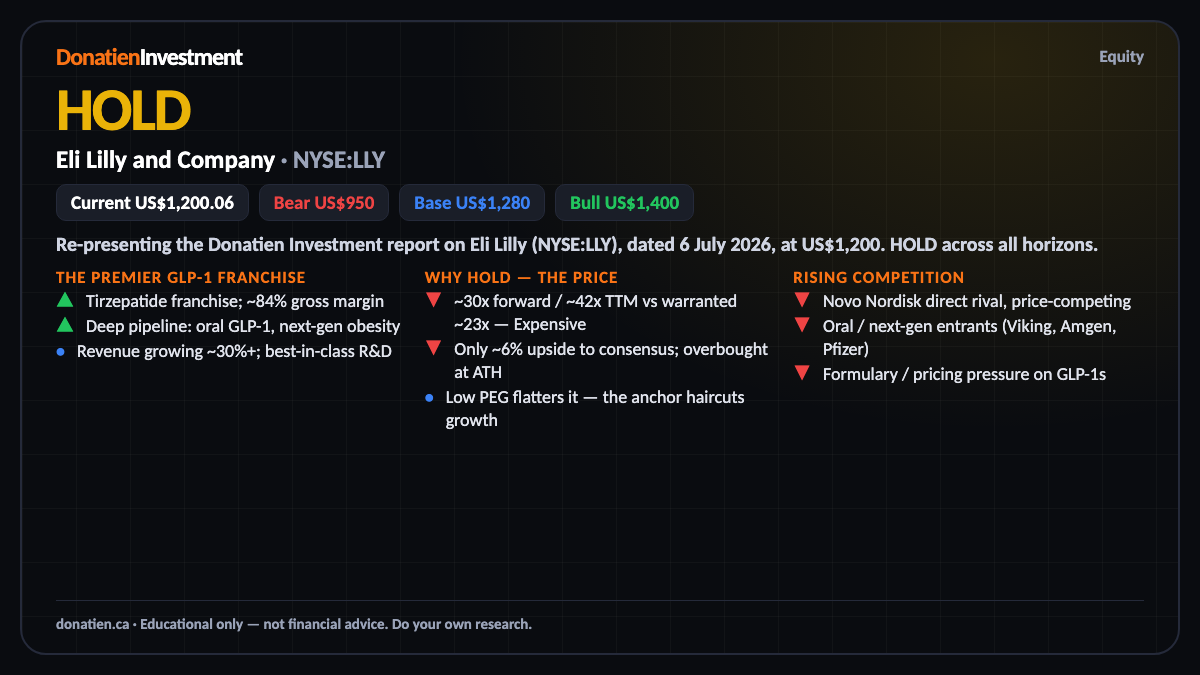

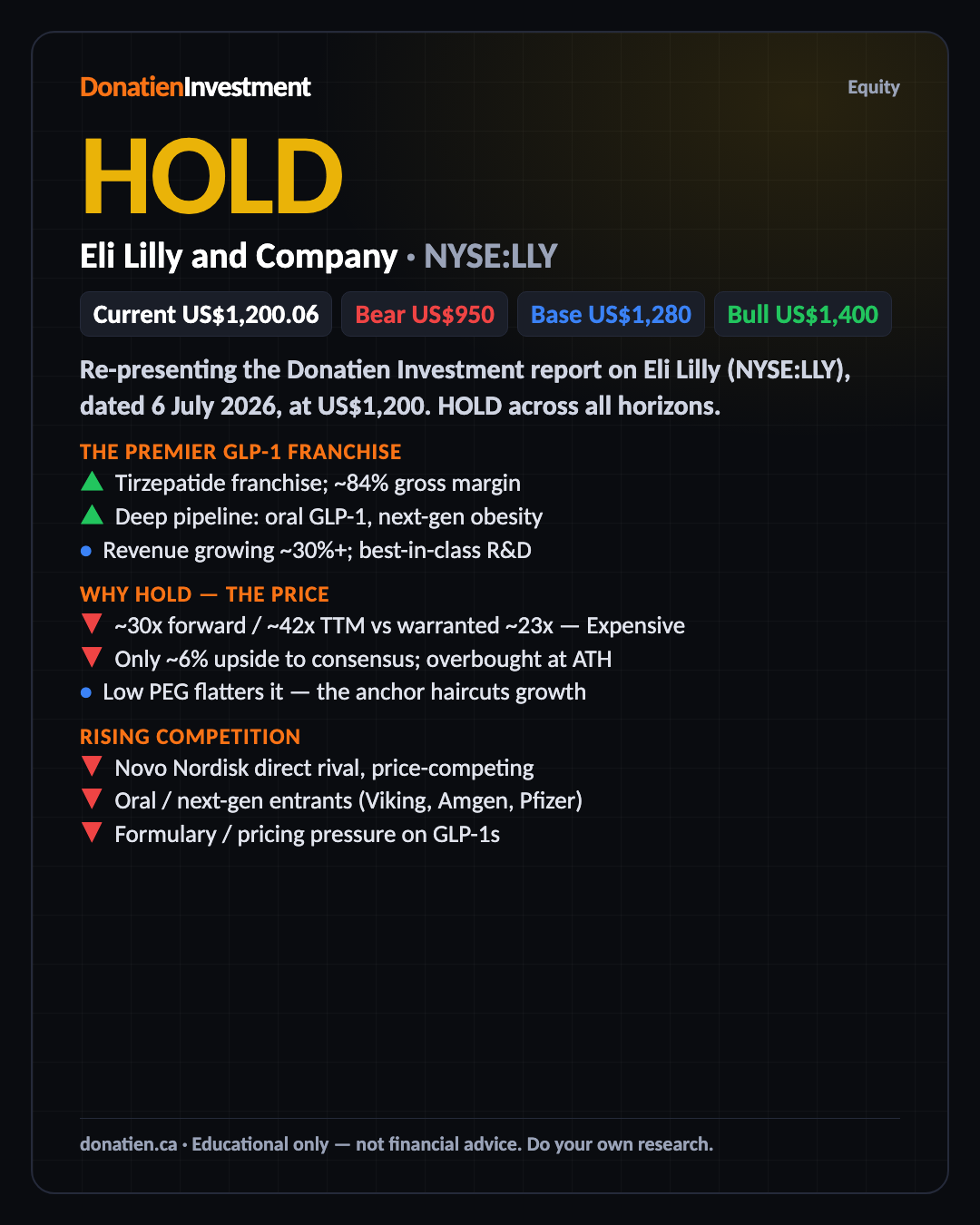

Eli Lilly and Company (NYSE:LLY) HOLD

Eli Lilly is the premier GLP-1 growth story — Mounjaro and Zepbound, elite margins, a deep pipeline. But after a nine per cent run to a fresh all-time high it trades at about thirty times forward earnings, in our Expensive band, with only about six per cent upside to consensus and an elevated competitive threat. A superb business at a rich price — HOLD.

Re-presenting the Donatien Investment report on Eli Lilly (NYSE:LLY), dated 6 July 2026, at US$1,200. HOLD across all horizons.

