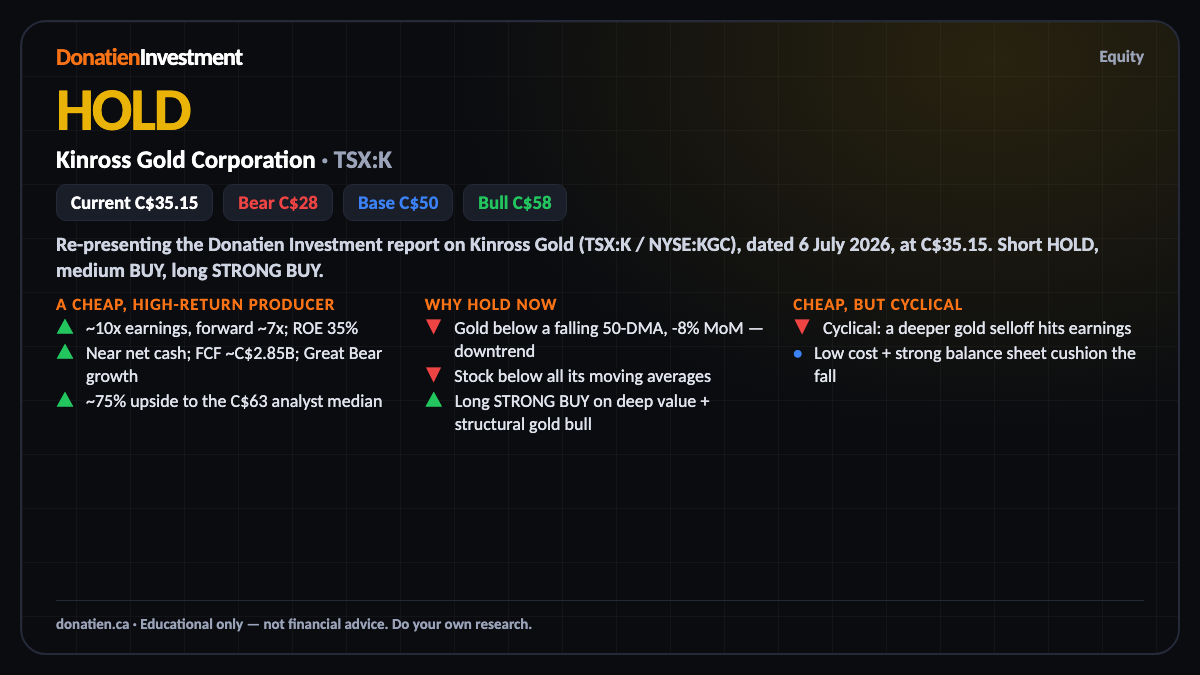

Kinross Gold Corporation (TSX:K) HOLD

Kinross is one of the cheapest high-return gold producers — about ten times earnings, a thirty-five per cent return on equity, and roughly seventy-five per cent upside to the analyst median. But gold and the stock are both in a live downtrend, so it's a hold short-term; medium term BUY, and long term STRONG BUY.

