slot in our model portfolio grid.

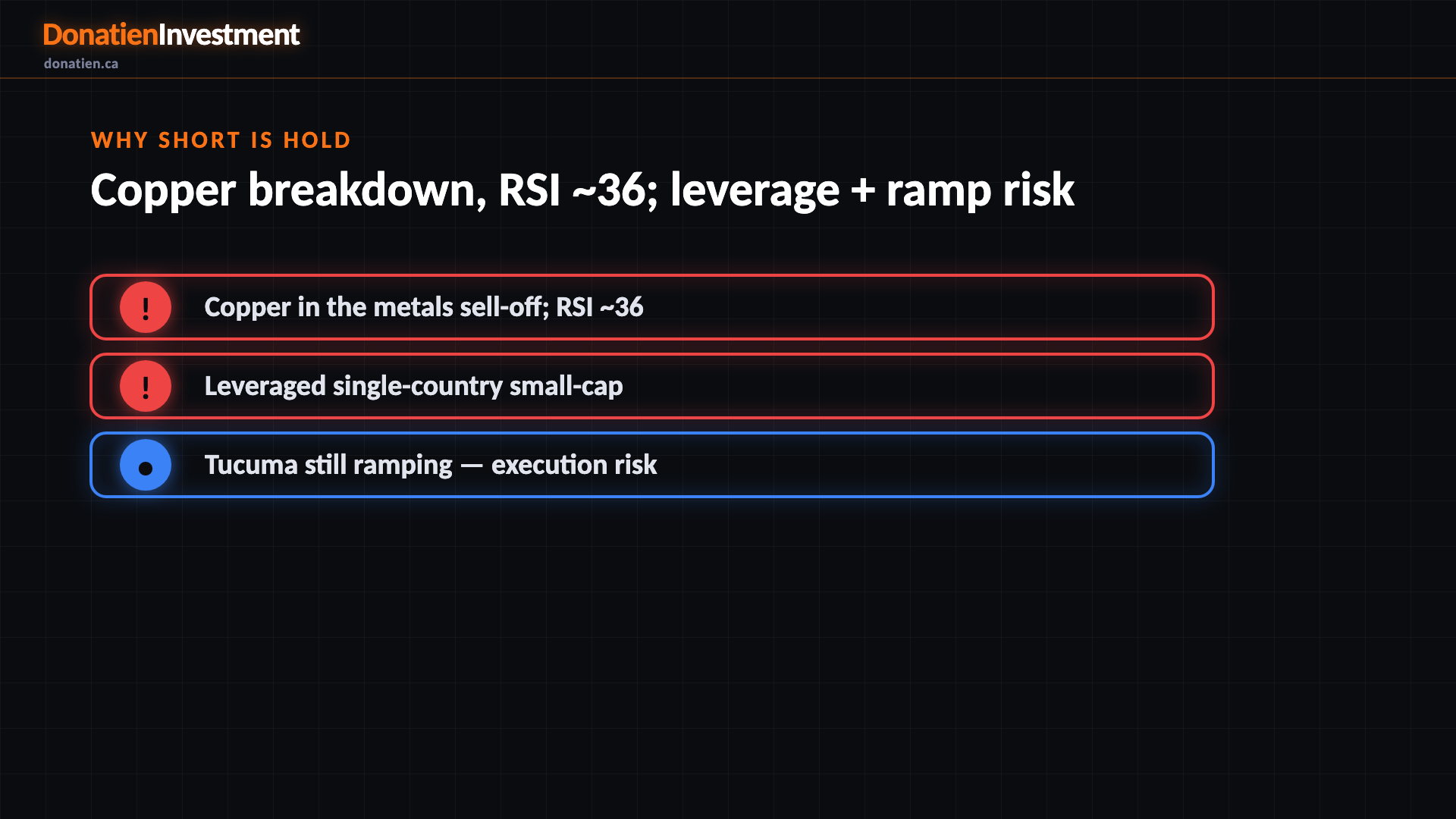

Why short is HOLD

Here's why the near-term call is HOLD. Copper has been dragged into the broader metals sell-off — Ero's chart shows a daily support breakdown, relative-strength index around thirty-six, an hourly strong downtrend. And this is a leveraged, single-country small-cap still ramping Tucuma, so the risks are real: net debt, execution, Brazil jurisdiction. Our price-trend overlay caps the short. Near oversold, but no turn yet.

