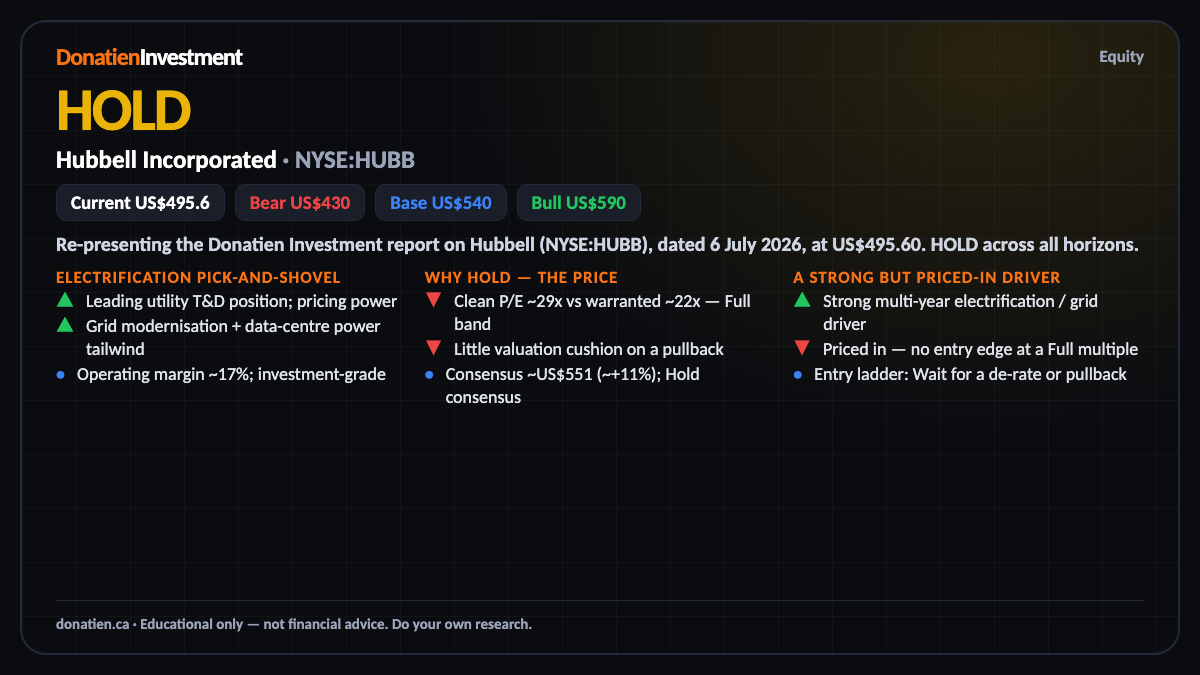

Hubbell Incorporated (NYSE:HUBB) HOLD

Hubbell is a high-quality electrical-infrastructure leader riding a strong grid-modernisation and electrification tailwind. But at about twenty-nine times earnings, against a warranted mid-twenties, it sits in our Full valuation band with little cushion — a great business at a rich price, so it's a HOLD.