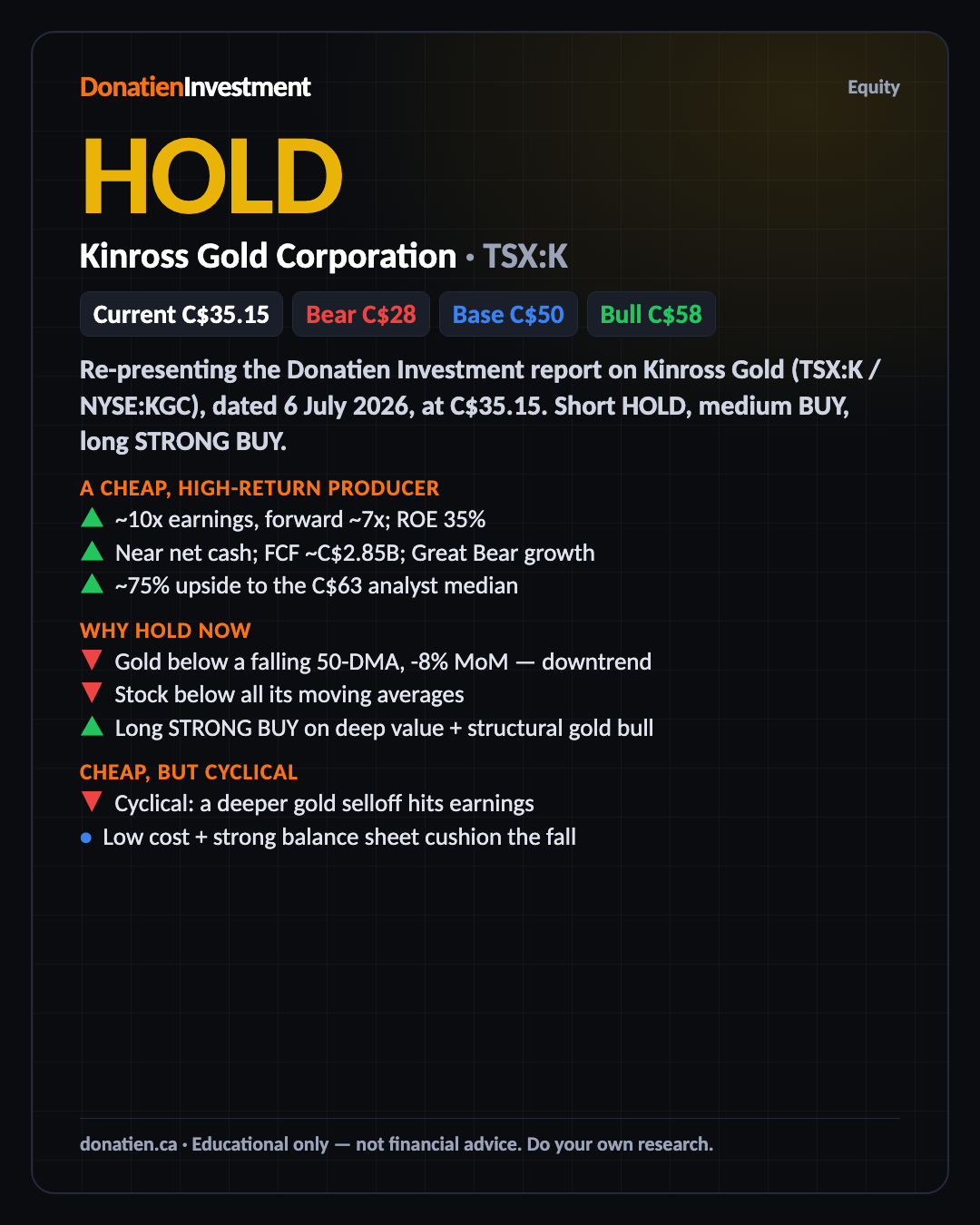

Re-presenting the Donatien Investment report on Kinross Gold (TSX:K / NYSE:KGC), dated 6 July 2026, at C$35.15. Short HOLD, medium BUY, long STRONG BUY.