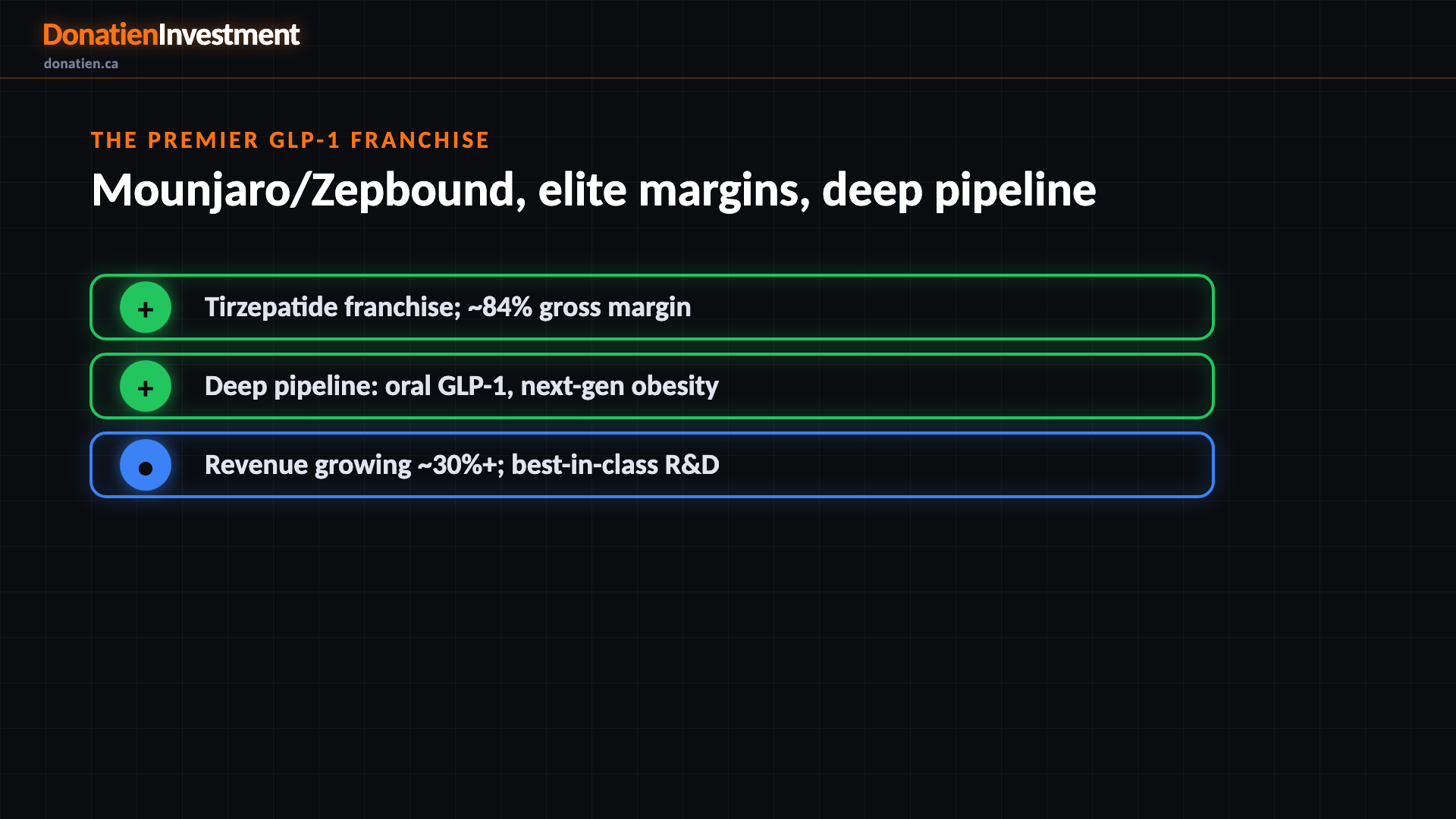

The premier GLP-1 franchise

Eli Lilly's growth is dominated by its incretin franchise — tirzepatide, sold as Mounjaro for diabetes and Zepbound for obesity — the fastest-growing drug class in history. It earns about eighty-four per cent gross margins, has a deep pipeline including an oral GLP-1 and next-generation obesity drugs, and a best-in-class research engine. It's a genuinely superb business commanding an enormous market.