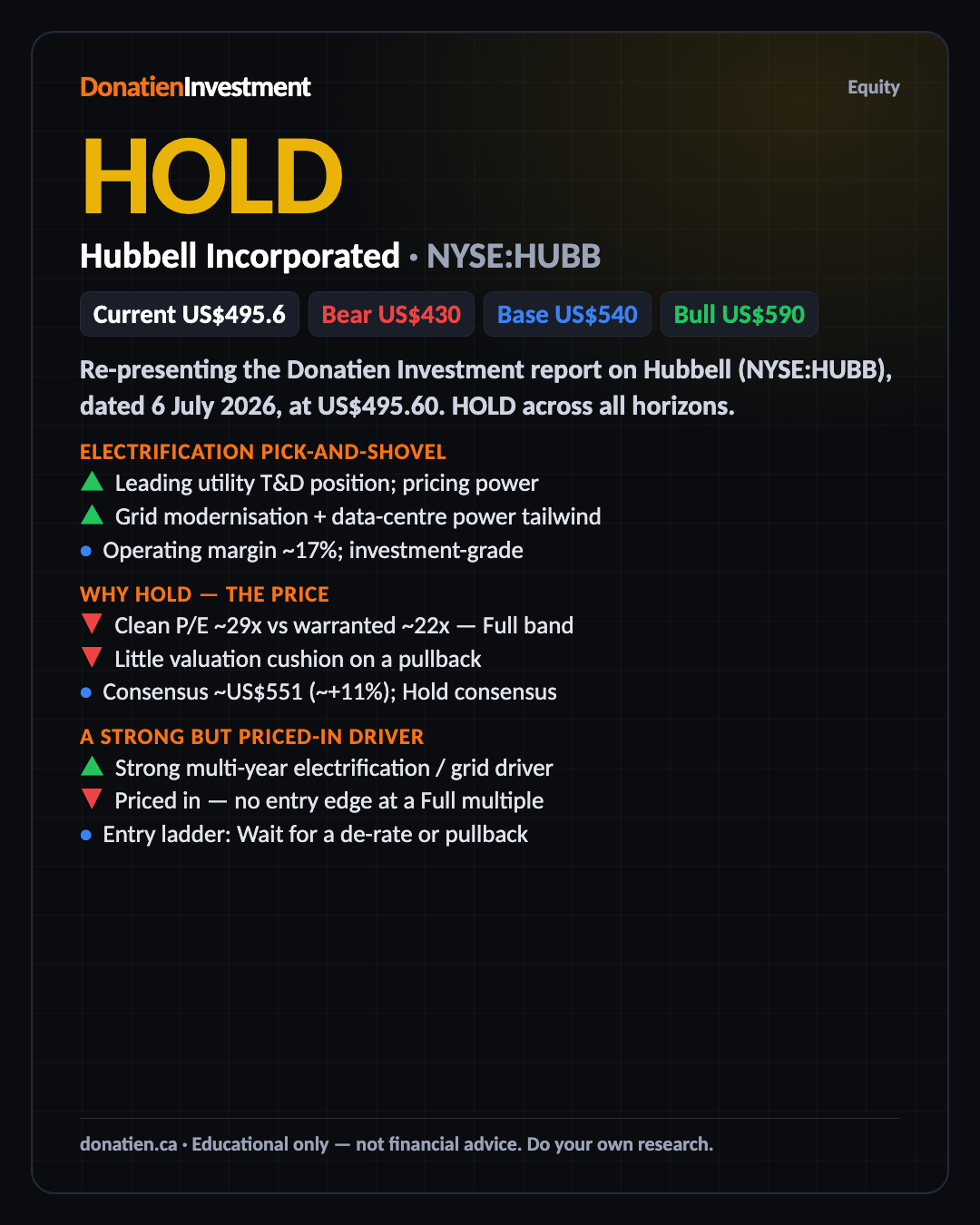

Re-presenting the Donatien Investment report on Hubbell (NYSE:HUBB), dated 6 July 2026, at US$495.60. HOLD across all horizons.