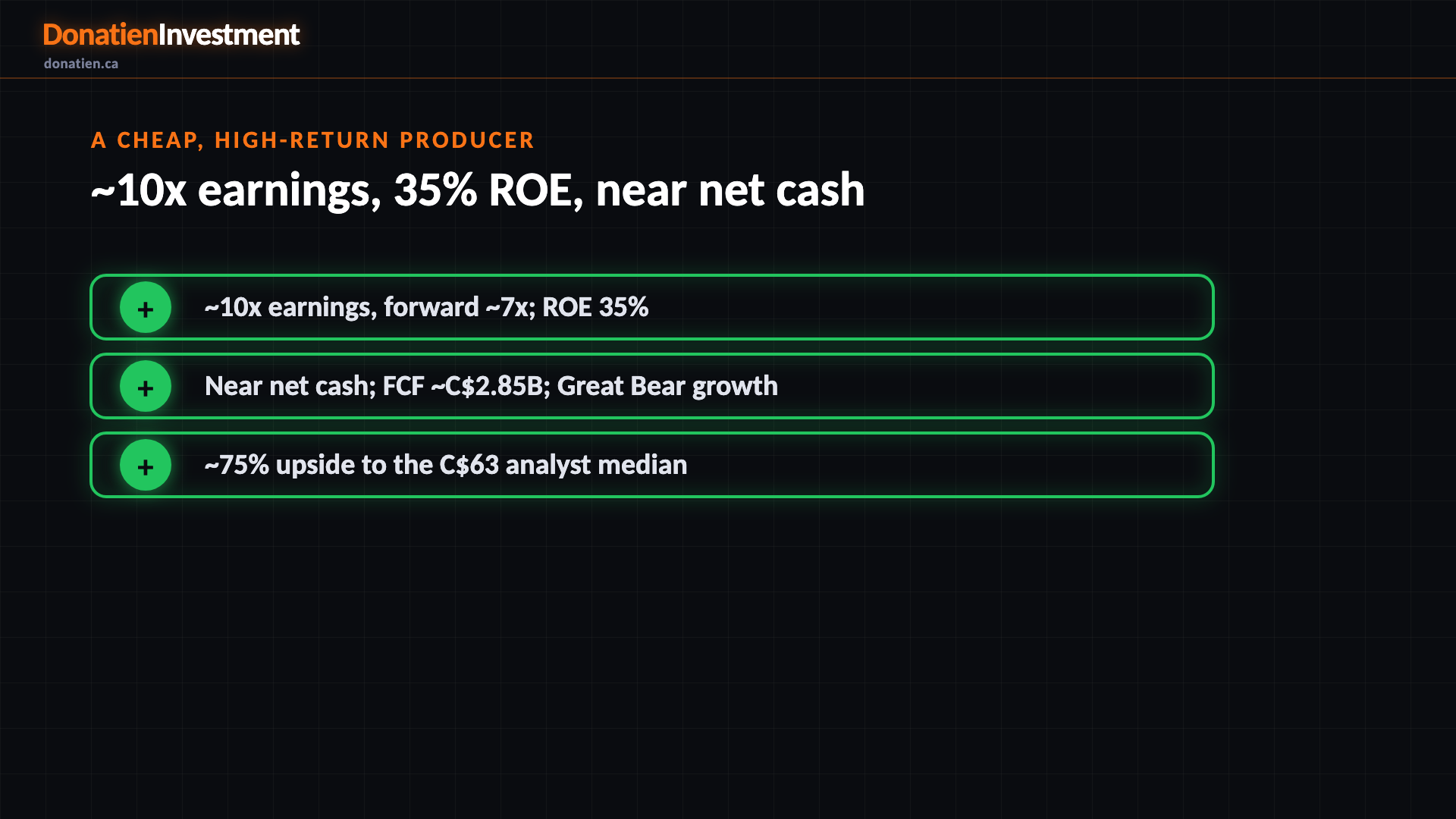

A cheap, high-return producer

Kinross is a mid-to-large gold producer with mines across the Americas and West Africa. Right now its financial profile is exceptional: a thirty-five per cent return on equity, strong free cash flow, near net cash after rapid de-leveraging, and a very low ten-times earnings multiple. It also has a real growth pipeline in Great Bear in Canada. This is one of the cheapest ways to own a high-return gold producer, with about seventy-five per cent upside to the analyst median.

Why hold now

The reason it's a hold rather than a buy today is the tape. Gold sits below a falling fifty-day average and is down about eight per cent on the month, and Kinross trades below all of its moving averages. Buying here is buying weakness. The valuation is so cheap that the long-term signal is a strong buy, but the near-term entry is best taken on a firmer gold tape or a hold of support, not chased into a falling price.

