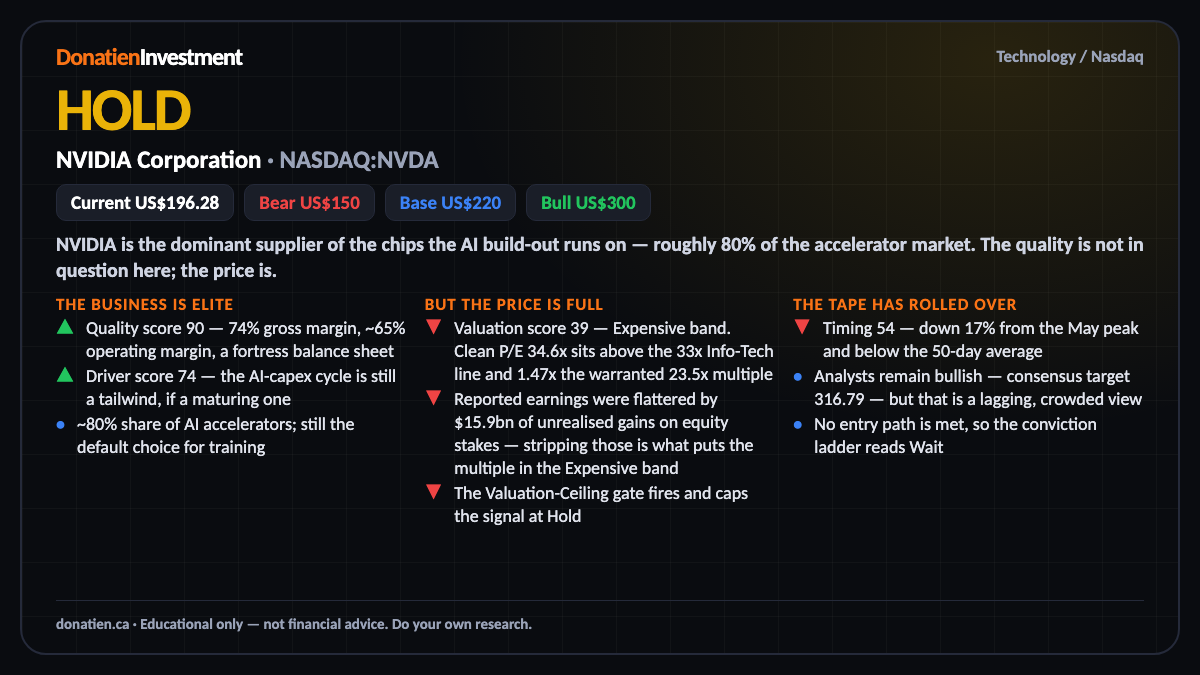

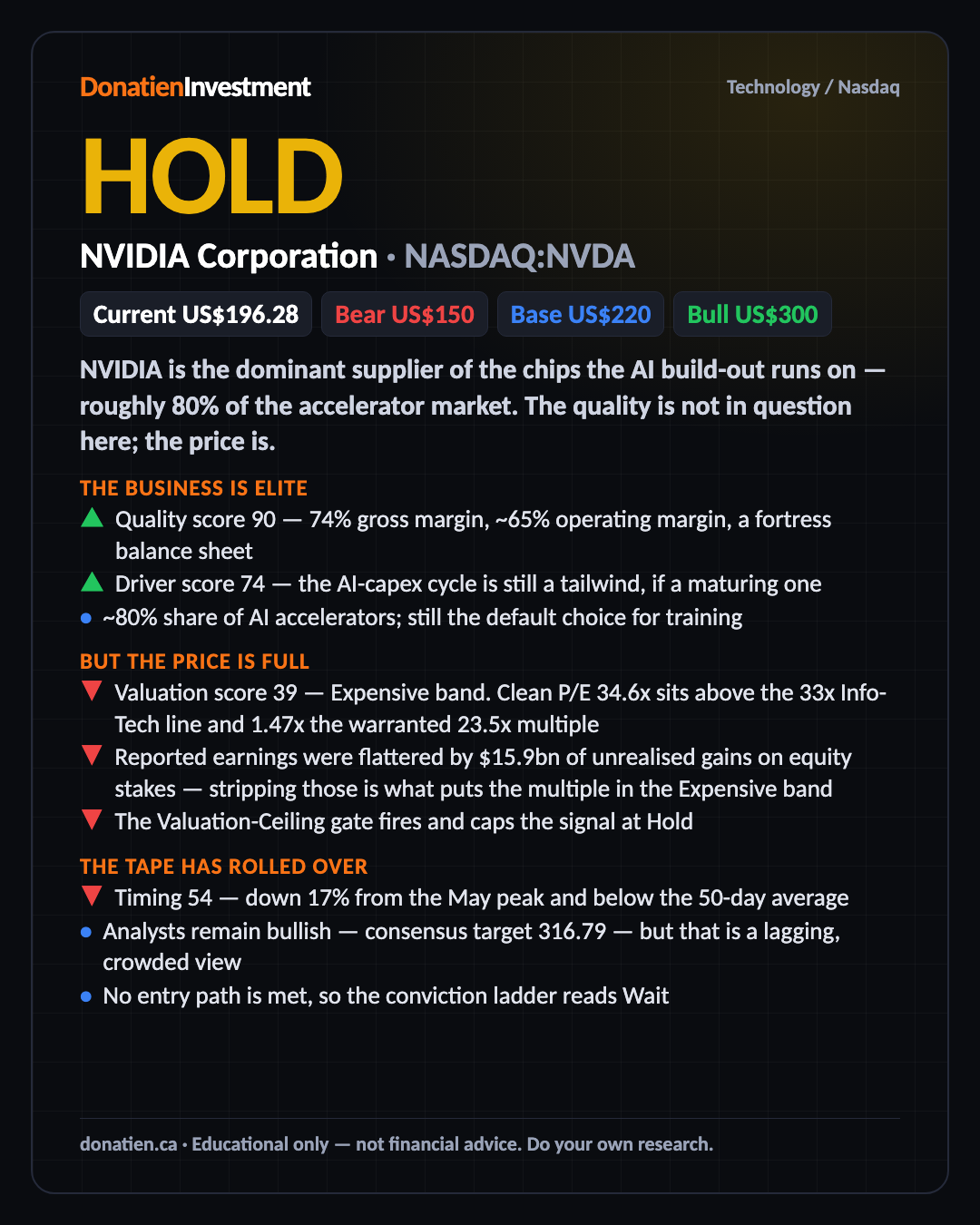

NVIDIA Corporation (NASDAQ:NVDA) HOLD

A superb business at a full price. The valuation anchor puts NVIDIA in the Expensive band, which caps the signal at Hold — not a sell, but not an entry either.

NVIDIA is the dominant supplier of the chips the AI build-out runs on — roughly 80% of the accelerator market. The quality is not in question here; the price is. At $196.28 the question is whether you are being paid to take the risk, and on our numbers you are not — yet.