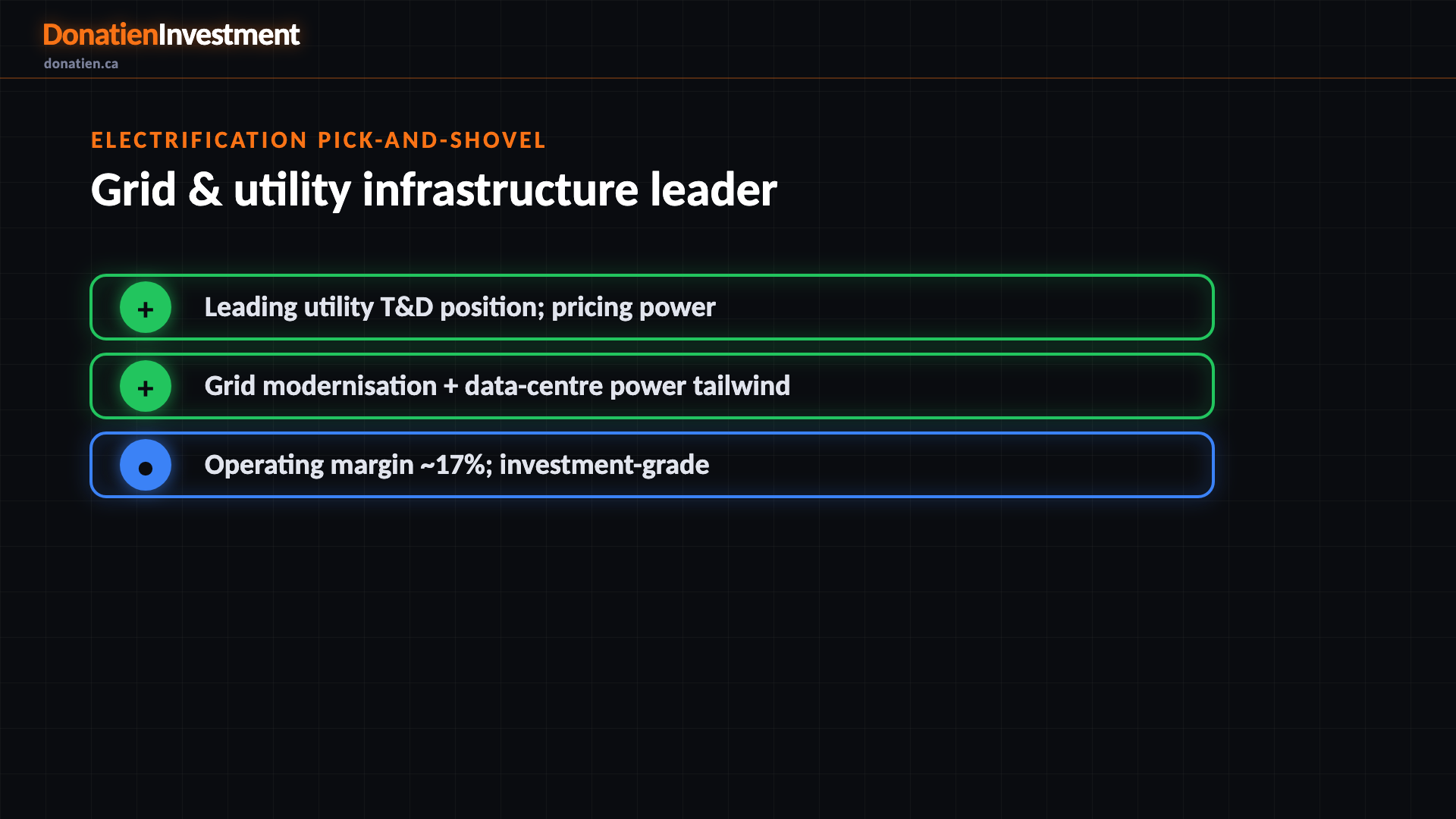

Electrification pick-and-shovel

Hubbell makes the essential hardware of electrification — grid components, transmission and distribution gear, metering and enclosures — for utilities and industry. It has pricing power in utility T-and-D, healthy margins, and a direct tailwind from grid modernisation, data-centre power and reshoring. It's a genuinely high-quality industrial compounder levered to a multi-year capex cycle.