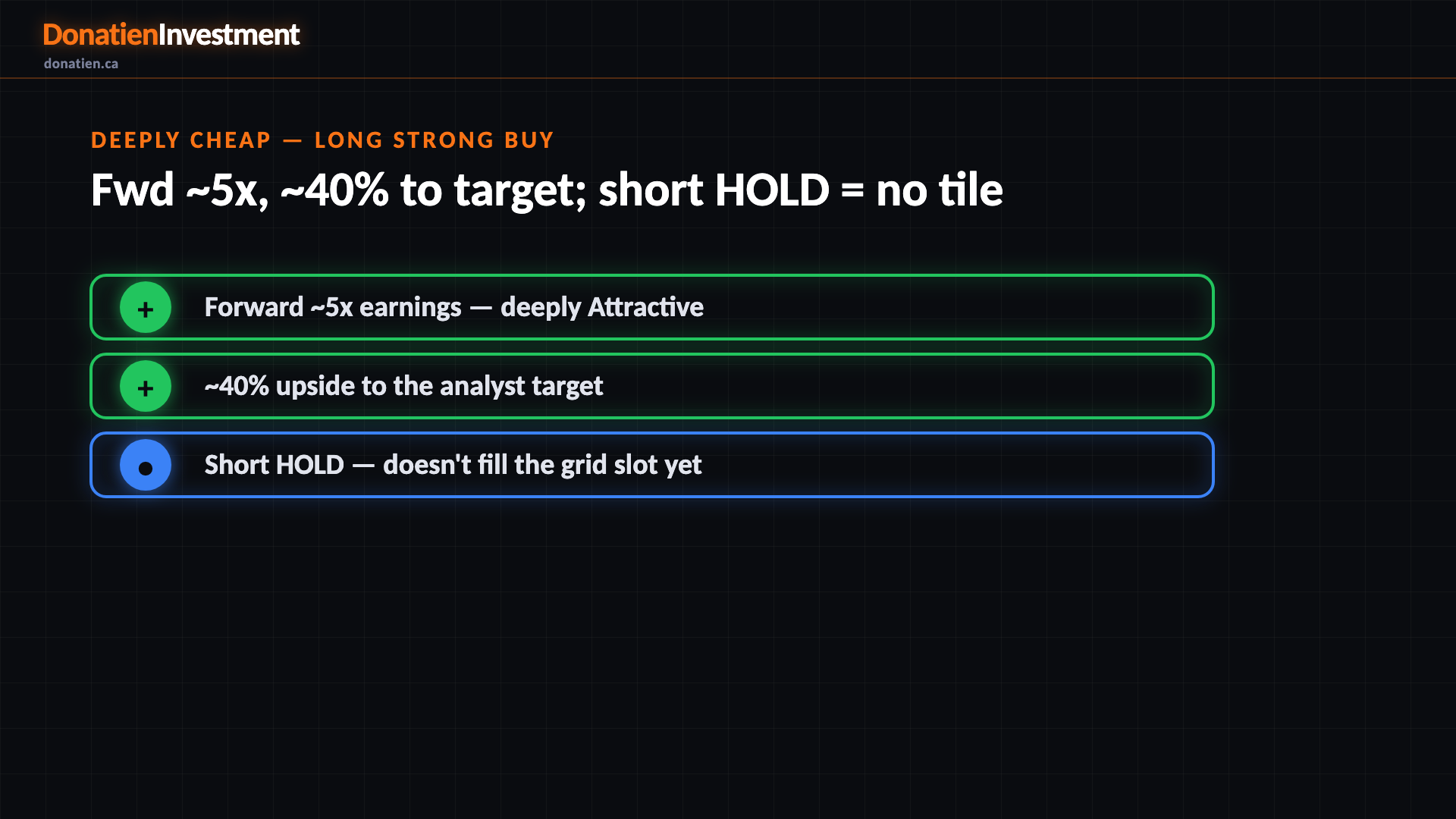

Deeply cheap — long STRONG BUY

But the value is striking even after discounting the risks: a copper producer growing output triple-digits at a forward five times earnings, with about forty per cent upside to the analyst target. Because the valuation is Attractive and copper's electrification bull is intact, the long-horizon signal is a STRONG BUY for risk-tolerant capital. Note: because the short signal is HOLD, Ero does not fill the empty Materials-Canada grid slot this cycle.