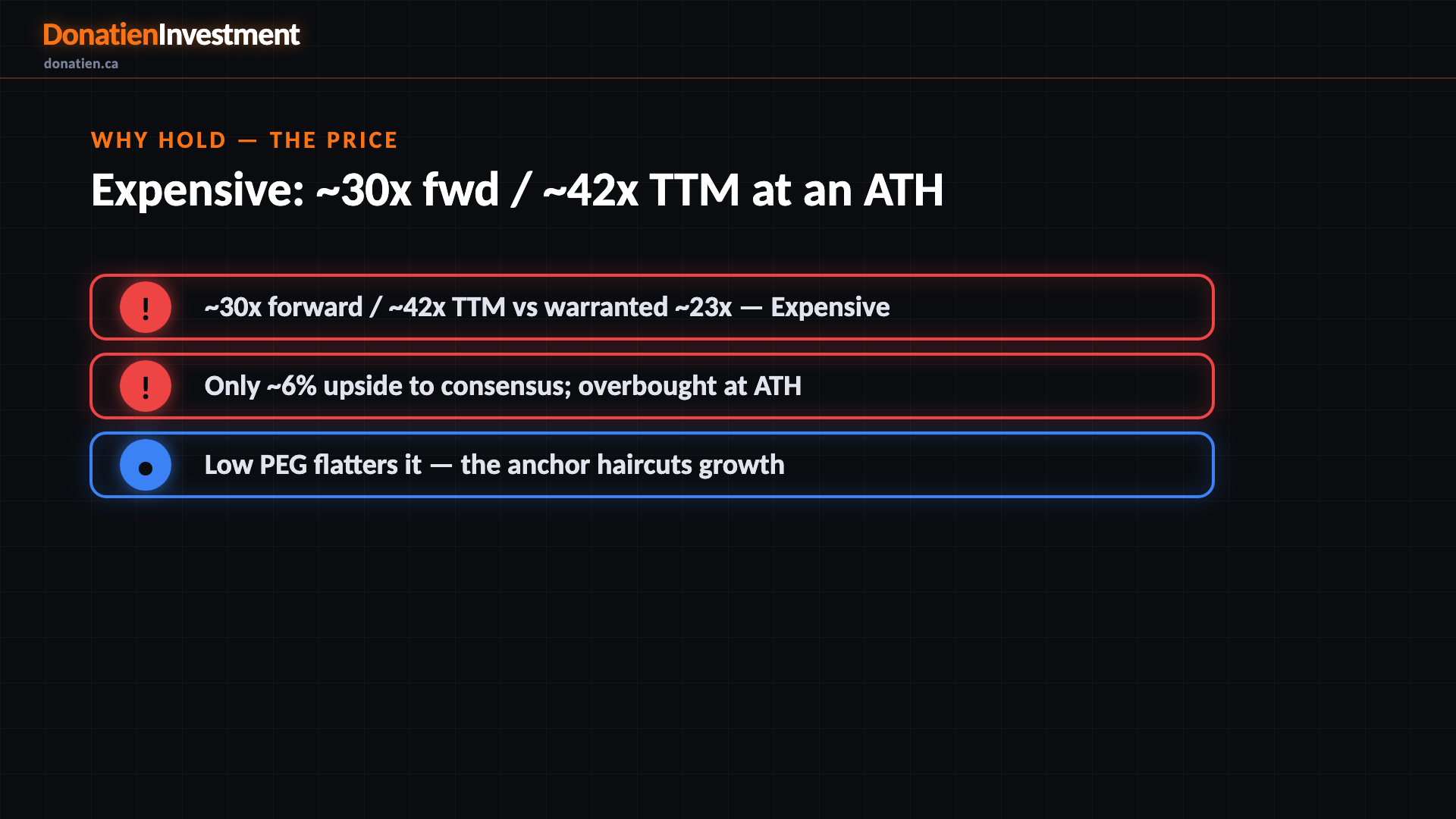

Why hold — the price

Here's what caps it. After a nine per cent run to a fresh all-time high, Lilly trades at about thirty times forward earnings — over forty times trailing — against a warranted multiple near twenty-three. That's our Expensive band, and there's only about six per cent upside to the analyst consensus, with the stock overbought. The low PEG looks cheap only if you credit the full hype-growth; our disciplined anchor deliberately does not.