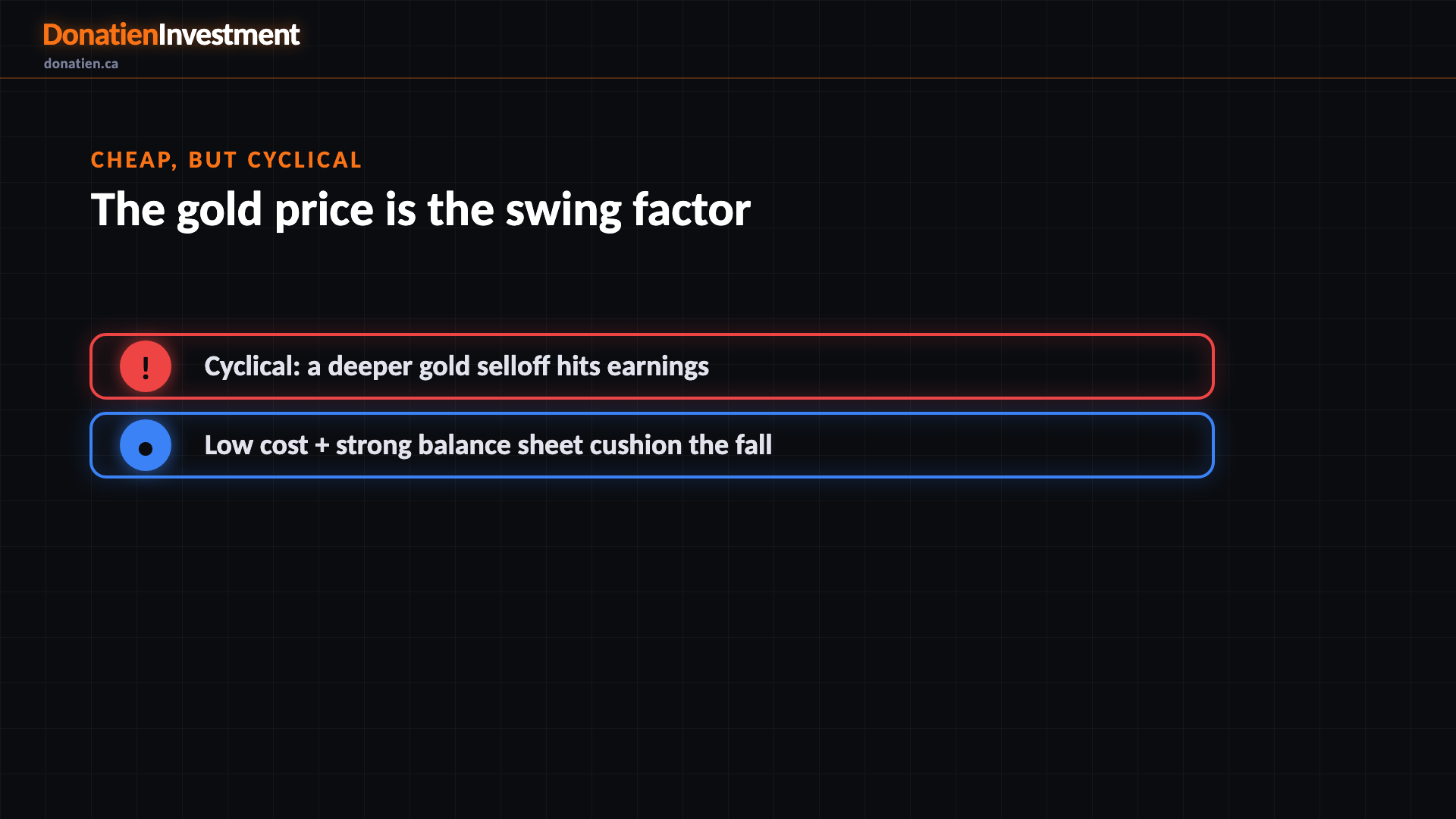

Cheap, but cyclical

Kinross is a geared bet on the direction of gold. Its low costs and strong balance sheet cushion the downside, but a deeper gold selloff would pressure earnings and the stock. The deep-value multiple and free cash flow are why the downside is cushioned rather than open-ended, and why we'd accumulate on weakness rather than sell.