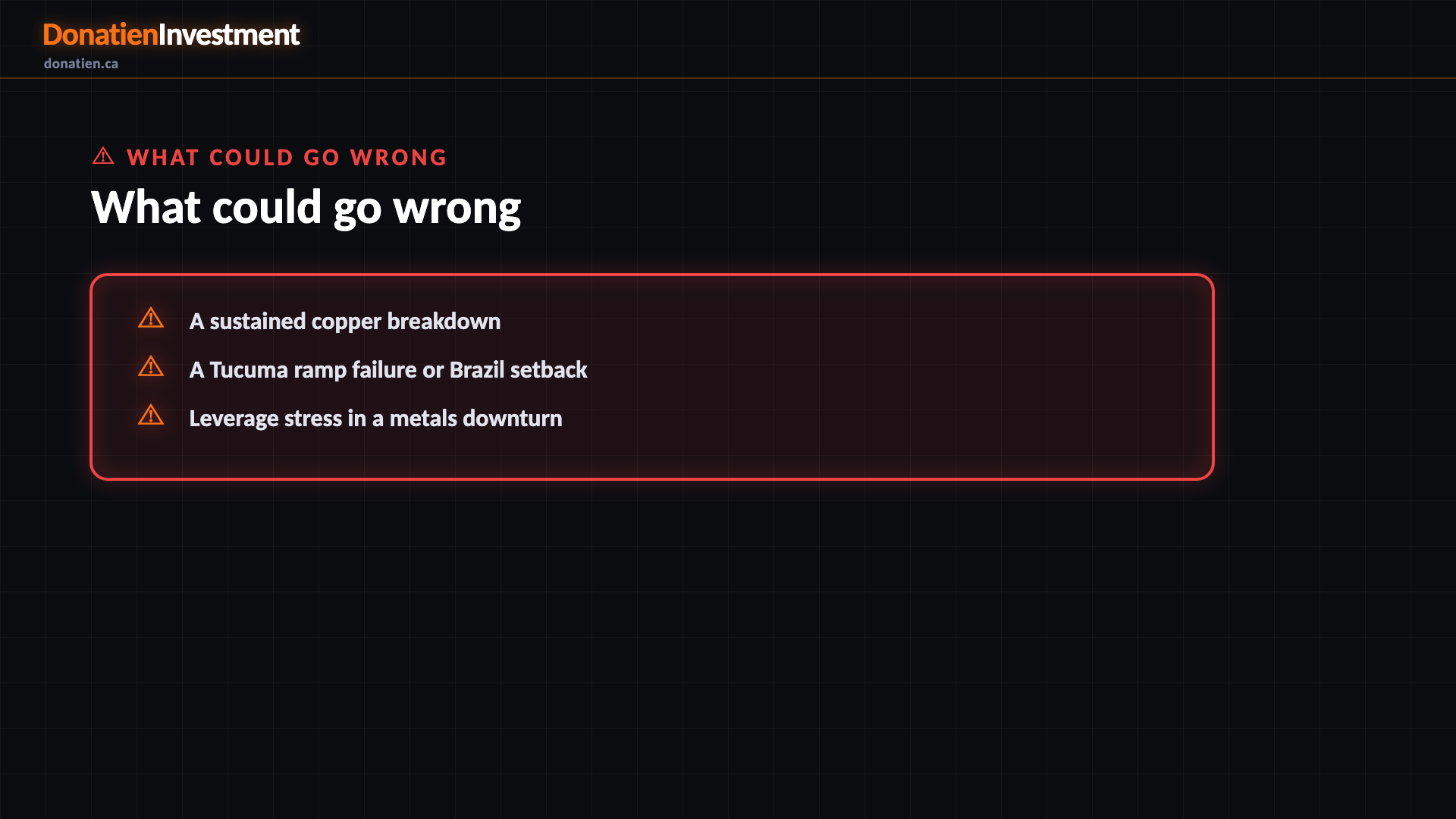

What could go wrong

A sustained copper breakdown. A Tucuma ramp failure or Brazil setback. Leverage stress in a metals downturn.

Risk vs Reward

The report weights three twelve-month paths. The base case, most likely at fifty-five per cent, sees Ero around C$45 — copper stabilises, Tucuma volumes build, and the five-times multiple normalises. The bull at twenty-five per cent reaches C$58 if copper resumes and Tucuma hits nameplate. The bear at twenty per cent falls to C$26 on a copper breakdown or a ramp stumble. Probability-weighted, about C$44, a strong positive skew — but with real leverage and small-cap risk.

The verdict

A deeply-cheap, high-growth Brazilian copper producer at forward five times earnings with a thirty-two per cent return on equity — a new watchlist add. The near-term call is HOLD on the copper sell-off and ramp risk; the long-horizon call is a STRONG BUY for risk-tolerant capital. This is not financial advice.

Read the full report on donatien.ca →{kind=link}

{kind=link}