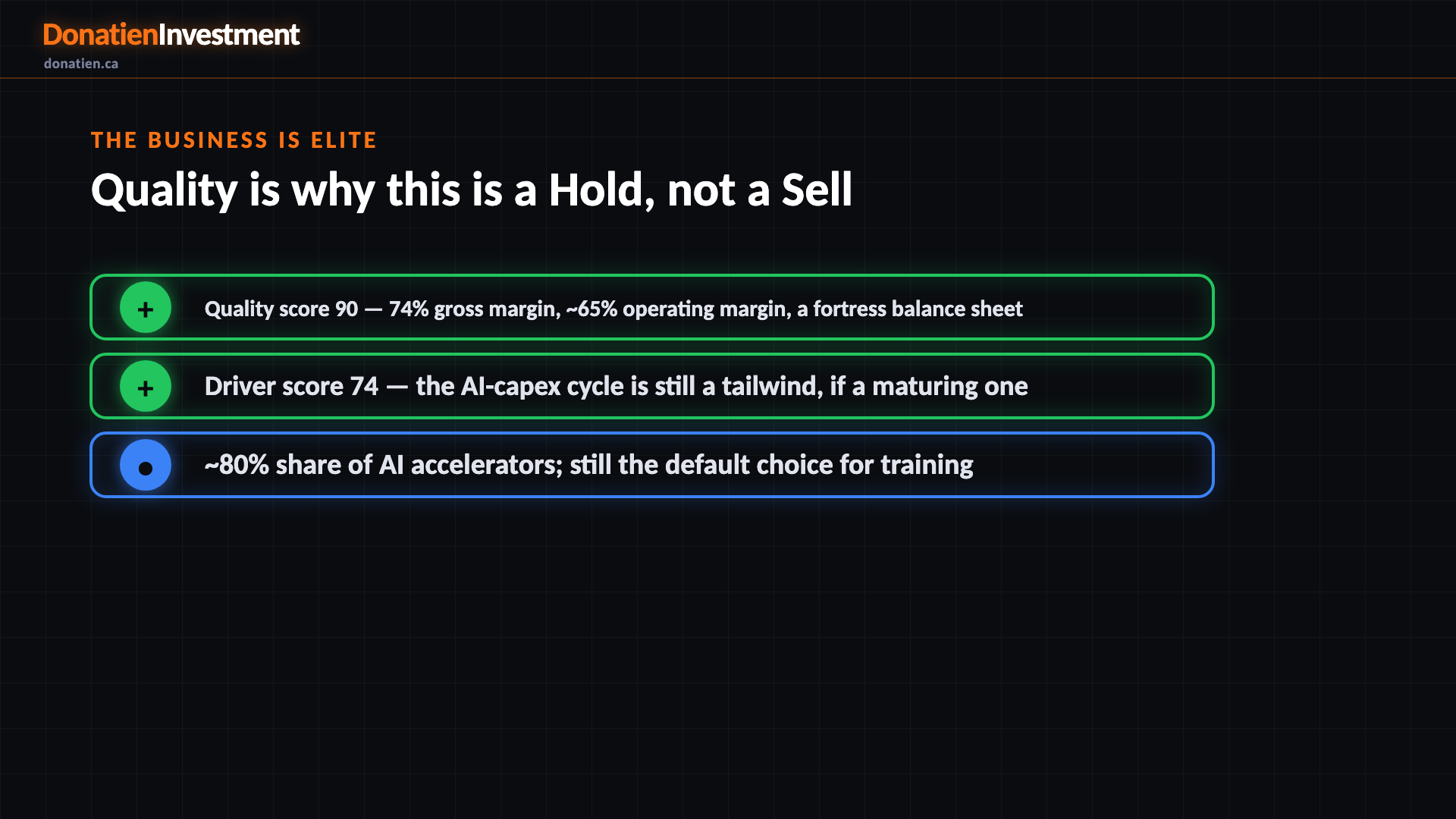

The business is elite

Start with the business, because it is why this is a hold and not a sell. NVIDIA scores 90 on quality: a 74% gross margin and a 64% operating margin, economics almost no hardware company achieves, sitting on a balance sheet with far more cash than debt. The AI build-out that drives it still scores 74, a tailwind even if a maturing one, and the company still supplies close to 80% of the world's AI accelerators. Judged on the business alone, there is very little to pick holes in.