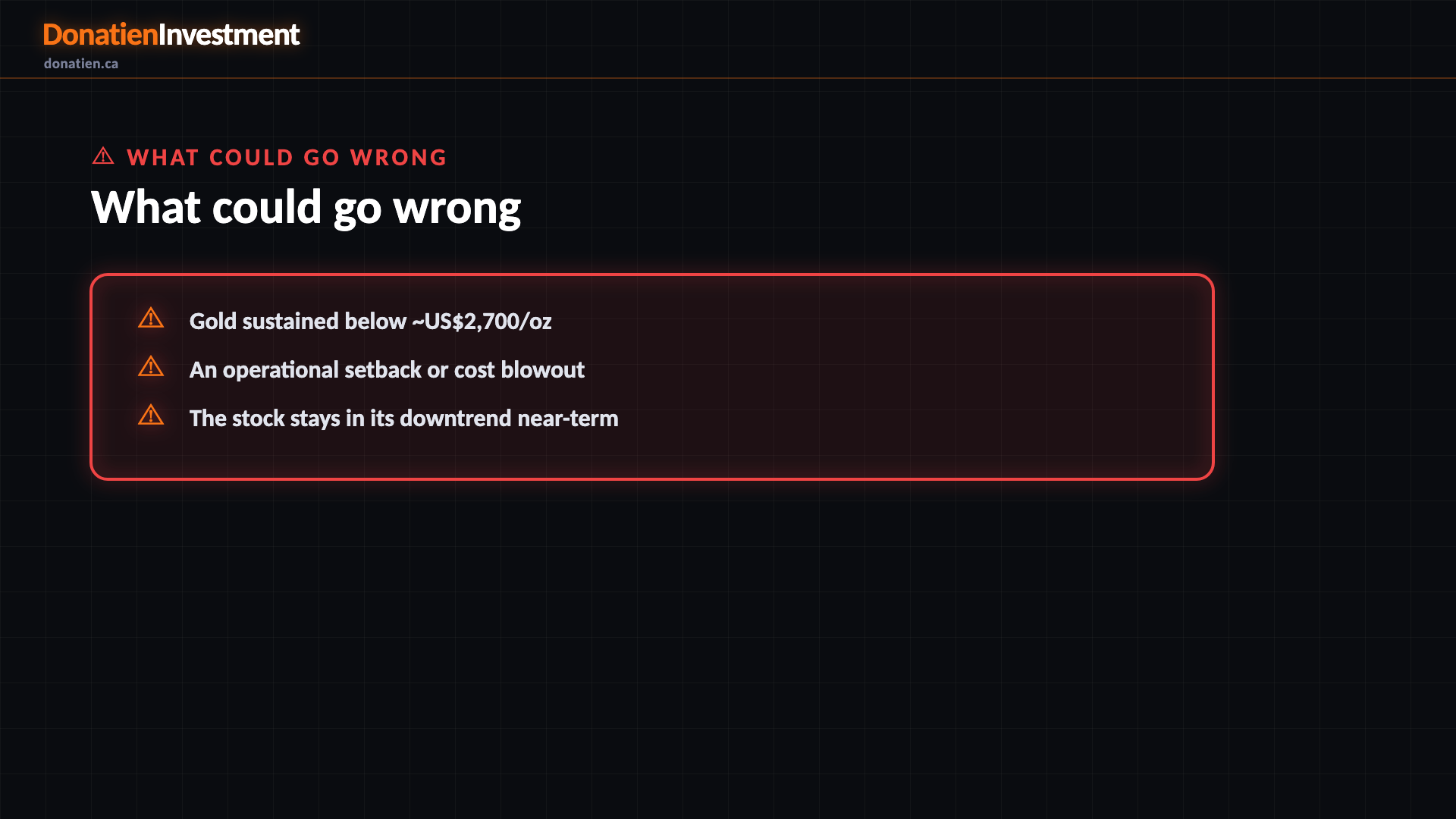

What could go wrong

Gold sustained below ~US$2,700/oz. An operational setback or cost blowout. The stock stays in its downtrend near-term.

Risk vs Reward

The report weights three twelve-month paths with a strong positive skew. The base case — most likely at 55 per cent — sees Kinross around C$50 as gold holds its range and free cash flow compounds, about 42 per cent above today. The bull at 25 per cent reaches C$58 if gold resumes its uptrend. The bear at 20 per cent takes it to C$28 on a deeper gold selloff, though the cheap multiple cushions that downside.

The verdict

The bottom line: one of the cheapest high-return gold producers, caught in a weak metals tape. Long term it rates a strong buy on deep value — ten times earnings, thirty-five per cent return on equity — and the structural gold bull; near term it's a hold. Accumulate on weakness — a firmer gold tape or a hold of the C$33 support is the trigger — rather than chasing a stock still in a downtrend. It also steps out of our Materials-Canada model grid until the short signal turns.

Read the full report on donatien.ca →{kind=link}

{kind=link}