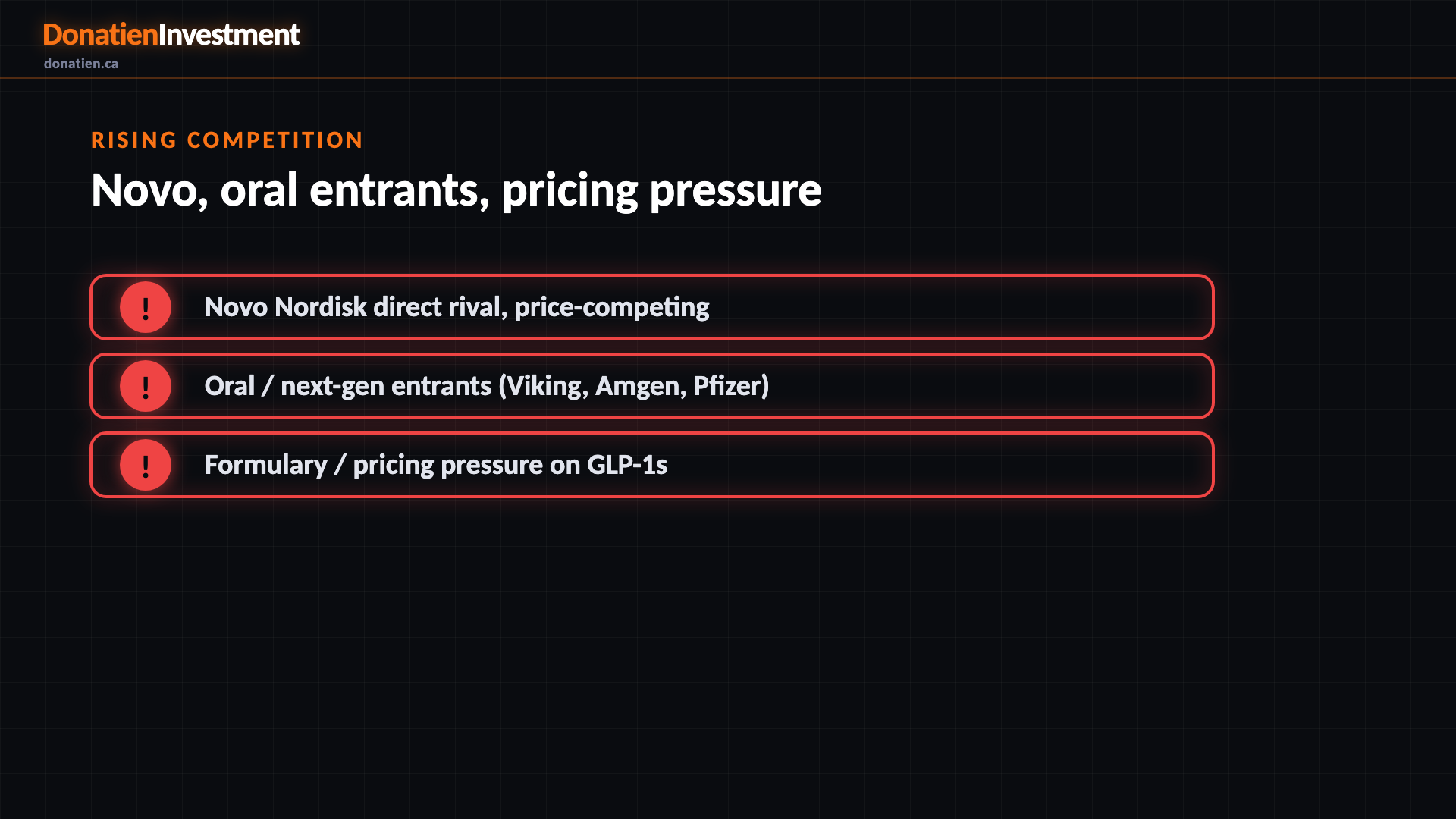

Rising competition

The competitive threat is elevated and rising. Novo Nordisk is a formidable direct rival and is price-competing; oral GLP-1s and next-generation drugs from Viking, Amgen and Pfizer could erode share and pricing; and payers and policymakers are pressuring GLP-1 prices. None of that breaks the franchise, but paired with an Expensive multiple it makes the risk-reward at this price poor.