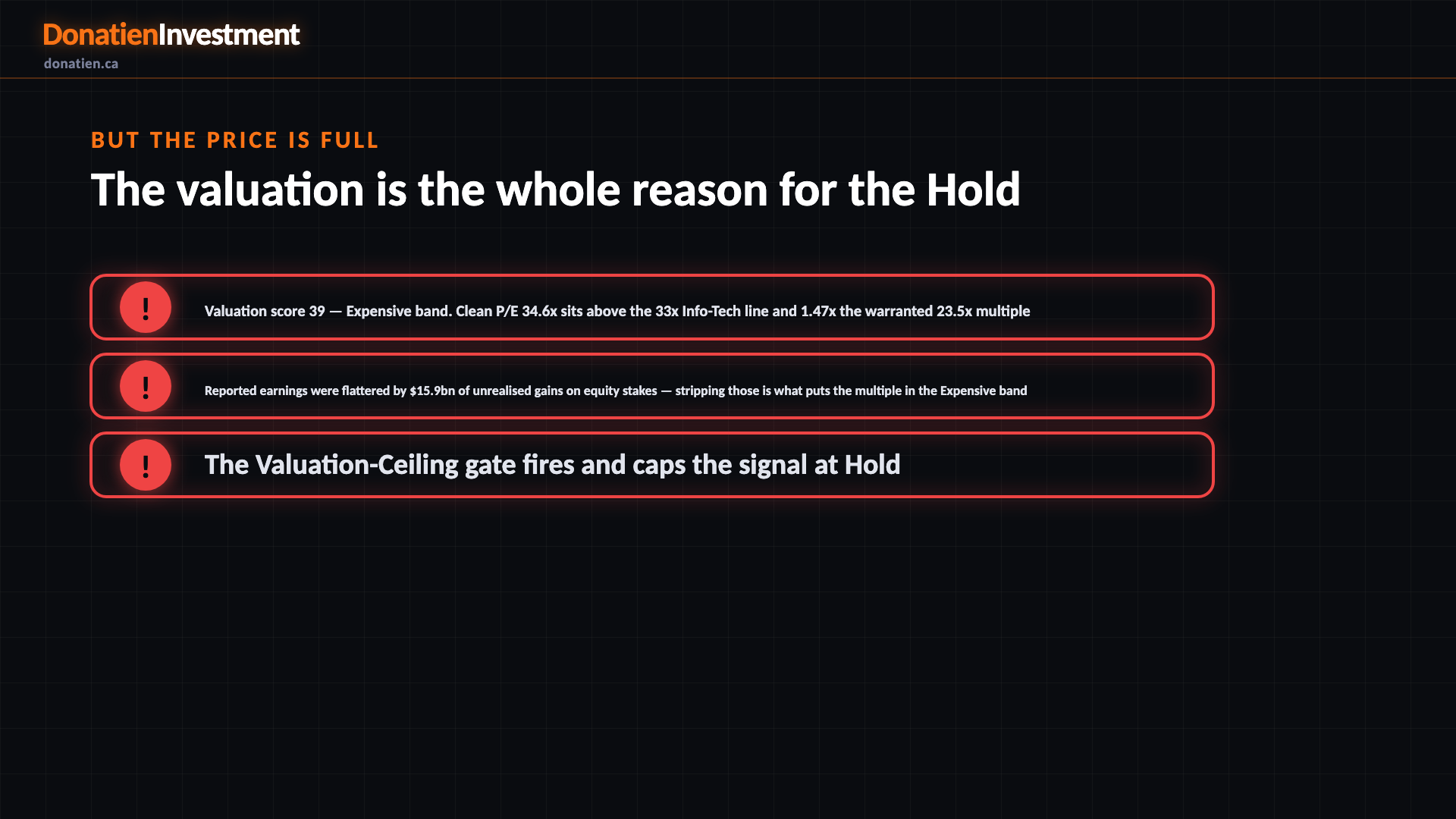

But the price is full

Here is the catch, and it is the entire reason for the hold. Valuation scores just 39, the expensive band. On clean earnings the shares change hands at about 34.6 times profit, above the 33 times we treat as rich for a chip maker, and roughly 1.47 times the multiple that growth and today's interest rates actually justify, which is 23.5 times. And clean is the operative word: reported profit was flattered by 15.9 billion dollars of paper gains on NVIDIA's stakes in other AI firms. Strip those out and the multiple looks fuller still. That trips our valuation-ceiling gate, which caps the signal at hold however good the business is.