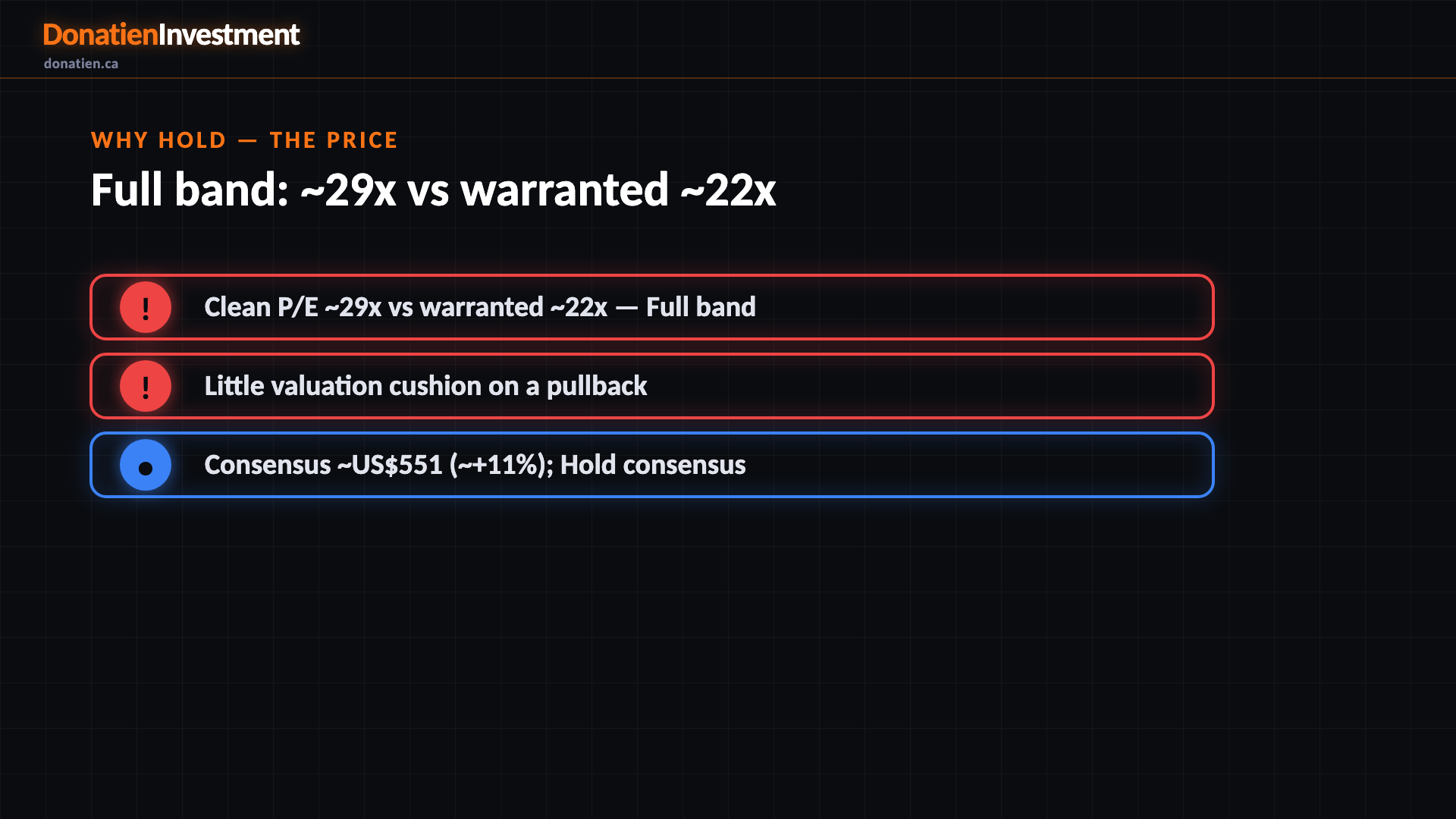

Why hold — the price

Here's the catch. At about twenty-nine times earnings against a warranted multiple near twenty-two, Hubbell sits in our Full valuation band — the recent five per cent pullback pulled it off the outright Expensive gate, but it's still rich, with little cushion if it de-rates. That's why the signal is a hold: the driver is strong, but you're paying up for it, and the Street sees only about eleven per cent upside.

A strong but priced-in driver

The electrification and grid-capex driver is one of the strongest in our coverage — a real, multi-year structural tailwind. But a strong driver can't lift a signal that's capped by a Full valuation. It's the reason to keep watching Hubbell for a better entry, not a reason to pay twenty-nine times today.