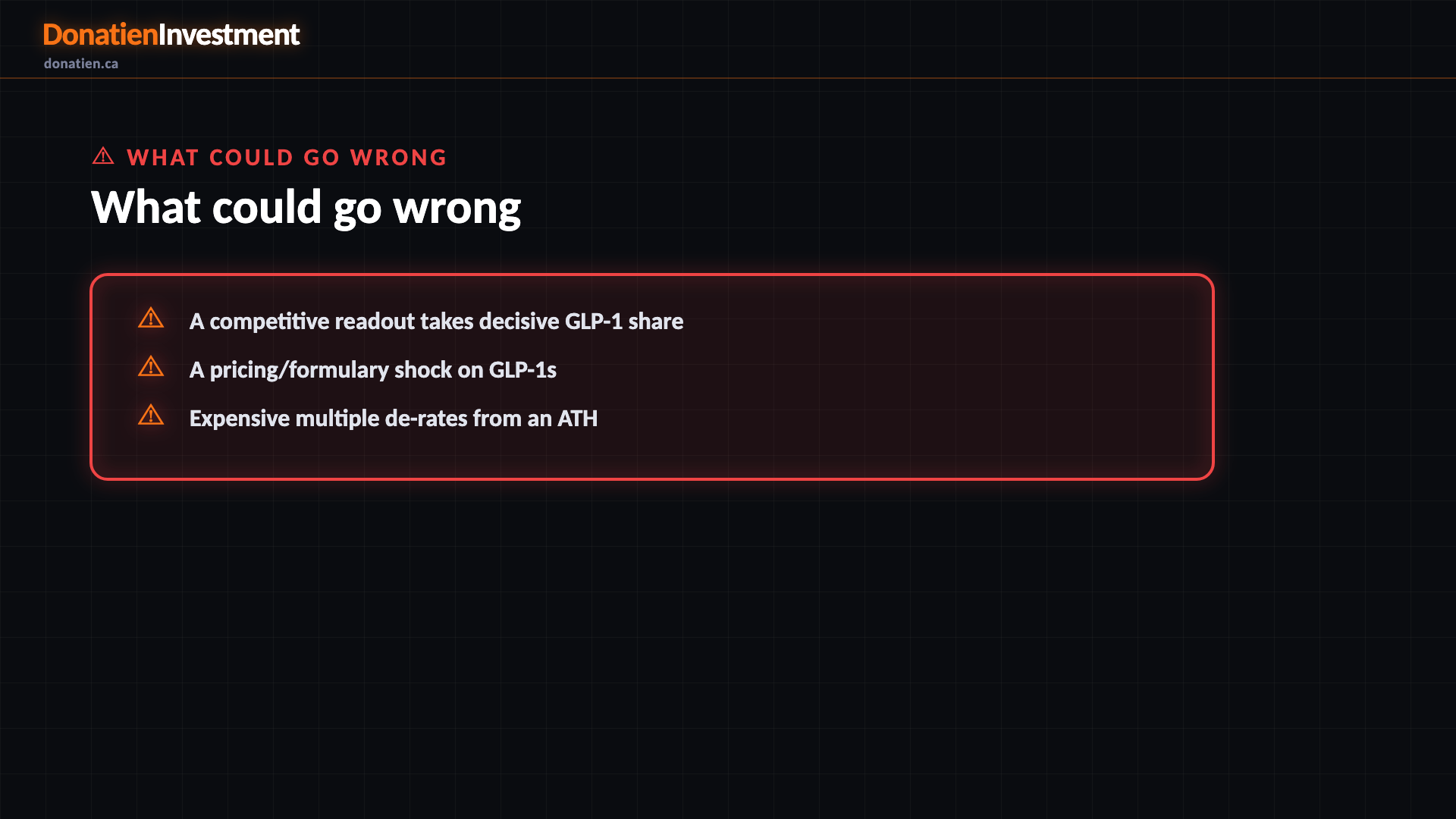

What could go wrong

A competitive readout takes decisive GLP-1 share. A pricing/formulary shock on GLP-1s. Expensive multiple de-rates from an ATH.

Risk vs Reward

The report weights three twelve-month paths that are essentially flat. The base case — most likely at 50 per cent — has Lilly around US$1,280 as strong growth is capped by a rich multiple, only about seven per cent above today. The bull at 25 per cent reaches US$1,400 if demand keeps outrunning supply and the multiple holds. The bear at 25 per cent takes it to US$950 if a competitor readout or a pricing shock de-rates the Expensive multiple toward twenty-three times.

The verdict

The bottom line: the business isn't the question — the price is. At about thirty times forward earnings at an all-time high, overbought, with only six per cent upside to consensus and an elevated competitive threat from Novo and oral entrants, the risk-reward at this price is poor. It's a HOLD. The entry edge only opens on a pullback toward support or a de-rate — not chasing a superb franchise at a rich multiple at the highs.

Read the full report on donatien.ca →{kind=link}

{kind=link}