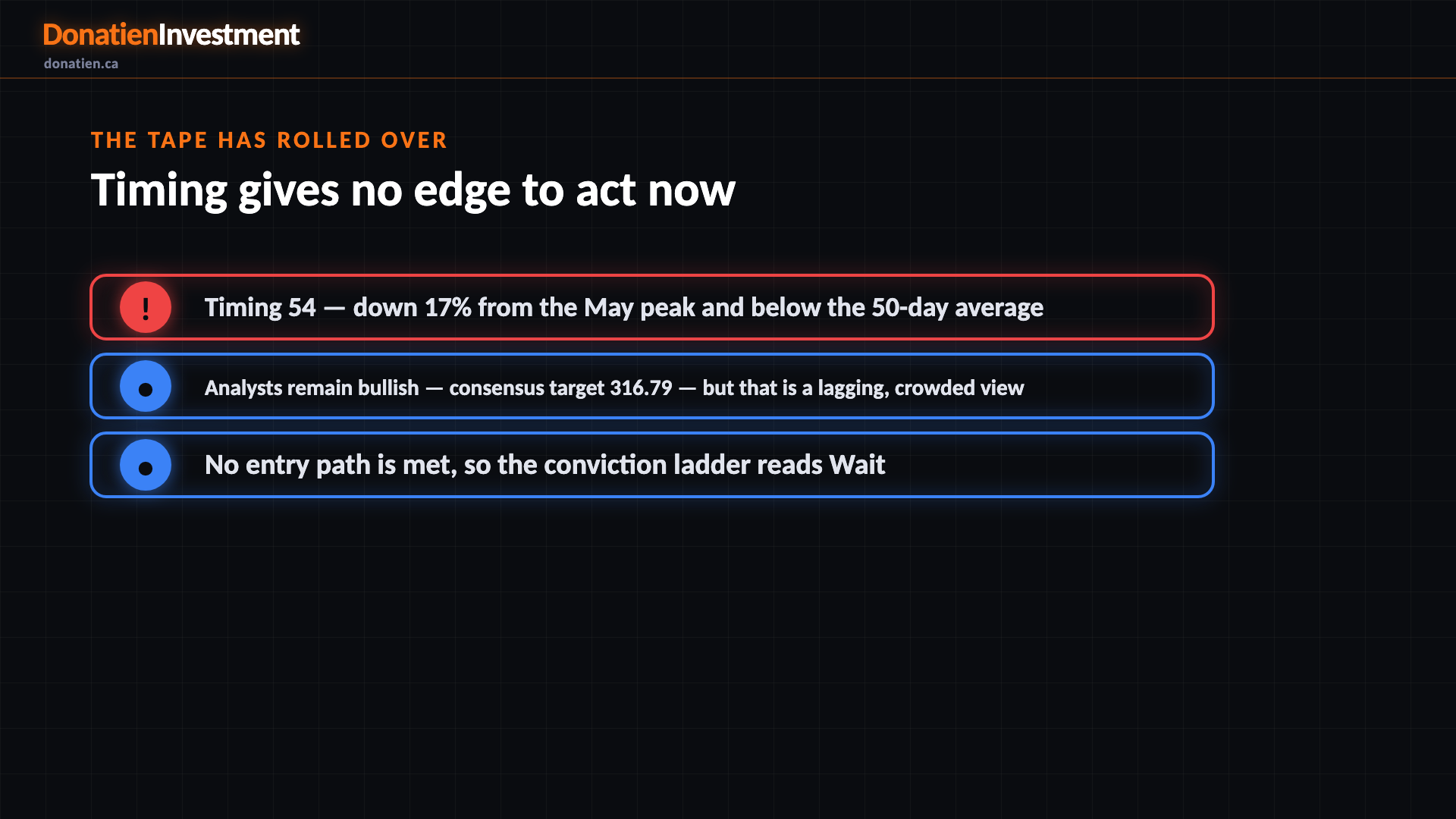

The tape has rolled over

Timing does not rescue the entry either. It scores 54: the shares are down 17% from their May peak and sit below their 50-day average, so momentum is against you right now. Wall Street is still bullish, with an average target of 316.79 dollars, but that is a crowded, backward-looking view. And on our own rules not one entry condition is met, so the conviction ladder simply reads wait. A full price into a soft tape is not where you start a position.