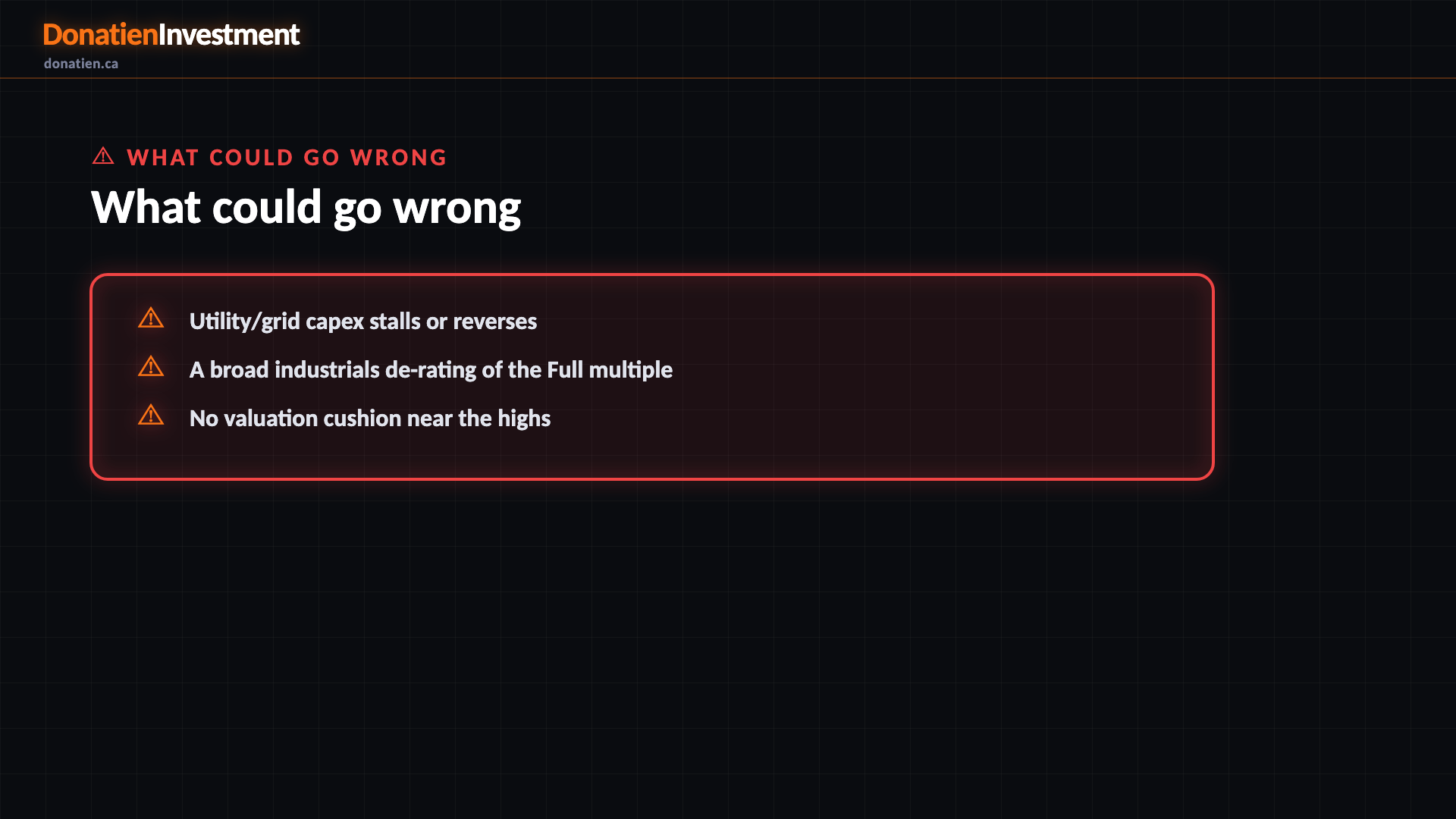

What could go wrong

Utility/grid capex stalls or reverses. A broad industrials de-rating of the Full multiple. No valuation cushion near the highs.

Risk vs Reward

The report weights three twelve-month paths. The base case — most likely at 50 per cent — sees Hubbell around US$540 on the electrification tailwind, but a rich multiple caps the re-rate, about 9 per cent above today. The bull at 25 per cent reaches US$590 if capex accelerates and the multiple holds. The bear at 25 per cent takes it to US$430 on a capex air-pocket or a de-rating back toward the low-twenties.

The verdict

The bottom line: a high-quality electrical-infrastructure leader on a genuinely strong electrification tailwind — but at about twenty-nine times earnings it's Full, with little cushion and only about eleven per cent upside to the Street. The quality isn't the question; the price is. It's a HOLD — wait for a de-rate toward the low-twenties or a pullback to support before paying up for the tailwind.

Read the full report on donatien.ca →{kind=link}

{kind=link}