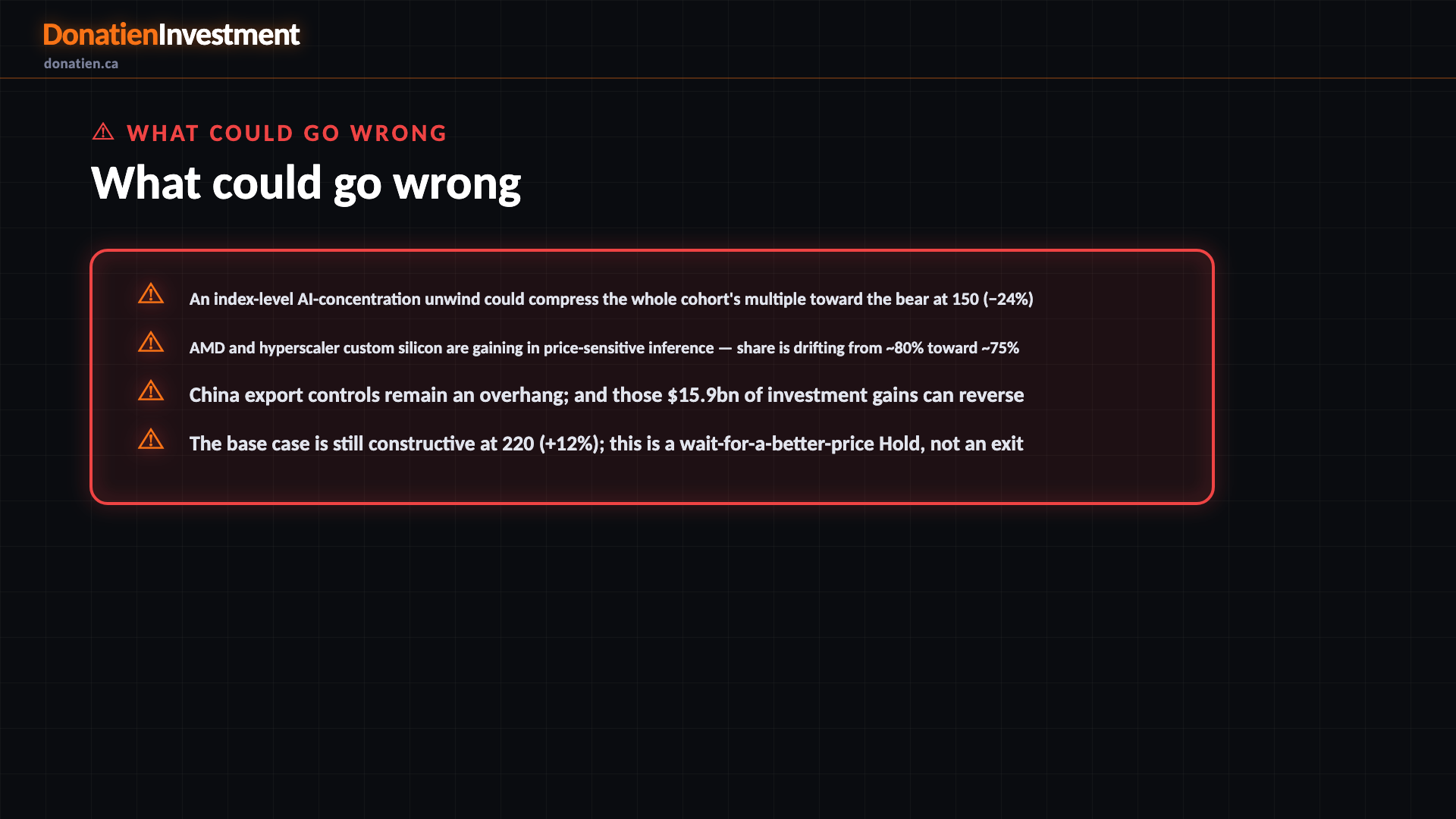

What could go wrong

An index-level AI-concentration unwind could compress the whole cohort's multiple toward the bear at 150 (−24%). AMD and hyperscaler custom silicon are gaining in price-sensitive inference — share is drifting from ~80% toward ~75%. China export controls remain an overhang; and those $15.9bn of investment gains can reverse. The base case is still constructive at 220 (+12%); this is a wait-for-a-better-price Hold, not an exit.

Risk vs Reward

The verdict

Hold. A great business is not automatically a great buy — at $196.28 you are paying a full multiple into a weakening tape and an armed concentration risk. Watch the 186–192 zone, or let earnings grow into the price.

Read the full report on donatien.ca →{kind=link}

{kind=link}